Wow, it’s hard to believe January 2022 is done and we’re in February already. Hopefully 2022 doesn’t fly by this quickly.

Thanks to work giving me January 4th off, we enjoyed a fun day skiing with almost no crowd up at Grouse Mountain. Best of all, it was snowing all day so we got to ski on the fresh powder! It was nice to see that both kids were getting better on skis. They even tried the blue run a few times.

We are aiming to head out and ski a few more times before the season ends.

In mid-January, Baby T1.0 and I also enjoyed a day of snowshoeing with the Cub Scouts. Since the trail was mostly hard-packed, I ditched my snowshoes and hiked around with crampons. It was fun hiking around crampons and it certainly made me think of some of the mountaineering adventures I had in my 20’s.

Every year, Mrs. T and I would try out the different types of hot chocolate during the Greater Vancouver Hot Chocolate Festival. This year was no different.

Although the financial independence journey is about saving and investing money for the future, we believe it is vital to enjoy the present moment as well. Spending money isn’t the enemy, what you prioritize and the purpose behind the spending are what we need to focus on.

Note: For those that have contacted me via emails, I’d like to thank you for supporting this little blog of mine. I am always pleased to connect with readers but due to the large number of emails lately, I haven’t been able to rely as quickly and provide in-depth responses as I’d like to be. Please do not take offence if I wasn’t able to provide all the analysis you’re looking for.

For those readers that are looking for more in-depth and one-on-one guidance please feel free to take a look at the coaching service.

Dividend Income – January 2022

Ok enough pictures, back to dividend income shall we? In January we received dividends from the following companies:

- Algonquin Power & Utilities (AQN.TO)

- BCE Inc (BEC.TO)

- Bank of Nova Scotia (BNS.TO)

- CIBC (CM.TO)

- Canadian Natural Resources (CNQ.TO)

- Capital Power Corp (CPX.TO)

- Dream Industrial REIT (DIR.UN)

- European Residential REIT (ERE.UN)

- Granite REIT (GRT.UN)

- PepsiCo (PEP)

- Rogers (RCI.B)

- RioCan REIT (REI.UN)

- SmartCentres REIT (SRU.UN)

- Telus (T.TO)

- TD (TD.TO)

- TC Energy Corp (TRP.TO)

- VICI Properties (VICI)

- Wal-Mart (WMT)

- iShares All World Ex-Canada ETF (XAW.TO)

