Are you dividend investing in Canada? As Canadian dividend investors, my wife and I hold a combination of Canadian dividend paying stocks, US dividend paying stocks, and index ETFs in our dividend portfolio.

Through this blog, I’d like to demonstrate that it is indeed possible to achieve financial independence through a diversified portfolio consisting of dividend stocks and index ETFs.

It is our dream to one day live off dividends. When this happens, we can call ourselves financially independent. We’d also have the choice to decide whether we want to continue working full time, work part time, or retire early.

What are dividends

If you’re new to dividend growth investing, you’re probably wondering, what are dividends and why they are so attractive. When a company makes profits, there are a few ways of sharing these profits with its shareholders. The company can reinvest the money in the business, try to grow the business, and reward its shareholders by increasing the share price. The company can also share part of the profit with shareholders via a cash distribution, or a dividend.

When a company decides to share part of its profits with shareholders, the company’s board of directors determines how much of the profits are shared with the shareholders (i.e. dividend payout).

Usually, companies pay out dividends quarterly. Some companies, like REITs, and income trusts, pay out dividends every month. Some companies pay out dividends semi-annually or annually.

Companies that pay out dividends tend to be larger blue chip companies that want to reward their shareholders. Since dividends are paid out regularly, many investors, including us, plan to rely on dividends as an income stream.

As long as dividends can grow over time and keep up with the inflation rate, investors don’t need to worry about the decrease in purchase power.

For example, say a dividend paying stock is trading at $50 per share and the company pay $2 per share of dividends year. That means this dividend stock rewards its shareholders 4% ($2 divided by $50 equals 4%) dividends every year, or $0.50 every quarter. Assuming you own 100 shares of this dividend paying stock, or $5,000 worth, you would receive $50 every three months, or $200 a year.

Now, imagine if you own 10 stocks with similar payouts, you’d get 2,000 in dividend income each year. Pretty sweet right?

What makes dividends even more enticing is that as companies grow their profits each year, they tend to increase their dividend payout. Instead of getting $2 per share of dividends, the company may increase its dividend payout by 5% to $2.10 per share. This increase allows dividend investors who are living off on dividends to keep up with the inflation rate.

One very important thing to note is that dividends are not guaranteed income. The company’s board of directors can decide to reduce or eliminate dividends if the company isn’t generating enough profits or when the company is trying to conserve cash during a bear market.

Assuming dividends are safe, essentially dividend stocks reward you for being a shareholder by paying you dividends regularly. This is the key attraction for owning a stock that pays dividends.

For this reason alone, we have decided to invest in these best Canadian dividend paying stocks to ensure our dividend income is stable and can continue to grow.

The important dividend dates for dividend growth investors

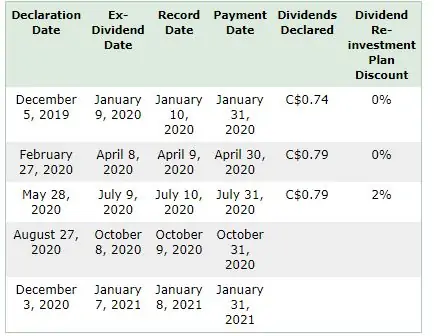

As a dividend investor, here are some of the key dividend dates you want to pay attention to:

- Dividend Announcement Date: This is the date when a company formally announces how much dividends it will pay out. Dividends must be approved by the shareholders before they can be paid.

- Ex-Dividend Date: This can also be called the ex-date. The ex-dividend date or ex-date is the date that the dividend eligibility expires. For example, if the ex-dividend date is on October 8, someone that buys the stock on October 8 or after this date won’t be eligible to receive the dividends.

- Record Date: The record date is set one day after the ex-dividend date. This date helps the company to determine which shareholders are eligible to receive a dividend.

- Payment Date: This is the date when the company issues the dividend payment. This is when the dividend cash is credited to the investor’s account.

When it comes to dividends, many people get confused on the ex-dividend date. In the picture above, when the ex-dividend date is Thursday, Oct 8, you actually need to purchase the stock before this date, not on this date to be eligible to receive dividends on Oct 31.

Why? The Securities and Exchange Commission (SEC) requires a trade to settle in two business days for a trade to settle (T+2). So when you purchase a stock, you technically don’t “own” the stock until three days later.

So, for you to be on the record as a shareholder of TD to receive the October 31 dividends, you need to be a stockholder as of October 29.

Given that it takes two business days for the trade to settle, it means you must purchase the stock on October 7 or earlier. If you are considering buying a dividend stock and counting on receive dividends for a specific payment date, make sure you purchase the dividend stock two days before the record date. I certainly made this mistake myself before.

If you want to build a portfolio that pays dividends each month, you may want to check out this Canadian Dividend Calendar I put together and pick out some of the dividend stocks on the list.

Why do companies pay dividends?

Why would a company pay dividends when it can reinvest the profits and grow? For the most part, smaller growth companies do not pay dividends because they reinvest earnings back into the company to grow and to generate more profits. These companies reward their shareholders in the way of total returns.

For a mature company with stable earnings, reinvesting 100% of its earnings back into the company may not make sense. So some mature companies issue dividends to share their profits with the shareholders.

Having said that, not all mature companies pay out dividends. For example, some mature companies like Berkshire Hathaway (BRK.A & BRK.B) and Amazon (AMZN) do not pay out dividends.

So why do companies pay dividends? Because by paying dividends, the company sends the message that the Board of Directors believes in the company’s future prospects and performance. In other words, paying dividends sends a clear message to investors that the company is financially sound.

Paying dividends can attract a certain type of investors (like us), who value dividend distributions rather than waiting for capital gains.

Why dividends?

Why dividend investing in Canada? Because dividend income is very tax-efficient in Canada, especially when are living off dividends, and we don’t have any earned income from full-time or part-time work.

If you take a look at our dividend portfolio below, you’ll notice that we invest in both dividend-paying stocks and index ETFs.

We like dividends because of the following simple reasons:

- Our portfolio is working hard for me to generate income so we don’t have to. This is truly passive.

- Dividends are tangible. We can cash deposited in our accounts whenever a company pays dividends.

- We plan to live off dividends, so we don’t have to touch our principles as we plan to pass down our dividend portfolio to future generations and create a long-lasting legacy.

- Before reaching financial independence, we plan to reinvest all the dividends by enrolling in dividend reinvestment plans (DRIP) or reinvest dividends.

- By buying dividend stocks, I am essentially creating my own index fund. The dividend income, therefore, is safer and predictable.

- Canadian dividends are very tax efficient. In fact, by having some good strategies, you can pay almost no tax.

- Dividends allow me to sleep well at night even when the stock market is very volatile.

After many years of investing in dividend-paying stocks and earning dividends, our dividend income can already cover some basic monthly expenses like groceries, car insurance, house insurance, property tax, utilities, term-life insurance, cell phone & internet, and car fuel.

As we continue to invest a significant amount of cash each year, I believe that living off dividends when we are in our 40s will be possible.

