Can you believe it’s already 2018? What happened to 2017? For some reason, 2017 just zoomed by for me. In many ways, it felt like it was only a few days ago that Mrs. T, Baby T1.0, and Baby T2.0, and I were just in Denmark, celebrating the start of 2017.

For this holiday season, I decided to take 3 days off work (27, 28, and 29) to allow me to have a total of 11 days off. For the most part, I relaxed, enjoy good food, and spent time with the family (playing with kids is an exhausting activity ha!). To maximize the time off, I decided to take a short 2 week break from blogging completely. It felt great to have a small break and tackle 2018 with a fresh set of mind. I am quite excited about 2018 as I have a number of exciting topics in mind that I want to explore.

Like 2016, 2017 was yet another great year for us financially. We successfully maximized TFSA’s and RRSP’s, as well as maximized both kids’ RESP accounts. On top of that, our net worth continued to grow steadily.

Anyway, without further ado, let’s find out our December 2017 dividend income.

December Dividend Income

In December 2017 we received dividend income from the following companies:

- Pure Industrial REIT (AAR.UN)

- Brookfield Renewable (BEP.UN)

- BP (BP)

- Corus Entertainment (CJR.B)

- Canadian National Railway (CNR.TO)

- Costco (COST)

- ConocoPhillips (COP)

- Chevron (CVX)

- Canadian Tire (CTC.A)

- Dream Office REIT (D.UN)

- Dream Global REIT (DRG.UN)

- Dream Industrial REIT (DIR.UN)

- Enbridge (ENG.TO)

- Enbridge Income Trust (ENF.TO)

- Evertz Technologies (ET.TO)

- Fortis (FTS.TO)

- Hydro One (H.TO)

- H&R REIT (HR.UN)

- High Liner Foods (HLF.TO)

- Intact Financial (IFC.TO)

- Intel (INTC)

- Inter Pipeline (IPL.TO)

- Johnson & Johnson (JNJ)

- KEG Income Trust (KEG.UN)

- Coca-Cola (KO)

- McDonald’s (MCD)

- Manulife Financial (MFC.TO)

- Magna International (MG.TO)

- Prairiesky Royalty (PSK.TO)

- Qualcomm (QCOM)

- RioCan (REI.UN)

- Saputo (SAP.TO)

- Starbucks (SBUX)

- Smart REIT (SRU.UN)

- Suncor (SU.TO)

- Target (TGT)

- Unilever plc (UL)

- Visa (V)

- WestJet (WJA.TO)

- Waste Management (WM)

- Exco Technologies (XTC.TO)

Wow! We received a total of 40 pay cheques in December 2017. That’s simply amazing! Talk about income diversification!

In total, we received $1,277.93 in dividend income for December 2017. I was a bit disappointed that we didn’t manage to cross the $1,300 mark (we only managed to cross this mark once in 2017). This was mostly due to a number of stocks like the Vanguard Canadian All Cap ETF, the Vanguard All-World Ex Canada All Cap ETF, Ventas, Was-Mart, and MCAN Mortgage Corp paying out their dividend payments in January instead of December. Having said that $1,277.93 is still very good income for doing absolutely nothing at all.

Out of the $1,277.93 dividend income that we received in December, $406.75 was in USD and $871.18 was in CAD. This is about a 30-70 split between dividends received in USD and CAD.

Please note, we use a 1 to 1 currency rate approach. Therefore, we do not convert dividends received in USD to CAD. We are ignoring exchange rate to keep the math simple. This is our way to avoid fluctuations in dividend income over time due to changes in the exchange rate.

The top 5 dividend payout in December 2017 were Suncor, Manulife Financial, Coca-Cola, Intact Financial, Enbridge. The top 5 payout accounted for 32.67% or $417.47 of our December dividend income.

Dividend Income Breakdown

We hold our dividend stocks in taxable accounts, RRSPs, and TFSAs. Every year, we maximize tax-advantage accounts first before investing in taxable accounts.

