I hope all Canadian readers had a great Thanksgiving weekend. For me, there are many things to be thankful for – a safe country, universal healthcare, a fulfilling job, a fun side project (aka this blog), and a happy and healthy family.

Like every year, once Thanksgiving hit, it started raining in the Lower Mainland. This year was no exception. It started raining like cats and dogs the day right after Thanksgiving.

Upon return from our Alaska cruise in early September, we were greeted by a backyard full of veggies and fruits. Harvests kept us busy in the garden. We were thankful for the sunny weather.

With so much fresh produce, we were busy eating. For things that we couldn’t finish right away, Mrs. T made jam, apple butter, and different types of chutney.

Lots of fresh flowers were blooming in our garden so Mrs. T made some awesome bouquets as home decoration.

For me, I was on a work trip to Taiwan and Hong Kong in the last half of September. By the time I was fully adjusted to the changing time zone, it was time to come back home (that always happens on business trips). The first couple of days back in Vancouver, I slept for over 14 hours! I guess I needed to catch up on sleep.

As usual, while in Taiwan I had some amazing food. Best of all, the food was much cheaper compared to that in Vancouver.

While in Hong Kong I came across many Circle K convenience stores at basically every other street corner. It was good to see Alimentation Couche-Tard’s global dominance.

This past May when I was in Hong Kong, there were barely any tourists and I didn’t have to wait for a taxi at the airport. This time around there were visibly many more tourists. My co-workers and I had to wait for 20 minutes for a taxi at the airport. This is a good sign for the Hong Kong economy.

Side note… I could never figure out which colour of taxi to take in Hong Kong. Upon arrival, we were going to the Courtyard Marriott in Sha Tin. We waited about 20 minutes for a green taxi and were told we had to take the red one. We ended up waiting in another line for 5 minutes before getting in a red taxi. Ironically, my co-worker is very familiar with Hong Kong and even he got it wrong!

Another side note, it was still very hot and humid in Hong Kong. We arrived in Hong Kong around 9:30 PM and it was 31C outside but felt like 39C. Needless to say, I was drenched in sweat while waiting for our taxi.

Since I usually stay at the Courtyard Sha Tin while in Hong Kong, staying for two nights on this trip meant I was greeted by the familiar view of the skinny tall buildings from my hotel room.

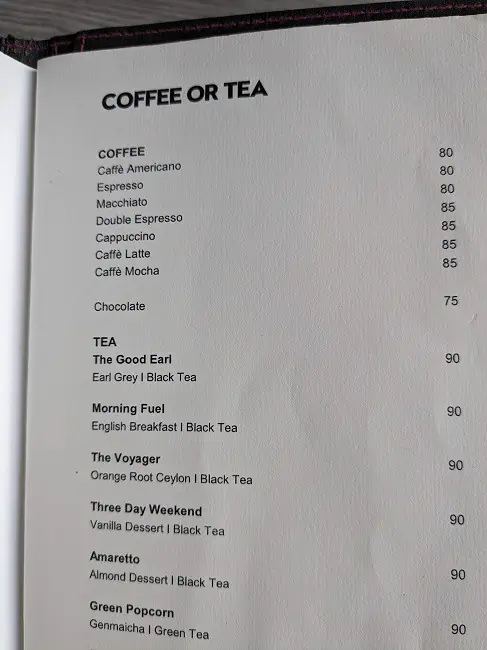

One day we had an informal customer meeting at Woobar at W Hotel in Hong Kong. I knew prices would be very inflated at a fancy hotel bar but my jaw dropped when I saw the drink menu.

Fortunately, we were just meeting the customer for coffee and tea. Imagine what the bill would be if we were there for alcoholic drinks!

The quick 10 day business trip was very productive. Unless something drastic happens, it should be my last business trip of the year. Given that I’ve been to Asia three times already this year, I’m happy to stay on the ground for a while.

