Hello everyone, welcome to another monthly dividend income update.

I have been writing these monthly dividend income updates since I started this blog back in July 2014. Why do I keep writing these monthly dividend updates? One, to keep us accountable and show how our financial independence journey progress. Two, to demonstrate that it is possible to build up a sizable dividend portfolio over time and eventually live off dividends.

After a really busy February involving oversea travel and a new job position, it was nice to have a more relaxing month in March.

In March, Mrs. T’s family came for a visit from Denmark and we spent a week in Whistler, skiing for five straight days. It was the first time for us taking our kids to Whistler.

Despite skiing in the middle of March, the snow condition was excellent. The first three days we had fresh powder (10-25 cm overnight each day), then two blue bird days. I even got a bit of the famous “reverse panda tan.”

Given how big the Whistler Blackcomb ski resort is, we were worried that we’d get separated while skiing. We had to remind both kids to follow one of us and always stop whenever there were multiple paths on the trail.

We did quite well, except for one time. On one of the runs, Pika’s Traverse, Kid 2.0 didn’t see me making a left turn and continued to ski down a different run for about 20 metres. I had to go after her and then walk up the hill together to get back to the correct run.

Another traumatic incident was that on the second day of the trip, Kid 1.0 didn’t get on the chair lift with us and had to take the next chair by himself. For the rest of the trip he made sure he was the first one to line up at the chair lift and paid a lot of attention to make sure he wasn’t left behind.

A good example of live and learn!

At end of the week, I was quite impressed at how much both kids have improved on skis. They even managed to go down a black run with relative ease.

We also had a lot of fun skiing with Mrs. T’s family and spending time with them.

Since both Mrs. T and I used to spend a lot of time in the mountains before kids, we really miss the beautiful snowy mountain views. While the trip was really expensive (the hotel room was over $500 per night, lift ticket was around $85 per day), we had a great time and felt it was money well spent.

After the two week spring break, we started cleaning up the backyard garden. Mrs. T ordered five yards of mushroom manure so I spent quite a few evenings shovelling smelly manure, and filling up the backyard garden.

We are looking forward to another year of awesome harvest from our backyard garden. Nothing beats fresh organic produce.

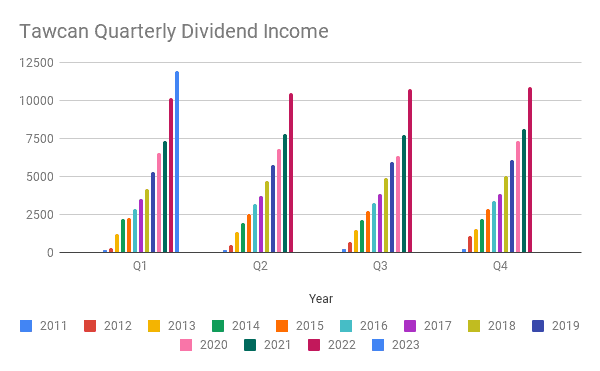

Dividend Income – March 2023

Back to dividend income…

In March 2023 we received dividends from the following companies:

- Brookfield Asset Management (BAM.TO)

- BlackRock (BLK)

- Brookfield Renewable Corp (BCEP.TO)

- Brookfield Corporation (BN.TO)

- Canadian National Railway (CNR.TO)

- Canadian Tire (CTC.A)

- Dream Industrial REIT (DIR.UN)

- Enbridge (ENB.TO)

- Fortis (FTS.T)

- Granite REIT (GRT.UN)

- Hydro One (H.TO)

- Intact Financial (IFC.TO)

- Johnson & Johnson (JNJ)

- McDonald’s (MCD)

- Manulife Financial (MFC.TO)

- Magna International (MG.TO)

- Metro (MRU.TO)

- PepsiCo (PEP)

- Qualcomm (QCOM)

- RioCan REIT (REI.UN)

- SmartCentres REIT (SRU.UN)

- Suncor (SU.TO)

- Target (TGT)

- Visa (V)

- Waste Connections (WCN.TO)

- Waste Management (WM)