We do this so we can be as tax efficient as possible. Why pay extra taxes when we can avoid them by utilizing these tax-advantage accounts? It seems like a no brainer to me. This is why I am always shocked to hear people who are investing using taxable accounts when they have tons of RRSP and/or TFSA contribution rooms left.

For December dividend income, the breakdown across the different accounts were:

- Taxable: $336.37 or 26.32%

- RRSPs: $534.56 or 41.83%

- TFSAs: $407.00 or 31.85%

The 2018 TFSA contribution limit is $5,500 per person. On January 1st, we transferred $11,000 into our TFSA’s. Hopefully the stock market will experience some pullback in the next few weeks to allow us to purchase dividend stocks at lower prices.

Now we have maximized our TFSA’s, the next goal is to maximize our RRSP’s before putting money in our taxable accounts. Being tax efficient with investments can be a pretty simple process.

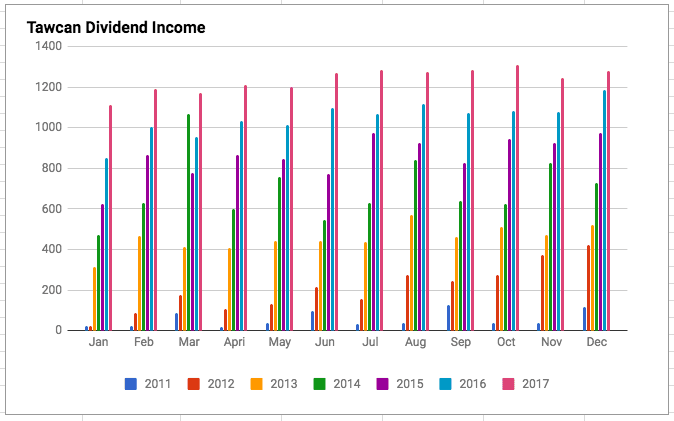

Dividend Growth

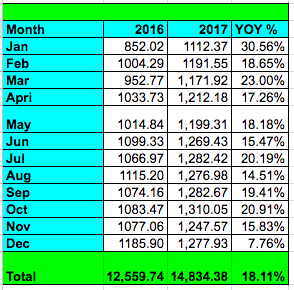

Compared to December 2016, we saw a YOY growth of 7.76%. This was the lowest YOY growth of 2017. This can be explained though, last December we received an abnormally high amount of dividend income due to the special dividend payout from Evertz Technologies.

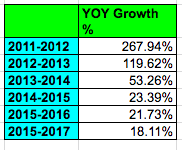

Overall, comparing 2016 and 2017 we saw a respectable YOY growth of 18.11%. This is a pretty solid number considering our 4 digit monthly dividend income level. If you take a look at the historical YOY growth over the last 6 years, it is clear that our YOY growth matrix has been dropping slightly the last 3 years.

This is unavoidable and is a reality that every single dividend growth investor will face eventually.

Why?

Imagine receiving only $20 per month in dividend income, or $240 for the year. A 100% YOY increase means a future annual dividend income of $480, or $40 per month. At a 3% dividend yield, only $8,000 additional capital is needed to see 100% YOY increase.

Now imagine a monthly dividend income of $1,000, or $12,000 for the year.

A 5% YOY increase in annual dividend income means an additional $20,000 is needed at a 3% dividend yield.

A 10% YOY increase in annual dividend income means an additional $40,000 is needed at a 3% dividend yield.

A 20% YOY increase in annual dividend income means an additional $80,000 is needed at a 3% dividend yield.

Finally, a 50% YOY increase in annual dividend income means an additional $200,000 is needed at a 3% dividend yield.

