I’ll start the blog post with a quote from one of the smartest men that ever lived.

“Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.” – Albert Einstein.

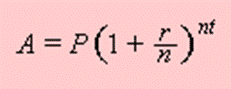

If you have taken math in school, you probably have come across the idea of compound interest. It’s a simple mathematical concept that shows the power of reinvesting the interests received from your principal. Since I’m a math nerd at heart I want to show you the standard compound interest formula.

What do the funny characters stand for?

P stands for the initial capital

r stands for the annual rate of interest (as a decimal)

t stands for the number of years the amount is deposited for

n stands for the number of times the interest is compounded per year

A stands for the final amount of money that you’ll get

With this formula in hand, I can show you the power of compound interest.

Imagine that I invest $5,000 at 5% annual interest rate for a year. If the interest is compounded annually I’ll get $5250 at end of the year. If I invest the entire amount for another year, I’ll get $5,512.5 at end of the 2nd year. Here’s what happens if I leave the money for 5 years and keep reinvesting the interests.

Year 0 – $5,000.00

Year 1 – $5,250.00

Year 2 – $5,512.50

Year 3 – $5,788.12

Year 4 – $6,077.53

Year 5 – $6,381.41

At end of the 5th year, my $5,000 initial deposit has grown to $6,381.41, or an increase of $1381.41. Because the interest is compounded each year, the actual annually return is greater than 5%. In this example I’m actually getting 5.52% annual return, an additional 0.52% more than the annual interest rate by simply doing nothing an reinvesting the interest. How cool is that?

The power of compound interest becomes even more apparent when I leave the money for a longer period. Let’s say I leave the money for 10 years. At end of the 10th year, my initial deposit would grow to $8,144.47. An increase of $3,144.47 or an annual return of 6.29%. The extra 1.29% is possible because the interest is compounded over 10 years, providing me with a better return.

What if other parameters like r and n change? Life gets a lot more exciting!

Scenario 1

The interest rate is now 10%. An initial deposit of $5,000 would give me $8,052.55 at end of the 5th year. That’s an increase of $3,052.55, or an annual return rate of 12.21%! An extra 2.21%! Nice!

Scenario 2

The interest rate stays at 10% but instead of compounding the interest annually, the interest rate is compounded monthly. At end of the 5th year, my initial deposit of $5,000 would become $8,226.55. That’s an increase of $3,226.55, or an annual return rate of 12.9%. Compared with scenario 1, an extra $174 is earned by simply compounding the interest monthly.

Scenario 3

Consider the same parameters as scenario 2 but instead of monthly compounding, the interest rate is compounded weekly. A $5,000 deposit would give me $8,239.65 at end of the 5th year, or an annual return of 13%. That’s an additional $187.10 than scenario 1 or an additional $13.10 than scenario 2.

If I make monthly contributions on top of the initial deposit, both the initial deposit and the monthly contributions are earning interest. The power of compound interest really takes off when regular contributions are made!

The power of compound interest is like rolling a small snowball down a long and steep hill. Initially the snowball is small but as it travels down the hill it starts picking up snow. The snowball slowly becomes bigger and bigger. As the snowball grows, it begins to roll down the hill at a faster and faster speed. Eventually the snowball becomes so big and so fast it’s unstoppable! Watch out!

This is the same concept that I would like to apply to our dividend portfolio. But how does this work? How does compound interest relates to dividend investing?

The answer lies in a very useful investing strategy called dividend reinvestment plan (DRIP).

A little background about the different types of DRIPs – regular DRIP and synthetic DRIP.

Regular DRIP

Regular DRIP is usually done through a transfer agent like ComputerShare. It requires you to acquire at least one share in a company and obtain the share in paper form. You then have to fill out DRIP enrolment forms and send them to the transfer agent for the company that you’ve chosen. Once regular DRIP is set up and running, the entire dividend amount is reinvested. In other words, fractional shares can be purchased. This is an effective way to build up your dividend portfolio with a small amount of capitals. This is a method that I’m currently set up for our son, baby T’s, dividend portfolio. That topic is for another post in the future.

You can find more information about regular DRIP on Canadian DRIP Primer.

Synthetic DRIP

Synthetic DRIP is what’s offered by discount brokers like TD Waterhouse and Questrade. With synthetic DRIP, only full shares can be purchased. If the dividend amount received is less than the price of the share, no share is purchased. Synthetic DRIP requires you to own sufficient amount of shares to enrol. For example, Royal Bank (RY) currently pays out $0.75 of dividend per share each quarter. In order to enrol in synthetic DRIP with your discount broker at current price of $82, you would need at least 110 shares of RY, or $9,020 ($82/$0.75 in case you’re wondering). Typically you want to invest more than the minimum amount of shares required in case the price of Royal Bank continues to go up. In this case 125 shares of RY would probably gives enough buffer to make sure enough dividend is received to cover the stock price.

