Welcome to another monthly dividend update. Through these regular dividend updates, I hope to demonstrate that it is possible to build up a sizable dividend portfolio and eventually live off dividends. For those that are new to this blog, it has been over 11 years since we got serious with the dividend growth strategy and I’m amazed at how much progress we’ve made so far.

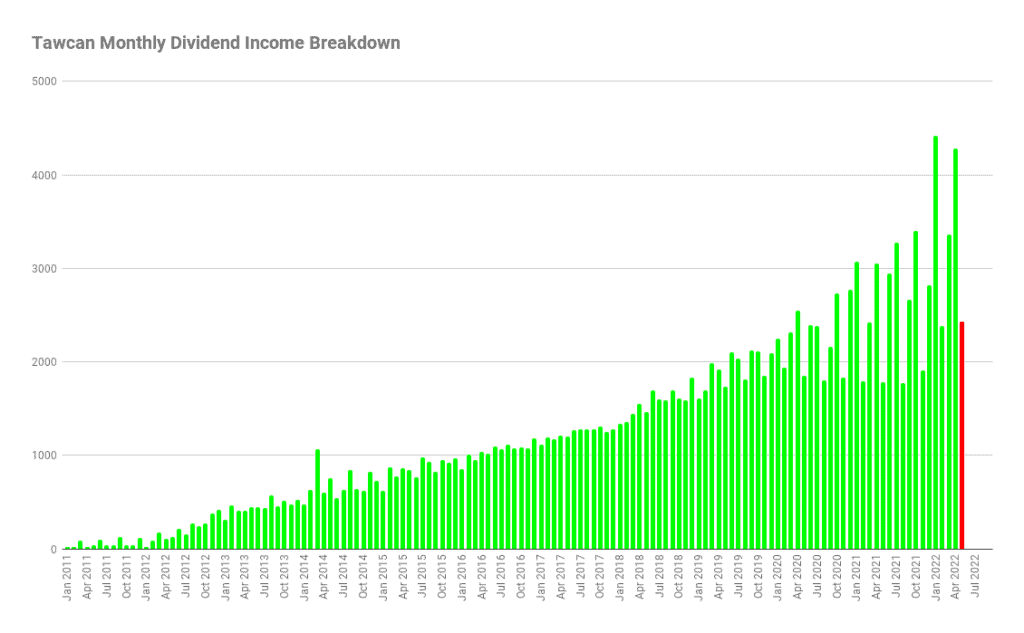

For readers that are getting a small amount of dividend income each month, please don’t get discouraged. Do continue adding new capital and building your portfolio value. As you can see from below, we were receiving less than a few hundred dollars worth of dividend income per month not that long ago.

May was unusually cold and rainy here in Metro Vancouver. This meant our backyard garden didn’t produce much. Last May we were enjoying fresh delicious strawberries and broccoli. I really hope the temperature warms up in June so we can start harvesting produce from our garden. It would also allow me to post some more garden pictures.

Mrs. T and I celebrated our wedding anniversary in May by going out for lunch at a local Mexican restaurant. The food was fabulous and we had a good time.

In case you’re wondering why I’m blocking my kids in these pictures… before the kids were born, Mrs. T and I agreed that we wouldn’t plaster their pictures all over the internet, especially on Facebook. So far, we’ve honoured this agreement.

Despite all the rain and cold weather, we took Beaver Scouts and Cub Scouts outside as much as possible. We enjoyed hiking in local parks and even went on a 3-hour canoeing trip.

When not spending time in the garden and her doula service, Mrs. T has been busy with pottery. We now have quite a few cups and mugs at home. I really like this design below that she created.

Dividend Income – May 2022

Back to dividend income, in May we received dividends from the following companies:

- Apple (AAPL)

- AbbVie (ABBV)

- Bank of Montreal (BMO.TO)

- Costco (COST)

- Dream Industrial REIT (DIN.UN)

- Emera (EMA.TO)

- European Residential REIT (ERE.UN)

- Granite REIT (GRT.UN)

- Magna International (MG.TO)

- National Bank (NA.TO)

- Omega Healthcare (OHI)

- Procter & Gamble (PG)

- RioCan REIT (REI.UN)

- Royal Bank (RY.TO)

- Starbucks (SBUX)

- SmartCentres REIT (SRU.UN)

- Verizon (VZ)

- Walmart (WMT)