This is a simplified example as we are ignoring any dividend income increases from organic dividend growth and dividend reinvestment plan (DRIP). But the message is clear, it takes a significant large sum of fresh capital to sustain a high dividend growth rate once your dividend income reaches a significant level. Unless you are making high 6 figure salary or 7 figure salary at your job, I believe it is extremely challenging to save and invest $200,000 or more each year. The more dividend income you receive, the more fresh capital is needed to grow future dividend income.

Here’s another example. Imagine you are receiving $4,000 in dividend income per month, or $48,000 per year.

A 5% YOY increase means an additional $80,000 is needed at 3% dividend yield.

If you aim for a 10% YOY increase that means an additional $160,000 is needed at a 3% dividend yield.

Conclusion? High YOY growth in dividend income is extremely hard to sustain once your monthly dividend income is in the 4 digit figures. You are climbing a very steep mountain at this stage of your investment life cycle.

Dividend Increases

In December a number of stocks that we own in our portfolio announced dividend increase:

- Bank of Montreal raised its dividend by 3.33% to $0.93 per share.

- Ventas raised its dividend by 1.94% to $0.79 per share.

- Waste Management raised its dividend by 9.41% to $0.465 per share.

- AT&T raised its dividend by 2.04% to $0.50 per share.

With these announcements, our annual dividend income has increased by $27.44.

This is not a lot of increase but I will take a dividend increase over no increase at all.

Dividend Stock Transaction

We didn’t make any dividend stock transaction in December at all. We expect to go on a major shopping spree this month in January. Some of the stocks we have in mind include:

- Enbridge

- Smart REIT

- BCE

- Algonquin Power

- Vanguard Canadian All Cap ETF

- Vanguard All-World Ex Canada All Cap ETF

- Shaw Communications

- Exco Technologies

- Fortis

- Metro

- Enbridge Income Fund

As mentioned, I am hoping for some market pullback in January so we can purchase shares at cheaper prices.

Conclusion and Moving Forward

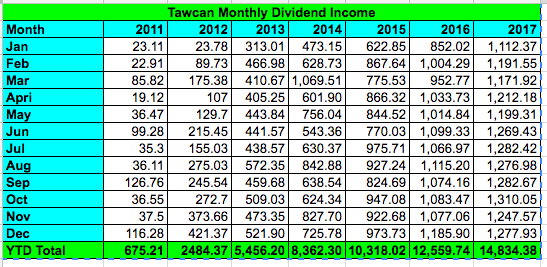

In 2017 we received a total of $14,834.38 in dividend income. This was an increase of 18.11% compared to 2016 annual dividend income of $12,559.74. This a large sum of income for doing absolutely nothing at all. All we had to do was save money and use that money to purchase dividend growth stocks. It’s a simple process that we plan to repeat for the foreseeable future.

Our dividend goal for 2017 was $15,000. This meant we missed the goal by $165.62 or 1.1%. We were so darn close! We did encounter a few dividend freezes or cuts throughout 2017 and as a result, sold some of these stocks. If these freezes or cuts didn’t happen, I had no doubt that we would have crashed this challenging goal.

To put the dividend income into perspective. At $40 per hour wage, or $83,200 annual salary, it means our dividend income saved us 370.86 hours, or 9.27 weeks of work. It basically meant we didn’t have to work the entire month of January and February in 2017! How cool is that?

Based on our financial independence assumptions, the passive income we need to be financially independence is $38,640 per year. Therefore, we are 38.4% of the way to this target number. We will compare our annual passive income with our actual 2017 expenses in another post.

For 2018, Mrs. T and I have not set a dividend income goal yet. At first I thought $18,000 would be a great milestone to aim for, or a 21.34% YOY growth. However, I don’t want to set up an ambitious goal only to force us to purchase higher yield dividend stocks to accomplish the goal. We are in this for the long run and organic dividend growth is extremely important. Therefore, it is important to have a mix of high yield low growth and low yield high growth dividend stocks in our portfolio.