Financial Independence

What do I mean by achieving financial independence via dividend and ETF investing?

Simple. Our goal is to earn sufficient dividends to cover our annual expenses. When this happens we can call ourselves financially independent and live off dividends without having to touch the principles. Who knows, maybe we can eventually pass our dividend portfolio to our kids and their kids too!

In case you’re curious about financial independence, here are some articles you can check out:

- What is financial independence?

- The financial independence journey – where do we go from here?

- Financially independent…but we choose not to be

- Why I practice financial independence…and why you should too

- What rock climbing has taught me about financial independence

When we are living off dividends, for the first few years we probably will continue working either full time or part time to build up some buffers to give us some safety. Eventually, we may decide to retire early and work on our hobbies, volunteer our time, or even travel around the world.

The key thing here is that once we are financially independent, we are empowered to decide our own schedule, rather than having to rely on the employment paycheque every two weeks.

Dividend Income

After reading tons of information, you’re probably really curious about how much dividends we have received over the years. I started dividend investing in 2007 by accident. We then got really serious with dividend growth investing and dividends in 2011.

The jump in dividend income between 2011 and 2012 was a result of investing a significant amount of cash into our dividend portfolio.

When it comes to growing our dividend income, we have been relying on three different key drivers:

- Purchase more dividend-paying stocks with new capital

- Organic dividend growth

- Reinvest dividends via dividend reinvestment plan and wait for dividends to accumulate to a big amount and purchase more dividend-paying stocks (see #1).

For now, the key driver for our dividend growth comes from the injection of new cash but it doesn’t mean we ignore points 2 and 3. Therefore, we are enrolled in DRIP whenever we are eligible.

For the dividend amount that does not get reinvested via DRIP right away, we wait till the amount is over $1,000 before reinvesting. We are doing this to keep the trading commission as a small percentage of the overall transaction cost.

You can see our complete dividend history here.

How much dividends do we need?

Just how much money does our dividend portfolio need to generate before it can cover all of our expenses and we can call ourselves financially independent?

Although our dividend income already covers a bulk of our expenses, you’re probably wondering just how much dividends we need to be financially independent. Do we need $40,000 in dividend income? Do we need $60,000 in dividend income? Or do we need more than $80,000 in dividend income?

Because dividends can be very tax-efficient, based on our annual expenses in the past few years (in 2019 we spent $54,906.02) and some financial independence assumptions, we think we need somewhere around $50,000 and $60,000 in dividend income to cover our expenses.

To be on the safe side, I think if our dividend income can generate $60,000 per year, we’d be able to live quite comfortably. If our dividend portfolio can generate more than $60,000 a year, that’s even better and would give us even more margin of safety.

To generate $60,000 a year of dividends, we anticipate we need about a $1.5 million portfolio (market value). Given stock price appreciation dividend growth, and that we’re investing money over time, the actual amount of money invested should hopefully be less than $1.6 million.

And please note, I am not including Canadian government benefits like the Canadian Pension Plan (CPP) and Old Age Security (OAS) in the calculation. I simply see CCP and OAS as the extra gravy (or income) that we may get once we are 65 or older. We also plan to defer the Canadian government benefits to maximize these payment benefits.

Getting started with dividend investing

Back in 2011, I was taking in a wide variety of investing strategies from sources all over the internet, and I was really attracted to the simplicity of the approach that Canadian dividend stock investors like Million Dollar Journey were taking to planning their financial independence.

Prior to that point, I had purchased a couple of dividend stocks almost by accident, just because I thought they were good companies in general (I wasn’t yet aware of the finer points of valuation, P/E ratios, dividend growth records, or anything like that).

But seeing how many Canadian authors were living simple satisfying lives in retirement or semi-retirement thanks to the dividend income that their portfolios spun off each year, was inspiring. The math behind it didn’t seem that difficult to grasp, and so I was off to the dividend income races.

I also began reading books like The Lazy Investor, and Common Stocks and Uncommon Profits, and my wife and I subsequently became very interested in holding dividend paying stocks. We like the idea of becoming a shareholder of a company that produces products that we’d use on a daily basis. We also like the idea of getting paid regularly via dividends for owning these companies.

Since getting very serious with dividend investing and dividend income in 2011, I have read many invested related books. I have listed some recommended books here.

You can also take a look at a couple of FAQ articles I have put together:

Our dividend investing approach

We invest in both Canadian and US dividend paying stocks and index ETFs. We are doing a hybrid invest approach, so we can select and pick dividend stocks that we like and use index ETFs to allow for asset and geographical diversification.

What makes dividend stocks and dividend income so enticing? Here are some of our reasons:

- Our portfolio is working hard for me to generate income so we don’t have to. We’d avoid the need to touch our principles when we are living off our investment portfolio.

- Dividends are real money and not some sort of play or funny money. Dividends are deposited in our accounts and we can use them to cover expenses.

- We plan to pass down our dividend portfolio to future generations and create a long-lasting legacy. So not touching the principals is ideal.

- I like having a predictable dividend income. With ETF distributions, the amounts are hard to predict.

- We can pay no tax or very little of it when we live off dividends because Canadian dividends are very tax efficient.

- By investing in dividend-paying stocks and receiving dividends regularly, I can prevent myself from wanting to sell when the stock market is volatile.

In 2020, our dividend income can already cover basic expenses like:

- Food/Groceries.

- Car insurance

- House insurance

- House property tax

- Natural gas & hydro

- Internet and phone

- Term-life insurance

- cell phone & internet

- Car fuel

| Expenses | Per Month | Pear Year |

| Groceries | $850 | $10,200 |

| Car Insurance | $200 | $2,400 |

| House Insurance | $100 | $1,200 |

| Property Tax | $400 | $4,800 |

| Utilities | $120 | $1,440 |

| Term-life insurance | $30 | $360 |

| Cell phone & internet | $90 | $1,080 |

| Car fuel | $150 | $1,800 |

| Total | $1,940 | $23,280 |

In fact, our dividend portfolio has been generating around $3 per hour in 2020, even when we are sleeping or vacationing. This is really amazing!

Which dividend paying stocks do we own?

We are doing a hybrid investing strategy by investing in a mix of US and Canadian dividend-paying stocks and index ETFs. This allows us to build our own dividend index ETF and utilize index ETFs to increase our asset and geographical diversification.

To build our dividend portfolio, we used methods outlined in this how to start investing in dividend paying stock tutorial. Essentially we purchase US and Canadian dividend-paying stocks that are in the top 10 or 20 holdings of key index ETFs like VCE and VTI. We also take a look at the different sectors and make sure we are sector diversified.

For the most part, we like to own companies that produce items that we’d use on an everyday basis. For example, banks, insurance companies, telecommunication companies, pipelines, utilities, etc.

The more reliance we are on the product(s), it means the company has a wider moat. for example, people don’t typically switch their banks, so banks like Royal Bank and TD have a wide moat in terms of keeping their customers. Banks can also easily increase their revenues by increasing monthly service fees. Similarly, people rely on natural gas and must pay the likes of Fortis and Hydro One for house heating.