Regular DRIP is powerful because the entire dividend amount is reinvested. The only downside is that you need to deal with fractional shares when calculating the cost basis. This could lead to some messy accounting. Synthetic DRIP, on the other hand, only purchases full shares, making accounting simpler.

How does all this information relate to our dividend portfolio? As mentioned in my dividend investing approach previously, I try to reinvest dividends whenever I can. Since our investment accounts are with TD Waterhouse and Questrade, we can only utilize synthetic DRIP. Whatever dividend money left over from synthetic DRIP is accumulated with other dividend incomes and to be used to initiate other positions.

Take the Royal Bank example again, I’ve made several purchases throughout the years to finally accumulate enough shares to start synthetic DRIP. Although initiating new positions to further diversify is very important, I’m always looking to add to our existing positions so synthetic DRIP is possible.

Enrolling in DRIP has definitely helped us in harvesting the power of compound interest. With our dividend portfolio, the current forward looking dividend is about $8,500. If I were to take out the forward dividend amount gained from the DRIP’ed shares, our forward looking dividend would drop to about $8,000. By utilizing DRIP and the power of compound interest, we are able to make additional $500 in our dividend income!

As I pointed out in the compound interest scenarios, the number of times the interest is compounded per year makes a significant difference. This is true for DRIP as well. Typically dividends are paid out quarterly, so the interest is compounded 4 times each year. However if you were to invest in stocks that pay monthly dividends, you would be compounding your dividend 12 times each year. The compounding effect takes off very quickly after a few years.

A word of caution on DRIP. If you’re DRIPing REITs or income trusts it’s best to hold them in registered accounts like RRSP or TFSA to avoid complicated tax calculation.

Do you utilize DRIP to power boost your dividend portfolio?

You mentioned you have a dividend portfolio for your baby, can you please tell me more about it? How did you open it and where?

Here are some articles I’ve written on this topic.

https://tawcan.com/creating-legacy-dividend-portfolio-kids/

https://tawcan.com/creating-a-legacy-kids-dividend-portfolio-update/

Hope this helps.

Hi, great site! Learning a lot, thanks!

When looking at Regular DRIPs, if fractional shares are purchased, how does one account for it? I’m not sure I understand, I’m trying to visualize it. For example, if you don’t earn enough income from dividend to reinvest the dividend in buying back the same security, where does this fractional share reside? How does that appear in your brokerage holdings? Essentially, what I want to know is, if a share of ABC is $10 and I made $8 of dividends, that would mean I re-purchased 80% of another ABC share, but since it didn’t buy a full share, where is this 80% share located? How can I account for it?

Thanks!

Not sure I fully understand. You’d own the fractional share.

For example if your purchased 100 shares at $10 then your ABC is $10.

Imagine you made $8 of dividend which gave you 0.8 shares. Then your new ABC would be

(100*10+8*0.8)/100.8 = 9.984.

I’m sorry, I don’t think I explained myself well and I don’t understand your reply and this is completely me, this is no reflection on you, so please allow me to try and re-explain my question. When I say ABC, I’m not referring to the adjusted cost base (ACB) if that’s what you thought I meant? I was simply using that as a ticker example of a stock.

I just don’t understand how fractional shares work. So the example I was giving was, if a stock XYZ costs $10/share and I have set up a DRIP with XYZ but the income I earned from the DRIP was only $8, then this means I only accumulated 80% of a full share cost of XYZ and therefore cannot buy 1 share of it, so a fractional share is bought instead. Is this correct?

If that is correct, then I just don’t understand “where” I can account for this. Meaning, when I log into my Questrade account, I can see all my positions of shares that I bought (ie., 20 shares of SBUX, 600 shares of AAPL, etc), but what would I see under XYZ for the fractional share? So let says before the fractional share was bought I owned 20 shares of XYZ, and after the fractional share is bought would I see something like 20.8 shares under my positions?

I hope that is a little more clear. I appreciate the feedback.

Hi,

Questrade does not support full DRIP. They only support synthetic DRIP where full share is purchased. For brokers that support full DRIP you’d see the fractional shares in your account. Does this make sense?

Yes, it does, thank you and I was aware based on your article that QT only has synthetic DRIPs, but my question is more about full DRIPs and how would I see it in my account? How will it be displayed? What exactly would I see? Would it be listed as 20.8?

Thanks again!

For our kids’ dividend portfolio we use ShareOwner which offers DRIP. It’s showing Telus as 20.9093 when it comes to number of shares we own.

Awesome, great, I always wondered how that worked. Thanks for following up!

Hi Tawcan,

It must be fun looking back at older posts like this one and seeing that the compounding interest idea is really starting to take off.

