Everywhere in the world, people require electricity and natural gas in their homes every day. Canada is no exception to this modern society rule. In fact, we depend on them. Long time readers will know that we like to invest in companies that produce products that people rely on every day.

The Canadian utility sector can be considered a boring sector because companies usually produce more consistent predictable revenues compared to other sectors. As a result, the sector is typically less volatile. Many Canadian utility companies pay an attractive dividend yield and have been able to raise dividend payouts for decades. For example, Fortis and Canadian Utilities have both raised their dividend payout for over 40 years. That’s a really impressive feat!

The high product dependency, consistent revenues, low volatility, attractive dividend yield, and consistent dividend payout increases make me believe that Canadian dividend investors should hold a percentage of Canadian utility stocks in their portfolios.

It’s no wonder I included some of the Canadian utility stocks in my best Canadian dividend stocks list.

Given Canada is a big country and there are many dividend paying utility stocks available to pick from. What are some of the best Canadian utility stocks? Let’s find out.

Canadian Utility Stocks

Although Canadian utility stocks tend to provide a good dividend income and have typically consistently raised dividend payouts each year, many of these utility stocks do not provide much growth. Another thing to keep in mind is that the utility sector is highly regulated so it is difficult for Canadian utility companies to expand.

Usually these utility companies grow by acquiring other utility companies, which would require getting government approvals, or by expanding into other business sectors. To continue to grow, one of the moves these utility companies are doing is expanding into the renewable sector.

| Company | Ticker | Yield | Dividend Growth Streak | 5 Year Growth Rate |

| Canadian Utilities | CU | 4.77% | 51 | 4.4% |

| Fortis | FTS | 4.07% | 49 | 6% |

| Atco Ltd | ACO.X | 4.39% | 29 | 7.1% |

| Emera | EMA | 5.12% | 16 | 4.7% |

| Brookfield Infrastructure Partners | BIP.UN | 4.17% | 15 | 6.6% |

| Brookfield Renewable Partners | BEP.UN | 4.55% | 13 | 5.1% |

| Algonquin Power & Utilities | AQN | 5.3% | 12 | 8.9% |

| Capital Power & Utilities | CPX | 5.11% | 9 | 6.9% |

| Innergex Renewable Energy | INE | 4.58% | 0 | 1.8% |

| Hydro One | H | 3.01% | 7 | 4.9% |

| AltaGas | ALA | 4.64% | 0 | -50.50% |

| Boralex Inc | BLX | 1.68% | 0 | 1.9% |

| Caribbean Utilities Company | CUP.U | 5.11% | 0 | 0.6% |

| Northland Power Inc | NPI | 3.24% | 0 | N/A |

| Polaris Infrastructure Inc | PIF | 5.62% | 0 | 2.64% |

| TransAlta Renewable Inc | RNW | 7.9% | 0 | 9.30% |

I included some smaller name companies that have not consistently increased dividend payouts to show that not every utility company is the same.

While it is easy to pick the five companies with the longest dividend growth streak, you’ll notice that fellow investors from the dividend growth investing community have picked some of the lesser-known Canadian utility companies like Boralex. Check out the best Canadian dividend stock picks from the DGI community.

Best Canadian Utility Stocks – My Top 5

Here are my top 5 Canadian utility stocks to buy. I picked these companies based on the consistency of dividend increases, dividend growth rate, and share price growth.

Remember, utility companies are sensitive to interest rates. When the interest rates are low, utility companies can borrow money for cheap and upgrade their infrastructures. The recent interest rate increases are hurting these utility companies. One prime example is AQN, they had to pay more and more interest on their debts because of the higher interest rates.

1. Fortis (FTS.TO)

Fortis Inc. is a Canada-based electric and gas utility holding company. The Company’s segments include Regulated Utilities and Non-Regulated Utilities. Fortis serves many different regions, including Arizona, BC, Alberta, New York, Newfoundland, Ontario, PEI, and the Caribbean.