Keeping a simple investing strategy

Your ego is not your amigo. This is a quote I heard when I first started DIY investing. To be successful with investing and able to beat the indices, one must control their emotion. Therefore, I like to keep a simple investing strategy by following these simple rules:

- Determine a list of dividend paying stocks that we are interested in owning. These include both Canadian and US dividend paying stocks.

- Do as much research as possible to understand the business strategy and model. Determine how these companies make money and stay competitive in their industries.

- Buy these dividend stocks and hold them.

- Whenever possible, enroll in DRIP so dividends can be reinvested.

- For the dividends not used in DRIP to buy additional shares, collect enough dividends then reinvest them.

- Put things on auto-pilot. Avoid panic sales when there’s a market drop.

- Deploy new capitals to buy more dividend-paying stocks

- Collect dividends and reinvest

- Repeat and repeat until we have enough dividend income to cover our expenses

Pretty simple right?

Which accounts to hold the different dividend stocks

For tax efficiency, we hold Canadian dividend paying stocks in RRSPs, TFSAs and regular accounts. All REITs and income trusts are held in TFSAs for tax efficiency purposes. All US dividend paying stocks and ADRs are held in RRSPs to take advantage of the tax treaty between Canada and the USA.

To summarize:

- TFSA: Good for Canadian dividend paying stocks, REITs, and income trusts.

- RRSP: Good for US dividend paying stocks, REITs, and income trusts.

- Taxable: Good for Canadian dividend paying stocks that pay eligible dividends.

We don’t hold US dividend-paying stocks to avoid paying the 15% withholding tax. If you hold US dividend-paying stocks in your taxable account, you’ll pay tax at your marginal rate on any US dividends received. Essentially US dividends are treated like interest income which is taxed at the highest tax rate (i.e. your marginal rate). Although you get a foreign tax credit for the amount you received.

Expediting financial independence

Although we estimated that we’d need about $60,000 in dividend income to cover our expenses, we can certainly expedite our financial independence if we reduce our annual expenses. One of the ideas we have is to move somewhere with a lower cost of living than Vancouver. That’s where geo-arbitrage comes in.

Essentially we can move to a small Canadian town or South East Asia and reduce our annual cost significantly. As a result, we may only need $40,000 in dividend income to cover our expenses.

Supplementing dividend income

In addition to geoarbitrage, there’s another way we can become financially independent earlier. We would need less than $60,000 in dividend income if we can supplement with other sources of income, like part-time jobs or side hustles.

In other words, we can consider a two stage approach.

- Stage 1: Reduce our annual expenses by living at a lower cost of living area. Or using other sources of income and our dividend income to cover our living expenses.

- Stage 2: Use our dividend income to fully cover our annual expenses.

Our Dividend Portfolio

As you can imagine, our dividend portfolio consists of a mix of individual dividend paying stocks and index ETFs is a key driver of our passive income stream. We do not invest in dividend ETFs for various reasons. You can see the holdings and account breakdown of our dividend portfolio in the table below.

Please note: All content posted on this blog represents my personal opinions and views and should never be considered as professional advice. I am not a financial professional, and I can buy, sell, or hold any investment at any time.

The dividend stocks that we own fall into the following two categories:

- Dividend growers. These are companies that have increased dividend year after year. Some of the companies on the list have increased their dividends for over 20 years. The yearly dividend increase is significant because this is a way to keep up with inflation. As our dividend portfolio grows, we will be relying more and more on organic growth. This is where these dividend growers come in.

- High income stocks. These are companies that pay over 5% dividend yield. Most of them have slower dividend growth than dividend growers. The slower dividend growth is OK because of the initial higher yield. Most high income stocks are REITs and income trusts.

Our dividend portfolio consists of a mix of dividend growers and high income stocks so our dividend portfolio can generate dividends at a reasonable yield rate. Since we are dividend investors in Canada, we own a large percentage of Canadian dividend stocks. This is known as the “home town bias.”

We are aiming to increase our international exposure by holding US dividend paying stocks and ex-Canada international ETFs like XAW.

As the value of our dividend portfolio gets bigger, it becomes increasingly more and more difficult to grow our dividend income via fresh capital. Therefore, over the last few years, we have been paying more focus on dividend grower stocks. The ultimate goal here is that our dividends can continue to grow organically without any new cash injection.

For those positions where the dividend received is enough to purchase additional share(s), we enroll in synthetic DRIP to maximize the power of compound interest.

We are currently investing in 35 companies and 2 index ETFs.

(Updated May 2026)

R = RRSP

T = TFSA

N = Non-Registered

Dividend FAQs

Here are common dividend investing FAQs for Canadian dividend investors. For a more comprehensive list, please check out the following two FAQ’s

Q1. What is the dollar value of your dividend portfolio?

This is a common question that I get from readers. We don’t disclose our dividend portfolio value and how many shares we own for each stock and index ETF for privacy reasons. I am not blogging anonymously anymore so I have to keep privacy in mind and determine what I share here.

Having said that, it shouldn’t take a rocket scientist to guess roughly how much our portfolio is. All you need is MATH!

Take 2018 for example, we received $18,734.29:

- At 2% dividend yield that means our dividend portfolio value would be $936,714.50 ($18,734.29 divided by 0.02).

- At 3% dividend yield that means our dividend portfolio value would be $623,476.33 ($18,734.29 divided by 0.03).

- At 4% dividend yield that means our dividend portfolio value would be $468,375.25 ($18,734.29 divided by 0.04).

- At 5% dividend yield that means our dividend portfolio value would be $374,685.80. ($18,734.29 divided by 0.05)

See how easy that is?

So, our dividend portfolio value is anywhere between $374,685.80 and $936,714.50 at the end of 2018. You can take a wild guess of the actual portfolio value.

Q2. Why are you a dividend investor? Why not invest in real estate? Doesn’t real estate provide a way better return on equity?

We do own our house so we are already investing in real estate. We haven’t considered rental properties for various reasons; we didn’t want to deal with tenants and potential tenant issues.

Here in British Columbia, the rental laws are set up to protect tenants. Landlords don’t get too much protection when you have bad tenants (our friends recently had to deal with some bad tenants and it was painful). We like to have the peace of mind you get with dividend investing.

Q3. What’s the best way to analyze a dividend-paying stock?

Before doing a deep dive of a stock I am interested in, I would take a quick look at some of the key financial numbers like P/E ratio, payout ratio, PEG ratio, free cash flow, debt to book ratio, etc. These numbers typically give me a good idea of how the company is doing.

The next step, which can take a bit more time, is to read the company’s annual and quarterly reports and determine the financial trend of the company. It is also interesting to read the CEO message and see if the narratives change over time.

Q4. Your dividend income amount seems to be roughly the same each month. Is this planned or by design?

