Canadian banks have a long dividend history. All the big five banks – Royal Bank, TD, Bank of Montreal, Bank of Nova Scotia, and CIBC have been distributing dividends since the late 1800s. Even during the financial crisis, none of the big five banks cut their dividends. Therefore, it is not a surprise that we hold all the big five Canadian banks, including National Bank, in our dividend portfolio. It is also not a surprise why I listed a number of Canadian banks in my best Canadian dividend stocks.

Recently, a reader (let’s call him Tom), reached out to me and asked me about my thoughts on Canadian bank ETFs. Is it better to invest in a Canadian bank ETF or to simply build your own ETF by buying the bank stocks?

Tom’s question:

Hi Bob,

I like the Canadian banks a lot because of their solid dividend distribution history. I noticed that you own Royal Bank, TD, BNS, BMO, CIBC, and NA. How come you decided to hold the big six on your own by buying individual shares rather than buying a Canadian ETF? What’s your thought on investing in the BMO Equal Weight Bank Index ETF (ZEB.TO)?

6 Best Canadian Bank ETFs

Before I answer Tom’s question, let’s dive in and take a look at the 6 best Canadian bank ETFs that are available for investors.

1. BMO Covered Call Canadian Bank ETF – ZWB

The BMO Covered Call Canadian Banks ETF (ZWB) has been designed to provide exposure to a portfolio of Canadian banks while earning call option premiums. The fund invests in Canadian banks and dynamically writes covered call options. The option premium from the covered call options provides limited downside protection. ZWB is rebalanced and reconstituted semi-annually.

- Ticker: ZWB

- Inception Date: Jan 28, 2011

- MER: 0.71%

- Dividend Yield: 5.6%

- Distribution Frequency: Monthly

- Net Asset: $ 1,886M

- Number of holdings: 30

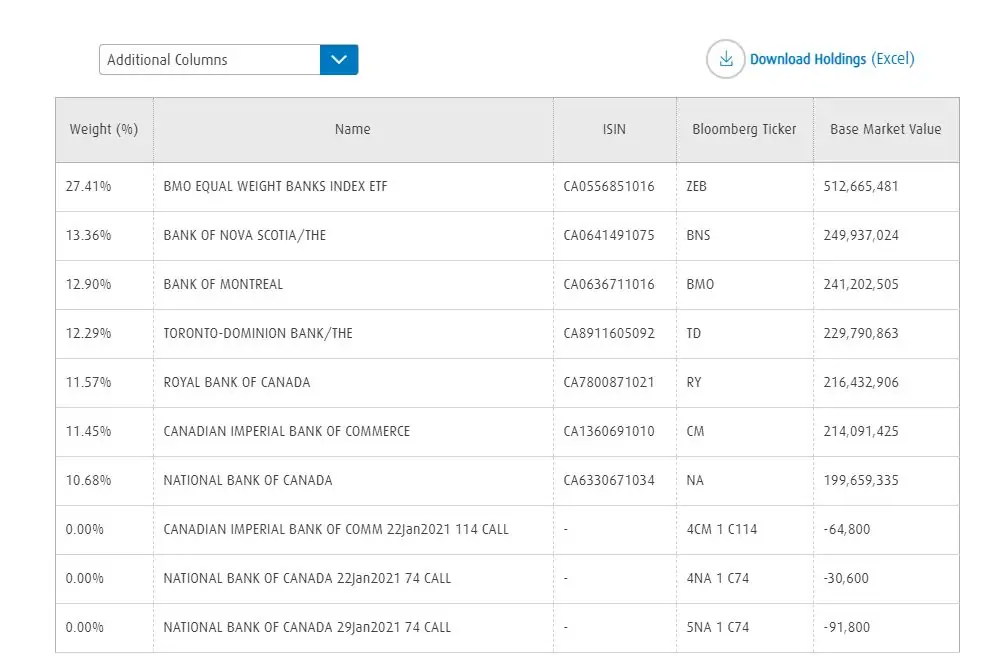

- Holding Breakdown:

| Name | Weight (%) |

| BMO Equal Weight Bank Index ETF (ZEB) | 27.41% |

| Bank of Nova Scotia | 13.36% |

| Bank of Montreal | 12.90% |

| TD Bank | 12.29% |

| Royal Bank | 11.57% |

| CIBC | 11.45% |

| National Bank | 10.68% |

| Various Covered Calls | 0% |

| Cash | 0.59% |

ZWB is an interesting ETF as it holds the BMO Equal Weight Bank Index ETF (ZEB), the big six individual stocks, and various covered calls. The utilization of covered calls means a slightly higher dividend yield compared to other ETFs covered in this article. In theory, the covered calls should reduce volatility.