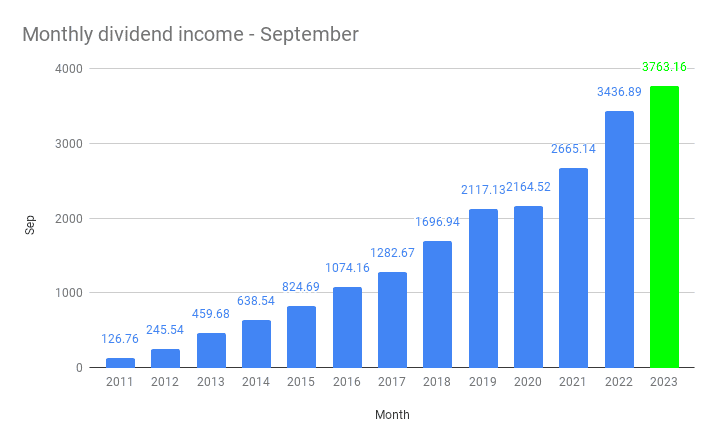

Dividend Income – September 2023

Back to dividend income. In September we received dividend income from the following companies:

- Brookfield Asset Management (BAM.TO)

- BlackRock (BLK)

- Brookfield Renewable Corp (BEPC.TO)

- Brookfield Corporation (BN.TO)

- Canadian National Railway (CNR.TO)

- Costco (COST)

- Canadian Tire (CTC.A)

- Enbridge (ENB.TO)

- Fortis (FTS.TO)

- Granite REIT (GRT.UN)

- Hydro One (H.TO)

- Intact Financial (IFC.TO)

- Johnson & Johnson (JNJ)

- McDonald’s (MCD)

- Manulife Financial (MFC.TO)

- Metro (MRU.TO)

- PepsiCo (PEP)

- Qualcomm (QCOM)

- SmartCentres REIT (SRU.UN)

- Suncor (SU.TO)

- Target (TGT)

- Visa (V)

- Waste Management (WM)

- Wal-Mart (WMT)

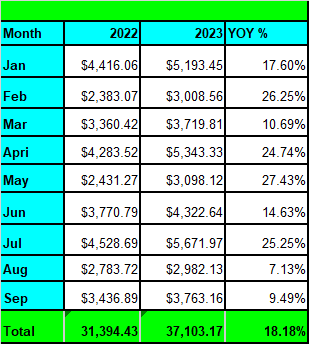

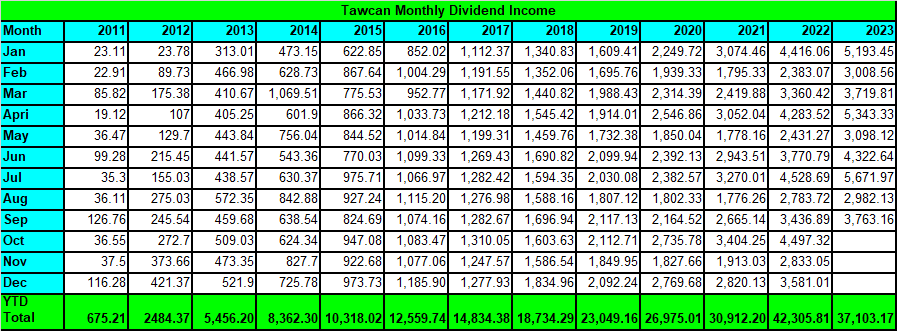

The 24 dividend payers added up to a total of $3,763.16. After a lower dividend income than usual month last month, it was nice to see our monthly dividend income climbing back to above $3,000.

Compared to September 2022, we saw a YoY growth of 9.49%. This is below our target of 15%, so it looks like we have some work to do in terms of growing our dividend income!

However, if we look at the average YoY growth rate after nine months, we’re at a respectable 18.18%. With three months to go, I suspect the YoY numbers for October, November, and December to be below 10% due to the fact that we closed out REI.UN and DIR.UN in August and re-invested the money to Alimentation Couche-Tard and Telus.

Out of the $3,763.16 received, $515.76 was in USD and $3,247.40 was in CAD or about a 15-85 split.

Please note that we do not convert USD to CAD when reporting our dividend income. This is to avoid fluctuations in our monthly dividend income due to changes in the exchange rate. I had indicated in the previous monthly dividend income update that we plan to convert everything into Canadian dollars in 2024 to get a more accurate picture. However, after thinking more about it, I’m not 100% sure that is the best plan since it would require some extra work in my spreadsheet. I’ll make the final currency conversation decision in early 2024.

Dividend Hikes

Considering we’ve been seeing zero or one dividend hike for the last few months, it was nice to see multiple dividend hikes for September.

- VICI Properties (VICI) raised its dividend payout by 6.4% to $0.415 per share.