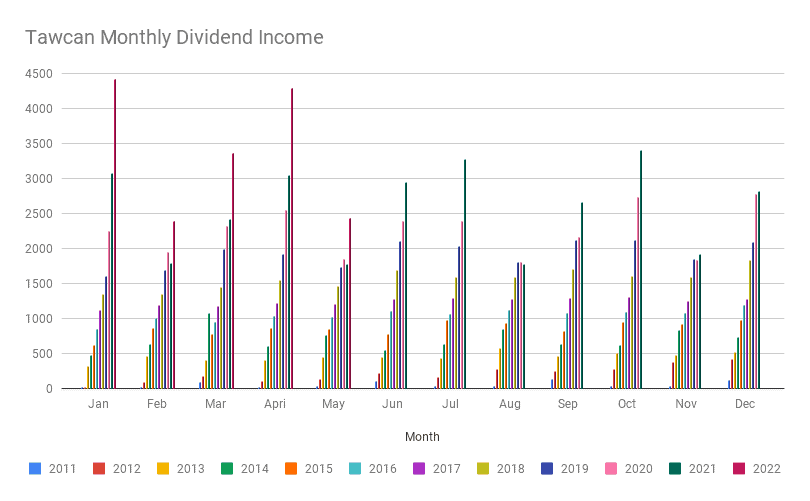

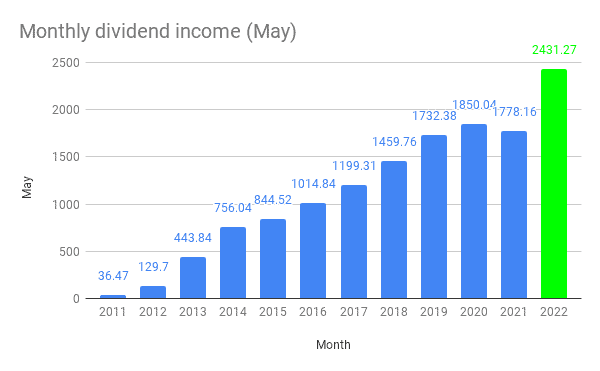

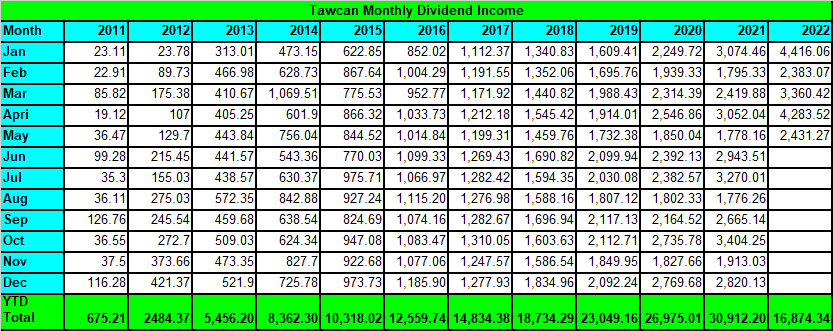

The 18 dividend paycheques added to $2,431.27. Since May is one of the weaker dividend income months, it was nice to see that the dividend income total was over $2,400.

While May’s dividend income was not as impressive as the $4,283.52 from last month, if you look at the chart above, you’ll see our weaker months have increased significantly compared to the previous years. This is a small success we can celebrate.

Compared to last year’s dividend income, we saw an incredible YoY growth of 36.73%! So far this year our dividend income has increased by an average of 39.23% compared to last year in the same time period. This is absolutely fantastic!

| Month | 2021 | 2022 | YOY % |

| Jan | $3,074.46 | $4,416.06 | 43.64% |

| Feb | $1,795.33 | $2,383.07 | 32.74% |

| Mar | $2,419.88 | $3,360.42 | 38.87% |

| Apri | $3,052.04 | $4,283.52 | 40.35% |

| May | $1,778.16 | $2,431.27 | 36.73% |

We’ve added a lot of new capital into our dividend portfolio over the last two years. This has been the main reason why our dividend income has grown so much. Can we continue to add such large amounts for the rest of this year and next year? Given that our dividend income is already quite sizable and that we’re encountering the law of the big numbers, I wouldn’t be surprised if our dividend income growth rate slows down to around 10% next year.