This is a pure coincidence. Many stocks we own happen to pay out monthly dividends. The stocks that pay quarterly dividend stocks seem to spread out somewhat equally. Having said that, our weakest dividend income months are February, May, August, and November.

Q5. What are some dividend investing resources that you use?

Here are a few sites that I use for dividend investing:

- DRIP Investing – an excellent website for DRIP investors. You can get an extended list of US and Canadian dividend champions and dividend all stars.

- Morningstar – a great website for getting stock evaluation information.

- http://longrundata.com/ – an excellent website for doing research on dividend growth history. I also like using its Dividend Reinvestment Calculator to reinforce the idea that DRIP is very powerful in the long run.

Q6. What are eligible dividends and non-eligible dividends?

The key difference between eligible dividends and non-eligible (or ordinary) dividends is how you get taxed if you receive dividends in a taxable account.

Essentially, eligible dividends get more favourable dividend tax credit while non-eligible dividends do not.

Why is that? Well, eligible dividends are paid from a corporation’s after-tax profits. This means the corporation has already paid corporate income tax on that income.

To avoid “double tax,” the Canadian government allows you to get a 38% dividend gross-up rate which leads to a higher tax credit rate. The net result is that eligible dividends will have a lower marginal tax rate than the marginal tax rate for employment income and interests.

On the other hand, for non-eligible dividends, you only get a 15% gross-up rate. Because of the lower gross-up rate, you don’t get as much tax credits compared to eligible dividends.

If you want to look at the actual numbers and the different tax brackets, you can find more information below:

- Federal & Provincial/Territorial Enhanced Dividend Tax Credit Rates

- Federal & Provincial/Territorial Non-Eligible Business Dividend Tax Credit Rates

Q7. What do you do when you max out RRSP and TFSA?

If you can max out RRSP and TFSA each year and have leftover money to invest, that’s a very good problem to have!

If you have leftover money to invest after maxing out RRSP and TFSA, I assume you want to be as tax efficient and simple as possible. I will also assume that you have no debt. If you do have debt, whether it’s a mortgage or consumer debt, I think it makes a lot of sense to pay down these before you consider investing outside of RRSP and TFSA. If you have kids, another option is to contribute to their RESPs with the extra money

If you don’t have any debt and have already maxed out RESP, consider yourself very fortunate. In this case, the only place to invest the extra money is in a non-registered or taxable account.

Since taxable accounts are subject to income tax (hence for the name “taxable”, ha!), you want to be as tax efficient as possible. Since bonds, GICs, and international dividends are taxed at 100% of your marginal rate, this means it’s best to invest in Canadian equities inside of your taxable account.

Where does that leave you? One option is to invest in an index fund that tracks the Canadian market. Vanguard Canada All Cap Index ETF (VCN) and iShares Core S&P/TSX Capped Composite Index ETF (XIC) are good options due to their low fees.

The other option is to invest in individual Canadian stocks. You can either purchase a Canadian stock that doesn’t pay any dividends or a stock that pays dividends. If you go with the dividend paying stock route, make sure that you purchase a Canadian stock that pays eligible dividends for reasons stated above.

If your TFSA and RRSP are maxed out, and holdings outside non taxable accounts are substantial, as long as your income is location independent, then it makes sense to start looking at tax residency in low tax jurisdictions. Holding assets in a fully taxable account is really going to hinder your compounding benefits.

Hi Kevin,

Can you explain what you meant by holding assets in a fully taxable account is going to hinder the compounding benefits? RRSP and TFSA have contribution limits so once you max them out the only way to invest is in a taxable account.

Yes, that’s true if you are a Canadian tax resident. I’m just stating that if you reach the point where your assets have grown to the level where your RRSP and TFSA are maxed out, and your holdings in a taxable account are sizeable, then it might be worth considering acquiring tax residency in a low tax jurisdiction so that your wealth will compound much faster without the hindrance of a high tax rate. Of course, this is dependent on your mobility, if you are tied to Canada through your job or business, you may have to wait until you are able to retire, or are otherwise financially independent.

Makes sense, thanks for the suggestion.

Have you considered focusing on a total return approach rather than solely dividends? With more and more companies pursuing share buybacks, as tax-efficient way to return capital to investors, it makes a lot of sense, rather than solely focusing on income.

We definitely focus on total return.

I noticed that you hold XAW in your non-registered portfolio. Is that an issue for tax efficiency given that XAW excludes Canadian equity? Also, is there a reason that you picked that ETF for your non-registered account? I’m guessing that the lower yield is helpful (for tax purposes) but there are many others such as XEQT. Thanks!

A very good question! I’d take a look here – https://tawcan.com/dividend-tax-drags-foreign-withholding-taxes/

We hold XAW in non-registered portfolio mostly because we already hold it in RRSP. The low yield from XAW is helpful for tax purposes.

Trying to understand this as well. You mention trying to focus on only on CAD dividend stocks in your non reg account but use XAW. Can you elaborate why and not more CAD dividends. Thanks and really enjoy your blog. Well done!

Again, we hold XAW for diversification reasons. We can certainly hold more CAD dividends but there’s only so much contribution room for RRSP And TFSA so naturally we needed to hold XAW in non-registered so we can increase our XAW weighing. Hope this helps.

Your estimates for expenses are awfully low. Not sure how Vancouver is so less expensive.

Car Insurance is only $200

Utilities – Hydro, Gas and Water are easily $300+ Not sure how you calculate only $120

Hi Mirza,

Those numbers were from 2020 and yes some numbers have increased since but you get the idea of using dividends to cover expenses.

I just discovered your blog and wanted to let you know I think it’s great. Thank you so much for sharing. I have been investing for ten years, I’m 56 years old, and am on my way to living off my own dividends – I follow a really similar strategy to yours, except that I do heavily use dividend ETFs. I have your “why we don’t use dividend ETFs” post on my list to read very soon, though, so who knows… maybe you’ll sway me. Thanks again so much.

Thank you so much Rhonda, happy reading. 🙂

Tawcan,

Thanks so much for the helpful article! I’m a beginner investor, 30y.o, currently holding 98% of my TFSA in XEQT and 2% in dividends (all Canadian). I’m looking to expand my dividend holdings to 10% in 2022. Do you think it makes sense?

Thank you!

What’s the reason for you to increase your dividend holdings from 2% to 10%? There’s nothing wrong with holding XEQT. But it’s really a personal choice. 🙂

Honestly Bob

Would you hold XEQT?

We utilize XEQT for RESPs.

If we were to start investing today, I’d start off by buying XEQT rather than individual dividend stocks.

I am a year into dividend investing, having started Jan 2023 with approx 12 individual Canadian stocks for combination of dividend growth and yield. These were purchased with new RRSP/TFSA contributions. Remainder is in all equities ETFs (XEQT), primarily, with small percentage in VGRO, as this was the first ETF I bought prior to becoming comfortable with all equities. Individual CAN stocks comprise approx 20%. Strategizing now about this year’s contributions – continue building dividend portfolio with new contributions & keep remaining ETFs as they are OR transfer existing ETFs to XAW, for example, to remove Canadian over representation and maintain diversification? Wondering what your hypothetical strategy would have been following the above – ie buying XEQT rather than individual stocks, if still planning to move toward hybrid approach.