As mentioned earlier, a high YOY growth percentage is getting harder to achieve/maintain. Perhaps it is not realistic to set a goal that will involve more than 20% YOY growth. With these things in mind, I will not set a 2018 dividend income goal and see how things unfold for us this year.

One thing I have been considering is utilizing options on top of collecting dividend income. Doing covered calls on dividend stocks that we already own can perhaps increase our overall passive income. This is an area I plan to learn more in 2018.

Dear readers, how was your December dividend income? How was your overall 2017 dividend income?

Hi Tawcan,

I have currently already contributed the full amount to my TFSA for the year. I am interested in buying some Canadian dividend paying stocks and starting to build a passive dividend income portfolio. Would it be better to buy these new stocks in a non registered account and take advantage of the dividend tax credit or hold them in my RRSP since I have not reached the yearly limit for that account. Thanks for the advice.

Hi Tom,

That’s a tough question to answer without knowing your situation. Generally speaking I think holding DGI stocks in both RRSP and TFSA is a good idea.

Hello Tawcan,

I have been an avid reader of your blog for sometime.

I have around 260000 CDN to invest.

I am not sure that I will be retiring in Canada so Investing in RRSP would not be worth it

I was thinking of the following:

In taxable account: (total 200 000 CDN)

30% VUN (US all cap)

30% VIU (all world ex North America)

40% VSB (short term bond)

In my TSFA (I will max it out)

Individual Canadian stocks one Canadian REIT ETF as well as an emerging market ETF market listed on TSX.

I will be re balancing once year my taxable account

Would appreciate you input.

Thank you and regards

Hi Ben,

Is there reason you’re not investing in Canadian market for your taxable account? Not sure how old you are but 40% in bond seems pretty high.

Hello Tawcan,

I am 42 years old with nopension plan this is why my allocation to bonds is pretty high.

On the other hand I will stick with this percentage and have no plans to go higher than that.

In regards to Canadian stocks I will be using My TFSA to buy individual stocks.

I will split as follows.

The big three (TD, BNS, RY)

Energy (ENB, SU)

Telecom (BCE)

REIT (HR)

I do not feel that using an ETF such as VCN for canadian stocks is worth it….

Would it be better to use the taxable account to buy Canadian stocks…

Regads,

Ben

Hi Ben,

I think all of these individual stocks that you picked are pretty solid, but you need to determine if their evaluations are OK for you to pull the buy trigger.

Impressive and very well done.

As you know, we hit $15,150 this past year in a few of our accounts. I hope to hit $16,500 by the end of 2018. I hope with our TFSA contributions we’ll be close to $15,700 by the end of January 2018.

Consistently earning over $1,200 per month is great and that will likely double for you if you keep investing at the rate you are for the next 5 years.

All the best for 2018 and stay in touch.

Mark

Hi Mark,

Hopefully one day we’ll be able to catch you, especially considering you aren’t counting your RRSP dividend income. 😉

So you didn’t cross $1300… you still managed a very respectable sum for the month of December. Congrats! Overall it looks like 2017 was a great year as you managed a double digit year over year gain. Keep it going strong in 2018. Look forward to following your journey.

Yes still a very respectable sum for the month of December, just wanted to challenge ourselves, that’s all.

A really informative and interesting article Tawcan. Thanks for putting so much effort into it 🙂 You make a great point about the dividend growth rate slowing down as a %, however I think it’s important to remember that in DOLLAR terms it’s increasing at a faster rate. You get paid in $s not %s, so think of it that way 😀 I compare both statistics on my blog, as small as the $ amount is (and large the % is).

Anyway, you’ve done an amazing job this year. I remember seeing you get over $1,000 mark each month and now you’re over $1,200. Truly fantastic job, well done 🙂

Mr DDU

Hi Mr. DDU,

Glad that you enjoyed the update. Yes in dollar terms it’s increasing at a faster ate, that’s an important point to remember. 🙂

Tawcan,

Where do I start. There are so many amazing things mentioned in this article haha Great results for December, great YOY increase, and a great foundation has been built for many years to come. You’re crushing it and I cannot wait to see what is next. I”m glad you also took some time away to refresh your mind. I’m sure you and your family loved the focused time together away from the screen and your regular job. It is something I need to be better about myself.