Out of the $2,431.27 received, $454.43 was in USD and $1,976.84 was in CAD, or about a 20-80 breakdown. Long time readers will recall that we do not convert USD to CAD when reporting our dividend income. We are doing this to keep the math easy and to avoid fluctuations in our monthly dividend income caused by changes in the exchange rate.

The top five dividend payers for May were Smart Centres REIT, Royal Bank, National Bank, Emera, and Bank of Montreal (not in order). These payments accounted for $1,859.45 or 76.5% of our May dividend income.

May 2022 Dividend Transactions

Throughout May, there had been a lot of noise in the market. As one would expect, the market was very volatile. At one point, our portfolio value was down over $100,000. Since we’re still in the accumulating phase, I was not worried. In fact, I was secretly praying that the bearish market will continue for a prolonged period of time. I’d love to scoop up more shares of Apple, Costco, Algonquin Power & Utilities, Starbucks, and Canadian banks at a discount.

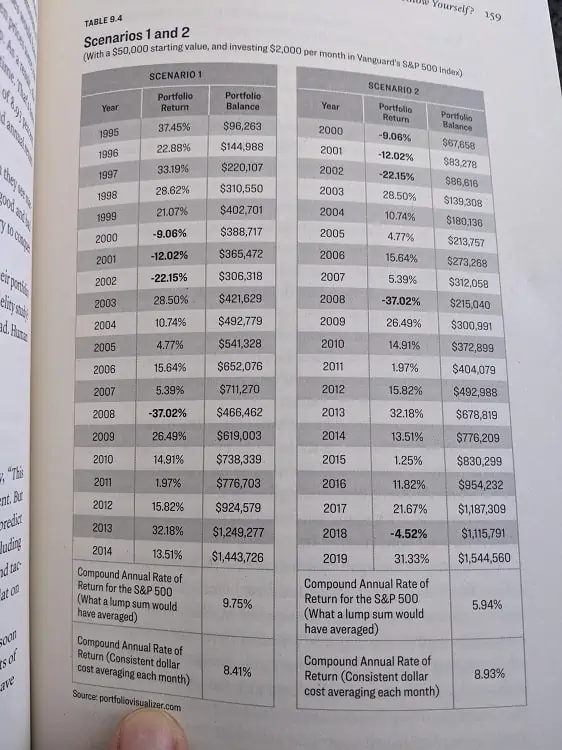

Unfortunately, too many investors only focus on the short term and worry about their paper gains or losses. After more than a decade of DIY investing, I’ve learned that it is vital to have a long-term view. Just how important is a bear market to investors who are in the accumulating phase? I came across this great example from Balance by Andrew Hallam:

In this example, the investor starts with a $50,000 portfolio and invests $2,000 per month in Vanguard’s S&P 500 index over a 20-year period. Scenario 1 has a higher compounded annual rate of return (9.75%) than Scenario 2 (5.94%). Surprisingly, the investor actually comes out ahead in Scenario 2.

This happens because in Scenario 2, the investor is able to take advantage of three years of bear market and is able to purchase the index fund at a discounted price (i.e. purchased more shares of the fund).

With the idea of taking advantage of the market downturn validated yet again, we purchased the following dividend paying stocks in May:

- 25 shares of Bank of Nova Scotia

- 61 shares of BCE

- 2 shares of Costco

- 56 shares of CIBC

- 11 shares of Apple

Ignoring the currency exchange rate, the total amount added to just over $12,600. First of all, I realized this is a large amount of money to invest in a month and not every household can do that. Therefore, we feel very fortunate to be able to invest large sums of money regularly.

Perhaps a bit of explanation is needed… some of the money was from regular monthly savings and dividends collected. Seeing buying opportunities, we also moved a large amount of money from our Long Term Savings for Spending (LTSS) account. In addition, a small percentage of the $12,600 was from exercising my company’s restricted stock unit (RSU) shares as part of my bonus from last year.