- Starbucks (SBUX) raised its dividend payout by 7.5% to $0.57 per share.

- Foris (FTS.TO) raised its dividend payout by 4.4% to $0.59 per share.

- Emera (EMA.TO) raised its dividend payout by 4% to $0.7175 per share.

Thanks to these dividend hikes, our forward annual dividend income increased by $98.36. At a 4% dividend yield, this is equivalent to investing $2,459 new capital in our dividend portfolio.

This is exactly why organic dividend growth via dividend hikes is so important as your dividend income gets bigger.

Dividend Reinvestment Plan

Since we’re not living off dividends yet, we reinvest 100% of our dividend income. To be most effective, we enroll in dividend reinvestment plans (DRIP) with our discount brokers whenever we’re eligible. The discount brokers, TD and Questrade, support synthetic DRIPs so only full shares are dripped at each dividend payout.

This is very different than the full DRIP through a company’s transfer agent or WealthSimple Trade.

We then wait for the “leftover” dividends to accumulate to over $1,000 before reinvesting the money.

We dripped the following shares automatically in September:

- 1 share of Brookfield Asset Management

- 4 shares of Brookfield Renewable Energy Corp

- 36 shares of Enbridge

- 3 shares of Fortis

- 12 shares of Manulife Financial

- 6 shares of SmartCentres REIT

- 1 share of Suncor

We automatically added 63 shares thanks to DRIP and $192.32 toward our annual dividend income. At a 4% dividend yield, that’s equivalent to investing $4,808 of new capital.

Dividend Transactions

The stock market was very volatile in September. One of the big news items in September was that Enbridge announced that it would acquire a trio of US companies to create North America’s largest natural gas utility franchise.

According to Enbridge CEO Greg Ebel, Enbridge’s earning mix is about 60% crude oil and liquids and 40% natural gas and renewable energy. Following the deal, the earning mix would be closer to 50-50. In Enbridge’s eyes, this deal is a “once in a generation” opportunity that can’t be passed up.

This announcement, however, was not received very well by the market, causing Enbridge’s stock price to tumble for a few days after the announcement.

Seeing this as a buying opportunity, we decided to use money from dividends to purchase 40 additional shares of Enbridge.

I’m not too concerned with the short term volatility. Long term, I believe Enbridge will be fine and the company has a very wide moat for others to come in and compete against. Like TRP’s recent split plan announcement, with this acquisition, I suspect Enbridge will announce plans to split the company into two in the near future.

Late in September, with the USD dividend saved up, we also purchased 6 shares of Visa. Some readers may recall that I identified Visa as one of our top 5 long term holdings earlier this year. Ideally, we’d like to accumulate enough Visa shares to allow us to enroll in DRIP.

But we’re a long way from being able to drip Visa shares. At the current dividend payout, we’d need over 527 shares of Visa to enroll in DRIP or about $125k invested in Visa. The goal of enrollment in DRIP for Visa is definitely a long term goal.

The two purchases added $152.80 toward our forward annual dividend income.