For readers that aren’t familiar with covered calls, a call is a type of options contract. The word “covered” means that the investor already owns the underlying stock whereas “naked” calls mean the investor doesn’t hold the underlying stock.

When you sell a call option, it means you’re writing a contract to sell the shares at a specific dollar value on or before the contract expiration date. The investor that buys the call option, therefore, has the option to buy the shares at the determined price on or before the contract expiration date.

When you sell a call option, you get paid a premium. On the day the contract expires, if the stock price is below the call price, the contract expires without being exercised, and you get to keep your shares and premium. Now if the stock price is above the strike price, the call option buyer can exercise the option. When this happens, you then have to sell your shares at the agreed price.

With a covered call, since you already own the shares, if the buyer decides to exercise the option, you simWith a covered call, if the buyer exercises the option, you are obligated to sell the shares. Since you already own the shares you don’t have to worry about the need to buy the actual shares then sell them to the call buyer.

Basically ZWB sells covered calls to get premiums and if the calls are exercised, the shares are sold. ZWB can buy back the shares at a lower price in the open market when the fund rebalances itself. If the call options don’t get exercised, premiums are the extra gravy that get distributed to the investors.

Covered calls are a way to protect your holdings. However, because ZWB utilizes covered calls as an investing strategy, it is not entirely passive. This means higher MER compared to the other Canadian Bank ETFs in this article.

Since inception, ZWB has returned 7.89%, including dividends. In 5 years, the ETF has a 8.38% return. Interestingly, ZEB, the BMO Equal Weight Bank Index, has actually performed better than ZWB during this time, with a 5-year annualized return of 10.39% at 0.10% lower fees.

2. BMO Equal Weight Banks Index ETF – ZEB

The BMO Equal Weight Banks Index ETF (ZEB) has been designed to replicate, to the extent possible, the performance of the Solactive Equal Weight Canadian Banks Index, net of expenses. The fund invests in and holds the big six (big five plus National Bank) and the holdings are equally weighted to lessen security specific risk.

- Ticker: ZEB

- Inception Date: Oct 20, 2009

- MER: 0.28%

- Dividend Yield: 3.98%

- Distribution Frequency: Monthly

- Net Asset: $ 1,484M

- Number of holdings: 7

- Holding Breakdown:

| Name | Weight (%) |

| Bank of Nova Scotia | 18.35% |

| Bank of Montreal | 17.71% |

| TD Bank | 16.87% |

| Royal Bank | 15.89% |

| CIBC | 15.72% |

| National Bank | 14.66% |

| Cash | 0.80% |

ZEB holds all big six Canadian banks. Unlike the name suggests, the six banks aren’t weighted equally. Rather, they are weighted roughly equally and the weighing is adjusted regularly.

If you are looking to hold an ETF that holds all of the big six and you want all six to be roughly equally weighted, ZEB is a great Canadian bank ETF to hold.

ZEB has an annualized return of 9.88% since inception and a five year annualized return of 10.39%. Due to the COVID-19 pandemic, the Canadian banks have not performed well, so ZEB has only managed to return 3.72% in the past year.

ZEB’s 3.98% dividend yield is pretty decent, however, considering BNS yields 5.14%, BMO yields 4.32%, TD yields 4.24%, RY yields 4.01%, CIBC yields 5.23%, and NA yields 3.85%, you are definitely getting a lot lower yield with ZEB than if you were to buy these stocks individually and weighted them equally (you’d get an average yield of 4.465%).

In addition, given that ZEB only holds six stocks, the MER of 0.61% seems extremely high compared to all-in-one ETFs like XBAL and XGRO, or all-equity ETFs like XEQT, which all hold way more stocks than ZEB.