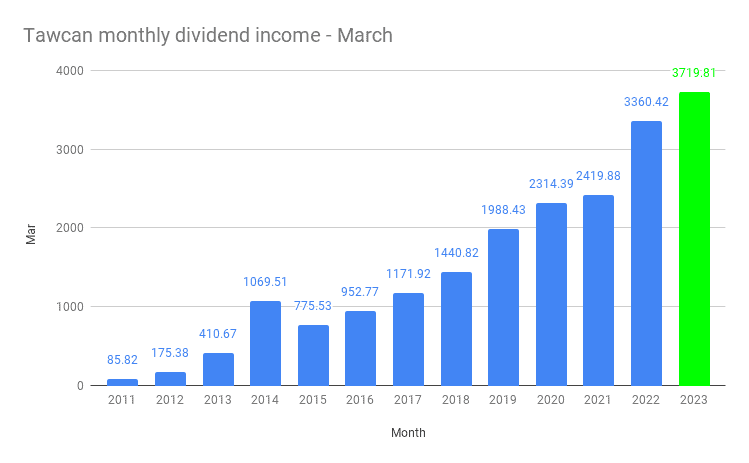

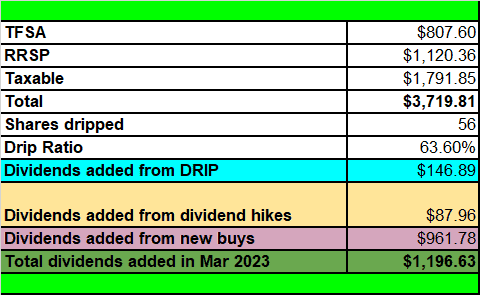

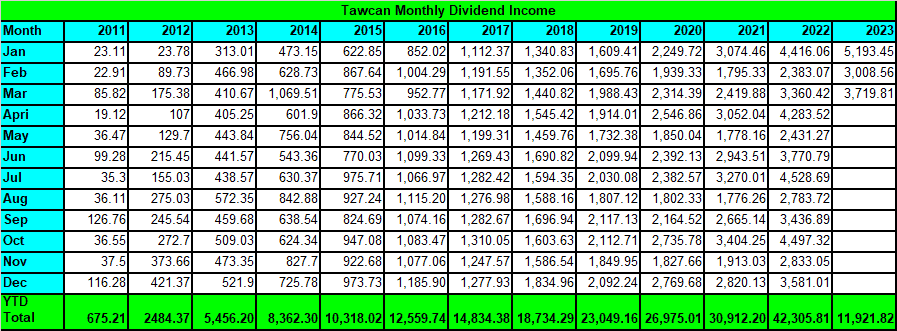

The 26 dividend pay cheques that we received added up to $3,719.81. We feel blessed and very appreciative that our dividend portfolio generated over $3,700 for us in March without us having to do anything.

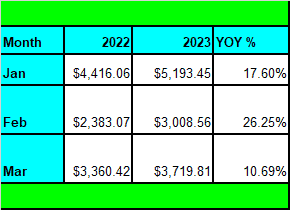

Compared to March 2022, we saw a YoY increase of 10.69%. Despite being the lowest monthly YoY increase so far in 2023, over 10% is still very respectable, especially considering our monthly dividend income is already quite sizable.

Out of the $3,719.81 received, $409.75 was in USD and $3,310.06 was in CAD or roughly a 10-90 split. Please note, we do not convert USD to CAD when reporting our dividend income. This is our attempt to keep the math easy and avoid fluctuations in our monthly dividend income due to the constantly changing exchange rate.

March’s top five dividend payers were Brookfield Renewable Corp, Fortis, Enbridge, SmartCentres REIT, and Manulife (not in order). These five dividend payers accounted for $2,683.96 or 72.2% of the March dividend income.

Dividend Hikes

We saw a long list of companies raising dividends in February, so the March list was relatively short in comparison. Despite that, I still did my usual small celebration dance whenever I see a dividend hike, because I love getting a raise from dividend stocks that we own without having to do anything.

- Canadian Natural Resources (CNQ.TO) increased its dividend payout by 6% to $0.90 per share.

- Power Corporation (POW.TO) increased its dividend payout by 6.1% to $0.525 per share.

