Happy new year everyone! What a year 2022 was and that wasn’t an understatement.

In 2021, our portfolio returned 32.8% excluding all the contributions we made throughout the year.

2022, however, was the opposite – a red and volatile year that many investors will want to forget completely.

Update: Some readers have asked about our portfolio return in 2022. Given that we were out of the country for 5 weeks and just got back to the daily routines, I didn’t have the chance to crunch the numbers (still catching up on many things). Anyway, after going through all the numbers and removing contributions and dividends, our portfolio returned -5.4% in 2022. I hope this answer any questions and no, I wasn’t deliberately trying to deceive readers by not posting our portfolio performance. Thanks.

Although our portfolio was down a bit in 2022, mostly caused by Algonquin Power & Utilities Corp’s poor performance and the bear market, we’re not concerned.

Why?

First of all, we’re looking at unrealized losses. They’re called paper losses for a reason. We only lose money when we actually sell the losing stocks and we have no plan in selling.

Second, since we’re still in the accumulation phase of our financial independence journey, we are actually quite happy to see a volatile bear market and stock prices going down. Beaten down stocks meant we were able to buy cheap assets – by dripping additional shares at each dividend payout and by adding new cash.

I really hope the volatility will continue in 2023 to allow us to build up our dividend portfolio.

In early December, we flew to Denmark for a 5 week family vacation trip. Although we had 1.5 hours of transit time in Toronto Pearson Airport, we almost missed our connecting flight, because our first flight was delayed by 1.5 hours.

While in the air, I was able to check on Air Canada’s app to find out that our 2nd flight was delayed by 20 minutes, giving us a little bit of time to get to the departing gate. We didn’t want to miss our 2nd flight because there were no more direct flights from Toronto to Copenhagen for the next couple of days. And the connecting options were quite undesirable (one option was to fly from Toronto to London then London to Amsterdam, then finally Copenhagen).

When we landed in Toronto, we ran from the end of Gate D in Terminal 1 to the end of Gate E. It wasn’t the first time that Mrs. T and I had to run in an airport to catch a flight (Zurich Airport, Frankfurt Airport, Paris Charles de Gaulle, and Chicago O’Hare to name a few). But it was different running while making sure our kids were keeping up with us.

Fortunately, we made it with a few minutes to spare. When we finally got to our seats, we were drenched in sweat!

The pilots ended up waiting for other passengers and all the luggage because it was the last direct flight available. Maybe we didn’t need to run at all?

But who wanted to take the chance right?

Oh, the joy of air travel and catching connecting flights!

Thanks to the remote work model developed as a result of the COVID-19 pandemic, I was able to work remotely in Denmark for 3 weeks and take a vacation for 2 weeks.

Since our family is big on LEGO, we knew we had to go back to LEGO House and spend the entire day there. Despite spending 9 hours in LEGO House, we didn’t get to see and play with everything. We will have to go back and check out this wonderful attraction another time.

When it wasn’t pouring rain we enjoyed the great Danish outdoors (I called Denmark Rainmark at one point of the trip… we went from Raincouver to Rainmark ha!).

Of course, visiting Denmark meant a lot of eating and having a lot of hygge.

The last time we visited Denmark was for the 2019 Christmas/2020 new year so it was really nice to see the Danish side of the family again. My Danish is getting a little bit better as I could understand some conversations or pick up a few words here and there. Learning Danish on Duolingo definitely helped.

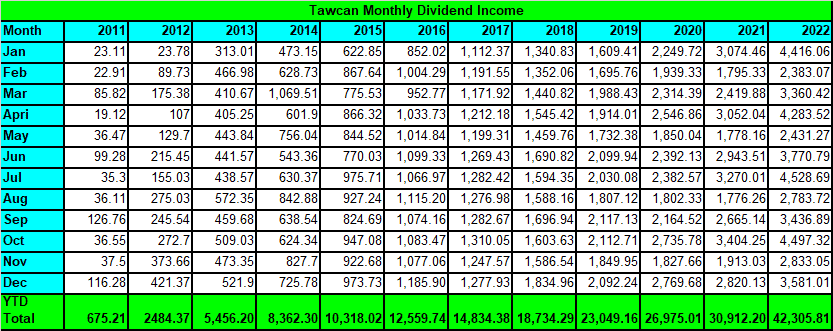

Dividend Income – December 2022

Back to dividend income, shall we?

