Happy New Year everyone! I hope everyone had a fantastic 2023 and enjoyed the holidays.

Some readers have been asking about our portfolio performance so I thought I’d provide some context and 100% transparency.

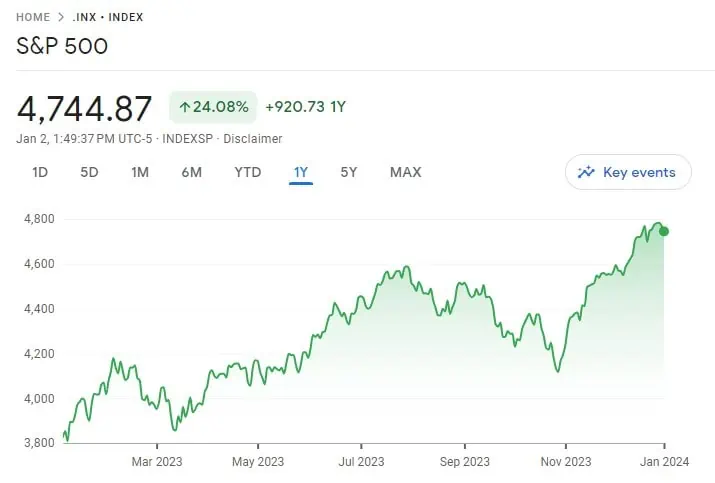

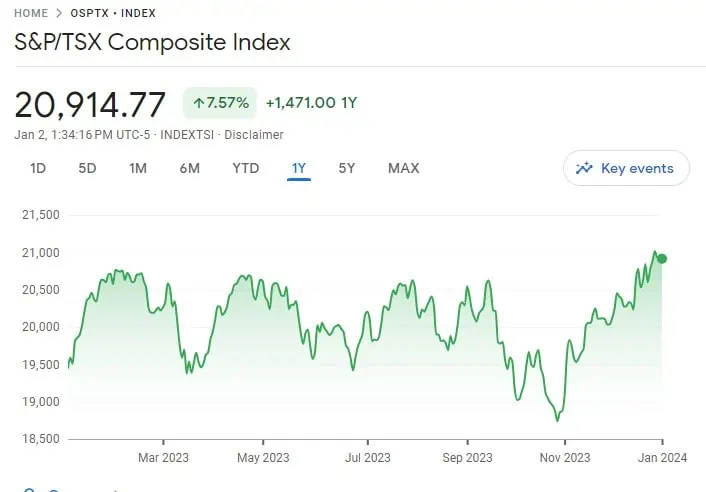

In 2023, our portfolio returned +10.48% excluding contributions. In comparison, the TSX had a +7.79% return and the S&P 500 had a +24.73% return.

A table comparison for those with a curious mind:

| Portfolio return excluding contributions | TSX return | S&P 500 return | |

| 2012 | +8.67% | +4.0% | +13.41% |

| 2013 | +33.04% | +9.55% | +29.6% |

| 2014 | +24.08% | +7.42% | +11.39% |

| 2015 | -5.97% | -11.09% | -0.73% |

| 2016 | +19.62% | +17.51% | +9.54% |

| 2017 | +12.33% | +6.03% | +19.42% |

| 2018 | -2.38% | -11.64% | -6.24% |

| 2019 | +11.32% | +19.13% | +28.88% |

| 2020 | +3.2% | +2.17% | +16.26% |

| 2021 | +32.8% | +21.74% | +26.89% |

| 2022 | -5.4% | -8.66% | -19.44% |

| 2023 | +10.48% | +7.79% | +24.73% |

| Averages | +12.80% | +5.33% | +12.81% |

Somehow, we have beaten the TSX a few times since 2012, mostly because our portfolio consisted of a mix of Canadian dividend stocks, US dividend stocks, and international stocks via XAW. Holding US stocks in USD also meant we benefited when USD was strong against CAD. Not surprisingly though, we weren’t able to beat the S&P 500 return every year given our portfolio composition.