Happy New Year and I cannot wit to see what 2018 has in store for you.

Bert

Hi Bert,

Thank you. You and Lanny are doing well when it comes to dividend income too! Keep up the good work.

Very nice report! You’re numbers are killing it! Good job maximizing your TFSAs and RRSPs right of the bat. I will max out my TFSA by the end of this year. Looking forward to your purchases in January! You should hit 1.3K in dividends in January 2018, right?

Thank you Dividend Income Stocks. Maximizing TFSAs and RRSPs is something that we do every single year. Great job on max out your TFSA by end of this year. Yes, hopefully we’ll hit 1.3k in Jan in Jan.

You are making some really good progress Bob! Despite some dividend stalls/cuts, you still came in very close to target, that means you are doing something right. Still not considering selling your Vancouver property, reinvest and move to a lower cost of living area and potentially be FI?

Thanks, Team CF. Funny you brought up about selling the property. That’s something I’ll talk about on Monday’s post

Even though you didn’t hit your goal of $1,300+ for Dec, at least you hit it once through the year! That’s still a boat of cash. Thanks for the update, Tawcan and happy new year! 🙂

Thank you Dividend Reaper and happy new year to you too!

Congrats on a great month and finish to the year. Very impressive.

Question please: you referenced above some Vanguard holdings pay out their dividends in January instead of December – what is the scheduled frequency of distributions for these holdings?

Excerpt: “This was mostly due to a number of stocks like the Vanguard Canadian All Cap ETF, the Vanguard All-World Ex Canada All Cap ETF, Ventas, Was-Mart, and MCAN Mortgage Corp paying out their dividend payments in January instead of December.”

Every Vanguard fund I’ve reviewed (although I haven’t done yet for ETFs) seems to have the following schedule:

– If annually, in Dec.

– If semi-annually, in Jun and Dec

– If quarterly, in Mar, Jun, Sep, Dec

I’m really interested to explore “off-month” payers that aren’t monthly, but I haven’t seen any within the Vanguard offerings until this post.

I’d appreciate any insight! Thanks.

Hi Mike,

Thank you. Good question. When I look at the distribution history for VCN I see the following:

Jan 4, 2016 payment date

Mar 23, 2016 payment date

June 22, 2016 payment date

Sept 21, 2016 payment date

Jan 8, 2017 payment date

Mar 30, 2017 payment date

June 29, 2017 payment date

Sept 27, 2017 payment date

So it’s not exactly every quarter for some reason.

You knocked it out of the park even if you did only hit 1300 once. I’m sure this year you will hit it a few times and get close to 18,000 even if you set the bar lower. I agree you don’t want to set the bar to high then hit unsustainable high yields to hit that. Good job keep it up

Thank you Doug. My focus this year is continue adding more shares to stocks that we already own. 🙂

I spent so much time getting ready for 2018 with all our tax uncertainty that I can’t believe it’s actually here now!

Thanks for sharing so much detail. As I work on building our portfolio, I need a lot more information and examples of how these work for other people so I can decide what may work best for us.

Dividend Growth Investing isn’t for everyone. Index ETF investing is definitely something you should look into if you’re just starting out.

Some people have big months at the end of the quarter, but in your case EVERY SINGLE MONTH IS A BIG PAYMENT!!!

You are absolutely crushing it. Don’t worry about the YOY% decreasing. In this case I think it is a good problem to have =P.

These numbers are very motivating! Back to the grind!

-MH

Thank you Money Hungry. Glad to have motivated you. 🙂

More than $1,000 on a monthly basis is a pretty impressive record for a year. Like another poster noted, with the FX rate, you probably beat your goal in all actuality. Congrats. Onward and upward in 2018!

