I don’t typically write about current events and I have been trying to stay away from politically-related posts on purpose. Lately, however, is it harder and harder to not write about them.

I am deeply saddened by what’s going on in the US lately. Months after the innocent killing of George Floyd and after many Black Lives Matter protests globally, things have not improved at all. The recent incident of Jacob Blake who was shot in the back by the police seven times is the latest example of the social injustice that black people face. A few days after the Blake shooting, a white 17-year-old killed two people and wounded another with a semi-automatic rifle during a protest over the police shooting of Jacob Blake.

Hundreds of years ago, it was common to carry swords in China and Japan. But you don’t see people walking around with swords in these countries anymore.

So why is it OK that carrying a gun is still OK?

Sure, it’s the constitutional right.

But..

Do we still live in the wild wild west where we have to protect ourselves from outlaws and bandits every day?

Given what’s going on in the world, it is hard to sit down and write about personal finance, money, and financial independence.

If you’re reading this, I strongly encourage you to learn more about discrimination and prevent and stop this terrible act. Help to change and improve this world!

Now, if you decide to unfollow this blog or unsubscribe to the email list because of what I wrote. So be it. If you think discrimination is OK, I’m sorry. For the betterment of yourself, I truly hope you can get educated and change your view.

Dividend Income

Back to the main topic of this post… dividend income. In August 2020 we received dividends from the following companies:

- Apple (AAPL)

- AbbVie (ABBV)

- Brookfield Renewable Corporation (BEPC/BEPC.TO)

- Bank of Montreal (BMO.TO)

- Costco (COST)

- Dream Office REIT (D.UN)

- Dream Industrial REIT (DIR.UN)

- Emera (EMA.TO)

- European Residential REIT (ERE.UN)

- Granite REIT (GRT.UN)

- H&R REIT (HR.UN)

- Inter Pipeline (IPL.TO)

- KEG Income Trust (KEG.UN)

- National Bank (NA.TO)

- Omega Healthcare (OHI)

- Procter & Gamble (PG)

- RioCan REIT (REI.UN)

- Royal Bank (RY.TO)

- Starbucks (SBUX)

- SmartCentres REIT (SMR.UN)

- AT&T (T)

- Verizon (VZ)

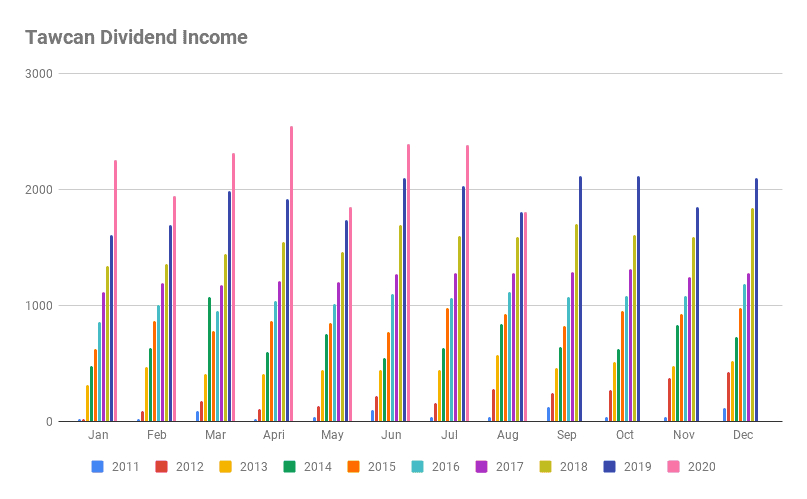

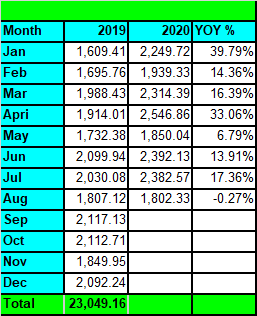

With 22 cheques deposited in our investment accounts, these cheques added to $1802.33, the lowest amount we have received so far in 2020. Typically February, May, August, and November are our weakest months in terms of dividend income, so it wasn’t a surprise to see our monthly dividend income to be below $2,000.

The August dividend income was a bit lower than the previous quarter (i.e. May) mostly because we had closed out our position in Laurentian Bank.

For those sharp-eyed readers, you probably wondered how we received dividends from Brookfield Renewable when the dividend payment is in September. Recently, Brookfield Renewable went through a merger with Terraform Power. The merger created one of the largest renewable platforms globally. Brookfield Renewable then did a stock split and created a new entity called Brookfield Renewable Corporation (BEPC), which is more tax efficient. With the stock split, each BEP unitholder received one share of BEPC for every four BEP units held. Because our shares did not divide evenly, we received some cash as a result. I figured I would count the cash as dividend distributions.