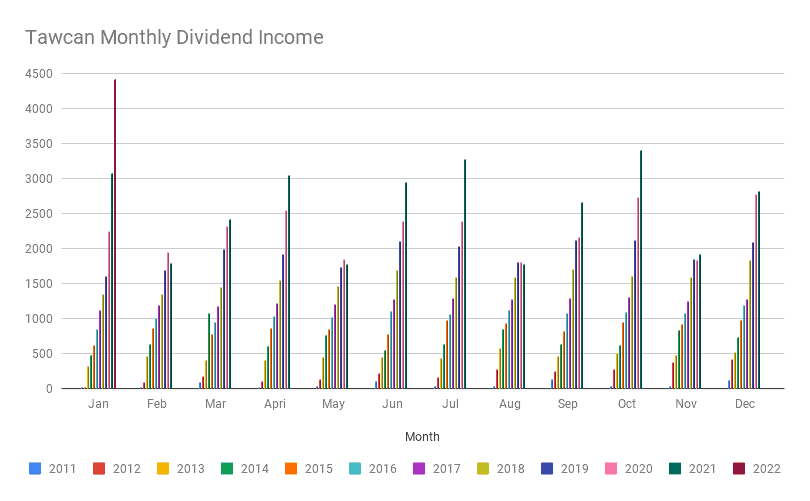

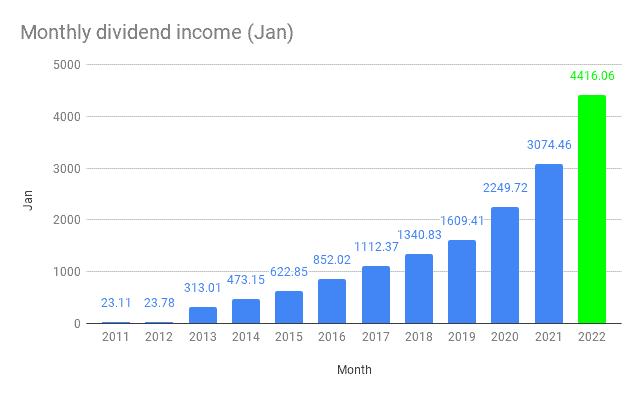

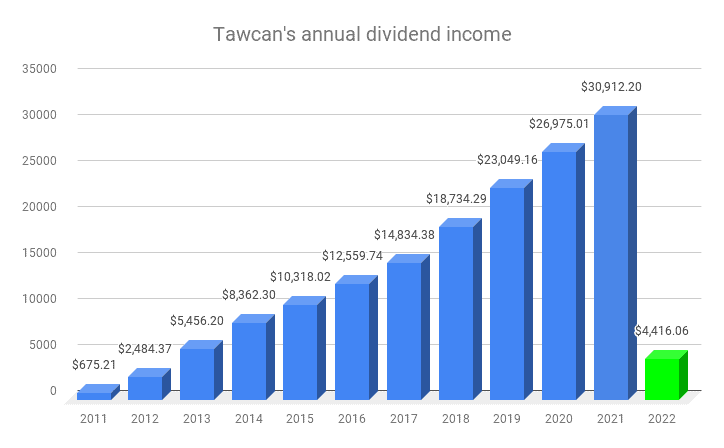

These 19 dividend paycheques added up to a whopping $4,416.06!

Wow, wow wow! We surpassed the $4,000 monthly dividend milestone for the very first time and set a new monthly dividend income record! It is absolutely amazing to start the year off with a very strong monthly dividend income.

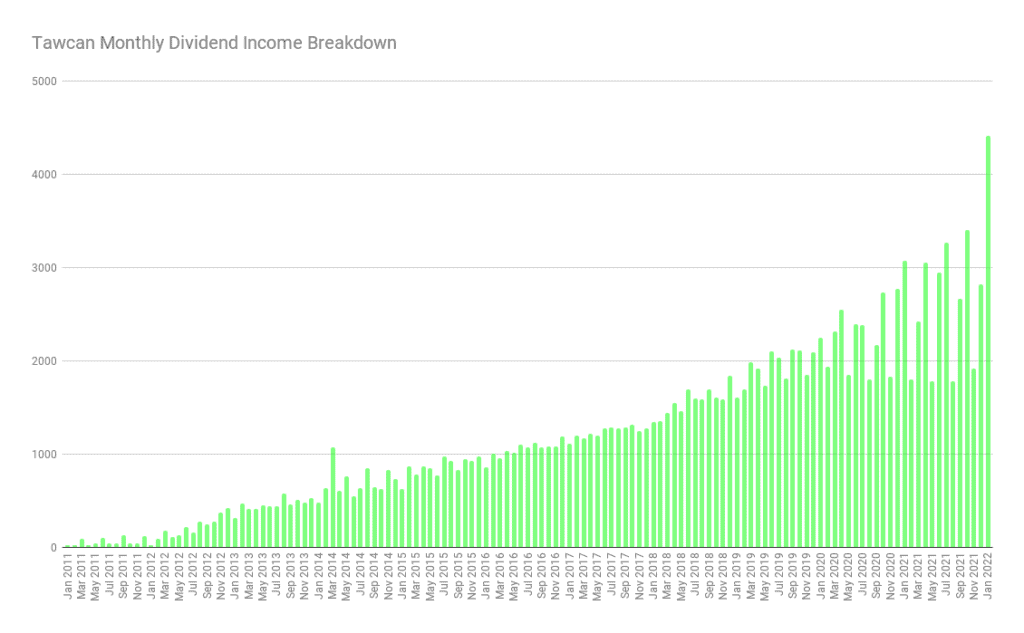

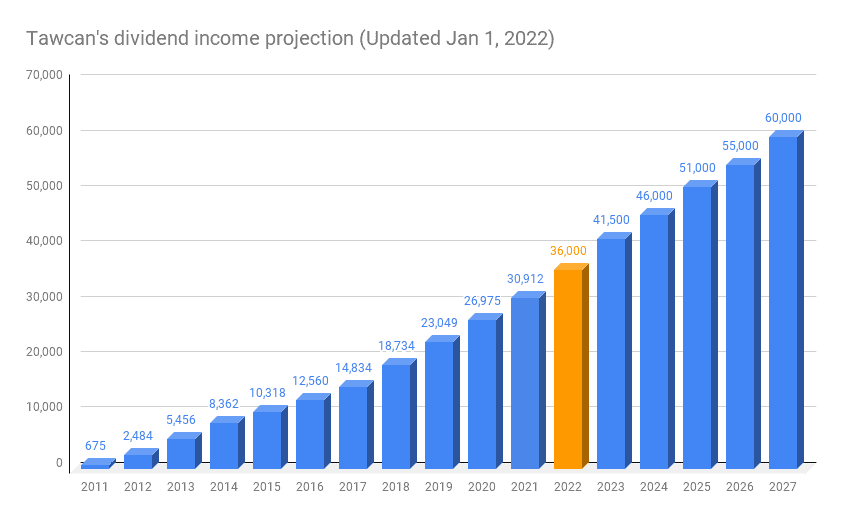

As you can see from the chart below, the monthly dividend income is trending upward quite nicely. We are starting to see a slight exponential growth in the last few years.