- Dividend Yield: 4.07%

- Dividend Payout Ratio: 75.3%

- 5 Year Dividend Growth Rate: 6.%

- Dividend Increase Streak: 4 years

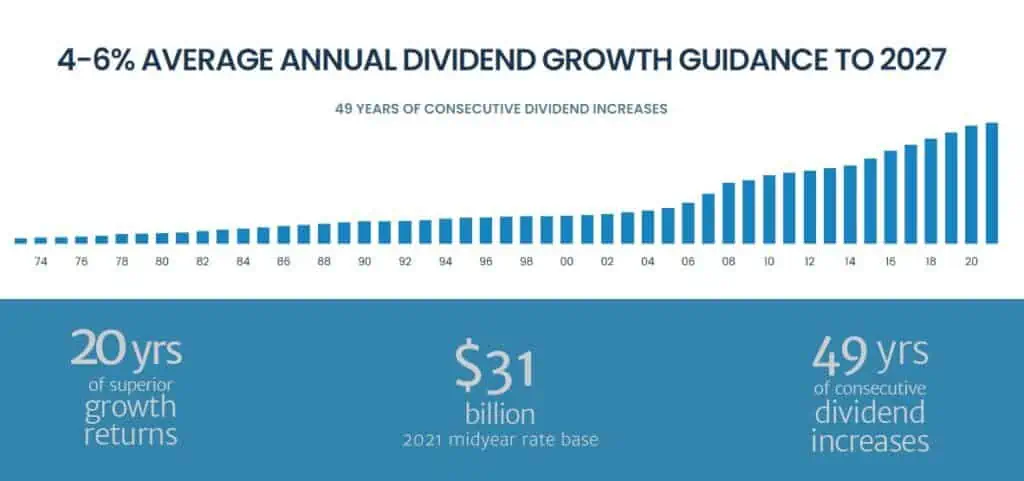

Who doesn’t like the 49 years of dividend increase streak? I sure do! Fortis is one of the few Canadian dividend paying stocks that can be called the Canadian dividend aristocrats. The dividend yield of ~3.5% gives dividend investors a good starting yield. Over the years, Fortis has been able to maintain a consistent and sustainable cash flow. This is quite important in the utility sector.

With the streak of almost five decades of dividend increases, in addition to the attractive yield, Fortis’ dividend payments can be considered bond-like. Since many Canadians must rely on natural gas or electricity to heat their home during winter or use natural gas or electricity for cooking purposes, this makes Fortis a very stable stock to own.

Fortis is also working hard to reduce its carbon footprint and increase its exposure to renewable energy. As an investor, that’s music to my ears.

2. Capital Power Corporation (CPX.TO)

We added Capital to our dividend portfolio only a few years ago. We added this position to increase our exposure to the Canadian utility sector and because we like the potential growth of CPX.TO.

Capital Power Corp has thermal, wind, solar renewable assets representing over 6,400 MW of generation capacity. On top of these renewable assets, it also owns natural gas, coal, and solid fuel energy units for electricity generation. The company realizes the importance of carbon-neutral and laying the groundwork to be carbon neutral by 2050. Currently, the company is working on carbon conversion and moving off coal power generation.

- Dividend Yield: 5.11%

- Dividend Payout Ratio: 130.5%

- 5 Year Dividend Growth Rate: 6.9%

- Dividend Increase Streak: 9 years

Although the standard payout ratio is above 100%. If we look at the payout ratio using AFFO per share, the payout ratio throughout is ~40%. The company aims to have a payout ratio of between 45% to 55%. Therefore, I’d expect Capital Power Corp to continue raising dividends for years to come.

3. Brookfield Renewable Partners (BEP.UN / BEPC.TO)

Brookfield Renewable Partners operates one of the world’s largest publicly traded renewable power platforms. Its portfolio consists of approximately 21,000 MW of capacity and nearly 6,000 generating facilities in North America, South America, Europe and Asia.

The company is a global leader in hydroelectric power, which comprises approximately 62% of its portfolio. It is also an experienced global owner and operator of, and investor in, wind, solar, distributed generation, and storage facilities.

The company’s investment objective is to deliver long-term annualized total returns of 12%–15%, including annual distribution increases of 5–9% from organic cash flow growth and project development. It has an established track record of creating value by prudently acquiring, building and financing assets, and actively managing its operations.

- Dividend Yield: 4.55%

- Dividend Payout Ratio: N/A

- 5 Year Dividend Growth Rate: 5.1%

- Dividend Increase Streak: 13 years

I like Brookfield Renewable Partners because I think there are a lot of future growths in the renewable space. The share price has dropped quite a bit in the last few years so this may provide long term investors with a good opportunity to purchase shares at a discount.