Of the $1802.33 dividends received, $432.48 was in USD and $1,369.85 was in CAD. Or about a 25-75 split. Long time readers would know that we did not convert USD to CAD when reporting our dividend income. Instead, we used a 1 to 1 currency rate approach. Why? Because we wanted to avoid fluctuations in dividend income over time due to changes in the exchange rate.

Curious about our dividend approach and our dividend investing strategy? Check out our dividends page.

The top five dividend payouts for August came from Bank of Montreal, Emera, National Bank, Royal Bank, and Omega Healthcare (not in order). The top five dividend payers contributed $1,187.32 in dividends toward our August dividend income or 65.9%.

Dividend Growth

We saw a -0.26% YoY growth compared to August 2019. This was the first negative YoY growth since 2011. Needless to say, we were very disappointed.

Considering that we closed out Laurentian Bank and re-invested the money elsewhere, we were expecting this subpar YoY growth. We used to receive ~$100 in dividends from Laurentian Bank. It was comforting to see that we almost made up the difference after only one quarter.

If we compared the total dividends received to date between 2020 and 2019, we saw a 17.5% YoY growth. With four more months to go, it would be great if we could continue to see the overall YoY growth to be above 17.5%.

Dividend Income – Account Breakdown

Our dividend investing goal is to be as tax efficient as possible. To do so, we hold Canadian dividend paying stocks in RRSPs, TFSAs and regular accounts. All REITs and income trusts are held in TFSAs for tax efficiency purposes. All US dividend paying stocks and ADRs are held in RRSPs to take advantage of the tax treaty between Canada and the USA.

To summarize:

- TFSA: Good for Canadian dividend paying stocks, REITs, and income trusts.

- RRSP: Good for US dividend paying stocks, REITs, and income trusts.

- Taxable: Good for Canadian dividend paying stocks that pay eligible dividends.

Why are TFSA and RRSP great vehicles for retirement savings? Check out the following guides:

Here’s our August dividend income breakdown:

- Taxable: $470.25

- RRSP: $836.96

- TFSA: $495.12

Dividend Stock Transaction

Although we have added over $70,000 to our dividend portfolio in 1H 2020, we will be slowing down our purchases for the remainder of 2020. Usually, we contribute to our TFSA in early January to max out the annual contribution limits. We also try to max out our RRSP contribution limits by around April. Once our TFSAs and RRSPs are maxed out, we then start contributing to our taxable accounts.

As a result, the majority of our dividend stock transactions happen in the first half of the year. In the second half, we try to continue adding cash to our investment accounts but our focus shifts to saving money for next year’s TFSA and RRSP contributions.

With that in mind, we purchased 18 shares of Bank of Nova Scotia at $56.95 per share in August. This transaction added $64.80 toward our annual dividend income.

Dividend Reinvestment Plan (DRIP)

As dividend growth investors, our goal is to live off dividends when we are financially independent. To do so, we need to make sure our dividend income can keep up with inflation.

Since we are still in the accumulation phase, the key driver for our dividend growth comes in the form of purchasing more dividend paying stocks with new capitals. As the value of our dividend portfolio grows and the amount of dividend income increases, it becomes harder and harder to generate more dividend income by adding new capital alone.

Therefore, it is important to rely on the two other important methods to grow our dividend income.

The other two methods are organic dividend growth and dividend reinvestment plan (DRIP). While we can’t control how much companies raise their dividend payouts (i.e. organic dividend growth), we can control whether we reinvest dividends or not. To keep things simple, one of our dividend growth investing strategies is to enroll in DRIP whenever we are eligible. This means when we purchase dividend paying stocks, our goal is to eventually hold enough shares so the dividend amount is greater than the stock share price.

For those of you that aren’t familiar with DRIP, there are two types of DRIP – full DRIP and synthetic DRIP.

Full DRIP means you can purchase fractional shares. To set up a full DRIP, you need to use the company’s designated transfer agent. Enroll in full DRIP requires you to follow a long process by getting a share certificate as the first step. After a bit of research, we did find one Canadian broker, ShareOwner, allows for DRIPing fractional shares. This was the key reason why we set up our kids’ dividend portfolio with ShareOwner.

With synthetic DRIP, you can only purchase full shares. Synthetic DRIP is what discount brokers like TD, Questrade, RBC, Interactive Brokers, etc, offer.

To entice shareholders, some companies offer DRIP discounts. For example, CIBC offers a 2% DRIP discount and European Residential REIT offers a 5% DRIP discount. It is important to note that not every discount broker honours the DRIP discount. For example, if you enroll in DRIP with TD, you will get the DRIP discount. If you enroll in DRIP with Questrade, you won’t get the DRIP discount.