Compared to dividend income from January 2021, we saw a fantastic YoY growth of 43.64%. That’s right, over 40% growth. This was mostly contributed by a larger than expected payment from XAW.

Out of the $4,416.06 received, 229.19 was in USD and $4,186.87 was in CAD or about a 5-95 split. Long time readers will recall that we do not convert USD to CAD when reporting our monthly dividend income. This is to keep the math easy and avoid fluctuations in our monthly dividend income caused by changes in the exchange rate.

The top five dividend payers for January were Algonquin Power & Utilities, CIBC, Bank of Nova Scotia, TD, and XAW. These top five dividend payer amounts added up to $2,932.47 or 66.4% of our January dividend income.

January 2022 Dividend Transactions

We are always happy to see January 1 because that means new TFSA contribution limits. So on January 1st, we transferred $6,000 to each of our TFSA. We also transferred some additional money to the spousal RRSP and non-registered accounts for additional dividend stock purchases.

Some readers may recall that I recently wrote about the 6 stocks that I plan to add more of in 2022. With money in our TFSAs, spousal RRSP, and non-registered accounts, we purchased the following dividend paying stocks:

- 203 shares of Smart Centres REIT

- 64 shares of Granite REIT

- 320 shares of Enbridge

- 387 shares of Algonquin Power & Utilities

- 26 shares of Brookfield Rewewable Energy Corp

Roughly $37,000 was deployed throughout January and these purchases increased our annual dividend income by $1,970. Adding almost $2,000 toward our annual dividend income at the beginning of the year should help us with this year’s goal of $36,000 dividend income.

Some readers may wonder why we’re purchasing stocks when prices are so high. First of all, we believe in time in the market rather than timing the market. I would rather have most of our money invested in the market rather than sitting on the sideline waiting for a possible market drop or correction. Can you really predict accurately when a market drop or connection will happen? I sure can’t.

Most importantly, we can’t just look at stock price alone. Stock price alone doesn’t tell you whether a particular stock is expensive or not.

For example, consider stock A is trading at $5,000 while stock B is trading at $2. Is it fair to conclude that stock A is ultra-expensive and we shouldn’t invest in stock A by only looking at the stock price?

I don’t think so.

What if I tell you that stock A is trading at a price to earning (PE) ratio of 15 and stock B is trading at a PE ratio of 15.5? Does that change your perception that stock A is ultra-expensive? Sure it is still expensive relative to stock B but I would consider stock A “cheap” since it’s below a PE ratio of 20.

What if I tell you that stock A has a PEG ratio (PE divided by expected growth over 5 years) of 0.5 while stock B has a PEG ratio of 2. Which stock would you rather buy?

What if I tell you that stock A has a profit margin of 44% while stock B has a profit margin of 15%?

What if I tell you that stock A has $1B in cash and generates roughly $250M cash each quarter while stock B has $10M in cash and $35M in debt?

Which stock is more expensive? And which stock would you rather buy?

For me, it is a no-brainer that stock A provided more future growth and better profitability compared to stock B, despite trading at a price that’s 2500 times more than stock B.

So please, do not evaluate stock only on the stock price!

Dividend Reinvestment Plans (DRIPs)

When it comes to dividend investing, we try to keep things pretty simple by enrolling in dividend reinvestment plans whenever we are eligible. Once enrolled, we drip additional shares whenever we receive a dividend payout and allow the dripped shares to dollar cost average for us.

In January we dripped the following shares:

- 19 shares of Algonquin Power & Utilities

- 3 shares of BCE

- 5 shres of Bank of Nova Scotia

- 1 share of Canadian Natural Resources

- 2 shares of Capital Power Corp

- 1 share of European Residential REIT

- 1 share of Rogers

- 1 share of RioCan REIT

- 3 shares of SmartCentres REIT

- 8 shares of Telus

- 5 shares of TD

- 3 shares of TC Energy

- 2 shares of VICI Properties

- 19 shares of XAW

In total 73 shares were dripped and $2,970.61 out of the $4,416.06 received was reinvested immediately. This gave us a drip ratio of 67.3%.

For the remaining cash that wasn’t invested, we typically wait till there’s more than $1,000 in the account before making a purchase to keep the trading commission below 1% of the overall transaction cost.