4. Emera (EMA.TO)

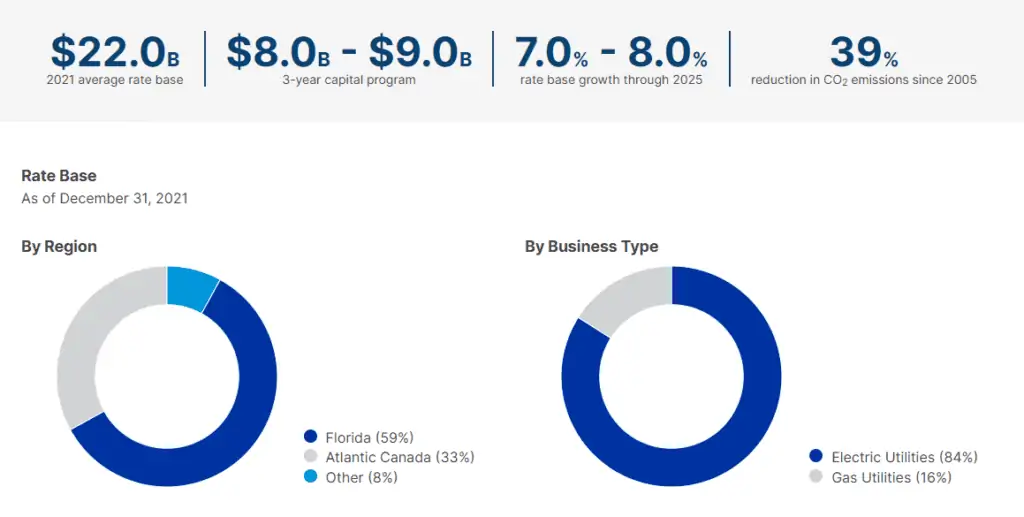

Emera started a a single electric utility in Nova Scotia and has grown into an energy leader with $36 billion in assets, serving 2.5 million customers in Canada, the US, and the Caribbean. In recent years, Emera has been focused on CO2 reduction and achieving net carbon zero. In addition to traditional utility generation, Emera has also been making investments in cleaner and renewable sources of energy.

- Dividend Yield: 5.12%

- Dividend Payout Ratio: 89%

- 5 Year Dividend Growth Rate: 4.7%

- Dividend Increase Streak: 16 years

Emera has been very shareholder friendly, raising dividend for 16 straight years with a 5 year dividend growth rate of 5.1% and a 10 year dividend growth rate of 7.0%.

Due to the increasing interest rates environment, however, the dividend growth rate may slow down slightly in the years ahead though. But at an initial yield of over 5%, the lower dividend growth rate shouldn’t be a concern.

5. Brookfield Infrastructure Partners (BIP.UN / BIPC.TO)

Brookfield Infrastructure Partners is one of the largest owners and operators of critical and diverse global infrastructure networks which facilitate the movement and storage of energy, water, freight, passengers, and data. It is one of the largest global infrastructure companies in the world. The company’s objective is to generate a long-term return of 12-15% on equity and provide sustainable distribution for shareholders while targeting annual distribution growth of 5-9%.

- Dividend Yield: 4.17%

- Dividend Payout Ratio: 415%

- 5 Year Dividend Growth Rate: 6.6%

- Dividend Increase Streak: 15 years

Over the years, Brookfield Infrastructure Partners have acquired high quality businesses on a value basis and opportunistically sell assets to reinvest capital into the business. For example, recently BIP saw an opportunity and offered to buy Inter Pipeline.

BIP currently has over $95B of assets under its management, including 6.6M electricity and gas connections,16,500 km natural gas pipeline, and 2,000 km electricity transmission lines. The company serves over 1.6 million residential infrastructure customers. To increase its growth, Brookfield Infrastructure Partners expanded into data infrastructure and owns 9,100 multipurpose towers and active rooftop sites, 52 data centres, and over 20,000 km of fibre backbone.

Like Brookfield Renewable Partners, Brookfield Infrastructure operates in a limited partnership (BIP.UN) and corporation (BIPC.TO). The Class A shares of BIPC are structured to provide an economic return equivalent to BIP units.

Knowing the share structures, I believe BIPC shares should have a slightly higher price premium over BIP.UN due to the more flexible corporate structure.

Summary – Best Canadian Utility Stocks

In summary, I believe every Canadian dividend growth investor should hold at least two or three of these best Canadian utility stocks in their dividend portfolio. What percentage one should hold in the utility sector is completely a personal choice. For us, we are comfortable holding between 10 to 15% in this highly dependable, low volatile, and stable dividend income sector.

For those that want to invest in utility stocks, you may also want to consider one of the best Canadian renewable energy stocks.

Since Canadians depend on using electricity and natural gas on a daily basis, it is nearly impossible for any of these top five utility companies to go out of business. You can certainly sleep peacefully knowing this. For some, including myself, may consider dividends from utility companies as bond replacements.

Want to learn to construct your own dividend investing portfolio and start investing in dividend paying stocks? I went through several methods on how I shortlist and screen dividend paying stocks. You may also want to take a look at this Canadian Dividend Calendar to see when the Canadian dividend all-stars pay out dividends.