Random thoughts on the market

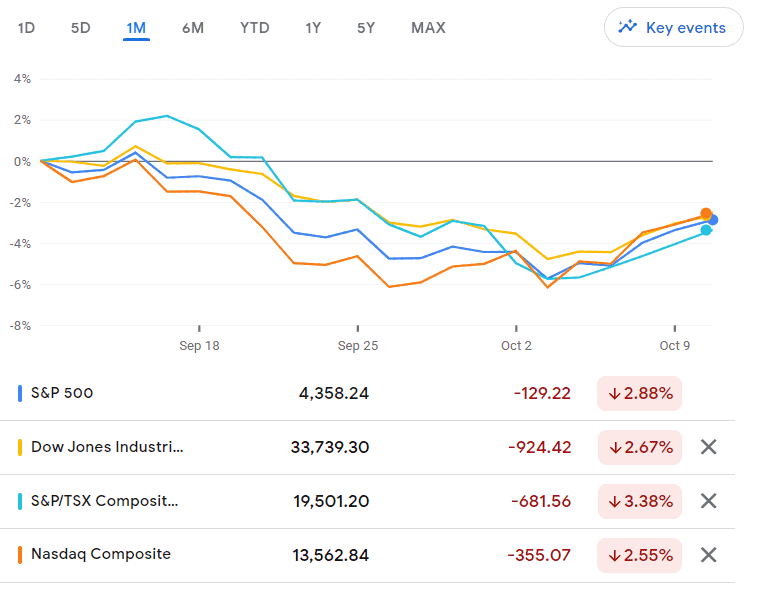

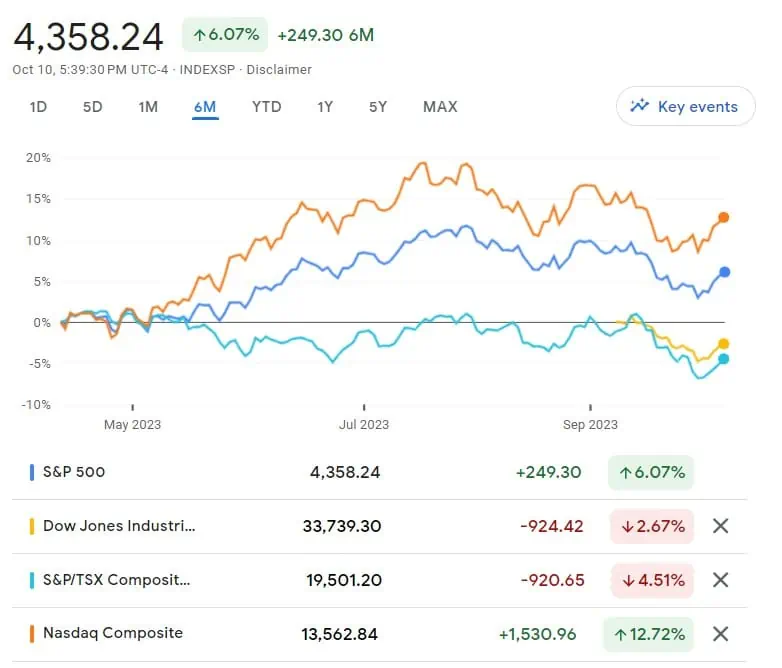

The market has been brutal the last couple of months, to say the least.

Even if we zoom out to YTD, both the Dow Jones Industrial Average and the TSX have done poorly.

With interest rates and inflation much higher than anticipated, this is putting tremendous pressure on stock returns, as investors invest in “safer” investments like bonds and GICs.

Random Thought #1 – Higher than average yields

The TSX has taken a beating lately, especially many of the big Canadian dividend payers. It’s pretty crazy that we’re seeing yields like below:

- TD – 4.81% (5 year average 3.90%)

- Royal Bank – 4.7% (5 year average 3.71%)

- Telus – 6.45% (5 year average 4.47%)

- BCE – 7.59% (5 year average 5.39%)

- Bank of Nova Scotia – 7.14% (5 year average 5.03%)

- Canadian National Railway – 2.16% (5 year average 1.66%)

- Enbridge – 8.17% (5 year average 6.33%)

- TC Energy – 8.13% (5 year average 5.18%)

For long term investors, it might be a great time to load up on these Canadian dividend stocks. This is, of course, assuming you’re OK with potential short term downsides.

The biggest question many dividend investors have is – will the dividend payments be safe? Or are we going to see dividend cuts?

Well, my crystal ball is as fuzzy as everyone else’s. My guess? I don’t see any of these companies cutting dividends. In terms of dividend hikes, my guess is that the Canadian banks probably will hold the dividend payout the same for the short term. I can see the likes of Telus, BCE, Enbridge, and TC Energy raising dividend payout by 2% or less. I would guess that CNR can continue raising dividends at around 10%, similar to its 3 years annualized dividend growth rate.

Until we see inflation and interest rates start to come down, I think more pain and downturns are to be expected. I truly believe the next little while will separate the emotional investors and the rational investors.

Remember to ask yourself these three key questions before you invest!

While dividend investing is great and all, let’s not forget it’s important to stay diversified – investing in index ETFs, therefore, is an excellent idea.

Random Thought #2 – The downward death spiral of Algonquin Power & Utilities Corp

Ugh AQN has been a terrible investment the last little while, to say the least.

Even after a 50% dividend cut, the price continues to slide. AQN terminated the Kentucky Power acquisition, changed its CEO, and announced plans to sell renewable assets and turn itself into a pure utility company.

With all these announcements, investors aren’t convinced that AQN can turn itself around.

So the share price continues to drop.

Originally we planned to continue to hold AQN, drip shares every quarter, and see if the share price could recover a little before closing out the position.