By enrolling in DRIP we increased our annual dividend income by around $115 which is about a 3.8% initial yield.

Dividend Increases

I was very pleased to see a number of dividend payout increases throughout January:

- BlackRock (BLK) increased its dividend payout by 18% to $4.88 per share.

- Intel (INTC) increased its dividend payout by 2.9% to $0.365 per share.

- Canadian Utilities (CU.TO) increased its dividend payout by 1% to $0.4442 per share.

- Metro (MRU.TO) increased its dividend payout by 10% to $0.27 per share.

- Canadian National Railway (CNR.TO) increased its dividend payout by 19% to $0.7325 per share.

These five dividend increases added $114.85 toward our annual dividend income.

For the past two years, Canadian Utilities had only increased its payout by 1%. Although CU has had a 50-year dividend increase streak, the less-than-inflation payout increase may be considered as a selling indicator. Despite the high dividend yield and longest dividend streak in Canada, we may consider selling CU at some point and reinvest that money elsewhere.

Summary

Looking at the chart above, I can’t help but feel proud of how much progress we’ve made in the last ten years. In the first month of 2022, we have already exceeded the annual dividend income of both 2011 and 2012! We are also only about $1,000 short of the 2013 annual total.

I believe the chart is an excellent example of how powerful the dividend snowball is – by investing new capital, relying on organic dividend growth, and enrolling in dividend reinvestment plans, our monthly dividend income has skyrocketed from less than $60 per month to over $2,700 per month!

If you told me this was possible back in 2011, I would have thought you were insane. So for those of you that are just starting out with dividend growth investing, please do not get discouraged. It takes years to build up a sizable dividend income. Remember to stay focused and support each other along the long financial independence journey.

To put our 2022 dividend income in perspective…

- $5.93 per hour earning rate regardless of what we’re doing

- $27.60 per hour of working wage assuming 4 working weeks and 40 hours a week.

We feel blessed that our dividend portfolio is working hard for us so we don’t have to.

Happy investing everyone. How was your January 2022 divided income?

Back in 2020 I put my entire non registered portfolio into CNQ. I am very familiar with the industry and really felt it was a once in a lifetime opportunity. My investment philosophy is heavy influenced by Munger and I have learned to ignore the noise and sit patiently and wait. Today, my 500k is worth almost 3 million, and I am collecting just a bit under $100,000 a year in dividends alone. When I tell colleagues what I had done, I typically get all sorts of people telling my how risky it was or how I am not diversified. I have thought of selling some shares, but would be heavily taxed on the gains and would give up all those dividends. So instead, I took the dividends and bought another stock. I will continue to use the dividends to make further purchases when they become available. Since I have a paid off house, a fully indexed pension, and a maxed out TFSA and RRSP, I really don’t consider the strategy to be all that risky since I am diversified outside my non registered account. Fingers crossed for another opportunity for it to rain gold again.

Wow $500k on CNQ was a major holding that’s for sure. Congrats on your success.

If only you’d diversified into equal weight Googl, Amzn, msft and cnq then you’d have $10Million

@ Dad md – actually I am far ahead by buying CNQ, not to mention all the dividends I am collecting, now a bit over $125,000 per year after the latest increase.

Nice to see that dividend income still continue to grow month in and month out. WMT looks like a company that is firing on all cylinders. Not in my portfolio yet but they seem to be handling higher input costs pretty well.

Thanks DivHut. Up up and up. 🙂

Holy smokes, your dividend income blew up last month! Huge congrats. You can really see things accelerating.

Great pics by the way. My wife and I were also doing some snowshoeing last month. We usually do Seymour but went to Cypress this time around. Haven’t done Grouse yet.

Thank AL. Yea dividend income totally blew up in January.

I’ve snowshoed Seymour a bunch of times but for this time we did an easy trail because hiking with kids.

Congratulations on income.

We and our 5 year old daughter had great fun last month in the Ski Wee program at Grouse but we picked all the rainy and cloudy days the go!

I’m worried about the upcoming Federal budget which will be designed to confiscate income from successful hard workers to pay for the trillions spent on Covid. Successful hard workers like you are the typical target . I suspect dividend income and capital appreciation will pay.

That’s why I’m not completely counting on the strategy of dividends to provide safety.

For the last year I’m increasing my allotment to non dividend stocks like BRK.B, GOOG, AMZN. Likely these are long termers. I plan in the future to sell some every year when need cash

Thank you. Sorry to hear that you only had rainy and cloudy days up at Grouse. Hopefully you’ll get better weather next time.

Amazing Bob!! Good job deploying all that capital- did you wait a bit for the downturn in the market in January?