But historical returns don’t mean that we’ll continue to beat the index. Remember the old financial dictum – past performance does not indicate future performance!

Our return in 2023 would have been higher if it didn’t get dragged down by the likes of AQN (we closed the position late in the year. Hindsight being 20/20 we should have closed the position earlier in the year), the Canadian telecoms, TC Energy Corp, and Enbridge.

On the flip side, the likes of Costco, Brookfield Asset Management, and Manulife had a great year.

You win some and you lose some right?

In other words, some years we beat the indices and some years we trailed behind it. That is the nature of investing in individual stocks instead of investing in index ETFs and tracking the market performance. Am I disappointed for not outperforming the market consistently? Should we just invest in index ETFs and track the market performance?

While index ETFs are excellent for most investors, we chose to go with a combination of individual stocks and an index ETF because we feel receiving dividend income consistently is a huge mental boost and helps us from emotional selling.

Some people may argue that dividends aren’t free money. It’s like having $100 in your right pocket, moving $5 to your left pocket, and leaving $95 in your right pocket. In the end, whether it’s index investing or dividend investing, you’d end up with about the same amount of money.

I agree with this statement.

One shouldn’t just count dividends. Rather, total return matters!

However, I truly believe the key benefit of dividend investing is the psychological boost that many people don’t talk enough about. When you’re getting a consistent dividend income, there’s a lower chance that you would sell shares when there’s a sudden drop in the market.

This was certainly the case back in March 2020 when we saw a portfolio value drop of around $250,000. Thanks to the regular monthly dividend income, we didn’t feel the need to sell anything. Instead, we loaded up on discounted stocks.

It was a similar story in 2015 and 2018, or whenever the TSX and/or S&P 500 went for a significant correction. We saw our portfolio value drop during that time but we didn’t feel the need to sell anything. We continued to earn money, save money, and invest money regularly and focus on the long term. Receiving regular monthly dividend income calmed our nerves and prevented us from making any knee-jerk reactions.

Yes, some research studies have concluded that indexing is better than dividend investing, but some studies showed the opposite results. For me, these studies are simply academic research exercises and are based purely on numbers alone. What they fail to include are the psychological and mental aspects of investing. On paper and mathematically, it’s easy to say that when the market tanks by 30% or more, you should be investing more money.

In reality, it is extremely difficult to separate emotions from investing, especially when it’s your hard-earned money we’re talking about here!

As a result, I have learned over the years to not pay too much attention to the performance of our portfolio. Instead, it is more important to focus on growing our net worth. Fortunately for us, our net worth grew higher than our salaries in 2023, so we were very pleased with this result.

Life-wise, December was relatively relaxed. We spent a couple of days skiing in Whistler (had some blog-related work in Whistler and used the free time to go skiing). Although it was early-season skiing and not as good as what we saw last March, we still had a lot of fun.

I always loved standing in the alpine and looking around the snowy landscapes.

We spent the rest of December getting ready for Christmas and having a lot of hygge. This was the first time that Mrs. T and I didn’t decorate the Christmas tree and left it up to both kids.

Christmas meant we made a lot of treats like chocolate, cookies, and burnt sugar almonds.

Kid 1.0, with some help from Mrs. T, made a HUGE gingerbread house (I meant a castle).

We hosted the family Christmas dinner and had a merry time. Since Mrs. T and I don’t like turkey (we find it too dry), we opted for roasted leg of lamb this year with many different side dishes. Overall we had a festive time over the holidays.

Since we have been focusing more on experiences over the last number of years, the coolest experience that we had in December was checking out The Infinite Experience where we explored inside and outside of the International Space Station via the Quest 2 VR headset. It was our first time immersing ourselves in a 360 VR environment and we had an amazing experience. If you have the chance, I’d highly recommend checking it out.