3. CI First Asset CanBanc Income ETF – CIC

The CI First Asset CanaBanc Income ET (CIC) owns a portfolio of common shares of Bank of Montreal, CIBC, National Bank, Royal Bank, Bank of Nova Scotia, and TD. As part of the fund’s investment strategy, each month, the fund sells call options on approximately, and not more than, 25% of the common shares of each bank held in the portfolio.

- Ticker: CIC

- Inception Date: Aug 18, 2010

- MER: 0.65%

- Dividend Yield: 4.58%

- Distribution Frequency: Quarterly

- Net Asset: $ 159.2M

- Number of holdings: 12

- Holding Breakdown:

| Name | Weight (%) |

| National Bank | 16.71% |

| Bank of Nova Scotia | 16.68% |

| Royal Bank | 16.60% |

| TD | 16.59% |

| Bank of Montreal | 16.56% |

| CIBC | 16.19% |

| Cover Call Options | 0% |

Like ZWB, CIC also utilizes covered calls to increase dividend yield. CIC aims to provide investors with quarterly distributions, capital appreciation, and lower overall volatility. One thing CIC is different from ZWB is that CIC doesn’t hold any underlying ETFs. It just holds shares of the big six.

Because of the utilization of covered calls, CIC’s MER is a bit higher than usual, but cheaper than ZWB’s MER.

Since its inception, CIC has an annualized return of 8.25% and a 5-year annualized return of 8.42%.

The iShares S&P/TSX Capped Financials Index ETF (XFN) seeks long-term capital growth by replicating the performance of the S&P/TSX Capped Financial Index, net of expenses. The fund holds a mix of Canadian banks and Canadian financial companies. XFN is very similar to CEW. In fact, CEW holds a small percentage of XFN as one of its underlying holdings.

- Ticker: XFN

- Inception Date: Mar 23, 2001

- MER: 0.61%

- Dividend Yield: 3.60%

- Distribution Frequency: Monthly

- Net Asset: $ 1,090.2M

- Number of Holdings: 26

- Top 10 Holding Breakdown:

| Name | Weight (%) |

| Royal Bank | 19.88% |

| TD | 17.54% |

| Bank of Nova Scotia | 11.13% |

| Brookfield Asset Management | 9.05% |

| Bank of Montreal | 8.34% |

| CIBC | 6.52% |

| Manulife Financial | 6.11% |

| Sun Life Financial | 4.65% |

| National Bank | 3.24% |

| Intact Financial | 2.73% |

Over 67% of the XFN holdings are in Canadian Banks. While the fund holds a large percentage of the big six, it does have a small exposure to smaller banks like Canadian Western Bank and Laurentian Bank of Canada.

Since its inception, XFN has had an annualized performance of 8.97% and 5-year annualized return of 8.84%. This is roughly on par with the other ETFs.

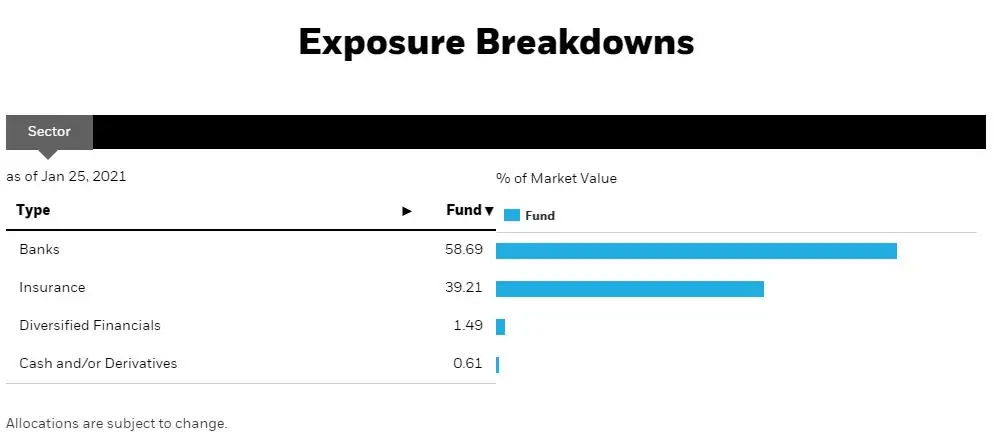

The iShares Equal Weight Banc & Lifeco ETF (CEW) seeks to provide a diversified, equal-weighted portfolio of common shares of the largest Canadian banks and life insurance companies. Given that CEW includes both Canadian banks and life insurance companies, it is not a pure Canadian bank ETF, with around 58% of the fund allocated to the big six. The weighting of the big six is roughly equal.