Looking back, that plan was clearly a mistake. We should have sold earlier when we had the chance. Yet another bad investment mistake!

So what do we do now? Given the tremendous headwind AQN is facing, it probably makes sense for us to start trimming some shares and re-invest that money elsewhere, especially when other Canadian dividend stocks are paying higher than average dividend yields.

Again, I should have done this earlier…but hindsight is always 20/20.

Would we close out AQN completely in the next little while? That certainly could be the plan but most likely we’ll trim our AQN holdings for tax loss reasons, continue to hold some shares, and see if AQN can recover early next year. Long term, I think closing out AQN completely is probably the right move to make.

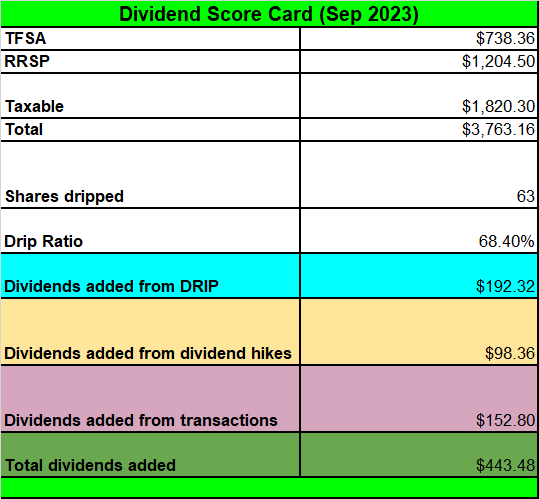

Dividend Score Card – September 2023

Here’s our dividend scorecard on how we did in September:

It was nice to see that we added $443.48 toward our annual dividend income. Having a drip ratio of 68.4% was also quite fantastic.

Going forward, we will continue to increase our dividend income by using the three pillars:

- Investment of new cash

- Organic dividend growth from dividend hikes

- Dividend reinvestment plans

Financial Independence Journey Update

It is our goal to be able to live off dividends when we are financially independent. After nine months, our dividend income was able to cover 102.5% of our necessity expenses.

Necessity expenses include things like groceries, mortgage, household items, utilities, internet, phone, health, car related expenses, insurance, and any other essential expenses.

Necessity expenses do not include things like eating out, charitable donations, massages, and vacations.

In other words, we are generating sufficient dividend income to cover all of our essential expenses. Soon, we hope to have our dividend income to cover all of our expenses.

Dividend Income – September 2023 Summary

After three quarters, we have received a total of $37,103.17 in dividend income. With three months to go, we are on track to receive over $49,000 in dividends for the whole year.

This would put us slightly ahead of our dividend income projection and I may have to adjust our projections in early January 2024. Being slightly ahead of our projections is a good thing though.

To put things in perspective, $37,103.17 after nine months is equivalent of:

- $135.91 per day or $5.66 per hour

- $951.36 per working week or $23.78 per hour after 39 working weeks

It’s nice that our dividend portfolio is working hard for us every single day so we don’t have to.

Dear readers, how was your September dividend income?

Very encouraging to see how you’ve grown the dividend income over the years. Do you have a post where you breakdown how much of this is due to investment of savings versus dividend reinvestment and dividend growth?

Thank you. There have been multiple posts k that topic so can’t just point one out, sorry.

AQN is definitely painful, and the price has gone below $7 now! I sold half of my shares in my taxable account to take a loss and hedge my bets. It’s such a small part of my portfolio I’m hoping it makes it’s way back to $10 LOL. I had some in a non-reg account too and I left those shares because there’s no tax harvesting. Hindsight definitely is 20/20 — should have sold them. My yield on cost isn’t terrible so I’m still hanging on…

More like extremely painful ha.

Great month of dividends and your harvest, I had a good year for lettuce and tomatoes, but not much else.

I’m having a hard time trying to decide what to do with my AQN.TO position. I bought into my RRSP account, so I can’t claim a capital loss and I’m down 60% in my position, so trying really hard not to freak out but once it went beyond 50% it did raise my eyebrows. So far, I’ve decided to hold, but will keep a close eye on it.

Thoughts? Any thresholds your considering before pulling the sell trigger?