If a discount broker honours the DRIP discount, it can take up to two weeks before the dividend payment and the DRIPed share(s) show up in your account. Many new dividend growth investors do not know this detail and they often freak out because they have not received their dividends on the dividend payment date.

In August, we were able to DRIP the following stocks:

- 1 share of Bank of Montreal

- 1 share of Dream Office REIT

- 1 share of Dream Industrial REIT

- 1 share of Emera

- 1 share of European Residential REIT

- 3 shares of H&R REIT

- 3 shares of Inter Pipeline

- 2 shares of National Bank

- 4 shares of Omega Healthcare

- 3 shares of RioCan REIT

- 4 shares of Royal Bank

- 2 shares of SmartCentre REIT

- 2 shares of AT&T

These 28 shares added up to $1,010.91, resulting a DRIP ratio of 56.1%. By dripping additional shares, we increased our forward dividend income by $57.92, or an equivalent of 5.72% dividend yield.

Financial Independence Journey Update

At the beginning of this year, I set a goal of having a 55% dividend income to expenses ratio. I picked 55% because we have been spent around $55,000 annually and I thought we could receive $30,000 in dividend income. After staying at home mostly and working from home for more than five months, I have realized that this year’s annual expenses should be much lower than $55,000. This should help us in hitting the 55% ratio given many companies have reduced dividends.

At $1,802.33, our August dividend income covered the following expenses:

- House insurance

- Car insurance

- Life insurance

- Groceries

- Household items

- Car gas

- Phone & internet

- Natural gas

- Hydro

- Charity donations

In August, we spent more than the previous months. The higher spending in August was mostly caused by the pre-school payment, credit card annual fees, and chocolate and chocolate mould purchases (for Mrs. T’s Christmas chocolate production).

Despite a higher expense month, August dividend income was able to cover 42.1% of total expenses. Living off dividends in the future is definitely achievable in the near future.

Summary

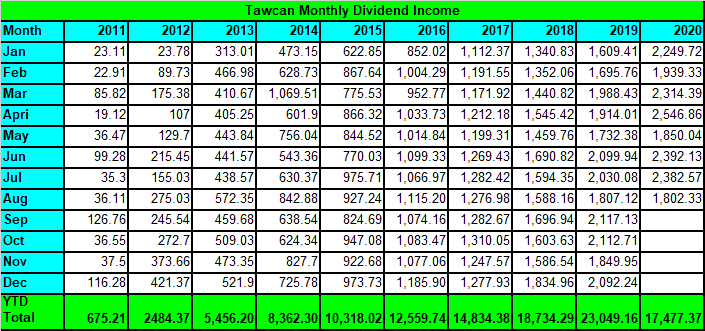

After eight months we have received a total of $17,477.37 in dividend income. This is an equivalent of $2,184.67 per month. We are extremely grateful for building up our dividend portfolio so our money can work hard for us. Given what’s going on in the world, we feel very fortunate that we live in Canada. We are extremely grateful and appreciative of not having to worry about things like health insurance and being treated unfairly because of our skin colours.

More than ever, we are more and more conscious of where we purchase things and how we are spending our money. Given the global pandemic, we are buying more local to support local businesses. We have donated money to charities that promote social equality.

Despite our dream of becoming financially independent and living off our dividend income one day, I want this world to be a better place. I want my kids to treat everyone equally regardless what their skin colour, gender, sexual orientation, religion, disability, age, etc. The best way to teach my kids is to show them through my own actions. We must improve and evolve as a society. We can’t continue making the same mistakes. Let’s all be better!

Hey Bob,

Congratulations again on your monthly dividend income record. I am in no way close to where you are but we will just keep on adding as much as we can. Have you maxed out your RRSP, TFSA, and RESP contribution? After that do you go for margin and non-registered accounts?

Thank you myprudenlife. Yup, we have already maxed out RRSP, TFSA, and RESP at the beginning of this year. After that we’d put the money in taxable accounts.

Hi Bob,

I’m glad to see others talking about racial injustice. Bravo!

I really like seeing the incredible progress over the years. Great job! I’m also impressed that you’re able to get a consistent amount of dividends each month. This is one that I’ve been struggling with. How do you do it? Is it the REITs?

What other options are there for fractional share DRIP?

Are you still using Canadian Shareowner? Maybe you have noticed that they are transitioning all accounts to Wealthsimple. Wealthsimple currently does not offer any DRIPs. I like the commission free trading but no DRIP leaves me wondering if I should move to another platform like Questrade. Could you discuss this in a future post?