There’s a spreadsheet on David Fish’s drip investing page called DCA Model Calculator. I actually took that Excel spreadsheet file and formatted it so that it would work with the online Google Spreadsheets. The result is similar to your compound interest formula above but also takes into account stock growth, dividend yield, dividend growth, and monthly, quarterly and annual contributions. It is pretty incredible to see the results over a 30 year time frame.

A “live” version is available here. For more information and for a version that you can download yourself, see my Spreadsheet page.

Hi Scott,

We use the spreadsheet all the time. Thanks for sharing the live version. 🙂

I am still amazed that compounding is actually a thing we mere mortals are allowed to participate in.

I love the Einstein quote – for those that don’t understand compounding, it pains me to think of how much interest people in debt have to pay!

Hi Steve,

Totally, the power of compound interest also can work the other way when you’re eyeball high in debts. Too bad so many people don’t understand that.

Tawcan,

Couldn’t agree more about the power of compounding. It’s truly incredible. 🙂

I take full advantage of the power of compounding, but not through a DRIP. I reinvest 100% of my dividends, but do so selectively. This allows me to allocate capital in the best way I see fit, rather than potentially reinvest back into overvalued stocks or perhaps stocks I’d rather keep as smaller positions.

Keep up the great work!

Best regards.

Hi Dividend Mantra,

It’s good that you’re reinvesting all your dividends. That’s another example of compound interest at work. 🙂

Cheers.

Hi Jason,

Do you have to pay any transaction fees by reinvesting all your dividends?

Tawcan, Scottrade only allow me to Flip instead of Drip. Instead of having fractional stocks, I pool all my dividends together to buy whole stocks. i guess it sucks in that I can’t build all my stocks overtime but the advantage is letting me buy a whole stock instead of .02 of a stock.

On the one hand i can buy better quality stocks without charge but on the other I can build my positions over time even if the process is really slow. I can’t really tell if it’s a good or bad thing

Hi Jack,

That’s cool that Scotrade allows you to pool all your dividends together to buy whole stocks. That’s still better than using your dividends.

This should be the only math taught in high school. If more people understood the power of compunding we’d have a lot more people in better financial situations. The only friend of compunding is time. The more time to compund the greater the effects. Thanks for sharing this elegant equation with us.

Hi DivHut,

The lack of personal finances and investing topics in high school is really embarrassing. Wish there’s more education in these topics.

100% agree Tawcan, preach it! Lovin that quote from Albert Einstein as well, thanks for sharing dude 😀

Ace

Great post, Tawcan!

My broker doesn’t DRIP, but I don’t think I would use it anyway. I’d rather re-invest any dividends in a new or another position. That way it’s easier to balance my portfolio on a regular basis, rather than create one runaway position in an unbalanced portfolio.

Hi No More Waffles,

Thanks. DRIP is a good way to put your portfolio on autopilot. Furthermore, DRIP will make you think twice before you liquidate your positions. I also re-invest dividends in new positions as well. Re-invest dividends works the same way as DRIP just the compound effect might not be as strong. The important thing is to keep re-investing your dividends until you need them. 🙂

Cheers.

Hi No more waffle,

Don’t you pay high transaction fees when reinvesting dividens received?

My brokerage Scottrade doesn’t offer DRIP, but offers something called FRIP which I use. It is similar to synthetic DRIP you mentioned, but not exactly the same.

https://dividendgrowthjourney.wordpress.com/2014/07/11/scottrade-flexible-reinvestment-plan-frip/

Recently I opened sharebuilder account as well, but haven’t decided whether to DRIP or use the dividends for other investments.

Hi Dividend Growth Journey,

FRIP sounds interesting. It’s interesting that you can pool all your dividends and invest them in selected stocks. That’s really neat!

I’m setting up ShareOwner for Baby T so allow regular DRIP. I think this is what you’re doing with Sharebuilder.

Cheers.

I DRIP my Sharebuilder positions, but my other brokerage account doesn’t allow me to DRIP. To make matters more complicated, I have some of the same companies in both accounts, so I am DRIPing some and some I am just receiving the cash in the other. I do reinvest all dividends it just makes the accounting a bit more cumbersome. In any event, I like the DRIP process better.

MDP

Hi MDP,

Too bad that your other broker accounts do not allow DRIP. I’m in the same situation as you that we hold some of the same companies in all of our accounts. I’m trying to add to these positions so we could DRIP.

Cheers.

Absolutely I DRIP! 🙂

I DRIP most of my 30+ stocks, including all CDN banks and ENB.

There are about 10 stocks I cannot DRIP yet, but I’m working on that. I figure a DRIP is a great way to put your portfolio on autopilot.

Mark

Hi Mark,

I’m DRIPing all my CND banks and I’m trying to add to our existing positions so we’re eligible to DRIP in stocks like ENB and SU. DRIP is indeed a good way to put the portfolio on autopilot. 🙂

Cheers.