Dividend Income – December 2023

Alright, back to dividend income.

In December we received dividend income from the following companies:

- Brookfield Asset Management (BAM.TO)

- BlackRock (BLK)

- Brookfield Renewable Corp (BEPC.TO)

- Brookfield Corporation (BN.TO)

- Canadian National Railway (CNR.TO)

- Canadian Tire (CTC.A)

- Enbridge (ENB.TO)

- Fortis (FTS.TO)

- Hydro One (H.TO)

- Granite REIT (GRT.UN)

- Intact Financial (IFC.TO)

- Johnson & Johnson (JNJ)

- Coca-Cola (KO)

- McDonald’s (MCD)

- Manulife Financial (MFC.TO)

- Magna International (MG.TO)

- Qualcomm (QCOM)

- SmartCentres REIT (SRU.UN)

- Suncor (SU.TO)

- Target (TGT)

- Visa (V)

- Waste Management (WM)

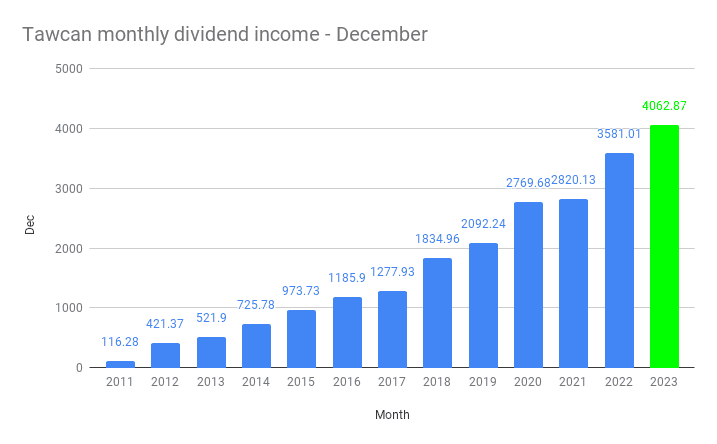

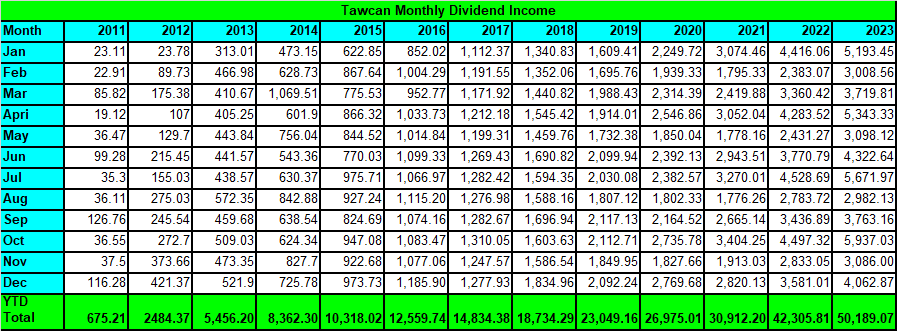

The 22 dividend pay cheques from December added up to $4,062.87. What a fantastic way to wrap up the year with a monthly dividend income exceeding $4,000!

Compared to December 2022 we saw a YoY growth of 13.46%, a very respective number given that we’re facing the law of big numbers.

Out of the $4,062.87 received, $609.02 was in USD and $3,453.85 was in CAD. Please note that we do not convert USD to CAD when reporting our dividend income. We wanted to keep the math simple and avoid any fluctuations in our monthly dividend income due to exchange rate volatility.

I don’t know about you, but I always find it a bit weird that some companies have irregular dividend payment schedules. Instead of paying dividends every three months, some companies decide to move things around. For example, instead of a January-April-July-October dividend payment schedule, Coca-Cola’s payment schedule is April-July-October-December.

Oddly enough, Coca-Cola’s key competitor, Pepsi also has an irregular dividend payment schedule of January-March-June-September. Walmart also has an irregular dividend payment schedule as well – January-April-May-September.

