Summer time in Vancouver typically means temperatures in the mid to high 20s and an extended period of nothing but the sun. The weather in July was exactly like that. We had nothing but sun for the entire month. Unfortunately, it meant many wildfires all over BC and many people were evacuated. I really hope we’d get a few straight days of rain throughout BC in August to help to control these wildfires.

In July we had the luxury to go to Vancouver Island for a four-day camping trip at the beautiful Goldstream Provincial Park. The campground had a sizable playground and a bike park with a pump track and two different bike trails. The playground and bike park kept Baby T1.0 and Baby T2.0 busy so Mrs. T and I were able to relax and read throughout the trip. There were a lot of kids at the campground and naturally both kids made many friends.

We also took the opportunity to check out the new Malahat Skywalk. Malahat SkyWalk is an accessible 600m tree walk through a beautiful arbutus forest leading to a spectacular gentle spiral ramp that takes you up 32m to a sightseeing lookout offering views of Finlayson Arm, Saanich Peninsula, Mount Baker and the distant Coast Mountains.

The view at top of the Skywalk was breathtaking! There was a net at top of the structure and we all tried to walk on it. A few of us even tried to jump on the net.

Our favourite part about the Malahat Skywalk was the slide. The slide was 20 m or 65 ft tall and 50 m or 165 ft long. It took me around 10 seconds to go down the slide which meant a speed of around 18 km per hour or 11 miles per hour.

While at home, we have been extremely busy harvesting produce from our backyard garden. Our garden exploded into a sea of green as you can see from below.

It has been fantastic to eat fresh home-grown produce! Since we couldn’t eat them all, we gave some veggies to neighbours and friends and froze some of them.

We are very grateful for our backyard garden and all the yummy home-grown produce. Best of all, it is nice to show both kids where food comes from.

Dividend Income – July 2021

Back to dividend income update… in July 2021 we received dividend paycheques from the following companies:

- Algonquin Power & Utilities (AQN.TO)

- BCE Inc (BCE.TO)

- Bank of Nova Scotia (BNS.TO)

- CIBC (CM.TO)

- Canadian Natural Resources (CNQ.TO)

- Capital Power Corp (CPX.TO)

- Dream Office REIT (D.UN)

- Dream Industrial REIT (DIR.UN)

- European Residential REIT (ERE.UN)

- Granite REIT (GRT.UN)

- H&R REIT (HR.UN)

- Coca-Cola (KO)

- Rogers Communications (RCI.B)

- RioCan REIT (REI.UN)

- SmartCentre REIT (SRU.UN)

- Telus (T.TO)

- TD (TD.TO)

- TC Energy Corp (TRP.TO)

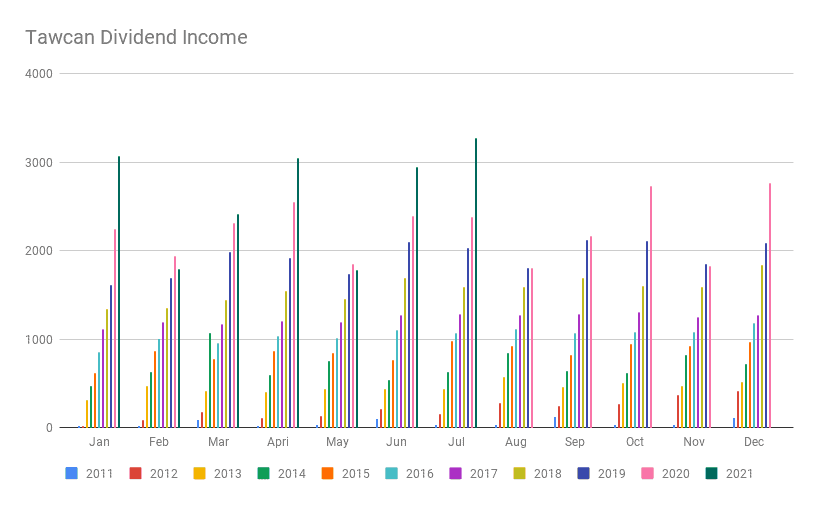

We received a total of 18 dividend paycheques throughout July that added up to $3,270.01, a brand new monthly dividend income record! We not only broke the $3,100 per month milestone but also the $3,200 milestone too! I’m so happy to see that our purchases in the 1H 2021 are finally paying off.

The July dividend income helped us to push our seven-month dividend income average up to $2,619.06 per month. This is absolutely fantastic! Can you believe we are getting paid over $2,600 regardless of what we’re doing? Gotta love our money working hard for us.