Hi Tam,

If you have 12 individual Canadian stocks, then there’s some Canadian overlap with XEQT and VGRO. We own XAW as we hold many Canadian stocks so we don’t need additional Canadian exposure from XEQT/VGRO. Having said that, the hybrid approach is great as the ETFs do provide some level of asset and geographical diversification. Given that you said individual CAN stocks are only about 20% of your portfolio, holding XEQT/VGRO should be fine IMO.

My opinion, 30 y.o, your TFSA should be invested in growth. If you max out your TFSA, say hypothetically contribution limit is $65k and it grows to $90k. If you were to withdraw $40k, you investment room does not shrink back to its contribution limit, but instead, you have $40k contribution limit. Any growth in your TFSA adds to your contribution limit.

At 30 I invested mainly in growth simply because I was earning top dollar and if thing went sideways, all it meant was more work at night or on weekends to make up the shortfall.

XEQT does not pay enough. look rather at ZHY which pays much better and has history. IMO

If you withdraw from TFSA, you can only contribute to the same amount the next year.

ZHY is a corporate bonds ETF. At 30 years old I would not touch bonds.

Whatever growth you have in a TFSA is added to your contribution limit.

Contribution limit TFSA say $65K, you invest $65K,. It grows to $90k because your investments have done well.

If you were to drawo out the full $90k, your contribution limit is now the contribution limit plus the growth.

Ergo Contribution limit $65k + the growth of $25k = $90k

Market gains increase your contribution limit in your TFSA, as do market losses decrease it.

Therefore if you need the money always use those assets which have gains is the general rule of thumb.

Fine, then ZWB or ZWC as an example far out does XEQT by a long shot.

Also a 992:1000 split at the end of the year, please.

You’re correct on the growth part. However, if you take out $40k in 2022, you don’t get the new $40k contribution room this year. You get that next year. If you withdraw the $40k say in Feb then contribute it back to the TFSA in June, you’ll get hit by the 1% per month over contribution penalty. This detail many people miss.

Hey there, great site. Thanks for the info.

Any thoughts on a MIC (Mortgage Investment Corporation)? Seems like they pay decent dividends, often higher than even energy stocks. I don’t see it mentioned as part of a potential cash-flow portfolio.

Cheers,

Mike

Hi Bob,

It was an excellent post so thanks a lot for sharing. But I have some confusion. I have only recently started to learn more about dividend /index investment so I hope you will not mind.

1) If you already use your dividend payments to pay for various expenses, how do you enroll in DRIP programs?

2) How can you expend the foreign dividends which are invested through RRSP? is it permissible to withdraw dividend payments from RRSPs?

Greetings from Ontario, Bob.

Thank you for your fantastic blog.

I started my own quest for FI some time ago and after considering and testing many different approaches, I found myself favouring an approach that is very similar to yours.

I am very appreciative of the level of detail that you have published.

Your taking the time to explain your rationale for your decisions has been extremely helpful to me.

Thank you Bob, please keep up the fabulous work.

Thank you JimBob.

Hi Bob,

Great post. I wonder if you could please elaborate on how you determine the value of the stock and long term forecast, or if you have written previously on this subject, a link to it

“It’s not just looking at the price of the stock, it has more to do with determining the value of the stock and the long term forecast.” Merci!

Hi Thara,

These should help:

https://tawcan.com/dividend-faq/

https://tawcan.com/your-dividend-and-index-etf-questions-answered/

Thanks for the info on your site. It’s been very helpful in my research. I understand in the TFSA and taxable accounts you may want to have dividend paying stocks where you can pull out cash to pay expenses. However, for the RRSP I’m assuming you wouldn’t withdraw cash until you retire. Why not pick stocks that are likely to have higher capital appreciation over the next decade vs dividend paying stocks. It seems like some companies are set to grow faster than some of the dividend paying stocks you have picked. Amazon, Google (Alphabet), and Tesla come to mind. Admittedly, you have to roll the dice and there is no sure thing but it seems like putting some cash into these would yield higher returns than companies like Suncor or Enbridge (oil is a four letter word these days). In 10 years, you could sell the stock in the RRSP and convert to a dividend paying stock for retirement with, hopefully, a larger amount of capital. Curious on your thoughts.

Hi Mike,

We do invest in growth stocks in our investment portfolio, I just don’t write about them on here

Thanks, makes sense. What ratio do you devote to growth vs dividend?

Would like to know as well how (and why) you split your divs & growth portfolios.

Since the governemnt rolled out the TFSA, you would be beter off to invest in growth stocks there, simply because they would not be taxed.

I am from the old school, way before the time of TFSA, but even then, if you wanted growth an RRSP was not the place to park it.

Let me put it this way. In an RRSP you have the initial tax savings for that year, but the taxman always take his cut when you withdraw. Canadian tax policy has always been, that they trust you and if you have capital gains you will report them at tax time.

MANY DO NOT and it is upto the the government to track them down. You would have better luck of finding a snow hare in a blizzard than the Canadian government tracking down all the delinquint debt.

Also once they charge you, if you personally do not own anything, the only thing they can do is garnish your Canadian pension and we all know what that is worth.

Just my two cents and nothing more

Would like to learn more about delinquent debt and declaring cap gains, if you don’t mind elaborating. vasra.invest@gmail.com if not here

Mike, it all depends on you age, financial status( debt level opposed to assets), family status and also with how much risk you are comfortable with.

If you wish to invest in growth there is nothing wrong with that or if you wish dividend investing great. Another approach would be to allocate funds into dividend stocks and at the same time allocate funds into growth because you can average out the dividend yield in this way.

Example: $ 5,000 invested in Enbridge yield 6.79%

$ 5,000 invested in Amazon yield 0.00%

Your average in this case would be 6.79%/2= 3.39% which is still fairly reasonable when you consider.

You have the dividend and can DRIP plus you have also hedged against losing out on growth.

There is nothing wrong investing either way, the trick is to have your money work for you and in a savings account it does not do that.

Read, read, read. Investment Reporter is one of the best subscriptions for Canadian investors and you did not hear it from me. But, if you have friends that also invest, share the subscription and it is the best money you will ever spend.

They actually put me onto BRK when they did not have A and B shares and at that time they were already valued at $8000+ US, so you figure out when I discovered that gem. Way before Bob even knew which high school he would attend after elementary school.

Another piece of advise, go talk to a financial planner at your bank and other banks and not just one, but a few, they all have different ideas where or how to allocate your portfolio. Do not worry if it is a man or a woman, they are both talking about your money, so if you have question ASK THEM. If they get offended, too bad, then they are in the wrong business, they are professionals and as such I pull no punches when it comes to MY MONEY and I expect her to hold the door for me, I AM THE CLIENT. Any financial planner worth a grain of salt will not charge you for a meeting, they all want more clients, but it seems that everyone thinks they charge for their service, THEY DO NOT.