CEW also holds a small percentage of the iShares S&P/TSX Capped Financials Index ETF which means CEW holds a small percentage of the smaller Canadian banks like Canadian Western Bank and Laurentian Bank of Canada.

Unlike the other ETFs in the list, CEW tracks the Canadian financial services industry. The ETF provides monthly distributions.

- Ticker: CEW

- Inception Date: Feb 6, 2008

- MER: 0.60%

- Dividend Yield: 3.75%

- Distribution Frequency: Monthly

- Net Asset: $ 164.6M

- Number of Holdings: 11

- Holding Breakdown:

| Name | Weight (%) |

| Bank of Montreal | 9.87% |

| Manulife Financial | 9.81% |

| IA Financial | 9.81% |

| National Bank | 9.81% |

| Great West Lifeco Inc | 9.81% |

| Sun Life Financial | 9.79% |

| Bank of Nova Scotia | 9.78% |

| CIBC | 9.76% |

| Royal Bank | 9.75% |

| TD | 9.72% |

| iShares S&P/TSX Capped Financials | 1.49% |

| Cash | 0.61% |

It’s interesting that CEW not only holds the Canadian banks but other Canadian life insurance companies too.

Since its inception, CEW has had an annualized return of 7.49% and a 5-year annualized return of 9.07%. However, the ETF has performed poorly in the last year with a -0.56% return.

6. RBC Canadian Bank Yield Index ETF – RBNK

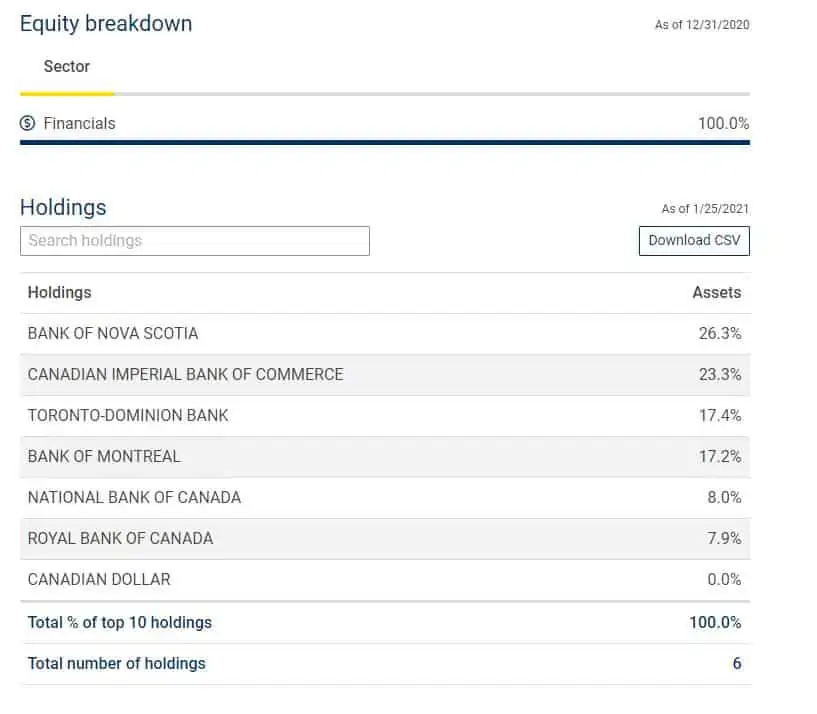

RBC Canadian Bank Yield Index ETF (RBNK) seeks to replicate, to the extent possible and before fees and expenses, the performance of a portfolio of Canadian bank stocks. The ETF seeks to track the Solactive Canada Bank Yield Index. The ETF provides a simple and efficient way to invest in the Canadian banks while providing a tax-efficient income via dividends. One key thing to note is that RBNK weights the big six differently. The composition is heavily weighted on two banks.