- Qualcomm (QCOM) increased its dividend payout by 7% to $0.80 per share.

These three dividend hikes increased our forward annual dividend income by $87.96.

Dividend Reinvestment Plan (DRIP)

In March we dripped the following shares:

- 3 shares of Brookfield Renewable Corp

- 29 shares of Enbridge

- 3 shares of Fortis

- 13 shares of Manulife

- 2 shares of RioCan REIT

- 5 shares of SmartCentre REIT

- 1 share of Suncor

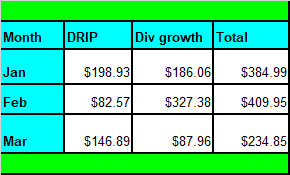

These dripped shares added $146.89 toward our annual dividend income.

Thanks to organic dividend growth and DRIP, we added a total of $234.85 toward our annual dividend income in March.

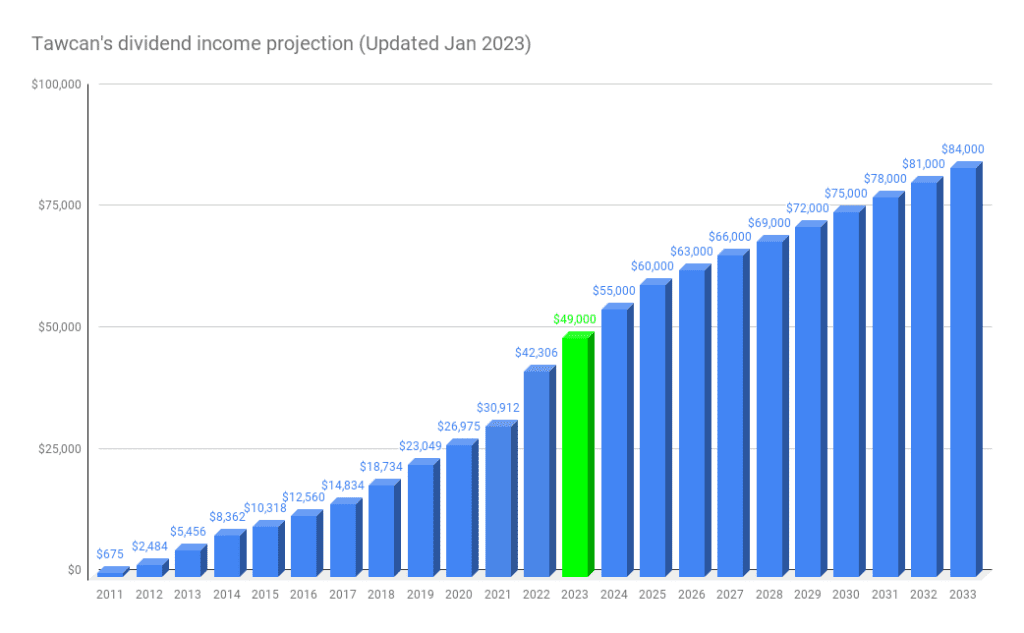

As you can see from the above table, after one quarter, we have increased our forward annual dividend income by $1,029.79. At a 4% dividend yield, that’s the equivalence of investing $25,744.75 worth of new capital in our dividend portfolio.

Moving forward, we need to rely more and more on DRIP and organic dividend growth to grow our dividend income as we face the law of the big numbers.

Some readers look at the dividend income projection above and my dividend growth calculations/simulations and think we have to invest over $167k worth of new capital in our portfolio this year. But the reality is, the actual number is a lot lower than that, thanks to dividend hikes, organic dividend growth, and the compounding effect.

Dividend Transactions

In January and February, we have been busy on the dividend buying front and purchased. Below are dividend paying stocks that we’ve purchased in those two months:

- 172 shares of Brookfield Asset Company (BAM.TO)

- 128 shares of CIBC (CM.TO)

- 157 shares of TC Energy Corp (TRP.TO)

- 63 shares of Enbridge (ENB.TO)

- 30 shares of National Bank (NA.TO)

- 70 shares of Telus (T.TO)

- 57 shares of Bank of Nova Scotia (BNS.TO)

- 67 shares of TD (TD.TO)

- 66 shares of Royal Bank (RY.TO)

- 25 shares of Canadian National Railway (CNR.TO)

We kept ourselves busy throughout March on the buying front as well. In March we purchased the following dividend paying stocks:

- 178 shares of Telus (T.TO)

- 80 shares of TD (TD.TO)

- 119 shares of CIBC (CM.TO)

Just slightly under $19,000 was deployed with these three purchases and we added $961.78 toward our annual dividend income.