They assess how comfortable you are with investing, debt asset ratio, funds available, where you would like to end up and much more.

If you feel, the person is not suited to you, fine, but it also works the other way also. After the meeting, you might find out that they feel, you are not a suitable client, it happens. They may want your funds to increase their portfolio they manage, but you are too much maintenance.

Show me a real estate agent that charges you to list your house before the sale and he or she was not in business long. It is a part of doing business.

I view blogs and vlogs as tools to help you and maybe you come out of it with a few good ideas, but they are not the be all and end all.

Quite honestly, if you have FIRE, would you need to share that with other people, sorry I have better things to do with my time than to talk to people I did not know before this whole journey. I do not need or want people to know my financial status and to post it like Reader B, I do not need to hear congratulations from people I don’t even know. Heck, my own family does not even know what my wife and I are worth, kind of personal and quite honestly we all had FIRE before 60.

I always told my friends, if I need the government to support me when I get older, then I did something wrong.

Hope it helps.

Gerhard, would like to disagree at your last point about FIRE. Like how you said you have better things to do than sharing your strategy. Actually they are not sharing these for free. If your blog website has decent traffics than there are multiple ways to generate passive income from these blogs. Many PF blogger earn on average 3000-5000 per month from their PF advice websites.

Great, thanks.

So in the “Why dividends?” section you say that you reinvest your dividends using DRIP. Then again in the “Dividend Income” section you repeat how to use DRIP for growing your dividend stocks. However later in this same page you start talking about how you are living off your dividend portfolio and using them to cover your expenses! You also provide a list of expenses that you cover using your dividend as an example! While it all sound so very assuring and exciting I am wondering, if you’ve already reinvested your dividend income through DRIP, is there any left for Food/Groceries, Car insurance, House insurance etc…?!!

Hi Tan,

Since we’re in the accumulation phase still, we’re not “using” dividends yet. We are dripping whenever we’re eligible.

The cover expenses part is just an example that our dividend income can already cover these expenses today if we aren’t dripping and using our dividend income. Hope this helps.

Hi,

I recently found your blog and really loving it. I am new to DIY investing. Transferred an RRSP account to questrade and have lump sum (40k) to invest in. Since I would now have the option to do both US and Canadian stock purchases, would need your recommendation on how to split this up between ETF and CAD/US dividend stocks and the stocks to buy. Have been buying VGRO ETF for monthly investments. Saw your post on how you would invest if you had 1k vs 10k but that was dates in 2015. So want to get your advice based on current market conditions. Thank you very much. Looking forward to your response.

Hi Pavirthra,

You might want to take a look this this article – https://tawcan.com/five-lessons-ive-learned-as-an-investor/

Without knowing more details about you and your goals, it’s nearly impossible to provide any suggestions. Furthermore, ultimately you need to make the buying decision on your own. 🙂

If you are looking for more one-on-one coaching, please take a look here – https://tawcan.com/coaching/

Hope this helps.

Thanks for your response!

Forgive me Bob.

But, when we sold our house in North Vancouver, our friends asked us, why wouldn’t we save it for our kids?(I have three) We own another house at the time, so I asked them, Should I buy a third, so all three get a house?

My wife and I worked hard to pay for what we have, and the legacy I will leave my kids is hard work, honesty, loyalty and above all else FAMILY. Believe me, they have survived this far, they will be fine and stand on their own two feet.

We now own an apartment in Vienna, a house in the country and also one in North Vancouver, as far as drawing down my investments, that will not be their legacy to enjoy.

It will be my wife and mine to do.

I did not work to make my kids rich, I work because actually I enjoy it.

People once told me I need a hobby when I retire, guess what, making money is my hobby.

Take care and do not lose sight of why you wanted financial independence. It was for yourself, no one else. You wanted the security, your kids do not know any better.

I’m not saying if we will absolutely pass down the money to our kids. It’s just an option that we’re considering.

Hi Bob

Good job.

Came across you and started reading.

If you can generate $60,000 in dividend income, wonderful.

Most Canadian companies or actually “Dividend Aristocrats” rarely lower their dividend or actually will cease all together simply because they maintain a certain pool of cash for hard times. aka April 2020 ‘The Covid pandemic’. One of my stocks quit paying for 2 months because they are in the restaurant business and were basically shutdown but they pay dividends again.

Only thing I would like to add is that at a certain age that $60,000 in dividend income also will have capital added to it when you start drawing it down in your retirement. You should add a section on that. Keep up the good work. Originally from north Vancouver, now touring Europe for the last 12 years.

Yes I did sail in Ca

Yes we probably will eventually draw down from the portfolio but if we can, it would be nice to pass down the portfolio to our kids as a legacy.

Hi Bob,

I have three questions for you after reading your post on how much money you “need” to retire.

1. No one recommends to have 100% of your portfolio in divided stocks so the 3% you talk about is at a high risk?

2. If you count on an average 3% return but inflation is at 2% would you not go backwards over time?

3. Considering the “new norm” of zero interest but we see inflation as prices are going up how do you keep up?

Thanks,

Josh

Hi Joh,

I think you have some incorrect assumptions…

1. I never count on an average 3% return. The long term stock market return is around 8%.

2. I’m being conservative and estimating a 3% dividend yield for our portfolio.

3. Companies have a tendency to raise dividend payouts every year. Being conservative, I’m estimating a 5% organic dividend growth, which will take care of the 2% inflation.

hi Tawcan,

Could you please post and update us with your actual weights in each company that you own?

Hi Sam,

Sorry I don’t disclose that information. 🙂

Hi Bob, question about how you plan a couples TFSA/RRSP to account/plan for if/when one spouse passes away (big concern during covid times). You and your spouse max out your contributions every year which means there is no room left to inherit the contents of the spouse’s investments. Do you therefore plan to hold stocks in each of the individual plans that will carry you forward in your FIRE plan as the other spouse’s accounts would be liquidated? Maybe there are rules for when spouses pass away that you don’t need room to continue to hold those stocks in the spouses accounts and therefore continue to receive the dividends. Thanks for sharing, Pat

Hmm good question Pat, since we are both still young, this is not something we are planning.

For things like TFSA/RRSP/taxable, we are each other’s benedictory so there shouldn’t be any problems if one of us were to pass away.

Hi Bob,

Thanks for sharing your success stories and money making strategies. I was wondering what the total return on your dividend portfolio (CAGR) is and whether it beats the S&P500 or the 10% annual return (kind of my rule of thumb for overall stock return). Also what do you think of a portfolio that has maybe 80% dividend ETF (ZWA or ZDY) and 20% aggressive growth such as qqc-f. This would generate a 4%+ dividend yield and a reasonable annual growth. Thank you

You can check out this post here:

https://tawcan.com/dividend-portfolio-beating-the-tsx/

Hi Bob,

Not sure if this has been answered before but I noticed some of the stocks in your portfolio are held in TFSA,RRSP, and Taxable. For example Telus.