In December we received pay cheques from the following companies:

- Brookfield Asset Management (BAM.A)

- BlackRock (BLK)

- Brookfield Renewable Corp (BECP.TO)

- Canadian National Railway (CNR.TO)

- Canadian Tire (CTC.A)

- Dream Industrial (DIR.UN)

- Enbridge (ENB.TO)

- Fortis (FTS.TO)

- Granite REIT (GRT.UN)

- Hydro One (H.TO)

- Intact Financial (IFC.TO)

- Intel (INTC)

- Johnson & Johnson (JNJ)

- Coca-Cola (KO)

- McDonald’s (MCD)

- Manulife (MFC.TO)

- Magna International (MG.TO)

- Qualcomm (QCOM)

- RioCan REIT (REI.UN)

- SmartCentres REIT (SRU.UN)

- Suncor (SU.TO)

- Target (TGT)

- Visa (V)

- Waste Connection (WCN.TO)

- Waste Management (WM)

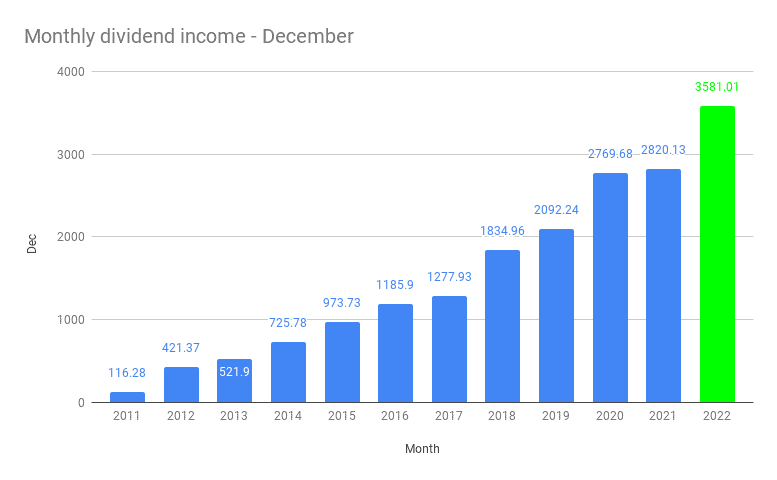

The 25 pay cheques added up to $3,581.01. Receiving over $3,500 in dividend income was a nice way to wrap up the year.

Compared to December 2021, we saw a YoY growth of 26.98%. Considering we’re facing the law of the big numbers already, I’m really pleased with our YoY growth.

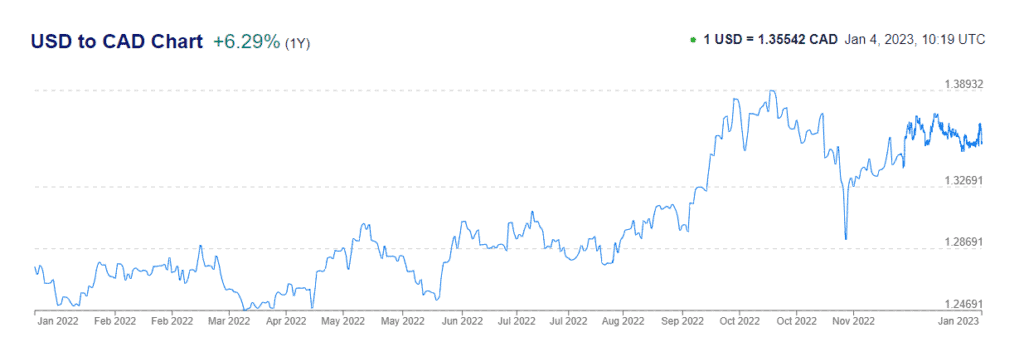

Out of the $3581.01 received, $643.67 was in USD with the rest in CAD. That’s roughly a 20-80 breakdown (rounded up). December was one of those months in which we received more USD dividends than in other months. The goal is to continue increasing our exposure to US dividend paying stocks so we can receive more USD dividends.