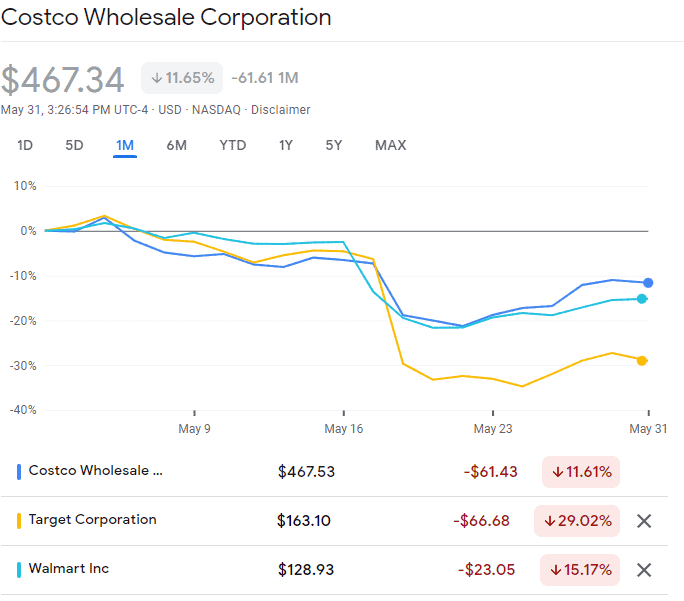

As some of you may recall, Costco’s share price got dragged down due to poor quarterly results from Walmart and Target. Overall, the retail sector took a big hit around mid-May because investors were worried about the sector.

We’re very bullish on Costco long term, so we decided to take advantage of the discounted share price. Unfortunately, we only had $900 USD sitting in my RRSP account from dividends received. So that meant we were only able to purchase two Costco shares. Ideally, we’d love to buy more.

Since our RRSPs are pretty much maxed out (taking my work’s RRSP contributions for the remaining of the year into consideration), we decided to take advantage of the $2,000 RRSP contribution buffer. We added more money to Mrs. T’s spousal RRSP so we had cash to purchase some more Apple shares.

Hopefully, the market will remain volatile for a little while longer. Some of the stocks we’re monitoring and planning to buy more are:

- Apple

- Starbucks

- Costco

- Canadian Net Real Estate Invest Trust

- Bank of Montreal

- CIBC

- Algonquin Power & Utilities

- Waste Connections

- Brookfield Asset Management

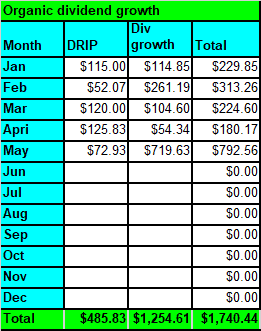

Dividend Reinvestment Plan (DRIP)

One of the ways that we grow our dividend income organically is through dividend reinvestment plans. Whenever we invest in a company, we try to purchase enough shares to enroll in DRIP. DRIP not only allows us to dollar cost average, it also allows us to increase dividend income over time.

In May we dripped the following shares:

- 2 shares of BMO.TO

- 1 share of EMA.TO

- 1 share of ERE.UN

- 5 shares of NA.TO

- 5 shares of OHI

- 2 shares of REI.UN

- 4 shares of RY.TO

- 4 shares of SRU.UN

By enrolling in DRIP, we added 23 shares in May without incurring any trading commission. Furthermore, we added $72.93 toward our annual dividend income. At a 4% dividend yield, that’s equivalent to adding $1,823.13 of new cash.

Dividend Increases

May was a fantastic month when it comes to dividend increases. We saw a total of ten dividend hikes!

- Hydro One (H.TO) increased its dividend payout by 5% to $0.2796 per share.

- Telus (T.TO) increased its dividend payout by 3.4% to $0.3386 per share.

- Suncor (SU.TO) increased its dividend payout by 11.9% to $0.47 per share.

- Canadian Tire (CTC.A) increased its dividend payout by 25% to $1.625 per share.

- Algonquin Power & Utilities Corp (AQN.TO) increased its dividend payout by 6% to $0.1808 per share.

- Bank of Nova Scotia (BNS.TO) increased its dividend payout by 3% to $1.03 per share.

- Bank of Montreal (BMO.TO) increased its dividend payout by 4.5% to $1.39 per share.

- CIBC (CM.TO) increased its dividend payout by 3.1% to $0.83 per share.

- Royal Bank (RY.TO) increased its dividend payout by 6.7% to $1.28 per share.

- National Bank (NA.TO) increased its dividend payout by 5.7% to $0.92 per share.

These ten dividend hikes increased our forward annual dividend income by a whopping $719.63! At a 4% yield, that’s equivalent to adding $17,990.76! Wow!

The only bummer is that all of these dividend hikes came from Canadian companies. Hopefully, we’ll see some US dividend raises in the next few months.