I haven’t been able to find the reasons behind these irregular dividend payment schedules. If I had to guess I’d wildly speculate that it was due to tax/fiscal year reasons. Does anyone know?

Dividend Hikes

When we do live off dividends, we would like our dividend income to continue to grow and keep up with inflation. This is why dividend hikes are so important as we get closer to financial independence.

Like November, December was a solid month when it came to dividend hikes.

- Waste Management (WM) raised its dividend payout by 7.1% to $0.75 per share

- Bank of Montreal (BMO.TO) raised its dividend payout by 3% to $1.51 per share

- National Bank (NA.TO) raised its dividend payout by 4% to $1.06 per share

In addition to the dividend hikes, Costco also declared a $15 per share special dividend, payable on January 12, 2024.

Not counting the Costco special dividend, we will see our forward annual dividend income increase by $171.24. At a 4% dividend yield, that’s equivalent to investing $4,281 in new capital.

We were overjoyed about Costco’s special dividend because that would result in a nice one-time jump in this year’s dividend income. On the flip side, it could mean that our dividend income year-over-year growth in 2025 may not be as high. But we’ll worry about that when we get there…

Dividend Reinvestment Plans (DRIP)

In December we dripped the following shares automatically by signing up dividend reinvestment plans with our discount brokers, TD Waterhouse and Questrade.

- 1 share of Brookfield Asset Management

- 3 shares of Brookfield Renewable Energy Corp

- 41 shares of Enbridge

- 3 shares of Fortis

- 1 share of Coca-Cola

- 12 shares of Manulife Financial

- 6 shares of SmartCentres REIT

- 1 share of Suncor

Thanks to DRIP, we added 68 more shares in December. More importantly, dripping allowed us to add $196.48 toward our forward annual dividend income.

Dividend Transactions

Because we knew that XAW’s ex-dividend was late in December with the distribution coming in late January, we decided to nibble a few XAW shares to slightly increase the bi-annual distribution we’d receive.

We added 39 shares of XAW in late December and added roughly $25 toward our forward annual dividend income.

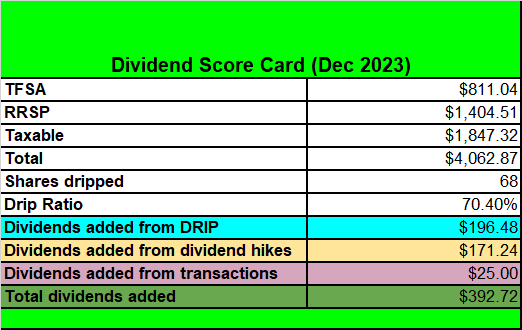

Dividend Scorecard – December 2023

Here’s our dividend scorecard for December:

Overall, a very solid month to wrap up the year.

2023 Dividend Income Review

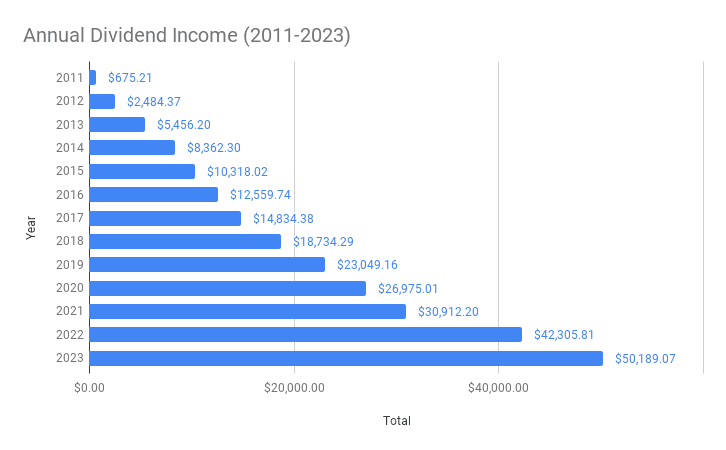

It’s hard to believe how far we’ve come in terms of dividend income. In mid-2007, I purchased ING stock (now called Intact Financial) without putting too much emphasis on dividends. Then in 2011, Mrs. T and I started focusing on building our dividend portfolio and generating dividend income.

