Happy new year! I hope everyone enjoyed their holiday break and spent time with their families while staying safe and healthy. What a crazy year we had in 2021 eh? It’s hard to believe that I worked from home the entire year. Hopefully, we’ll see the end of the pandemic in 2022 and go back to our “normal” lives.

I had the pleasure to be off for 18 days over the holidays and it sure was nice to not have to think about my full-time work, not write any blog posts, and just enjoy my time off. I really really really enjoyed that.

Throughout the break, Mrs. T, Baby T1.0, Baby T2.0, and I all shed a good amount of tears after losing our beloved cat Perlemus just before Christmas. The other day we got a postcard from the veterinarian hospital regarding Perlemus’ passing. Two cat paw prints were on the postcard and we could only assume were Perlemus’. Getting the postcard resulting all of us bursting into tears again… who knew losing a pet would be this hard?

Getting outside of the house kind of helped us with the grieving process. So thanks to the deep freeze in December, we had a lot of chances to play in the snow. Both kids had a lot of fun jumping around on the trampoline and sleighing on the local slopes.

We also enjoyed skiing at Grouse Mountain before Christmas and checked out some of the Christmas attractions. Both kids had gotten more comfortable on skis and could get themselves up whenever they fell. This made my life a lot easier since I no longer had to sidestep up the slope to pick them up (a real workout).

We plan to spend more time skiing this winter and get both kids down blue runs proficiently by the end of the season.

Dividend Income – December 2021

Back to the key topic… dividend income! In December we received dividends from the following companies:

- BlackRock (BLK)

- Brookfield Renewable (BEP & BEPC & BEPC.TO)

- Canadian National Railway (CNR.TO)

- Canadian Tire (CTC.A)

- Canadian Utilities (CU.TO)

- Dream Industrial REIT (DIR.UN)

- Enbridge (ENB.TO)

- European Residential REIT (ERE.UN)

- Fortis (FTS.TO)

- Granite REIT (GRT.UN)

- Hydro One (H.TO)

- Intact Financial (IFC.TO)

- Intel (INTC)

- Johnson & Johnson (JNJ)

- Coca-Cola (KO)

- McDonald’s (MCD)

- Manulife Financial (MFC.TO)

- Magna International (MG.TO)

- Qualcomm (QCOM)

- RioCan REIT (REI.UN)

- SmartCentres REIT (SRU.UN)

- Suncor (SU.TO)

- Target (TGT)

- Unilever plc (UL.TO)

- Visa (V)

- Waste Management (WM)

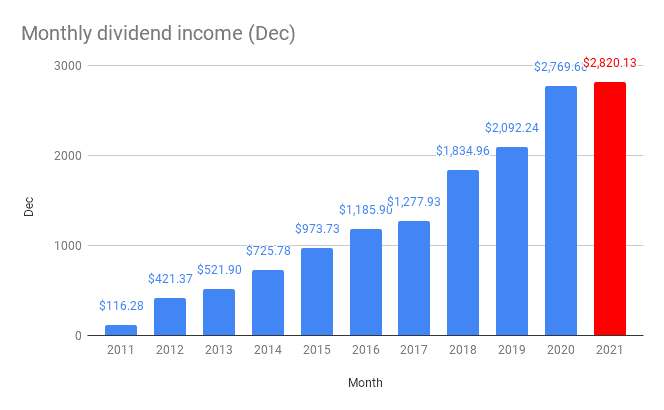

A total of 26 dividend paycheques summed up to $2,820.13, resulting in a very fantastic way to wrap up the year. The December 2021 dividend income only increased by 1.82% when compared to December 2020 dividend income. Since we received a special dividend payout from Costco last December, the small YoY increase made sense.

Out of the $2,820.13 received, $523.26 was in USD and $2,296.87 was in CAD or about a 20-80 split. Long time readers will recall that we do not convert USD to CAD when reporting our monthly dividend income. This is to keep the math easy and avoid fluctuations in our monthly dividend income caused by changes in the exchange rate.

The top five dividend payers for December were Enbridge, Canadian Utilities, Brookfield Renewable, Fortis, and Manulife (not in order). These top five dividend payer amounts added up to $1,915.61 or about 67.9% of our December divided income.

December 2021 Dividend Transactions

At first, we thought we wouldn’t make any dividend transactions in December and wait until January but that wasn’t the case. First, due to the poor Unilever plc price performance over the last five years, I decided to close out the position. We then used the proceeds from the UL sale and some additional USD to purchase 75 shares of VICI. We started a position in VICI back in September and have been adding more shares in the last few months. I continue to like VICI, its management team’s vision, and VICI’s real estate portfolio. If you can aren’t familiar with VICI, you can take a look at my investment thesis of VICI here.