Summary

Whenever I look at the table below, I am always amazed at how much progress we’ve made with our dividend income. We continue to feel blessed and appreciative of how well we’re doing financially. Therefore, whenever possible, we try to provide helping hands to those in need either by donating money to charities or volunteering our time. If you’re in the same position as us, please consider helping those in need.

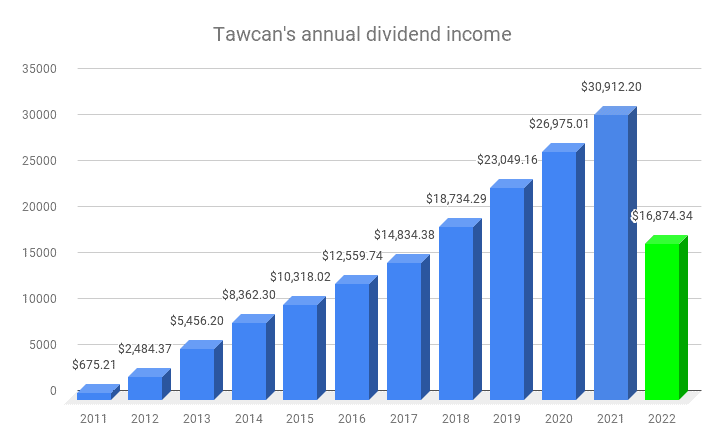

So far in 2022, our dividend portfolio has generated $16,874.34 without us having to do any work. After only five months, we have already exceeded our annual dividend income from 2018.

Looking ahead, if we are able to increase our June dividend income at a 30% YoY growth rate, we’d reach over $20,000 in dividend income after six months. That’d put us over the entire year’s worth of dividends from 2019!

Now, to put things in perspective:

- $16,874.34 dividend income in five months is like earning $4.66 per hour. That’s earning money regardless of what we’re doing.

- After 23 work weeks, our dividend income translates to $18.31 per hour, assuming a 40-hour workweek. It’s amazing to know that our dividend portfolio is earning above BC’s minimum wage rate of $15.65 per hour.

Most importantly, our dividend income has grown organically by $1,740.44 after five months or an average of $348 per month. If we can continue at this pace, it’d mean our dividend income would grow organically by ~$3,600 in 2022.

At a 4% dividend yield, growing dividend income by $1,740.44 organically is like investing over $43,000 new capital into our dividend portfolio. Instead, when we do add that much new capital, we are generating another $1,740.44. This is a perfect example of how powerful compounding is.

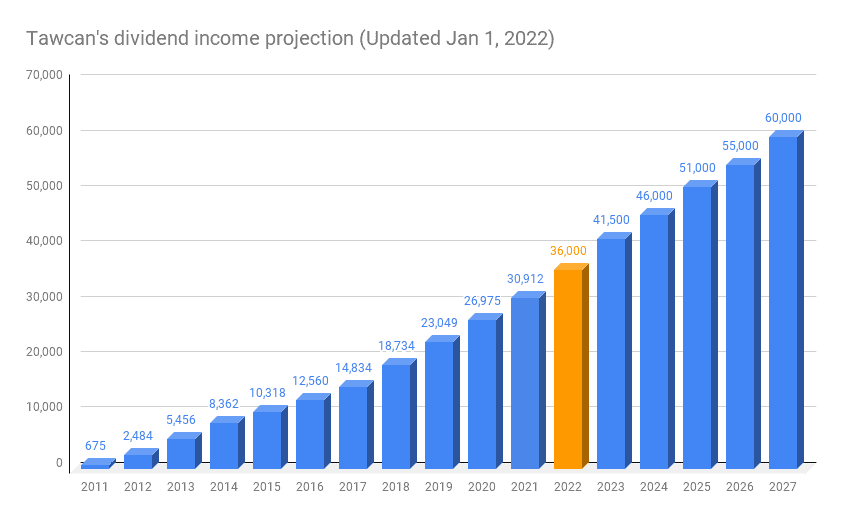

At this rate, we should be able to easily hit our $36,000 dividend income goal for 2022.

Dear readers, how was your May dividend income?

Fantastic dividend growth, Bob. Congratulations and thank you for sharing. I do have one question, do you have any strategies or concerns if your grossed up dividends in your non-registered accounts could cause you to get your OAS clawed back when you reach 65 to 70?

Thanks

Hi Henry,

Thank you. My view is that if we end up facing OAS clawback, that’s a good problem to have.