Looking back, it’s pretty insane that we went from $54 in annual dividend income in 2007 to over $50,000 16 years later. What’s even more amazing is that we managed to double our dividend income in under four years!

Compared to 2022, we grew our dividend income by 18.63% YoY. Although it was not as big of a jump compared to last year’s performance of 36.86%, we were very grateful for such an increase.

Many readers have been asking how have we grown our dividend income. It comes to these VERY boring steps:

- Increase our income

- Having a relatively high savings rate

- Invest our savings

- Max out TFSA and RRSP every year

- Invest in taxable accounts once we max out TFSA & RRSP

- Reinvest 100% of our dividends

- Enroll in DRIP whenever possible

- Not only buy high yield dividend stocks, but have a handful of lower dividend yield dividend stocks that have high dividend growth

- Avoid any emotional financial decisions

Rinse and repeat. Get in line and stay in line.

In my relatively short DIY investing career, I have seen many investors jumping in and out of different investing strategies. Some even consistently sell 100% of their portfolio and then jump back to the market a few months later. Sometimes they “timed” the market correctly, and ended up with a sizable gain, so they boasted that timing the market is a valid strategy. Sometimes they “timed” the market correctly and got out before the massive market drop. Then they jumped back in when the market was on the way up.

But many failed to see that they simply got lucky.

I mean, would anyone have predicted that the market would hit a high in late February 2020 before it crashed down? Would anyone have predicted with 100% accuracy that the market would bounce back up by late March 2020? How could anyone predict global macro events such as wars, extreme weather, and substantial interest rate hikes???

When the S&P 500 was dropping in February 2023 down to below 3,900 points, would anyone have predicted that the index would start gaining in mid-March and end the year at over 4,700 points? Similarly, the TSX was very volatile throughout 2023. Who would have predicted it’d go for a rally in late October?

I certainly didn’t and that’s precisely why I wouldn’t want to make any sort of future predictions.

Because I know at best, my prediction is only 50% correct.

Timing the market is a fool’s game. Time in the market and continuing to invest throughout time (i.e. dollar cost averaging) is boring but is a sure way to make sure your investment will continue to grow and flourish.

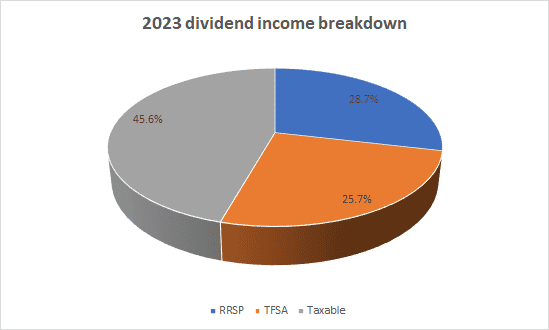

2023 Dividend Income Breakdown

Every year we aim to max out both TFSAs and RRSPs. Once we max out TFSAs and RRSPs, we then invest in non-registered accounts. We invest this way so most of our dividend income is either tax-free (TFSA) or tax-deferred (RRSP). Only a portion of our dividend income is taxed. Dividends in our taxable accounts are split between Mrs. T and me, further reducing our overall taxes.

Our 2023 dividend income breakdown is as follows:

- RRSP: $14,384.61, 28.7%

- TFSA: $12,913.87, 25.7%

- Taxable: $22,890.59, 45.6%

In other words, over half of our 2023 dividend income was either tax-free or tax-deferred.