Many readers will look at the list of stocks we’ve added in Q1 and think, wow Bob and his wife must make A LOT of money. That’s not realistic and relatable. Some explanation…

- We usually do the bulk of our purchases in the first half of the year. We save up money from the previous year to max out our TFSA and RRSP contribution rooms early in the year. This year we were able to add $13,000 to our TFSA.

- As mentioned, my previous company got acquired in early January and I received cash payment for all the equities (Restricted Stock Units, RSUs) I had.

- Another acquisition condition was that the new company would pay out over 100% of the 2022 salary bonus, which I received in March.

- Cash from maturing of the RSUs and the 2022 salary bonus got us a lot of cash in Q1 2023 to deploy. This was extremely unusual and we don’t believe will repeat.

- We also have a relatively high savings rate, which allows us to invest a large amount of new capital each month.

- Furthermore, we reinvest 100% of our dividend income.

Basically, all the stars aligned for us so far in 2023 and allowed us to deploy a large amount of cash. In Q1 we added about $83k worth of dividend paying stocks, from a combination of savings and reinvested dividends.

We expect the cash deployment to slow down significantly for the rest of the year. We also expect to contribute less money in 2024 because I don’t expect any RSUs to mature or the bonus will be a lot less (if I get anything at all).

Financial Independence Journey Progress Update

When my wife and I started building our dividend portfolio in 2011, we had a goal to eventually live off dividends by 2025. Since we are about 2 years away from this target, we have been tracking our financial independence journey progress quite closely.

In 2022 our total core spending was $40,563.19 CAD and our 2022 annual dividend income was $42,305.81. This meant we had a dividend to core expenses ratio of 104.3%.

After three months, we have received $11,921.82 in dividend income and spent $10,910.10 in core expenses. This means our dividend income covered 109.3% of our core expenses so far in 2023. In some sense, you can say that we’re well on our way to living off dividends!

Please note that core expenses only cover the basics like food, mortgage, property taxes, utilities, household items, clothing, health expenses, car gas, and other essential items.

Core expenses do not cover things like entertainment, eating out, vacation, charitable donations, gifts, etc. Since vacation and eating out can fluctuate year to year depending on what we do, I decided to not use these numbers when calculating the dividends to expenses ratio.

In case you’re curious, if we exclude vacation-related expenses, our dividend income covered 81% of our expenses so far in 2023. Pretty solid considering we ate out a lot the first three months and had some pretty big dining out bills (like paying for 15 people for a birthday dinner and paying for 9 people a few times while in Whistler).

Overall, we are very pleased with our financial independent progress.

Dividend Income – March 2023 Summary

For this month, I decided to borrow the score card idea from Josh at Money Making Habits. I think it’s really cool to see a summary of the monthly dividend income and dividend added from the various sources in one table. I plan to continue with the score card in future monthly dividend income updates.

It’s pretty amazing that we were able to add $1,196.63 toward our annual dividend income in March!

Looking at the yearly dividend income, we have received a total of $11,921.82 after three months.

What’s unbelievable is that we have already exceeded the total dividend income we received in 2015. Based on my projection, by end of April, I’m quite certain that we will exceed the total amount from 2017.

Talk about the power of compounding!

We feel extremely blessed and thankful that our money is working hard for us so we don’t have to. We also feel very lucky that the stars aligned so far this year and allowed us to deploy a significant amount of money. Furthermore, a volatile market has allowed us to add dividend paying stocks at a discount.

Per usual, putting things in perspective, our dividend income is equivalent of:

- $132.46 per day or $5.52 per hour. This is an increase of $16.55 per day compared to the end of 2022.