We also added a few more shares of iShares Ex-Canada Internal ETF, XAW in time for the semi-annual distribution in January. We also added more shares of Royal Bank, National Bank, and Algonquin Power & Utilities.

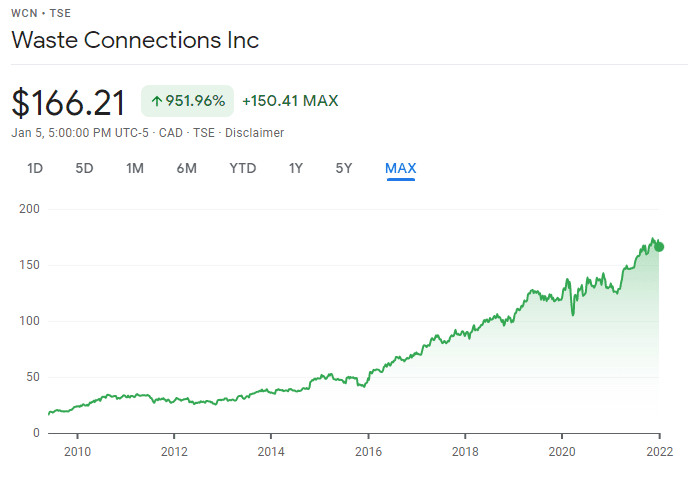

Finally, we initiated two new positions – 50 shares of Waste Connections (WCN.TO) and 100 shares of Brookfield Asset Management (BAM.A). I have been monitoring both of these companies for a while and decided to finally pull the buy trigger. Since we already own Waste Management, I wanted to add Waste Connections to increase our stake in the garbage disposal sector. Because we all make garbage and need a way to dispose of all the garbage we make, to me, the garbage sector is an easy-to-understand sector to invest in.

BMA.A happens to be Reader B’s favourite stock and the stock itself has had a significant price and dividend growth over time. I figured listening to someone that pulls in a $360k dividend a year (now up to over $400k) is a smart idea. Below is Brookfield Asset Management’s investor day presentation from 2021 that solidified my view on the company.

Many dividend investors may glance over both Waste Connections and Brookfield Asset Management due to lower than 1% dividend yields. But I want to stress that we focus on both dividend income and capital appreciation, or total return. Both WCN and BAM.A have shown solid total returns over the last 10 plus years and I believe such strong returns will continue in the foreseeable future. These two purchases are an example of focusing on low yield but high dividend growth.

I have updated our dividend portfolio to reflect the addition of these two new stocks.

Dividend Reinvestment Plans (DRIPs)

One way we have been increasing our dividends is by enrolling in dividend reinvestment plans (DRIP) and adding new shares whenever there’s a dividend payment. This is our way to take advantage of the compounding power.

We dripped the following shares in December:

- 2 shares of Brookfield Renewable (BEP)

- 2 shares of Canadian Utilities (CU.TO)

- 25 shares of Enbridge (ENB.TO)

- 1 share of European Residential REIT (ERE.UN)

- 3 shares of Fortis (FTS.TO)

- 1 share of Hydro One (H.TO)

- 1 share of Intel (INTC)

- 1 share of Coca-Cola (KO)

- 9 shares of Manulife (MFC.TO)

- 1 share of RioCan REIT (REI.UN)

- 3 shares of SmartCentres REIT (SRU.UN)

In total 49 more shares were dripped and $1,954.35 of our December dividend income was re-invested immediately. The dripped shares added $120.96 toward our annual dividend income.

Dividend Increases

December was a fantastic month. The Canadian banks announce significant dividend payout increases and every Canadian dividend investor got their Christmas present early.

- Bank of Nova Scotia (BNS.TO) increased its dividend payout by 11% to $1.00 per share.

- Royal Bank (RY.TO) increased its dividend payout by 11% to $1.20 per share.

- National Bank (NA.TO) increased its dividend payout by 23% to $0.87 per share.

- CIBC (CM.TO) increased its dividend payout by 10% to $1.61 per share.

- TD (TD.TO) increased its dividend payout by 12.6% to $0.89 per share.

- Bank of Montreal (BMO.TO) increased its dividend payout by 25% to $1.33 per share.

- Enbridge (ENB.TO) increased its dividend payout by 3% to $0.86 per share.

- Waste Management (WM) increased its dividend payout by 13% to $0.65 per share.

All these payout increases added $1,809.88 toward our annual dividend income. At 4% dividend yield, that’s the equivalent of adding $45,247 new cash to our dividend portfolio.