Out of the $3,270.01 received $196.28 was in USD and $2,972.95 was in CAD. July was definitely a month that was Canadian dollar heavy in terms of dividend income. Please note, we do not convert USD to CAD when reporting our monthly dividend income. I have been using this approach to avoid fluctuations in our monthly dividend income because of changes in the exchange rate

The top five dividend payers for July were (not in order):

- Algonquin Power & Utilities (AQN.TO)

- TD (TD.TO)

- Bank of Nova Scotia (BNS.TO)

- CIBC (CM.TO)

- TC Energy Corp (TRP.TO)

These five companies accounted for 68.7% of our July dividend income or a total of $2,243.83. Just like June, July dividend income was highly concentrated to these top five companies. For income diversification purposes, it would be a good idea for us to reduce the percentage.

Many curious readers have asked how much our portfolio is. For privacy reasons, we don’t share our portfolio value and the number of shares of each stock we hold. But it shouldn’t be hard to take an educated guess by working backward.

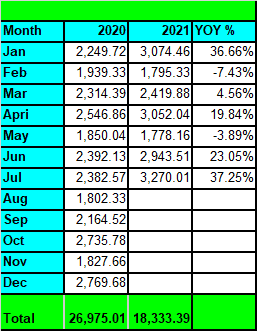

Let’s consider some numbers… last year, we received $26,975.01 in dividend income and this year our goal is to receive over $32,000 dividends.

Using these two numbers, at a 3% dividend yield, that means our portfolio is somewhere between $900k to $1.07M Canadian. At a 4% dividend yield, our portfolio is somewhere between $675k to $800k Canadian.

So our dividend portfolio value is somewhere between $675k to $1.07M. I hope this satisfies the curious readers.

Dividend Growth

Thanks to a record-breaking month, we saw YoY growth of 37.25% compared to July 2020. I’m amazed at this growth. If we look at the 2021 average YoY growth rate, we moved from 13.3% to 17%.

For us to hit our 2021 dividend goal of 32,000, we need to continue to increase our overall dividend growth rate as we need to have more than an 18.6% annual YoY growth rate to hit this very challenging dividend income goal.

Dividend Transactions

Compared to 1H of this year, July was a relatively quiet month for dividend transactions. We didn’t sell any dividend-paying stocks but we made one purchase.

- Purchased 75 shares of Telus (T.O)

While the purchase may be considered a small purchase, we are extremely grateful that our high savings rate allowed us to add about $2,000 worth of Telus shares in July. This purchase added $94.86 to our annual dividend income.

Considering that the COVID-19 Delta variant has created many uncertainties and many companies have pushed out the return to office schedule, I have been debating whether it makes sense to close out our positions in Dream Office REIT and H&R REIT. Both of these REITs have a high concentration in office properties (HR.UN is diversified but has 49% of assets in office spaces). Furthermore, both of these stocks have cut dividends in the past year. I don’t believe either one will see a price recovery any time soon. It may make sense to move on from these two REITs and invest the money elsewhere.

Some dividend-paying stocks I have been monitoring include Apple, Telus, and Brookfield Renewable Corp. With Wealthsimple Trade becoming more and more prominent in the Canadian personal finance and investment space, I am also considering starting a position in Power Corp (POW.TO) to become an owner of Weathsimple. Furthermore, we may continue to add a few shares of the top 13 Canadian dividend stocks.

- Check out my Wealthsimple Trade view

Two other dividend paying stocks I’m keeping a close eye are two US REITs – Royalty Income Corp and Vici Properties. Both REITs have done well throughout the COVID-19 pandemic despite the economic challenges.

Dividend Reinvestment Plan (DRIP)

When it comes to dividend investing, we want to keep everything as simple as possible. Therefore, we always aim to enrol in dividend reinvestment plans whenever we’re eligible. This way, we can drip away and put our holdings on auto-pilot and dollar cost average over time – when the stock price is low, we drip additional shares at a low price, when stock price is high, we either drip fewer shares or no shares at all.

In July we dripped the following shares in our RRSPs, TFSAs, and taxable accounts:

- Algonquin Power (AQN.TO) – 13 shares

- BCE Inc (BCE.TO) – 3 shares

- Bank of Nova Scotia (BNS.TO) – 5 shares

- Canadian Natural Resources (CNQ.TO) – 1 share

- Capital Power (CPX.TO) – 1 share

- European Residential REIT (ERE.UN) – 1 share

- H&R REIT (HR.UN) – 1 share

- Coca-Cola (KO) – 1 share

- Rogers Communications (RCI.B) – 1 share

- SmartCentre REIT (SRU.UN) – 2 share

- Telus (T.TO) – 6 shares

- TD (TD.TO) – 3 shares

- TC Energy (TRP.TO) – 3 shares

Thanks to DRIP, we were able to add 41 shares in July without paying any additional fees. Since TD honours the DRIP discounts that some companies offer, we were able to obtain some shares at slightly discounted prices. In total, $1,704.51 was reinvested or a drip ratio of 52.1%.