Our taxable dividend income was split between Mrs. T and I:

- Mrs. T: $8,476.91, 37%

- Tawcan: $14,413.64, 63%

As we get closer to the dream of living off dividends, we anticipate that a higher and higher percentage of our dividend income will be coming from taxable accounts. This is because both TFSA and RRSP have annual limits. Ideally, we would want to leave our TFSAs alone so they can continue to compound tax-free and only utilize dividends from our RRSPs and taxable accounts.

2023 Organic Dividend Growth & DRIP

Moving forward, I believe we will rely more and more on organic dividend growth and DRIP to increase our dividend income.

In 2023 these two pillars added $4,596.13 toward our annual dividend income, an improvement of 20.4% compared to 2022.

| Year | Organic dividend growth | DRIP | Total $ |

| 2022 | $2,367.36 | $1,450.21 | $3,817.57 |

| 2023 | $2,491.14 | $2,104.99 | $4,596.13 |

At a 4% dividend yield, adding $4,596.13 toward our annual dividend income is like adding almost $115,000 in new capital! That is the power of organic dividend growth and DRIP!

Summary & Looking Ahead

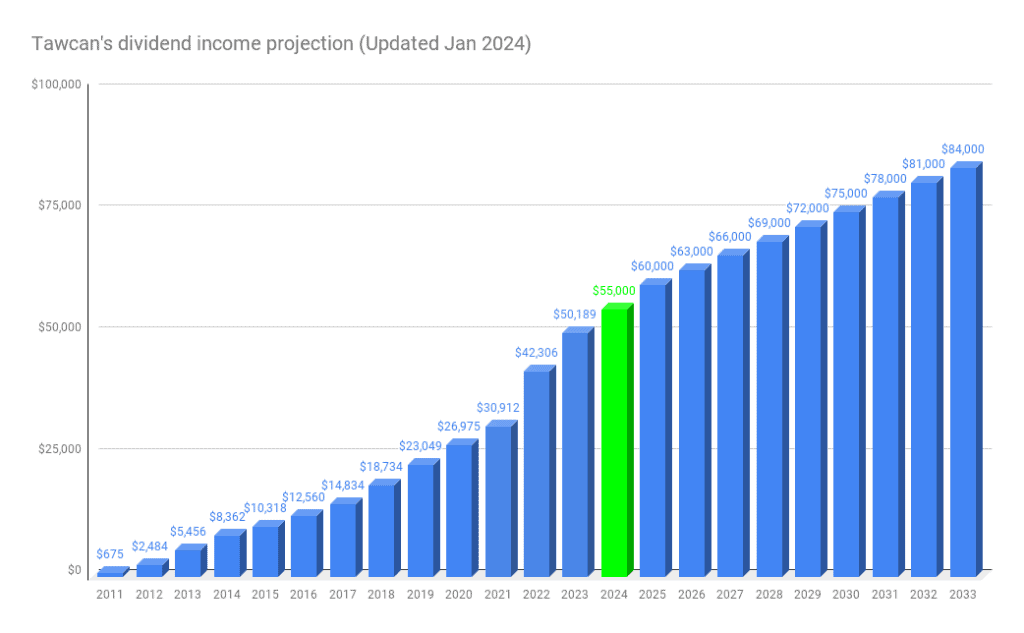

It felt fantastic that we not only accomplished our goal of receiving $49,000 in dividend income in 2023, we exceeded it by 2.4%. The dividend snowball is getting bigger and bigger each year and doing so at an increasingly faster pace.

We continue to feel very blessed and grateful that we’re doing very well financially, hence for providing a helping hand in the community whenever we can.

At $50,189.07, our 2023 dividend income was equivalent to:

- $137.50 per day or $5.73 per hour

- $965.17 per working week or $24.13 per hour

Back in Jan 2022, I projected that our 2023 dividend income would be $41,500 and our 2024 dividend income would be $46,000. So we have exceeded this projection already.

Last year, I projected that our 2024 dividend income would be $55,000. Rather than increasing this amount slightly, I have decided to stick with the $55,000 projection. My reasons?