So yes, getting all these significant raises was indeed an early Christmas present!

2021 Dividend Income Summary

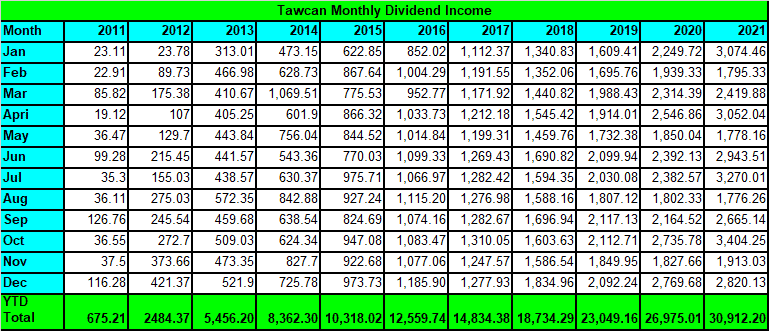

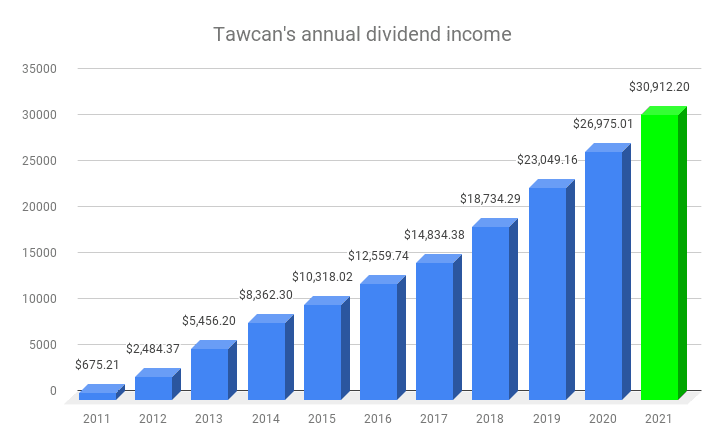

In 2021 we received a total of $30,912.20 in dividend income. Despite not meeting our dividend goal of $32,000, we still did really well. We were only short of $1,087.8 or 3.4% of our target.

Compared to 2020, we saw a YoY increase of 14.6%. Since we were aiming for an above 15% YoY growth, we were slightly below the target. We need to focus more on dividend growth in 2022.

To put things in perspective, at $30,912.20 dividend income it means…

- $3.53 per hour earning rate regardless of what we’re doing.

- $14.86 per hour of working wage assuming 52 working weeks and 40 hours a week. We are getting pretty close to BC’s $15.20 minimum wage.

2021 Dividend Income Breakdown

Every year we work hard to max out both TFSAs and RRSPs. Once we max out TFSAs and RRSPs, we then invest in non-registered accounts. We invest this way so most of our dividend income is either tax-free (TFSA) or tax-deferred (RRSP). Only a portion of our dividend income is taxed and eligible dividends are taxed quite favourable as Reader B pointed out in his excellent interview series.

Dividend income in our RRSPs will be eventually taxed at our marginal tax rate when we make withdrawals. Therefore, I have been looking into RRSP early withdrawal strategies to minimize taxes.

With that in mind, here’s our 2021 dividend income breakdown:

- RRSP: $10,996.94 or 35.6%

- TFSA: $9,122.02 or 29.5%

- Taxable: $10,793.24 or 34.9%

Comparing to our 2020 dividend income breakdown, RRSP decreased from 38.9% of our dividend income down to 35.6%, TFSA stayed the same last 29.5%, and taxable increased from 29.5% to 34.9% of our dividend income. In other words, we have made progress in decreasing the amount of income coming from our RRSPs.

For eventual income splitting and tax efficiency when we are financially independent and living off dividends, the dividend income is broken down between Mrs. T and me. The breakdowns are as below:

- RRSP: Mrs. T 31.6%, Me 68.4%

- TFSA: Mrs T 46.5%, Me 53.5%

- Taxable: Mrs. T 42.7%, Me 57.3%

So about $5,700 of our dividend income is taxed under me and $5,000 is taxed under Mrs. T. So the actual taxes we pay on our dividend income is extremely low.

Ideally, we’d like to see a roughly 50-50 split between the two of us but that may not be possible given Mrs. T’s TFSA contribution room is $10,000 less than mine and that I only started contributing to the spousal RRSP in 2016.

2021 Dividend Portfolio Performance

The stock market was on a roll in 2011 and everyone and anyone seemed to make money. Just how well did the market return in 2021?