Throughout the last year, we have been busy buying AQN.TO to take advantage of the lower price. It was nice to see that we managed to drip 13 shares of AQN.TO in July. It’s also comforting to see that we dripped 6 shares of Telus.

Because CIBC’s share price has increased significantly over the last year, we no longer can drip additional shares. Ideally, I’d like to drip more CM.TO shares each quarter. This may mean that we need to buy more shares to allow us to continue to drip.

Financial Independence Journey Update

Although we can be financially independent now if really wanted to, we choose to delay our financial independence journey. For us, when our dividend income is equal to or greater than our annual expenses, we can then say we’re financially independent. This definition is different than many folks in the financial independence space.

Last year our dividend income covered 55.15% of our annual expenses. This year we’re aiming to hit a FI ratio of 60%. It is an ambitious and challenging goal!

Thanks to a record-breaking month in July, if we were to use the $3,270.01 dividend income, we’d be able to cover the following expenses:

- Property tax

- Housing insurance

- Car insurance

- Groceries

- Internet & cellphone

- Car gas

- Utilities

- Charitable donations

- Dining out

- Household items

In fact, our July dividend income was able to cover 79.2% of our July expenses! While we wouldn’t get to the $360k dividend income per year like Reader B anytime soon, I truly believe that living off dividends (and being financially independent) will be possible in the near future.

Please note, since we’re still in the accumulation phase, we aren’t spending any of our dividends. Instead, we reinvest every single dividend dollar received to take advantage of the power of compounding interest.

Summary

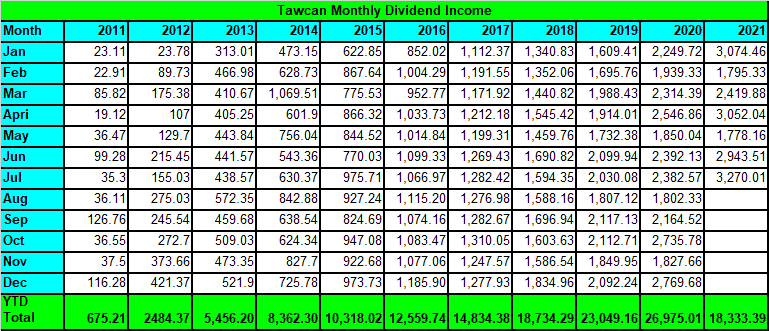

After seven months we have received a total of $18,333.39 in dividend income. I’m very impressed and happy with how much we have increased our dividend income over the last ten years. It’s crazy to think that we are very close to exceeding the annual dividend income from 2018 already!

Since I like to put our dividend income into perspective…

- We have earned $3.60 per hour so far in 2021 ($18,333.39 divided by 24 divided by 212). This is amazing since it means after an eight hour of sleep, we’ve made $28.80!

- An hourly wage equivalent of $14.78 per hour (31 working weeks, eight hours a day, five days a week).

A while ago I used this picture below to reflect how I feel about dividend income. I really love this picture because it is a perfect reflection of how I feel about dividend income.

Gotta love having our money working hard for us so we don’t have to.

Dear readers, how was your July dividend income?

Hi,

If you don’t mind , can you tell me how big your seed is to get this dividend income?

I believe you are the top 5% investor with dividend income. So I want to figure out for me how much I have to prepare for my retirement based on your seed size.

Thanks.

Sorry, what do you mean by how big our seed is? Do you mean the value of our portfolio? If so, I gave a range in this post.

Thanks for replying quickly!

What I meant by seed was the amount you put in(like a principal) not the current portfolio value. I believe you didn’t put the whole amount with your own money. There must be grown portion of it.

Thanks

Hi Conan,

I don’t disclose that information for privacy reasons.

Hi,

In summary section, the comparison of dividends that you posted. I would like to understand what happened in year 2013 ? How come the dividend rose so drastically from 2 to 300 something.

Thanks

Hi Mohanish,

We got serious with dividend investing in 2011 and moved a lot of money between 2011 and 2013.

Time to do a review on National bank free usd and cdn trades account! I’m switching from ibkr and ws to it…. I even wrote to ws and asked when will they have free usd trades and they are still testing.

The National Bank commission free trading looks interesting. Hopefully other banks will follow. I’ll see about doing a review… it’d require me opening an account with them though.

Great read Tawcan! Very impressive results.

Can I ask what your philosophy is on having cash on hand for potential downturns in the market?