The USD to CAD exchange rate varied quite a bit in 2022. If we had converted our USD dividend income to CAD every month, our overall dividend income would have been arbitrarily inflated in Q4.

Therefore, to keep the math easy and avoid fluctuations in our monthly dividend income, we do not convert USD to CAD when reporting our dividend income.

The top five dividend payers from December were Brookfield Renewable Corp, Enbridge, Fortis, Manulife, and SmartCentres REIT (not in order). The total from these five dividend payers was $2,530.27.

These top five payers contributed 70% of our December dividend income. Ideally, I’d like to reduce that amount to 60% or lower so our dividend income sources are more diversified.

Dividend Increases

In December, a number of companies we own announced dividend hikes.

- Waste Management (WM) increased its dividend payout by 7.7% to $0.80 per share.

- CIBC (CM.TO) increased its dividend payout by 2.41% to $0.85 per share.

- Bank of Montreal (BMO.TO) increased its dividend payout by 2.88% to $1.43 per share.

- TD (TD.TO) increased its dividend payout by 7.86% to $0.96 per share

- Royal Bank* (RY.TO) increased its dividend payout by 3.13% to $1.32 per share.

- Enbridge* (ENB.TO) increased its dividend payout by 3.20% to $0.8875 per share.

- National Bank* (NA.TO) increased its dividend payout by 5.43% to $0.97 per share.

* These were announced on November 30 but I forgot to cover them in the November dividend income report.

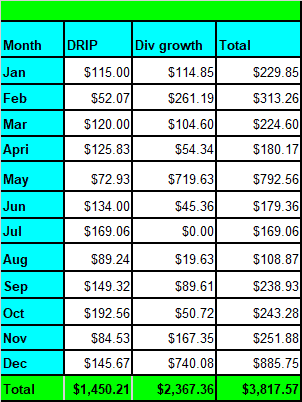

I always love seeing dividend hikes because they mean we’re getting a raise without having to lift any fingers. Our forward annual dividend income increased by $740.08 as a result of these dividend hikes. At a 4% dividend yield, that’s the equivalent of adding $18,502 of new capital.

Dividend Reinvestment Plans

Each month, we reinvest our dividends by enrolling in drips whenever we’re eligible. Dripping allows us to dollar cost average over time without paying any trading commissions. When the stock price is depressed due to market volatility or bad news, we can add additional shares at a lower price; when the stock price is inflated and the price is above the dividend amount we’re collecting, we simply don’t drip any more shares and can reinvest the money elsewhere.

In December we dripped the following shares:

- 6 shares of BEPC.TO

- 28 shares of ENB.TO

- 3 shares of FTS.TO

- 2 shares of INTC

- 1 share of KO

- 12 shares of MFC.TO

- 2 shares of REI.UN

- 5 shares of SRU.UN

We added 59 more shares to our dividend portfolio and added $145.67 toward our annual dividend income.

Combining dividend hikes and DRIP, we added a total of $885.75 toward our annual dividend income in December 2022. What’s more amazing is that we increased our forward annual dividend income by $3,817.57 in 2022 through dripping and organic dividend growth.

At a 4% dividend yield, increasing dividend income by $3,817.57 is the equivalent of adding $95,439.25 worth of new cash. This is the power of growing dividend income via organic dividend growth and DRIP!