Could you explain the reason for that?

Thanks!

Hi Bruce,

I have answered that in the past. Please take a look here (question 3) – https://tawcan.com/dividend-faq/

Bob! Your blog is amazing! Greetings from the U.S.! You really give such a great in-depth explanation when it comes to dividends. Take a moment to realize how far you’ve come since emigrating from Taiwan. Keep up the great work!

Hi Bob

I like your site. I hope you make your early retirements goal!

I was wondering how you project your future dividend yields. I looked at your numbers and I find the % increase from 2021 to 2025 follows this pattern:

2020 $27500

2021 $33000 +20%

2022 $38940 +18%

2023 $45600 +17%

2024 $52400 +15%

2025 $61800 +18%

I have projections I use for my dividend income as well and I’m trying to understand what projections are reasonable. I was hoping you could provide some insight into how you determine this.

Cheers,

Mich

Thanks Mich.

I used the assumption that we can continue to grow our dividend income by ~15% each year. Some years are higher because I think we can contribute more money.

Hey Bob,

Quick question, notice you have no bond component in your portfolio, why ? Mainly stocks with global diversification only. Also why did you buy VCN when you will have overlapped the same stocks you already own ? Just curious.

Regards and thank you for your website

Anhvic

We are still young so no bonds. With the current low interest rates, it doesn’t make sense to hold bonds. We have some VCN for diversification purposes.

Hi Bob,

I’m also a fellow Taiwanese-Canadian living in Vancouver, I came across your blog by accident while I was Googling about Dividends. I’ve learned lots from your blog and felt extremely inspired that my dividends projected for this year is about the same as what you had received in 2011. Your blog inspired me to look at how I can achieve FI in 10-15 years when turn I am 45. Thank you so much for sharing your journey! 謝謝!

-Rybo

Glad that you found this site. 🙂

Hi tawcan, I love your forum. I currently own about 10 stocks in your portfolio but looking to add some more. What would be your top 3 recommendstions at the moment in your portfolio for a long term hold.

Thanks!

HI Tawcan, can you let me know what’s your average dividend % you are getting from all your holdings. Also which stock broker do you use for trading?

We used Questrade. Our average yield is in the range of 3-4%.

Hi Bob,

Do you recommend owning preferred shares ETFs or stocks over traditional stocks or bonds? They seem to pay a significantly higher dividend though I guess their upside can be limited? I just learnt about them from the blog whose book you recommend in your last post and it sparked my interest. Any suggestions you have are welcome.

Hi Ivy,

Preferred shares is a good way to boost dividend income for sure. Just make sure you understand the potential shortcomings with preferred shares.

Dear Bob! I have good warm feeling while reading your opinions, considerations. I am especially please to see Mrs. T and your photo.

There are 2 more sites attracted my attention. It’s your peers- adwisers. What is your oppinion about ?

-https://www.simplysafedividends.com/dividend-safety-scores/

– http://www.dividendmachine.com/

Also, what do you think about following W. Buffet advice (see below) for the person with .5M cash willing to invest in minimum managed fund/(s)?

WB: “It would probably make more sense for the small investor to achieve appropriate diversification and lower fees by accumulating shares of an ETF until his or her account was more sizeable.

…90% in a very low-cost S&P 500 index fund. (I suggest Vanguard’s.) I believe the trust’s long-term results from this policy will be superior to those attained by most investors “

Hi Ivan,

Sorry I’m not familiar with the 2 sites you mentioned so I can’t comment.

Generally speaking with these paying sites I don’t pay much attention to them. It’s fine they provide stock picking recommendations and all, but unless the authors have a sizable dividend portfolio and actually are playing with their hard-earn money, it’s really hard for me to follow their advice. Hope that makes sense. It’s like why would I pay and listen to someone that hardly have any money in the game? You’re just playing with paper money. 🙂

Regarding your Buffet question… that’s exactly why we do a hybrid approach – investing in both index ETFs and individual dividend paying stocks.

The problem with these paying sites is that they do not even invest in what they recommend so how can we trust them?

It takes discipline to hold while down! I am holding some underwater positions but have cut a couple of big losers (HCG, CJR.B) because of dividend cuts and fundamental issues. I see in a responce above that a full position for you is 100 shares? Was that only meant in regards to drips? I am using a portfolio percentage as a guide for full positions and increase or decrease the amount based on market cap of the company. What are you using as a full position guide?

Full position is 100 shares because back in the days before online discounted tradings, trades typically have to be in full lot (100 shares). Companies charge higher commissions for trading odd lots (not in multiples of 100 shares). It has nothing to do with DRIP.

Hello Bob,

I see you have a relatively large portfolio, I also maintain a similar fairly large portfolio as well.

Do you ever sell holdings or are you a buy and hold no matter what investor? For example I see you have HLF.to is this a recent purchase or have you held it and are underwater? YTD-34.25% , 1 year -43.97% , 3 year -60.54%

If you do cull your herd of dividend growers, what is your criteria for selling? I am watching for any dividend cuts or significant changes to fundamentals.

We are down with HLF.TO quite a bit but plan to continue to hold. Do we sell stuff here and there, mostly if we don’t have the conviction of the company future performance anymore.

Hi Bob,

Great website and information! Quick question. In your dividend portfolio, when or at what price will you decide to buy and add to your portfolio?

Many thanks!

Jerry

It’s not just looking at the price of the stock, it has more to do with determining the value of the stock and the long term forecast. The best way is really to look at each company’s quarterly and annual reports.

Thanks Bob

Hi Bob,

Looking good! I have a quick question for you – how do you know how much dividend income you got from each of those stocks?

Thanks,

You can take a look here:

https://tawcan.com/dividend-income/

Thank you ! I am a beginner and I feel overwhelmed by inviting. Your website really helped me out to understand things and how to keep it simple. keep up the good work and awesome site. It would be awesome if you have a section for beginners like a 101. I wish you all the luck in the world. Cheers 🙂

Hi Yaz,

You could check out Dividend FAQ.

https://tawcan.com/dividend-faq

Maybe I should call it Dividend 101 instead?

Just found out about your blog, nice! I have to wonder – why do you invest in high dividend yield stocks directly and not through an ETF such as VDY? Stock picking seems more laborious (requiring tracking) and riskier (due to less diversification) over the long run. Also, presumably basing your income on dividends is fine for a rising market, but I’d imagine that in a slump dividends would be slashed drastically, requiring another source of income or selling of assets to stay afloat.

You can take a look at my reasons here:

https://tawcan.com/top-canadian-dividend-etfs-dont/

Hi Tawcan,

I love your portfolio. I currently use the CCP ETF strategy for my kids RESP. I am considering switching over to a dividend stock portfolio similar to yours. With a portfolio of approximately 50k, what kind of stock diversification would you recommend considering 15 years until the money has to be withdrawn?