I liked the pictures of you having chocolate treats and having a “kids date” that’s a good idea for one on one time.

January was good for me too, just short of yours by about $50.

Thanks GYM. Some of the capital was deployed in early January. Some were deployed during the market downturn.

Congrats on a solid January too.

Congratulations on reaching the $4000 per month dividend mark. Thats a great achievement. Its a snow ball growth effect you may be truly experiencing. I believe at this stage you will just need to steer the dividend flows in the right way. Adding more capital would not be require unless you want to. So IMO thats a great flexibility to have.

Thank you Sridhar.

Outstanding.

Am I reading this correctly:

“Roughly $37,000 was deployed throughout January and these purchases increased our annual dividend income by $1,970.”

That means you invested that much last month???

Wow.

Amazing.

Mark

Yes you read that correctly Mark. Big purchases last month.

Congratulations on hitting the milestone! That’s awesome!

Do you setup DRIPs for stocks held in non-registered accounts or prefer taking it as a cash dividend? I ask because if you do DRIP in your non-registered account I would guess you would have to keep a lot of paperwork for CRA purposes and for you in calculating your weighted average cost when the time comes to sell the stock.

Thank you. We enroll in DRIP in all the accounts. Keeping the ACB isn’t really that hard if you utilize a spreadsheet.

Isnt about 50 stocks still too much to handle. I have about the same and struggle. I hold about 67% of my portfolio in 25 stocks. I term these are low risk stocks. In medium risk, I have about 11 stocks for about 20% of my portfolio. The reminder I hold in high risk/speculative investments. These are about 14 stocks (Theres a bunch of EV stocks that fall under this category).

So I find it a struggle to maintain and keep up to date on developments with these. I ideally am thinking of getting my low risk stocks to about 10-15.

I don’t think so. We only pick blue chip dividend stocks and once we invest in them, we try to enroll in DRIP and put them on auto pilot.

None of these 50 stocks are high risk/speculative investments.

I hold 24 as of last week and 70% of my portfolio is in the top 14. I also have about 4 stocks not in the 14 covering 5% as more opportunistic investments.

I am mostly curious as to the reasons.

Hey Tawcan,

Solid month. Just curious, how many holdings in total do you have and is it too much? Too little? Or just right?

Cheers.

Thanks Dividend Earner. We hold ~50 dividend stocks and 1 index ETF. I think that’s a little bit too much. I’ve been trying to trim it down to ~40 but it’s hard. 🙂

What do you find hard if you don’t mind me asking? Just curious.

Figuring out which one to close out. 🙂

I’ll get you to think 🙂

Drop the REITs … Put the money in a bank, it will be better overall in the long term but your income might drop in the short term.

Why still hold to Rogers?

Ha that’s a good point but are you worried about having more than 5% allocated per Canadian bank?

Yea looking to close out Rogers one of these days.

Ah, is that one of your rule? 5% per holding? or 5% per industry?

I have close to 9% in MSFT, AAPL, BLK, TD, ABBV.

I have 18% exposure to the Canadian banks total.

5% is relative too because of the size of my portfolio those have over $100K per hodling.

So the question is around the fear of a drop and the impact on ? total value? Yield?

I used to have a 5% rule and I was selling MSFT and AAPL to bring it down and that was a BIG MISTAKE …

Now, it it reaches over 10%, I will monitor and decide but no hard rules.

5% per holding but have a few holdings that are larger, it’s not a hard rule.

Since we hold 6 Canadian banks already, the sector quickly adds up if we do 5% across all 6 banks. Even at 4% each that’d give us 24% exposure, which seems a bit high to me.

What a fantastic month to start off the year Bob. 🙂 Nicely said about valuing a stock not based on its price alone. There’s a lot of moving parts, and I’m looking at picking up more shares as well. BLK is looking pretty cheap these days relative to where it was a few months ago.

My total dividend income in January was about $2,000 but I’m also working on some projects that should pay out a lot of capitals gains in the future.

Thanks Liquid. $2k is pretty solid considering you’re doing option trading for income too.

When you receive dividend income in a non-registered account, does that income get added to your Total Taxable Income? I realize you get a tax credit, but the taxable amount of dividend income could cause you to move up to a higher tax bracket, meaning all your other income will be taxed at higher rates? Do I have this correct?

It does but we split our dividend income between my wife and I so the actual amount that hits in the non-registered account is pretty small.

Just to add William, if part of your income is in a higher tax bracket, it doesn’t change the tax on all your income. Each bracket applies a certain % tax to the amount in that bracket. So if you have $5,000 in the top bracket, say, only that $5,000 is taxed at the highest rate.