- Allow us to focus more on the low dividend yield high dividend growth stocks like ATD and Apple. These stocks typically provide higher total returns.

- Prevent us from adding high-yield stocks that potentially have higher risk due to high levels of debt (i.e. AQN, Inter Pipeline, etc).

- Avoid buying certain stocks purely to hit dividend income goal/projection

At the time of writing, I believe there’s a very high chance that we’d exceed the $55k projection. If that were to happen, that’d be fantastic!

All in all, we had a fantastic 2023. We look forward to a great 2024.

Hi Bob, one thing you didn’t mention about the benefits of dividend investing is over long term (multiple decades) that nearly half of the return is coming from dividend return. I started my journey back in 1998 so I had been throught two major market correction: dotcom bust or technology bubble in 2000 ; subprime crisis in 2008/2009. Of course, there were older folks who had more experience than I do like the guy who had been through the black friday of 1987. Today you talked about the magnificent 7 (MSFT, Amzn, meta, goog, nflx, aapl, tsla) and don’t ever forget we had magnificent 4 in 2000 lol (CSCO, MSFT, INTC, QCOM). Only 1 out of the 4 survived to be parts of the new magnificent 7 today so the success rate is only 25%. I bought MSFT at its peak in 2000 at around $95 a share before the split and then it took 16 yrs to be exact (2016) for MSFT to get back to its peak in 2000. Then CSCO, INTC are just about 50% of its peak they reached in 2000. After 24 yrs, you are still half way of being the old magnificent 4. History is mirror and it would repeats itself over and over again. I was just talking to a friend and he asked me the same question why doing all the extra work for owning dividend stocks than index. I said one thing dividend investing is timeless and you don’t need to find next magnificent 10, 15, 20 or whatever that number is!

Hi Dan,

Return – a very good point! Interesting point on how long it took MSFT to get back to its peak.

Fantastic work and results Bob, I’m so proud of you. It was amazing compound rate of return over the years! keep up the good work!

Thank you Dan.

Jef made an RSP comment about getting it out tax efficiently. With higher interest rates a person might be better off paying down more debt and accumulating RRSP room. As your taxable income increases or if you know future bonuses/ promotions are possible having RRSP room might be a better used later.

No simple answer, everyone is a different scenario.

I filled my RRSP since my first job at age 16. I pay a higher amount of taxes now to try and draw that amount down for our estate tax issue later on death.

A true financial planner would put that all in a projection for you. Instead they try sell you another product like insurance etc. I think a good excel geek like Bob will make money with a program some day. Bob is right to have an exit plan. Semi retire(slow down), drawing from registered accounts first.

The majority of pensions are defined contributions and filling up RRSPs turns into a tax trap if you don’t plan it all out.

Yup, everyone’s situation is different. It certainly helps to do some planning and consult with a few specialists to get different opinions.

Incredible growth over the years. Congrats!

Thank you!

Hi Bob,

What a way to begin the new year!

Congrats on hitting the milestone and cheers to the next run upto 100k+ ;).

I love the fact that your focus is not just on dividends but also overall portfolio performance. While I’m on a similar journey on the dividend income side, I have not fully committed to dividend growth only stocks, just yet. Wondering if you analysed your portfolio from that perspective of growth only stocks vs dividend growth players. Also, what that split might be.

I’m currently in almost a 50-30-20 split between growth/high-dividend/dividend-growth stocks. By growth, I mean no divs on stocks.

At what point did you decide to move towards the later – divided growth stock concentration.

Cheers,

Sukal

Hi Sukal,

Thank you! Haven’t done deep analysis on growth only stocks vs dividend growth players. This might be something I need to look into. Thanks for the suggestion.

Hi Bob,

If you are maxing out the RRSP each year, just wondering if the company you work for has it’s own pension plan.

No, I don’t have a pension plan.