TSX posted a 21.7% return.

S&P 500 posted a 26.9% return.

NASDAQ posted a 21.4% return.

All of a sudden, everyone is an investment expert and making money quickly via the stock market was easy. It will be interesting to see what happens in the next market downturn.

In the past number of years, we have been very lucky to have beat the TSX return. We managed to do the same in 2021. In fact, our dividend portfolio returned 32.8% when excluding all the contributions we made throughout the year. If we counted the contributions, that return number was much higher.

Will such an amazing return continue in 2022? I certainly won’t hold my breath over that.

Dividend Income – Summary and Looking Forward

2021 was a very solid year for us both from a dividend income front and total return front. I’d never imagined seeing a return of 32.8% excluding contributions.

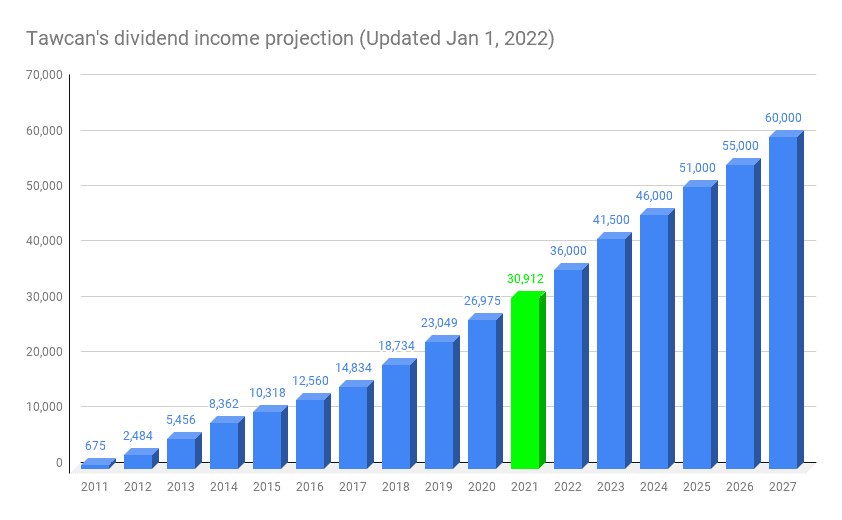

Where do we go from there? For 2022, our goal is to receive over $36,000 in dividend income per our dividend income projection. Per the chart below, we are still aiming to receive over $50,000 in dividend income by 2025 and be able to live off dividends. Per the recent retirement projections from Cashflows And Portfolios, we should be on track with this target.

Here’s to a fantastic year ahead and receiving over $36,000 in dividend income.

Happy investing everyone!

Congratulations on a great year, wishing you much success this year as well. Great summary.

mb

Thank you.

A solid year Bob! You’re making great progress! 15% dividend growth y-o-y is great!

I’m not able to put in as much capital these days, so our dividend growth is mostly tied to dividend raises at the various assets we own. Still, it’s a very sizeable amount of income these days!

Thank you Mr. Tako.

Well done, Tawcan! Continued success in 2022. I enjoy reading your posts.

Thank you C.

Hi Bob!

Congratulations on your dividend growth progress! The details you share are quite helpful.

I have mentioned in my previous comments, and I would like to reiterate: I appreciate your blog very much! I have learned a lot from your posts in 2021 & I would not be where I am now financially without your blog

My goal in 2022 is to gradually rebalance my stocks so that each company proportion gets below 5% of the overall portfolio… I have created pivot piechart of my stocks and was shocked how my portfolio is way too heavily concentrated in tech companies

Thank you Sarah, you’re too kind.

Hi do you have instructions somewhere on how to calculate dividend income from Questrade and TD bank?

Hi Louise,

Sorry, what do you mean by how to calculate dividend income?

sorry like how did you calculate your dividend income? In TD is it under Accounts -> Gains & Losses? Do you also know how to do it in Questrade?

I’m inspired by your graphs and chart and want to create something similar for myself, but not sure how.

Accounts -> Activities to see what you have received in your accounts.

All the charts and graphs were done in Google Spreadsheet.

thanks for sharing 🙂

bam! another great month Bob.

looks like a good time on the hill.

Huge dividend growth and raises especially!

1 month of dividend raises with that 4% yield is more than I invest in a year. haha gotta love it!

keep it up man

cheers

Thanks Rob.

Hello Bob, congratulations on the re-cap of 2021!

Question for you in the indices performance in 2021: Are these the total-return (dividends reinvested) indices, or just the increase in the share prices? Please let us all know. Thanks.