Thanks and keep up the great work.

Ivy

Thanks Ivy. For RESP I’d just stick with the index ETF strategy, that’s what we’re doing with our kids too.

I appreciate the quick reply!

Curious. Do you have a fixed income component to your portfolio? If so, what percentage did you go with overall and what sorts of things is it invested in? The fixed income part is aggravating me!! Lousy yields and bonds losing value due to interest rate increases. I’m thinking of lowering my fixed income to maybe 25% or less and just develop a better dividend paying portfolio.

We are more or less about 98% in stocks. The only bond that we own are through my work RRSP.

Hey Tawcan,

Just two questions. 1, do you know if you can import google finance info into a regular excel file & 2, what site do you

use to get your info regarding companies (eg dividend growth, etc..)

Hi Peter,

I don’t believe you can import google finance into a regular excel file.

Please take a look at the dividend FAQ page for your question about research.

Hi Bob,

New reader here, just getting started on saving and investing towards FI. I was just wondering, which account do you hold your two index ETFs in?

Thanks!

Hi Will,

We have these ETFs in TFSA and RRSP.

How many stocks did you start with? What would be a decent amount to start with in each? When younhave more money to invest, how do you decide between adding to what you own already or buy something else? Do you rebalance based on sector weight? Under what circumstance do you consider selling a position? You might have answered these questions already but I just found your blog ….thanks!

Hi Mona,

You might want to read about how I got started with dividend investing here

https://tawcan.com/how-to-start-dividend-investing

Here are a few scenarios you can consider

https://tawcan.com/tips-on-dividend-investing-with-canadian-perspective/

I like to add to existing positions so we own full position (100 shares) or sufficient shares to DRIP. Then we buy something else. We try to rebalance based on desired sector weighing. Don’t typically sell a position but you can certainly read about all the sells I have done on the blog to see the reasons behind selling.

You mentioned that you buy Canadian Dividend paying stocks in TFSA and US stocks in RSP.

But i also see many US listed companies in your portfolio above . . . e.g Apple.

Right, these US stocks are held in our RRSP.

The portfolio are all the dividend stocks that we hold.

Something wonky with HLF in your portfolio listing.

Nice portfolio, keep up the good work.

Great portfolio, good job.

What are the holding weights?

I currently do not share this info but may in the near future.

I think your dividend portfolio is quite impressive for me.

BTW, could I kindly ask the magic formula for “Div $” and “Yield %” in google spreadsheet?

Thank you in advance.

Charles

Thanks Charles, please take a look here: https://tawcan.com/using-google-spreadsheet-dividend-investment/

Hello Tawcan,

out of curiosity, what’s your current average yield based on book value? Should be pretty high by now. Would be cool to see how that compares to the current yield based on market value. Since you have been investing for a while (and thus would have purchased at relatively low book values + had increasing dividends), we are curious to see how this has developed over time. Maybe an idea for a future post (hint hint!)?

Your portfolio is great, well deversified and you are way ahead of me 🙂

Take care!

Dividend Freedom

Thanks a lot Tawcan. I’ll go over it. It looks very helpful. Thank you!

Hi Tawcan, Very strong portfolio. I noticed the above share price are all upto date with current market value. I’ve an excel spreadsheet where i have list of stocks i own, my cost price, no of shares etc however i don’t have the column that shows up to date market value for each individual stocks. Is it possible to automatically reflect daily market value on the excel spreadsheet or I have to have an online blog or website in order to reflect daily price of each stocks? can you please give me some information

Hi Dipu,

I use Google Spreadsheet. You should take a look at this post: https://tawcan.com/using-google-spreadsheet-dividend-investment/ Hope it helps.

That’s a huge list of strong companies! For me, it would be too much, as I like to sell options on my holdings. For that strategy it is better to have few stocks, but many.

I also think more European companies would be a great fit! Keep on investing! 🙂

Great portfolio Tawcan. I like your strategy and I’ll most probably mimic it partly. You’re pretty heavy on current income / slow grower in your TFSA for tax efficiency. That’s my plan too. I’ll most probably hold a mix of banking stocks, high yield stocks and reits in my TFSA until I max it out and then I guess I’ll diversify it with lower yielders but higher growth stocks. It seems to be the best tax efficient and balanced strategy I’ve found yet for that account. The ARCP mess has slowed down my appetite for REITs though and I really wonder what will be the impact of higher mortgage rates in the future. I guess that time will tell and lets celebrate the fact that the government doubled our maximal authorized contribution to this account. It’s going to help us get tax free income from our stocks! 🙂

best regards,

Hi: Do you use the Canadian Dividend All-Star List as an information source to select which DGI stocks to buy? Or, some other source? Some stocks appear to have a pretty ;low yield, such as Saputo, CNR, and even Apple, so I wonder why you chose these stocks. Thanks.

Hi Hlen,

We use Canadian Dividend All-Star list for DGI stocks selection but we also look at other sources like what we use on a daily basis. We also. Saputo, CNR, and Apple do have low yields but they have amazing dividend growth history. High yield isn’t everything. We aim to have a balance of high yield stocks and high dividend growth stocks in our portfolio. Hope this helps.

Hey Tawcan,

Is there a link to this Canadian Dividend – All-Star list for DGI you can provide?

Impressive list! Are the US stocks in an RSP? If not, how do you justify paying the 15% withholding tax on dividends in a non-registered account? Is it worth it? Thanks.

Hi Helen,

All the US stocks in our portfolio are held in the RRSP. We do not want to pay the 15% withholding tax on dividends.

If holding US stocks in a non-registered account, the 15% tax drag is still recoverable when filing your taxes. You want to avoid US stocks in a TFSA, RESP and RDSP, as they are not recoverable in these account types. Of course this in mind if your RRSP is already maxed out.

You have it wrong; the US WHT is 30% if you are Canadian and owning US securities in a non registered account. You can recover 50% of it, ie., 15% when you file in your taxe report.

Got 27 companies in your list 🙂

Good diversification in your portfolio. I will be looking to buy some British ADRs in my USD $$ TFSA next year.

Tawcan,

Your portfolio is really kicking. The sheer quantity is outstanding, I cannot wait until I am there one day. I like how you differentiate out some of the Canadian stocks, because as the ticker symbols seem to cross nationals differently.

Nice to see a few stocks I have there as well.

Keep it up,

Dividend Gremlin

You have built a nice diversified dividend portfolio. Looks like you are well on you way. We both share the same interests for the outdoors. I am a avid forager, hiker and snowshoer. I have been building up my dividend portfolio and investments slowly over time. Thanks for sharing your portfolio and keep up the good work.

It’s great to see other people out there holding the same companies. It goes to show that investing for the long term in quality companies just plain works.

Look forward to your progress!

I see you have been investing for a while now and holding a very nice looking portfolio. I see quite a few similar names I am invested in, so glad to have a as a fellow shareholder to these great businesses.

Keep up the good work.