Dividend Transactions

Just before the end of the year, we decided to make a small change to our portfolio. As many of you know, Intel’s share price has struggled in the last couple of years, so we decided to close out our position in Intel.

I know you’re probably thinking – “why sell Intel when it’s at its 52-week low and when the price is the lowest ever in the last 5 years? Why not just keep Intel and wait for the price to recover?”

Yes, we could have certainly done that and that’s one of the beauties of owning dividend paying stocks – if the price drops, as long as the company can continue paying out dividends and not cutting dividends, investors can collect dividends and wait for the share price to recover.

Despite Intel investing billions in new fabs in the US, I believe the recovery is going to be very slow and painful. Intel has really gotten behind in fabrication technology compared to the likes of Samsung and TSMC. For example, both Samsung and TSMC are already shipping chips based on the 3 nm process technology but Intel won’t be doing that until 2024. Intel used to be in the driver’s seat but now they have to play the catch-up game.

In addition to falling behind in fabrication technology, Intel is facing a lot of competition in the CPU and GPU markets from the likes of Qualcomm, AMD, Nvidia, and Texas Instruments. Intel is no longer as dominant in the CPU/GPU market as they were a decade or two ago.

Let’s also not forget Apple is moving away from Intel’s chips and using Apple’s own M series Apple silicon, which will only hurt Intel CPU sales.

I have no doubt Intel will recover eventually but we decided that our money can be invested better elsewhere. We bought Intel many years ago so we closed out the position with a decent profit.

After closing our Intel position, we invested the proceeds and some USD cash and purchased 57 shares of Johnson & Johnson and 10 shares of Costco.