- Ticker: RBNK

- Inception Date: Oct 2017

- MER: 0.32%

- Dividend Yield:4.58%

- Distribution Frequency: Monthly

- Net Asset: $ 107.44M

- Number of Holdings: 6

- Holding Breakdown:

| Name | Weight (%) |

| Bank of Nova Scotia | 26.3% |

| CIBC | 23.3% |

| TD | 17.4% |

| Bank of Montreal | 17.2% |

| Royal Bank | 8.0% |

| National Bank | 7.9% |

| Cash | 0% |

The best thing about RBNK is the low fees. At 0.32% MER, the management fee is roughly half of the other five Canadian Bank ETFs that I’ve covered above.

It is interesting that RBNK is heavily weighted on BNS and CIBC while Royal Bank, the largest Canadian bank, makes up only 7.9% of the fund.

The fund is relatively new and has a 4.2% annualized return since inception and 3.1% in the last three years. In comparison, ZEB which weighs roughly equally across the six holdings, returns 3.13% in the last three years.

Best 6 Canadian Bank ETFs – Comparison Summary

Below is a summary table of the key attributes for the six top Canadian bank ETFs that I have covered.

| MER% | Yield % | # of holdings | Distribution Frequency | 5 Year Performance | 3 Year Performance | |

|---|---|---|---|---|---|---|

| ZEB | 0.28 | 3.98 | 7 | Monthly | 10.39% | 3.13% |

| ZWB | 0.71 | 5.6 | 30 | Monthly | 8.38% | 2.26% |

| CIC | 0.65 | 4.58 | 12 | Quarterly | 8.42% | 1.81% |

| CEW | 0.60 | 3.75 | 11 | Monthly | 9.07% | 2.94% |

| XFN | 0.61 | 3.60 | 26 | Monthly | 8.84% | 3.21% |

| RBNK | 0.32 | 3.60 | 6 | Monthly | N/A | 3.1% |

It is interesting to note that RBNK has the lowest MER and has performed relatively well in the last three years compared to the rest of the other Canadian bank ETFs. Meanwhile, ZWB and CIC, which utilize covered calls haven’t exactly provided higher returns, although the two ETFs do have slightly higher yields than the other four ETFs.

One thing to note is that all six of these ETFs have much higher management fees than the all-in-one ETFs like XBAL and XGRO, and all-equity ETFs like XEQT. Given the small number of holdings, I am very surprised that these Canadian bank ETFs have such high management fees.

What exactly are you paying for when the ETF only holds Canadian banks?

Should I invest in a Canadian Bank ETF? Or Should I build my own?

Back to Tom’s original question. Why do we invest in individual stocks rather than buying one of these Canadian ETFs?

Well, we purchase Canadian bank stocks rather than relying on a bank ETF because we wanted to be able to adjust the weighting accordingly. By holding Canadian banks stocks ourselves, we can adjust the weighting on the fly and increase our exposure to one or two of the Canadian bank stocks as we see fit. I like to have this control rather than relying on professional managers.

Another reason is that we know exactly how much dividends we will receive each month from the banks. Whereas ETF distributions can vary, making it slightly difficult to determine the exact amount. This might not be an issue when you’re in the accumulation phase, but when you are living off dividends, a predictable income can be important and may bring you peace of mind.

By holding the Canadian bank stocks ourselves, we are able to get a slightly higher yield than if we were to hold one of the ETFs. For example, if we were to hold the big six equally, it would result in an average dividend yield of 4.465%. Meanwhile, ZEB, which is roughly equal weighted across the holdings, only yields at 3.98%.

In other words, if we were to invest $10,000 in ZEB, we’d be paying $61 in fees each year and we’d receive $48.5 less in dividends – a total of $109.50 missed out on.

Given that we typically buy individual dividend paying stocks with a lump sum to minimize trading commissions, I don’t think that he ETF management fees and the difference in dividend income are worth it.