Thank you Chris. Yup with the exchange rate we definitely beat our goal.

Nice work last year Bob. The YOY growth of 18% is excellent, considering it bought you 2 months off work and it’s off a very decent base. My December total was $102.14AUD and for 2017 $351.19AUD. There was a special dividend in there but I still anticipate being able to grow the income stream in 2018.

That’s pretty awesome dividend income for Dec and 2017. It takes time to build up your portfolio so don’t get discouraged when comparing to our dividend income.

Great month Tawcan! Nearly $15,000 for the year in passive income is amazing! Love the YOY growth as well. Keep up the great work! It is inspiring! 🙂

Hi My Dividend Dynasty,

Thank you. The YOY growth was pretty impressive when we consider how much dividend income we’re receiving already. Would have liked to hit the 20% mark. Oh well.

Wow 18% YoY increase. Well done you had a great year! All the best for 2018.

Thanks Steve. 🙂

Man awesome stuff Tawcan. Over $14k for the year and an 18% YoY increase. That’s big stuff and I love seeing the hours worked/saved comparison. 9.27 weeks free sounds awesome. All the best in 2018!

Hi JC,

Thank you. I also like seeing the hours worked/saved comparison. Hopefully we’ll get to 12 or more weeks for this year.

Welcome back. Dam man. Nice work. 18% growth on that income is fantastic! No need to justify that… haha. All the best in 2018! Lets see where you put that cash to work

Cheers

Thanks Passivecandianincome. 🙂

Great job on the dividend earnings. The 18% annual growth rate is quite impressive. I think if you account for USD/CAD exchange rate then you definitely met your $15,000 goal for the year. Yay. 🙂 My medium term goal is to make $23,000 in annual dividend and interest income.

Thanks Liquid. Yea we’d be over $15k if we convert USD dividend income into CAD but I feel that would inflate our numbers somehow.

$23k per year in passive income would be pretty awesome. 🙂

Looks like a great way to ring out the year, Bob. Congrats on the dividend income and all the best for 2018.

cheers

R2R

Thanks R2R. Wish 2018 will be a great one for you too.

Wow, what a great year! I am very impressed. I am new to the blog, I have a lot to catch up on your journey!

I am relatively new to the game, so starting from the bottom. Funny how when you are really interested in something, you can read a book in a day! Normally takes me 3 weeks!

Haha I know how that feels, I was like that not so long ago. 🙂

Nice 2017 Tawcan! 18% YOY dividend growth is pretty incredible!

I just barely achieved our goal of 10% growth this year, reaching $53k in dividends. It definitely gets harder with the larger numbers!

I’d be pretty happy with 10% growth if we have $50k in dividend income. 🙂 It gets harder and harder with larger numbers for sure.

The 18% y/y increase is still awesome even if it the growth rate starts to slow down, the dollars are still solid! Nice in depth analysis and congrats on the continued growth.

Yup 18% YOY is still pretty good when we look at the dollar amount. Very happy with the performance.

Wow Tawcan. What an impressive group of companies and awesome stream of passive income. My December was great as well. I had a couple mutual funds with dividend payments that were greater than I expected. My dividend growth stocks were steady and paid as expected. Happy New Year. Good luck in 2018 and I look forward to reading all about it! Tom

Thanks Tom. That’s awesome you had a great December dividend income. 🙂

Welcome back from your break! Over 14K in dividend income, that’s so great, keep up the good work:)

I like how you put it into hours of work, it always makes it so much more real.

And you already transferred your $5,500 over to your TFSA, right on top of your game. That is on my list to do… at some point this week.

Happy New Year!

Thank you Caroline. I like putting the money into hours of work too because that gives me a good quantitative view.

I was going to say the same thing!

Pretty soon it will be 3 months off…and then 4…and then 5….

Congrats!

Thank you Nick. You totally read my mind!