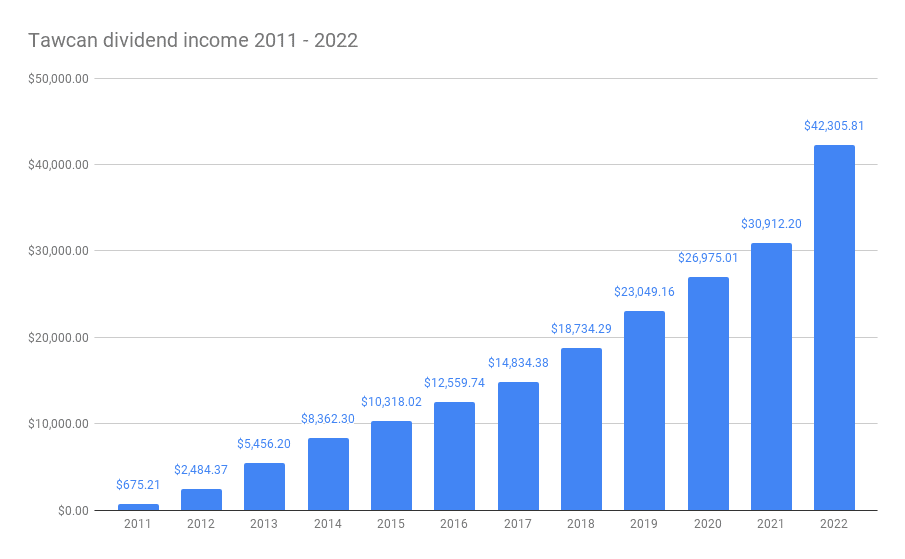

2022 Dividend Income Review

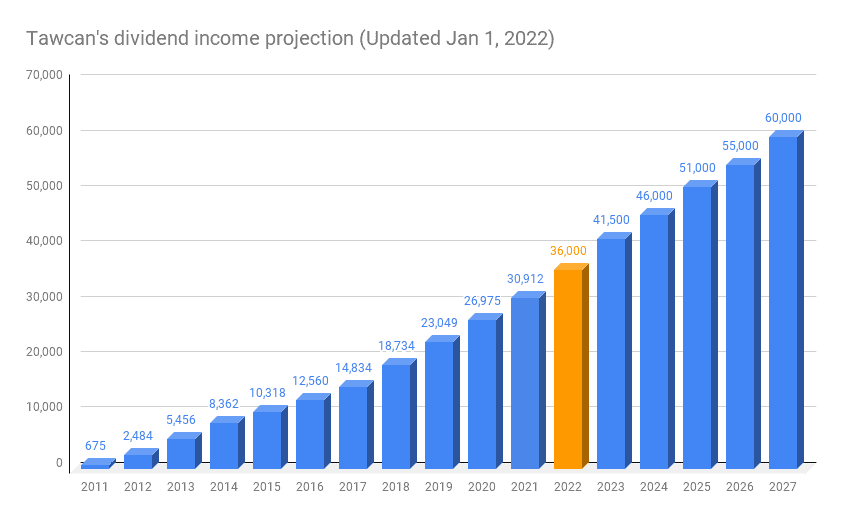

In 2022 we received a total of $42,305.81 in dividend income and completely overachieved our goal of receiving $36,000 in dividend income for the year.

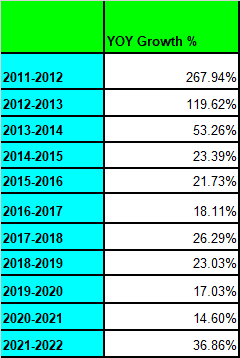

We grew our dividend income by 36.86% YoY, it was the biggest jump since 2014. Needless to say, 2022 was a very successful year for us in terms of dividend income.

How did we manage to grow our dividend income so much in 2022?

There’s no secret really. Thanks to our relatively high savings rate, we were able to invest a lot of money in the last few years. I also have to thank Mrs. T for being completely on board with our living off dividends FI plan and being super supportive.

While it is important to cut necessary expenses and fully optimize expenses, I believe there’s only so much you can do before you start depriving yourself and your loved ones. Therefore, it is far more effective to try to maximize your income. This is exactly what we did in 2022 – I asked for a raise at my full time job (and got one), Mrs. T’s doula business was more profitable, and both of us continued improving income from our side hustles.

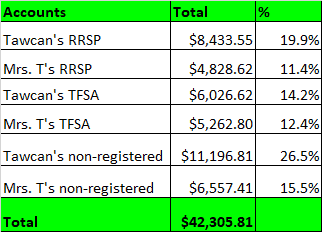

2022 Dividend Income Breakdown

Every year we aim to max out both TFSAs and RRSPs. Once we max out TFSAs and RRSPs, we then invest in non-registered accounts. We invest this way so most of our dividend income is either tax-free (TFSA) or tax-deferred (RRSP). Only a portion of our dividend income is taxed.

Since dividend income from our RRSPs will be eventually taxed at our marginal tax rate when we make withdrawals, we are planning RRSP early withdrawal strategies to minimize taxes.

Generating dividend income from TFSA, RRSP, and non-registered accounts will give us the ability to pull different levers when we are living off dividends in the not so distant future. Our 2022 dividend income breakdown is as below:

- RRSP: $13,262.17

- TFSA: $11.289.42

- Non-Registered: $17,754.22

From a percentage point of view:

- RRSP: 31.3%

- TFSA: 26.7%

- Non-Registered: 42%

In other words, over 25% of our 2022 dividend income was tax free and another 31.3% was tax deferred. To maximize overall tax efficiency, the dividend income was split between Mrs. T and me.