How refreshing to see someone take a deep dive on dividend investing instead of rental properties, much less time and hassle. I’m going to read more on your rationale for why not dividend ETFs.

Do you dollar cost average across all your holdings in a sequential manner or just pick a few shares you want to buy of a company each month and focus on that? Sorry if I missed that somewhere.

Been building our portfolio for over 11 years so you can consider it as dollar cost average across all these years.

Aren’t you still invested in Manulife MFC ?

I noticed that there was a dividend for May, but it wasn’t mentioned ?

MFC pays dividends in June.

This is amazing Bob! So wonderful to see how your dividend income has grown over the past 10-12 years with persistence and financial discipline. Way to go! I find it so inspiring.

Thank you Moe.

You are certainly proving that investing for income works, and that one should ignore the market, accept to take advantage of buying opportunities. Buy the best, reinvest, hold and add, then give your investments time to grow.

Good work Bob.

Thank you HenryM.

Hi Bob,

Just wondering, in regards to your DRIP dividends, how do you pay the taxes owed? Do you sell stock at tax time? Thanks

Hi David,

Just pay with cash saved up, not selling stocks at tax time.

Wow! Congrats on a great month of May! Wish our slow month provided over $2,400. We did pull in over $700 across our taxable and retirement accounts though and are continuing to improve each month which is all we can ask for.

Thank you JC. Congrats on recieving $700 in passive income.

Amazing progress Bob! Like you said it takes time and patience to build a sizable portfolio.

Bob I know you hold few REITs and so do I so I just wanted to know what you think about REIT is there any concern specially with the interest rate hikes and more to come apparently?

Thanks

At this point, I’m not concerned about raising interest rates and REITs.

Another stellar month, congrats.

I find it very hard to gauge the benchmark for future YoY growth when it comes to dividend income. I’ve used 10%, like your mention, but it always ends up being way off when compared to actual. The YoY actual often falls between 20-40%. I want to be conservative but not overly so.

I know that moving forward, new capital invested may not be as robust as previous years, but as my dividend income increases so do the reinvestments. Maybe I should be looking beyond the 10% benchmark to 15% YoY income growth instead?

If I’m thinking 10% might be too low in my projections, it is surely too low for your projections.

M: Hope you don’t mind if I add a comment. As long as you are adding new money, especially higher amounts, you should see closer to 20% or more income growth. It’s when you stop adding money that the income growth drops to 10% (as long as one is reinvesting) and it’s the increases that bump it up.

That’s good to hear about 20% rather than 10% estimate. But when you have say $50,000 in dividend income, growing 20% means $10,000. At 4% yield, that’s like adding $250k. Of course, that’s ignoring organic dividend growth.

Bob: believe me it continues to grow at that pace. Because even though we are gifting larger amounts, the recover rate is still about 10%.

Good to know, makes sense. I guess I should use a higher YoY for modeling then.

Thank you Our Life Financial. Yes it’s always tough to gauge the future YoY growth. I just arbitrary set it to around 10% thinking it might be harder to grow moving forward.

Very interesting following you and happy for your journey outcome so far.

Do you calculate the average dividend payout ratio of your overall portofolio? Relative to earnings or free cash flow.

Thanks for following along JF.

That’s an interesting question, I do keep an eye on payout ratio of each stock we own but interestingly I haven’t calculated the average payout ratio for the entire portfolio. Something to consider, thanks for giving me this tip.

Yes, hard work pays off.

You’re braver than me, but I like a good deal and I’m accumulating cash and staying on the sidelines for the next several months . Interest rate hikes , stagflation , end of QE and recession coming.

But have my shopping list ready to go for the 10-15% lower deals coming up: TD, RY, BCE

And taxable account: BRK-B, DIS, QQQ, SHW, GOOG.

We plan to continue investing new cash every month and just dollar cost average. Market will continue to be volatile and it’s nearly impossible to time the market. You never know when the market is at the bottom.

Great job Bob!

I like the upward projection. Makes me look forward to where I’ll be at in 5 years.

cheers,

John

Thank you John. Takes time to build a sizable dividend portfolio. 🙂

Wow, over $700 in dividend increases is incredible! Congrats on an awesome month! Like you said, a volatile market is an opportunity to buy. Keep loading up on some nice stocks at a discount! 🙂

Very fortunate to get a $700 raise that is for sure. Happy investing and buying.