Thanks. Personally I’m not sure if AQN can recover. The share price seems to slide lower and lower. I think we all wish we had trimmed or closed out the position much earlier…

It’s certainly been painful watching AQN tank. I came across an article in the Globe a while back when AQN was trading at $11 and had recently announced the spinoff for the utilities group. Will be interesting for those that hang in there if the pure play utility stock increases to a sector fair valuation after the breakup is said and done.

From the Globe…

The utilities group is valued at less than 15 times analysts’ estimates for 2024 earnings, which is lower than the valuations of larger stand-alone Canadian utilities. The price-to-earnings ratio for Fortis Inc. is 19.4, according to Robert Hope, an analyst at Bank of Nova Scotia. For Hydro One, the P/E is 21.2.

Very inspiring portfolio you have. I am still a long way from even coming close to having dividends paying for my living expenses, but one step at a time.

I received good news yesterday, my stock TFII.TO announced a 14% dividend hike, way above the inflation rate %, this is why I love holding those low yielders, high growth stocks, they have a lot of room to increase those dividends. CNR is another one I own that hopefully will announce another double digit dividend hike today.

I do have some high yielders too like TD.TO, QBR.B.TO (Quebecor, a telecom in Quebec if you are wondering who they are) and CNQ. Hopefully CNQ will announce another special dividend this year like they did last year and with oil still remaining high in demand, I expect them to hit all their targets in order to give us that special dividend.

Keep up the good work my friend 🙂

Thanks Fil. Building your portfolio takes time, be patient. 🙂 Congrats on the TFII dividend raise.

I share Doug’s comment on your garden! Thanks for sharing.

The current state of the market is contrary to markets a decade earlier. My entrance two years ago was poor timing to say the least! Over the past two years I have developed a matrix of formulas to determine the time to buy or sell a stock based on specific criteria. My losses have been buying too high. One criteria now is to delay buying until the stock is within 10% of its low for the year and with dividends at least the current rate available from GICs (currently at 5.7%). There are a surprising number of good quality stocks in Canada worth further review satisfying these criteria. I had fairly high losses (April 2023 was -14% for the portfolio) due to split stocks I sold at a considerable loss. That loss has been offset by gains having sold stocks whose value increased beyond their projected dividends for the year and other dividends–no new monies going in. I may repurchase the stocks again when stock prices bounce again. The bounce is due to speculation, not value of the stock. Timing the market? Yes, with conditions and detailed review. I enjoy reading your blog Bob! Thanks!

Thank you Dianne. We all have to learn through experience. I recall similar stock market state in around 2016 where things were down significantly. But we kept buying stocks then thinking things were on sale (we were right). The same pattern repeated itself Feb/March 2020. If you’re investing for the long term, this is a great time to accumulate.

My wife and I are long time readers of your blog appreciate your posts every week. With interest rates being higher for longer, have you thought about allocating some money to fixed income (GICs, Treasuries, etc.) until rates start coming down?

Hi Ian,

Since we’re investing for the long term, we have not allocated money to fixed income yet. You may want to take a look at the video from Ben Felix here- https://www.tawcan.com/will-canadian-banks-cut-dividends-good-reads-from-the-pf-community/

What are your thoughts on Johnson & Johnson with their large talcum powder lawsuit hanging over their head?

Thanks

Stephen

Hi Stephen,

I think they will get it sorted out. Some money will need to be paid but don’t see JNJ disappearing anytime soon just because of the lawsuit.

A truly great report, informative and encouraging. But the best dividends of all are coming from your garden. Press on!

Thank you Doug.

I have a small stake in AQN as well. Disappointing to say the least. My picks that have done poorly are the ones who did not have their financial house in strong order because they gorged themselves on low interest rate borrowing and acquisitions. Now that it is time to pay up with rising rates and debt restructuring these entities are scrambling to regain their financial footing. As painful as it is the right decision would have been to sell non-core assets and cut dividends to solidify financial footing for the future. A good example of this is RioCan. It was a sting initially when they cut their dividend by 1/3 years ago but it shored up their finances in a trying time. Comparing them with some other REITS such as True North and Northwest Healthcare you can see what the right decision was. Now these Reits are languishing because they did not act. I am wondering what your thoughts are on those two Reits? I am struggling to make a decision with them and would appreciate your insight. AQN I am going to hold onto.

I don’t follow True North and Northwest Healthcare all that much but agree with you, often than not it’s better for companies to cut dividends to get their finances in order. I’d rather companies doing that than trying to keep the dividend streak alive.