So what do I think about holding ZEB? My personal opinion is that I would not hold ZEB or any of the Canadian bank ETFs that I listed above. I would rather hold the individual Canadian banks and manage them myself.

For ETFs, I don’t like the idea of focusing on a single sector. This is simply far too risky. If you were to hold an ETF, I think it is far better to hold a diversified broad market index ETF like XEQT, VGRO, XAW, or VXC. Not to mention these index ETFs have way lower management fees.

Now, if you want to keep things simple, do not want to manage your portfolio yourself, and want to focus on only the Canadian banks, then these Canadian bank ETFs are a good fit. If I were in this boat and have to pick one ETF, I would probably go with either ZEB or RBNK.

If you don’t want to manage your own portfolio and don’t want to utilize an ETF and pay the management fee, is there a way to do that? Fortunately, some smart folks created Passiv to do that for you automatically. With Passiv, the tool can put your portfolio on autopilot. You can build your own personalized index, invest, and rebalance all through a click of a button. Passiv can even calculate and execute the trades needed to keep your portfolio balanced. Essentially, Passive makes investing super simple! A community user account is free to sign up. The elite member account is $99 per year…but it’s free for Questrade clients! Make sure to check out Passiv.

Summary – Are Canadian Bank ETFs worth it?

Are the Canadian Bank ETFs worth holding? Well, I think it totally depends on your investing strategy. For us, I think it is far better to hold the Canadian bank stocks ourselves to allow us to adjust the weighting accordingly. It also allows for predictable dividend income.

But for investors that do not want to manage the portfolio, and want to focus on the Canadian banks only, the Canadian Bank ETFs can be a good fit. If I were one of these investors, I would want to keep things as simple as possible and pay as low fees as possible by going with either ZEB or RBNK.

However, I do believe it is far better to invest in a diversified broad market index ETF like XEQT and XAW. If you wanted some bonds, then VGRO or VBAL is a good choice, depending on your risk level.

My question if your retired and just need income and capital appreciation is not a concern would a covered call eft work better than owning individual stocks ? I own 30 stocks ( canadian dividend) but wondering if I should increase my covered call investment .

If capital appreciation isn’t a concern covered call might be a good option.

I re-did the math with share prices and dividend yield as of April 4 2023. Assuming an investment of $12K for ZEB and $12K for 6 Canadian banks that are in ZEB, ZEB would give you a minuscule advantage in a yearly dividend of $594.72 vs $592.64 for the 6 individual banks… Also ZEB would be 1 time commission vs 6 times commission. Also ZEB would allow you to reinvest the monthly dividend every month (354 shares x $0.14 = $49.56/month), whereas the quarterly dividend from the 6 banks, some you would need to wait over 12 months to reinvest the dividends cause the individual bank share price is higher than the dividend paid out for the year i.e Royal bank gives an annual dividend of $5.28, so with 15 shares, you would get $79.20 but 1 share of RY is currently $130.46. So even with a MER associated to ZEB, it has it’s advantages. The only thing I can think of where the 6 individual banks might be better is that they could split and you would get more shares over the long run…

Very interesting, thanks for doing the calculation. I wonder if this changes from time to time though.

I have been into CIB512 for 10yrs and it pays a nice Div of .72Cents very solid and great return at it value today. I have switched to being my own financial advisor and have switched the fund to a lower MER CIB239 series F still pays .06×12 or .72..

The obstacle to direct ownership of bank shares cost: acquisition & transaction fees

Banks’ mkt price per share are high, and unlike ETFs, little chance of free trading .

Therefore you need a substantial amt of money to buy say a minimum number of shares in all six banks.

You’ll need a minimum dividend amt coming in to take advantage of dividend reinvesting.

That being said, if you have the money, I prefer owning the banks directly.

Hello

I’m perplexed. ZEB’s MER, appears to be .62% on their Fact Sheet, .60% on Yahoo Finance.

Where does the .28% in your list above come from?