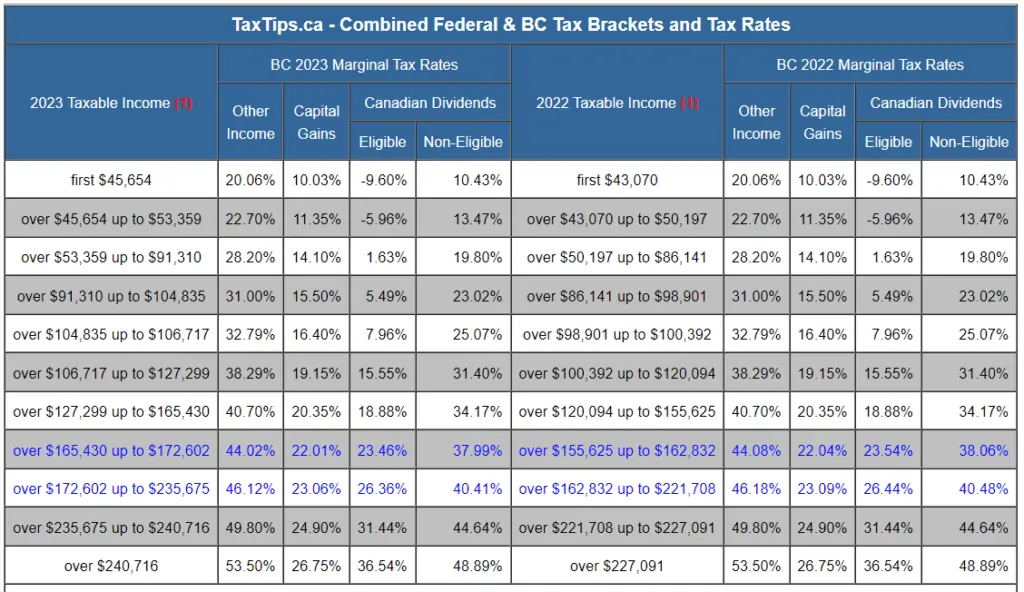

So just over $11,000 of our dividend income will be taxed under me and about $6,600 of our dividend income will be taxed under Mrs. T. As you can see from TaxTips.ca’s combined federal and BC tax brackets and tax rates, eligible dividend income is taxed much more favourable than working income.

We will definitely take advantage of the favourable treatment of eligible dividends when we are financially independent and living off dividends.

Summary

Wow, what a great way to wrap up the year with another solid monthly dividend income! We feel very blessed and fortunate that our money is working hard for us so we don’t have to.

As usual, I like to put things into perspective. At $42,305.81, that’s the equivalent of:

- $115.91 per day or $4.83 per hour

- $162.71 per day of working wage, or an hourly wage of $20.34.

It was really nice and exciting to see that we exceeded our Jan 1st, 2022 dividend income projection by two full years. I will have to update our dividend income projection again to reflect our improved progress.

Dear readers, how was your 2022 dividend income?

Hello. You only get $8k in div from your rrsp?? Why is it so little when you said you max it out every year. Seems like youve been working a long time so should have earned the more room but your overall limit feels low. Is there a reason for this?

Hi Jules,

Mrs. T’s RRSP is a spousal RRSP. I’ve been adding money in the spousal RRSP rather than my own for tax efficiency reasons.

What a great end to the year Bob! Sounds like your trip was great although the travel itself was hectic. Really impressed with you guys adding nearly $900 in forward dividends in December alone with just DRIP and dividend growth. That’s really amazing!

Thanks JC.

Outstanding Bob.

The beauty is your 60K target income for 2027 will likely all be TAX FREE. The current income of 42305 certainly is for 2022.

Thank you Gruff403.

Great article I’ve enjoyed reading your blog since a guy at work recommended it. I’m not a tax guy and I don’t know the laws in Denmark but I’m sure you have to claim that income and file taxes in Denmark.

Thanks Jay. Are you referring to tax for dividend income? If we were to live in Denmark, it’d be taxed in Canada, as far as I know. Something to figure out in the future.