Thank you. From what I can find those returns are with dividends but not reinvsted.

Thanks. I am curious as to the source of the index returns. The “official indicies” do not consider the dividends paid of their holdings. The total return Index reinvests the divìdend based on the closing price of the security on the day the dividend is paid. The re-investment is made without any commission, which frequently is not accurate.

My suggestion is if you are comparing your portfolio’s performance to the index, you should be using the total return version of the index for an accurate comparison. Please let me know your thoughts. Thanks.

Total return for indices typically means index performance + dividends. It’s harder to calculate the return with dividends reinvested.

Congrats on a nice financial finish to the year! I love your charts. They really show a colorful display of your impressive progress over the years. Nicely done! 🙂

Thank you My Dividend Dynasty. The charts are very motivating that’s for sure.

Thanks for sharing your financial journey! It is most impressive!

I’m wondering how many stocks you hold in your tfsa and how many stocks Mrs. t. holds in her tfsa.

Thanks. I love your blog!

Jb

Thank you Jill. You can see our portfolio here – https://tawcan.com/dividends/

I think we each hold about 12-14 stocks in our TFSA.

I’m surprised you sold all UL.

To me it’s a buy and forget to sleep well at night. Worldwide exposure on items people need.

Stable dividends for years .

In fact with the GSK deal I’m buying more tomorrow when the price goes down.

Many of your other stocks are sideways or have been going down like SU, KO.

I’m scratching my head about literally buying a gamble in Nevada (Vici ) from a stable dividend payer

It is a solid stock but it hasn’t done much over the last 5 years. We already own PG so UL is perhaps a little redundant.

That’s an incredible 2021 return Bob, well done. 🙂 I think a lot of growth this year will come from bank earnings. How do you think higher interest rates will affect bank stocks? I think it’s good as long as rates don’t move up too much too fast. Good luck with the $36,000 dividend goal this year!

Thanks Liquid, I was surprised with the returns, especially after excluding contributions. Buying a lot of banks in 2020 definitely paid off.

I don’t see interest rates affecting bank stocks all that much, the price should already be built. I can’t see a sudden 1% interest hike. It will be many small incremental increases IMO.

Hi Bob

Amazing photos. You have a very beautiful family. Sorry for your loss.

It is great to see the growth both in monthly payouts and the annual dividend growth. It is inspiring and shows how being consistent pays out.

I started my Dividend journey in 2021 and currently sitting at your 2016 level including the income from my leftover in GICs. Hopefully, I see the growth you saw to keep going.

And wow! Your plan to get up to $60K in couple years is fantastic. Wishing you (and myself) all the best.

Have a great 2022 🙂 Full of joy, success, and growth.

Thank you Mr. Dreamer.

Congrats on getting started with dividends. It takes years to build up your dividend income stream. Keep it up.

Thank you for this post. Please consider having Reader B back on your site for another interview. I learnt a lot from your interview with him. I wanted to ask if you had any suggestions or tips on starting new positions at these elevated market levels. I have a list of stocks I want to hold (hopefully for life!) and am planning to dollar cost average into the positions. I will need to use the dividend income in about 4 -5 years for living expenses.

You’re welcome. Will see what I can do with Reader B.

If you’re planning to hold a list of stocks for life, what’s preventing you from buying them? Would you regret if you don’t buy them if the price never get to your desired entry point?

Woww this is an amazing end of year run up! Hope you enjoyed your time off!

Thanks Alex, enjoyed my time off. 🙂

Hey Bob, well done on beating the TSX! When you calculate 32.8% are you including all the distributions made by the companies throughout 2021?

I remember reading somewhere if one overweights the dividend payers on the TSX 60, one will outperform the TSX 60. I think that also holds true for the S&P/TSX Composite Index too.

Cheers

Thank you. Yes, I included the distributions made by the companies but I’m not including any contributions we made in 2021.

Congrats Bob on a Steller year!

Yes certainly a nice month for Dividend increases 🙂 I wonder if the banks will do anything more in 1H2022?

I see you have a significant holding in ENB (25 DRIP, wow!) It is one of my largest holdings right now, but I am cognizant of the share price being essentially flat over the past past 5 years. Div growth and yield of course help ENB in this situation.

My question re diversification: Do you have a hard and fast rule on MAX weight in your portfolio for an individual equity?

Thanks and be well,

Josh

Thank you Josh. I think the Canadian banks will raise more dividends in 2022. Not sure if it’ll be in 1H2022 though.

For individual dividend stocks, we try to stay below 5% of the overall portfolio. There are a few stocks that are a percentage or so higher than 5% and ENB is one of them.