Thanks

I’ve noticed that, I’m working on a post about ShareOwner. 🙂

Nice Bob.

The political views are interesting. Something really needs to change for sure. I kinda touched on it on my post but I feel for the cops as well. They must be on edge constantly these days.

Look at those 2 cops who just got ambushed and shot. Then they went to the hospital and BLM went there and were outside saying they will finish them.

Crazy times..

Less guns would be a great start right? Sounds so easy…

Love all your divs and I completely forgot I got that cash payment from bep as well.

Your drips are insane! that snowball will only grow faster.

wow ms T getting christmas chocolate ready already? haha nice! I love Christmas.

cheers man

Incidents shouldn’t all end up with someone firing their guns. Less guns will probably help with the overall situation.

Your expenses coverage from dividend income is so impressive! Do you guys still have a mortgage to cover?

Preschool fees- how exciting! Did your child get preschool cancelled in March? We started preschool for our older one last week 🙂

Thanks! Yea both our oldest and youngest are in school this year. Youngest three days a week only. It will be weird working from home and being so quiet. 🙂

Hey Bob,

Thanks for going out on a limb to share your thoughts on the current political climate. Challenging times and hopefully we see positive change come about as a result. Horrible to see the destruction and people fighting against one another.

As far as the income goes, great work. The Feb-May-Aug-Nov quarterly schedule is the worst for myself, as well. Always hard writing the updates when they’re so much lower than the other months, but it all balances out in the end.

I bought my REI.UN shares back in August 2009 and sadly didn’t realize at the time that I could have put them in my TFSA. Due to the naming convention of “Tax-Free SAVINGS Account”, I thought it was just a spot to park some cash (which I think is the misconception plenty of people still have). All the same, I’m maxed out at this point and loving the tax-free compounding.

Take care,

Ryan

Thank you Ryan. I hope we can do less finger pointing and treat each other better.

I hope you didn’t purchase REI.UN in your taxable because that’s a bit of a tax nightmare.

Haha, I would like to write about political issues in mainland China, but since I’m afraid of getting arrested and blocked from leaving I avoid doing it. Political events generate a lot of interest but they can really be a hot button.

I don’t blame you. 🙂

Don’t get me wrong, I simply wanted to make sure that people understand that discrimination is not OK.

It’s important that we keep talking about this stuff, so I’m glad you are. Money is VERY political, there’s no way around that. And it’s so hard to read bloggers who only talk about money and don’t acknowledge what’s going on in the world around us. Police here have only escalated their brutality in the past months and it’s horrifying.

We need to look at both sides of the story and try to walk in both side’s shoes before coming to a conclusion. My key point is that shooting someone in the back, especially when you have grabbed them by the shirt, is not OK IMO.

I love how you’re using your platform to talk about things that are meaningful to you. Good job!

Last year alone, 14 (FOURTEEN!) unarmed blacks were killed by the police. Even 1 death by police (unarmed) is too many, so this # is simply unacceptable and further actions need to take place.

Regarding Jacob Blake, however, he had recently, allgedly, sexually assaulted (raped) a girl. (Where is the girl’s justice?) Therefore: Police wanted to take him for questioning. Why was Jacob Blake disobeying the police’s order? Why was he resisting arrest? Why was he going to his car? Was he to get to his weapon, which was later found under his seat?

There are a LOT of questions that are unanswered in this case, and I wouldn’t make a judgement call without knowing further information. The entire BLM movement has a case to be made, but they’re not helping their situation by further instigating hatred/violence towards the police.

Keep up the good work, Tawcan. It is good to see this coming from you as it takes courage.

Agree that there are a lot of questions regarding Jacob. But ask this question… would a white man get the same treatment as Jacob? Most likely not. There appears to be differential treatments when it comes to coloured people, especially black people and that’s not OK.

I just cannot comprehend shooting someone in the back when the police had grabbed Jacob by the shirt already.

Agreed. The treatment of blacks are absolutey different than that of whites.

Though I dug up stats and noticed that 25 (!) unarmed white men were killed. This brings the total up to 39. THIRTY NINE lives lost… that could’ve and should have been prevented. So the issue is definitely larger and I am positive it will be addressed.

Not only did they shoot Jacob once, he got shot multiple times. That is bad policing.

No need to worry about a negative year over year result. You are more than on track to best your 2019 totals and that’s what really counts on an annual basis. August still brought in a hefty amount passively and that’s a great achievement. Keep on buying, dripping and enjoying those raises when they come!!!

Thank you DivHut. We’re on track to beat what we received in 2019 so we’re already quite grateful about that.