Very well done. Congratulations. I started before you (2005). What you are now seeing is the snowball effect kick in. 2022 was the first year I received –just barely– over $100k in dividend income. It does not take much % increase to really move the actual numbers skyward. If you have not tried supplementing the income with options, you may want to explore that avenue. I wish I had started doing this years ago. I studied it for a while then with a little hesitation sold my first contracts January of last year. I tracked the results. It made a huge difference and helped offset the market drop. My options income for the 2022 was $47k. So far, January 2023 I’m just under $5k with one week left in the month. Your portfolio is probably large enough to begin utilizing basic strategies, covered calls and cash secured puts. That’s all I do, and it’s easy. Since I use dividend stocks I already own or would not mind owning, I don’t feel it’s risky and I’m very cautious. I don’t use margin, play with stocks that are trendy. Everything I owns pays me to own it. Best wishes.

Congrats on solid dividend and option income. I have looked at options a bit but thought it’d take too much time for me. How much time do you spend each month on cover calls and secured puts?

Subjective question, opinionated reply. I don’t feel I spend much time for the income generated. I typically review weekly options every day, sell a few contracts if the numbers look right then anticipate the contracts will expire worthless. If a stock I would not mind owning gets hard hit on their ER then I’ll sell some puts with a strike price a few percent under. If I get the shares, I switch to covered calls a few percent above my cost basis until I dispose of them; at times I got stuck with them for several weeks, then the share price recovers and they are gone. If I don’t get the shares I take the profit from the contract and play again. It’s a lot of fun. When you look at a contract that only pays a few cents, keep in mind that those pennies add up over time. I envision you spend quite some time on your website, as it is nicely done. It’s all in what you enjoy doing. Keep up the good work. Best/

Great Post Bob, love the pics of Copenhagen, hate to hear about the Airline challenges, they seem like a common thing these days. You’re doing a great job with the dividends, I’m still holding my INTC, though I do have a ‘Call Option” set at a $31 strike price for the end of this week, so we’ll see if it executes. I agree there are better options like TSMC and Qualcomm.

Thank you Jim. Yea, probably could have done a call option and see what happens to generate some money but didn’t want to mess around. 🙂

Love your site. Have you ever considered that you are still just stock picking and that the dividends are not perfectly being compounded? Isn’t dividend income still taxed as income when filing taxes? If you were to buy HXT or HXS, you get the ‘drip’ built in without the income or tax. In the TFSA, if you hold HXS, you don’t need to pay the us withholding tax. Any thoughts? Isn’t it better to just sell shares from you regular trading account when you retire rather than being dividend income reliant? Thanks!

Thank you Jon. Yes HXT or HXS may work for some people. For us we like having the ability to pick our own stocks and determine the portfolio weighting.

Selling shares from your regular trading account when retired is a good way to generate income. Relying on dividend income, in theory, should give you more margin of safety compared to selling stocks. 🙂

Did you take a flight with the same airline or did you buy tickets from 2 different airlines? I only ask, because I always thought that they were responsible for bringing you to your destination if you buy a flight (with a connecting flight) from the same airline company.

Btw, seeing your year to year dividend income is very inspiring, I hope to be able to have a similar result as you. looking at your graph, I’m somewhere in your 2013-2014 dividend income bar right now.

Tickets from the same airlines. If we were to miss the connection, Air Canada would have rebooked us. The problem was that there were no direct flight for the next few days.

Tebrik ederim. Ben de temettü geliri elde etmek için yatırım yapıyorum ama yolumuz uzun. Turkiye’den sevgiler.

Teşekkür ederim

Amazing progress! If your 2022 divs went up over $11K and only $3.8K was from organic growth/DRIP then you guys are definitely squirrelling away a huge amount annually.

My own goals and progress are definitely much more modest since I am using a hybrid of index funds for growth and dividends to establish an income flow baseline in retirement. Plus I don’t make nearly as much as you guys! My dividend-focused holdings (started only recently) paid out ~$850 in 2021, $1900 in 2022, and expecting about $4100 in 2023. After that I am expecting about an average increase of around $1000/yr from contributions/DRIP/organic. My goal is to have about $10K/yr from my dividend-focused holdings and over $20K/yr for all distributions, and then sell some of my stocks and bonds annually to cover the rest of my expenses (which are modest).