- $22.93 hourly wage or $183.41 per day after 13 weeks of work. This is an increase of $20.70 per day compared to the end of 2022.

It’s pretty neat that our dividend portfolio is generating more money than BC’s minimum wage. Essentially, our portfolio is like us having another job, except we don’t have to do anything.

April is gearing up to be a big dividend income month for us. Hopefully, we can set an all-time monthly record again (we broke that back in January this year). I’m excited to see what we’ll end up with.

Amazing Bob! Well done! Impressive seeing the power of the DRIP shares and the forward income it adds every time.

Hi Bob, I plan to eventually reach out to you privately for a coaching session, but may I ask when you first started investing. Was it strictly through your RRSP or TFSA? I’m novice to this whole thing, but hope to learn through your blog and with your help!

Hi Justin,

When we first started we focused on RRSP And TFSA first but quickly branched out to non-registered too.

I love reading about your adventures outside investing. How about some gardening tips? My husband and I moved to the west coast a few years back, and gardening has been trial and error. Mostly error ☺️

Thank you Laura, will try sharing some gardening tips.

Hi Bob. Just to update you this is what Questrade is telling me in required to dividends in US funds after I had it elevated to the next level manger.

Hi Gregory,

I hope you are doing well. My name is Mandy and I am emailing to follow up on a recent conversation with Sanaa regarding a recent dividend payment.

Kindly be advised that although the Algonquin Power & Utilities Corp (ticker symbol: AQN.TO) dividends are received in USD, since you hold the positions on the Canadian exchange, the dividends received are automatically converted to CAD. I apologize for the confusion and appreciate your understanding.

If you have any questions regarding this case, please reply to this email for prompt responses. For all other inquiries unrelated to this case, our client services team will be happy to assist you.

Thanks,

Mandy

Support Specialist, Client Services

Ah, thanks for the update Greg. Looks like you’d have to hold the US listed ones to get dividends in USD.

Thanks for the update.

Glad you had a great time at whistler. We’ve been wanting to go for years but it’s so painful looking at the prices . On principle I will not spend almost $1000 for a room. Thought about a day trip but that would be stressful driving.

Grouse is the go to place for us but the weather and parking are so unpredictable. Maybe when kids are 7-8 we’ll go to whistler or sun peaks .

Yes , March dividends for us have gone up bigly. It’s nice to see all those deposits filling up my coffers.

Bought CM, TD with the recent bank crisis . Couldn’t resist the 6% yield on CM. Also ENB and BAM. Also more BIL etf on the US $ side

Thanks Dad MD. Whistler was a lot of fun but yes, very expensive. Grouse we’ve found it’s a hit and miss in terms of parking and weather.

Thanks for the inspirational article. I have learned a lot reading your monthly updates, thank you.

It would appear, based on the list of stocks purchased in this update, that you buy right before the ex dividend date. Am I correct in that assumption, and if so, what would you buy between now, to get in on, close to the ex dividend date? I’m having a hard time finding household names that are going dividend ex in the next few weeks…thank you

Hi Patrick,

Thank you. That’s purely coincidental. We don’t purchase stocks just because of ex-dividend date.

Thanks for the update and it seems very encouraging.

I noticed that you have 3 different stocks of Brookfield – Is there a preference for a specific stock?

Do you like National Bank over TD or BNS?

Thanks

Thank you Raj.

We like BEPC for the renewable aspect. BN and BAM for the asset management aspect.

We like NA and TD over BNS at this point.

Congrats. I have been following you for years now and it is nice to see your progress in achieving FI.

How do you deal with dividends from Canadian companies that are originally in USD but receive in CAD? I am with Questrade and they charge an FX conversion fee of %1.5-2% every time. Is there a way around this? Example AQN, MG etc

Thanks

Kevin

Hi Kevin,

Thank you! For Questrade you can ask them to deposit the dividends in USD for payers like AQN & MG.

Good afternoon Bob. I checked with questrade. They said only way to get the dividend in US funds is to journal my shares to AQN from AQN.TO. Is this what you were thinking?

You should be able to tell them to deposit your dividends in the default currency and not do any exchange. That’s what we’ve been doing…