Are the fact sheet & yahoo not accurate?

http://fundfacts.bmo.com/EtfEnglish/BMO_Equal_Weight_Banks_Index_ETF-EN-CAD_Units.pdf

https://ca.finance.yahoo.com/quote/ZEB.TO?p=ZEB.TO&.tsrc=fin-srch

From their website directly:

https://www.bmogam.com/ca-en/advisors/investment-solutions/etf/bmo-equal-weight-banks-index-etf-zeb/

Management Expense Ratio: 0.28%

On the fund fact sheet there’s an * that states: During the last year the management fee of this series was reduced. The adjusted MER is 0.28% and represents what the MER would have been had the change been in effect during the full financial year

Any inconvénient with holding the 6 banks individually in your portfoiio?

Nope, haven’t encountered any inconvenience with holding 6 banks individually.

Brilliant and Thoroughly reflecting common people capabilities and risk tolerance …

Your sharing is a fantastic approach to contributing back to society …

Keep on the Great work

Stay safe Keep well Keep sharing

Zeb fee have droped to .25% a few months ago…

Thanks, updated accordingly.

Great analysis Bob. I took a page out of your investment advice from way back and invested directly into Canadian bank stocks rather than through an ETF.

As many observers pointed out, “why pay a bank (MER) to hold distributed bank stocks?”

Being able to trace those dividends straight from the source alone is worth doing the homework to balance the distribution yourself.

ETFs should be reserved for true diversification, any ETF that is industry-specific sounds like a cash-grab to me.

Thank you Olivier. I think ETFs are great when you use them properly.

I noticed you mentioned vgro and xeqt. But why not veqt ? That would fit the bill I suppose!

Thanks

VEQT is a great pick too. See comparison here – https://tawcan.com/all-equity-etfs-veqt-xeqt-hgro/

Great post! Personally prefer to invest in Canadian banks independently outside of an ETF. I had a dividend ETF previously and ended up selling it.

We think alike. 🙂

I can think of only one scenario where buying something like ZEB might be warranted. If a person is just starting out as an investor, and is only saving a small amount each month, then perhaps you use a platform that allows you to buy ETFs for free, and you buy units of ZEB. Even then, it’s very focused on a single sector.

Frankly the MER for ZEB is highway robbery. Nowadays you can even use something like WealthSimple Trade and buy individual stocks for free. For something as core as the Canadian banks, once you reach some critical mass, just buy the shares.

My favorite Canadian dividend ETF is XEI, the iShares S&P/TSX Composite High Dividend Index ETF. With this one, you at least get something for your 0.2% MER. You get a bucket of 75 holdings, with some sector diversification, and (currently) a 4.36% yield.

You need to get something for your MER dollar, because that money is coming out of your pocket.

I’m a bit suspicious of those funky ETFs that also use options to try and juice the yield. There is no guarantee that it does anything but drag down the return, and it may affect the taxation of the distributions.

When you buy yourself a common share of a Canadian bank, you get a quarterly eligible dividend. It’s very predictable, and nothing is skimmed off the top.

I think you’re better off buying a broader index like XEQT or VEQT rather than buying a concentrated Canadian index ETF…but maybe that’s just me. 🙂

You’re right. Buying yourself a common share of a Canadian bank makes dividend income very predictable.

Thanks for the great article. I want your opinion: which one is a better ETF, is it XIU or XEI?

Hey great write up. Question from an American reader. I understand in Canada dividends from Canadian companies receive favorable tax treatment. Does that include ETFs, or do you have to own the underlying stock? If the latter, is that not also a reason to hold the individual stocks?

Yes that includes ETFs as well.

I actually did not know ETFs were allowed to have options embedded as part of the securities they hold. I learned something new today.

I am starting to get skeptical of bank stocks though. Although they are a big business, most seem to be slow at embracing and adapting to change. They love to overcharge customers, these days it seems like.

Yes ETFs can use options as part of the investing strategy. 🙂

Excellent article. I have pondered the ZEB etc…. dilemma for some time. You writing has cleared up several points to consider.

Thank you

Colster

You’re welcome.

With just so few holdings, indeed why bother paying management fees as high as 0.7%. RBNK seems the best choice but even then… Since you mentioned VBAL and VGRO, for predictable income what do you think about VRIF? It’s quite new and I’m curious as to your opinion on this one.