If my non-dividend equity can grow fast enough then I may consider switching some of it over to dividends to get my baseline income higher and having to sell off less each year. Same with the fixed income I hold: if by switching them to dividends I can get close enough to my total income needs that I do not need to sell much of my equity each year, then I may do that since I won’t really need the fixed income to avoid any big sequence of return risks anymore.

Thank you Peter. Yup, squirrelling a lot of money over the last few years. Very fortunate that we have been able to do that.

Sounds like you have a solid long term investment strategy. 🙂

First of all Happy New Year to you and your family!! Very impressive dividend income for 2022.

I am hoping to increase mine as well for the year 2023!!

Thank you Raj.

Great update. After bad experiences we never do connections. Pretty easy from YVR to EU, Asia or Australia. To EU our best experiences have been Frankfurt and Schiphol. Avoid Heathrow and CDG Paris . We get the long haul direct flight out of YVR done with first as there are way more frequent flight or train connections in EU to get to your final destination. I will never travel to Toronto, Chicago or NY for connections ever again!

Our RRSP and TFSA additional 2023 contributions are completely in safe 5.1% brokerage GIC’s until the dust settles later this year.

Unfortunately there’s no direct flight from YVR to CPH or we’d be booking that flight all the time. Frankfurt can be a hit and miss though. Although once you’re over in Europe there are multiple flights going to Copenhagen daily. I have had many bad experiences connecting through Chicago…

Hi Bob I am glad to hear that your family had a chance to visit your extended family in Denmark 🙂 I have been MIA in commenting but have been reading your posts regularly 🙂 Thanks for sharing your progress and I hope I will be able to reach that level at some point! In 2021, I made dividend income of $382.86 and in 2022 I made a dividend income of $630.39, all of it taxfree/deferred! Obviously minuscule compared to your dividends given my smaller portfolio, but I am pleased nonetheless that I made my own progress by mimicking portions of my portfolio to hold positions that you have shared on this blog. Thank you and thank you 🙂 🙂 I wish you and your family a healthy and prosperous new year!

Hi Sarah,

Glad to hear from you. Congrats on your higher dividend income in 2022. Happy 2023 to you too. 🙂

This is a great read and though I was already invested in dividends it has given me the hope that I can achieve similar numbers as I grow my portfolio. Thank you.

Thank you Ryan.

Bob, it would be useful to know what your return was in 2022. Before and after dividends. Thanks Dave P.

To be honest I haven’t sat down and calculated because we’ve been in Denmark. Plan to write up on that later.

Yep I’d like to know as well!

Thanks

Looks like our portfolio returned -5.4% last year when subtracting contributions and dividends.

I think that’s very good. You must be close to -2% including div? Good work. Dave P.

Thanks David. 🙂

Well done.

Thank you.

Amazing work Bob! Such an inspiration for the entire Canadian dividend investors community!

#dividendinvesting #dividendincome #dividends

Thank you very much Dividendes & FNB.

Fantastic year, Bob. Very well done and exceeding your own expectations, giving yourself a 16% raise ($42K received vs. $36K projected) is amazing. Reminds me of my first full job in Canada. I used to earn $36K then switched to another job for $42K. Good times.

And glad you guys had an amazing vacation in Denmark and could catch your flight. Do they give you a hard time at work when telling them about your remote work from an international location plan (You don’t have to answer)?

Thanks Dreamer. We need to do a better job with the projection. Being completely off with the projection makes me look like I don’t know what I’m doing ha!

No, my boss was cool with working remotely, and actually told me to go for longer if I wanted. 🙂

Congratulations on a successful year! Nice job completely blowing passed your yearly dividend goal! Over $42K for the year is extremely impressive along with the HUGE year over year growth!

Happy New Year! Here’s to an even greater 2023! 😀

Thank you My Dividend Dynasty. Here’s to an awesome 2023.