Hi Tawcan, great work here! You say you max out RSP’s… Careful here tax man will take a big bite on the contribution and its growth. You will forever be managing how to efficiently melt down the RSP. You may want to look at your projected income and future tax rate. We are retiree’s and maxed RSP’s it is a comfortable feeling having the best egg, but not too long before I pay 30 percent for withdrawals. Now I wish I had specific recommendation such as better to put $ in open accounts so tax is only 50 percent on growth… I have never say down to seriously run the cases… You may want to… 30 percent on withdrawals, ( or 52 percent tax if balances left in there) and potential OAS claw back, can hurt.

Hi Brad,

Yes, need to be careful with RRSP, hence for contributing to spousal RRSP rather than my RRSP. We plan to do some early withdrawals to reduce the RRSP amount to avoid the RRIF mandatory withdrawals later on.

You are an inspiration to us all. Congratulations are in order. You are so right about the psychological boost of a juicy dividend payment!

Thank you very much Pierre.

Hi Bob,

May I ask a question? What is the difference between Organic dividend growth and DRIP? Thank you.

Hi Emily,

Organic dividend growth = companies raising dividend payout. For example, RY increases dividend payout from $1 to $1.10, or a 10% increase.

DRIP = dividend reinvestment plan. Basically when you receive dividends, if the amount is enough to buy 1 full share, the discount broker will DRIP for you without any cost. Wealthsimple Trade now allows fractional DRIP which is an amazing feature.

Hi Bob,

Great Job! I really enjoy seeing this growth in your investments!

As a long term div investor myself, the most true words for this method to really take off are “Time in the Market”. I have found it truly amazing what long term dripping and compounding does to an investment account. As a retired person, the only downside is that I will never get OAS as my income keeps growing and I am far past the threshold now.

I suspect your 2033 estimate will be wayyyy less than what the actual income generated will be.

Thank you very much Dale, I appreciate it.

It’s unfortunate that you will never get OAS but that’s better than having to rely on OAS no?

You are right, an income that is high enough to be above the OAS threshold is MUCH better than relying on using OAS as part of my income. It means the dividend money machine is trouncing inflation by a large margin.

It was the only downside I could think of, and it doesn’t hold much water!

Hi Its not so bad the Feared claw back of Old Age security is not lost, rather it shows up as one of your current year tax contributions. In effect your paying your income tax up front. Your already in a tax bracket where the amount owed will far exceed the old age security tax credit. Might not have clued in until I started doing my own income tax when retired. Hope this helps .

M

It is always nice to reflect back and do analysis. I just turned 65 and I retired 10 years ago. I have twice the investment value as when I retired but have also been pulling from the pot. Managing the portfolio is tasking at times and makes me wonder why wouldn’t a person put more towards the S&P 500 with something like VFV. It performs better than TSX consistently and is simple.

The polictics have changed so much in Canada, we are a country with all the resources but the changes that have been made will stop the investments from so many foreign countries. Each year the restrictions are set to increase. Your point is dead on about your past returns aren’t an indication of the future. Our commodities are being retsrticted, which will change the returns for the future. The fuel tax for example affects every sector, which drives up inflation. In summary, less income from commodities, increased taxation isn’t a place to invest for the future.

Investing only in S&P 500 is a potential strategy but you’d be limited to the US market only. Having said that, most of the companies in the S&P 500 are global companies.

I am inspired by your div/year and growth. I am currently at 22k/yr and hope to get to 1M mid year. I have some growth stocks that could be converted to income. I could easily live off of 50k, but I am just one.

Congrats on $22k per year.

Would it be possible to know how much is invested (total $ value) in each account (TFSA, RRSP, Taxable)? I believe this is an important factor in helping achieve the monthly dividend income. It will also help me determine if this is achievable for my portfolio.

Hi Gianluca,

I don’t disclose the $ amount publicly but you can do a rough estimate by using a 4% yield.