Some of you might wonder if preferred shares have a place in your portfolio. This is a very personal question and totally depends on whether your aim is a total return or dividend income. Personally, I think there are too many preferred shares available and it can be very confusing looking at preferred shares from the same company and understanding all the different jargon. Therefore, if you’re considering holding preferred shares in your portfolio, it might be a good idea to utilize one of the best preferred share ETFs in Canada and let the professionals manage it for you.

If you’re reading this post, you are probably managing your own portfolio and may not want to use an ETF and pay the management fee, is there a way to do that? Fortunately, some smart folks created Passiv to do that for you automatically. With Passiv, the tool can put your portfolio on autopilot. You can build your own personalized index, invest, and rebalance all through a click of a button. Passiv can even calculate and execute the trades needed to keep your portfolio balanced. Essentially, Passive makes investing super simple! A community user account is free to sign up for. The elite member account is $99 per year…but it’s free for Questrade clients! Make sure to check out Passiv.

In case you’re curious, for diversification outside of Canada, we hold a handful of US dividend paying stocks. In addition, we utilize one of the low cost ex-Canada ETFs like XAW to diversify our portfolio internationally.

Do you already own dividend stocks and want to create a spreadsheet to track your portfolio? Take a look at my Google Spreadsheet Dividend Portfolio Template.

Want to learn more about how to analyze dividend stocks? Make sure you check out this comprehensive guide on how to read annual and quarterly reports.

Note: This blog post represents my opinion and not an advice/recommendation to purchase these stocks. Before you buy any stocks, please consult with a qualified financial planner.

There are only 4 top picks above instead of 5.

Did I misread somewhere?

Oops mislabeled one of them. Should be corrected now. Thanks for pointing it out.

Thanks for this, Bob! Apologies that I am late to this (as it was updated March 2024), but I am just curious if your opinion on any of these companies has materially changed since then? Or does everything essentially hold true since they are generally very stable over time? Thanks again!

I’d have no problem continue to hold or add more shares to any of these 5 companies. Hope this helps.

Hey Bob.. there’s been a steep drop

In AQN share price.

Do you see this as a buying opportunity?

I plan to write an analysis soon. 🙂

Thank you so much Bob for this great article,

Utility is my fav sector since I consider myself a conservative investor and I do hold FTS CU AQN EMA and CPX , what I wanted to ask Bob is how you calculate payout ratio for these companies because looking at yahoo finance payout ratio for FTS and AQN looks way higher.

Thank you so much for what you do to help new investors try to make a better decision for their financial future

Love my Fortis. We have CU in our joint investments too.

Both are good stocks to hold. 🙂

Great analysis Bob. This gives a good comparison of stocks within the sector and their dividend track record. Helps to see where each one stands vs. the other.

Good list. I’m not too familiar with the Canadian energy market myself so I can’t say I have an opinion on any of the stocks you listed. However, it goes without saying that utilities are relatively safe bets to produce income in the form of dividends where price appreciation is just the icing on the cake.

Sharing my own personal views regarding AQN, which is been discussed and liked by everyone and popular in blogs, youtube, etc. This is not a recommendation – just my own view. There are a few drawbacks which doesn’t appear at first sight. Im going to share this despite my unpopular opinion.

1) The capital structure is more oriented towards issuing more shares resulting in diluting shareholder value

2) Earnings are covering dividend but cash flows dont, which is a red flag

3) Debt-equity at 1-1.2 x appears good compared to other utilities but not so great because equity issuance has been used to bring it down.

4) A major chunck of revenue/CF goes back in to capex so not much of free cash flow for future. But this is justified given utilities nature of business and thats why stock is cheap.

5) Dividends are increasing or growing but not services from cash flows.

HOwever, there are good points too

1) They have solid margins

2) Good revenue growth and profits are growing too

3) Dividend growth is good but not supported by cash flows

It looks like there is some kind of a mixed bag with risk factors attached.

Very good points Sridhar, thanks for mentioning.

great list there Bob

Our utility sector is one of our highest sectors due to the run up of renewables. This space should continue to run in the future and is a great place to be.

I plan on adding more algonquin at these prices, although it would be nice if they stopped diluting their share count. =)

cheers

Yea it’d be nice if AQN stopped diluting their share count. We plan to add more too.

Great overview Bob. I like utilities too. Not the fastest growers but steady dividend growth with future potential and decent moats.

I think your Atco dividend growth number may be off. I believe its closer to 12% over 5 yrs.

Thanks for noticing that, you’re right, it’s closer to 12% over 5 years.

You’re welcome. Keep up the good job on your blog and your investing journey!