I’d love to go all in with 100% of my investable money in dividend growth stocks and could do as I have a wonderful DB pension awaiting my retirement that will easily cover my lifestyle.

Am i being too conservative by having cash that is not paying me anything? Do you believe in a cash reserve?

I could always get a line of credit as an emergency fund but don’t have the need for one now.

I agree with your concern with REITs and recently sold my positions.

Kudos on the chairatible giving…love that!

Thanks GB.

We try to stay fully invested as much as possible. Last March when the market tanked, we moved a bunch money saved to allow us to take advantage of the market. We typically save and invest money each month.

I have been reading your post for over 2 years now, but never left a comment. Just wanted to let you know that from one DIY investor to another, you are inspirational, very helpful, transparent, smart, dedicated and humble. Thank you for unselfishly sharing your financial journey, and congrats on your new dividend income milestone

Thank you Carol for your very kind words. I appreciate it.

I agree. Well said!

Tawcan –

Insanely killer month here, WOW! Keep that income moving up, as well as the average dividend income per month.

Also – looks like you had a great trip, so much fun!

-Lanny

Thanks Lanny.

Thanks for another great write up – very inspiring. Love looking at your garden pics too!

You’re welcome, thank you!

That skywalk and especially the slide look awesome. And I love seeing your garden. I started a small backyard garden this year and while it wasn’t as successful as I’d have liked our oldest daughter still goes and checks on it every day. My next week off I’m hoping to get it cleaned out some to see if we can get a late harvest of some other vegetables. The best part about it though has been that she’s been more willing to try new vegetables since she grew them herself.

Also those dividends are truly fantastic. You guys have done a great job saving and investing and building up that passive income stream.

Congrats on starting a backyard garden this year. We started small many years ago and it has grown significantly. It’s really cool to get the kids involved. 🙂

Growing your own food is especially important during COVID IMO.

You guys are living a self sustaining lifestyle!!!

I remember I told my parents one day, I want to grow my own vegetables, my own chickens, cows, pigs, and live a self sustaining lifestyle. My friends called it an out there idea, haha.

Maybe I will give up that dream but I can only hope!

It’s Mrs. T’s dream to move to a farm and have our own chickens, cows, and pigs. Not something easy to do around Metro Vancouver, given the expensive real estate. 🙂

Excellent work my friend 🙂

Mark

Thanks Mark, appreciate it.

Solid dividend growth there Bob! Pretty soon you’ll start to hit the law of large numbers (like me).

That’s really when dividend growth rates (not savings rate) really start to matter.

Love all those garden pictures too! Thanks for sharing!

Yup, getting harder and harder to avoid the law of large numbers. 😐

Nice vegetables in backyard. I got are few tomatoes and Mint leaves. Love to visit malahatskywalk.

If july is like this ,september must be awesome

Thank you. I assume you mean October. Yup, hopefully October dividend income will break another record.

Hi Bob,

Just a general question. When the portfolio value reaches above six figures $100 K + and dividends are few thousands of dollars. In this scenario is it possible to grow the portfolio simply by reinvesting the dividends and adding no capital at all? Just curious to know how it works because for smaller portfolios the issue is it requires more and more capital injection to see it grow to a significant level.

Hi Sridhar,

As your dividend income gets larger and larger, you run into the law of big numbers. It becomes harder and harder to grow dividends simply by investing new cash. Therefore you need to rely more and more on organic growth, either drip or dividend raises.

Congrats on a record breaking month! Great July in more ways then one. That skywalk and slide looks awesome! That is a huge cabbage too, lol. Keep up the great work! 🙂

Thank you My Dividend Dynasty. The skywalk was a lot of fun for sure.

How do you drip automatically . I do it through the royal bank and it’s whole shares thanks

We drip by signing up synthetic drip with Questrade and TD. It’s whole shares rather than fractional shares. Currently no Canadian brokers support full drip, unless you go with a transfer agent.

I’m with Questrade and turned off my drip because I would like to be selective with what I buy (currently overweight ENB, would rather buy other stocks with my divs)

I also own other companies with good drip plans, PPL has a 5% discount on its drip. Do you think it’s worth the hassle of setting up with a new brokerage for companies with a drip?

Makes sense if you want to be more selective with what you buy.

For me it’s not worth the hassle to switch just to get the drip discount. However, seeing how National Bank has removed trading fees, if other brokers follow, it will be interesting to see how Questrade reacts. Either way, this could be a big win for us DIY investors.

Great pic of you holding the massive cabbage.

Congrats on the July div. income record.

Thank you for helping many people reach their financial goals; you ought to get a ‘Teacher of the Year’ award!

You’re very welcome Pierre.