Recently a few readers reached out and asked me about bond ETFs. Since most of these readers are close to retirement or are already retired, they are curious about my thoughts on bonds. In particular, does it make sense to invest in one of the many Canadian bond ETFs?

For us, we are still in the accumulating phase and our investment timeline is quite long, so we currently hold minimal bonds in our investment portfolio. By investing in stable dividend-paying stocks like Fortis and Telus, which we regard as bond equivalents (or as some commentators say, “bond proxies.”).

But even safe stable dividend-paying stocks can face significant volatility, especially when the entire stock market tanks as we’ve seen in recent times. So for some investors, as a way to protect their portfolios, it makes sense to invest in bonds as you get close to retirement.

Let’s take a look at the best Canadian bond ETFs and see which ones Canadians should consider investing in.

What are bonds?

Bonds, also sometimes referred to as fixed income, are a type of loan in which the issuer is obliged to make a fixed amount of payment on a fixed schedule to the bondholder.

In addition to the fixed amount of payment, when the bond matures, the issuer is also obliged to repay the principal of the bond.

Essentially, if you hold the bonds till maturity, you won’t lose any money You will get the fixed interest payments plus the principal.

One important thing to note when it comes to bonds is that there’s an underlying market where bonds are traded like any commodities. In fact, amazingly, the dollar amount traded in bonds far exceeds that of stocks.

Why bonds are tied to interest rates

How much interest the bond pays out is typically determined by the interest rates when the bond is issued. To attract investors, bonds typically have a slight premium over interest rates.

Imagine the latest bonds have a yield of 2% because interest rates are at 1%. If the interest rates were to go up from 1% to 2%, what would happen to newly issued bonds? Well, new bonds would provide a slightly higher yield, so the new bonds may have a 3% yield or higher.

This means the 2% yield bonds aren’t as attractive anymore (i.e. you can get new ones that yield 1% or higher). As a result, if you were to sell the 2% yield bond in the open market, the price of these bonds must decrease to remain attractive and competitive.

In other words, bonds have an inverse relationship to interest rates. Or another way to think about it, bond prices rise when interest rates fall, and they fall when interest rates rise. For some reason, this simple concept confused me a lot when I took ECON 101.

What should investors do given the current low interest rate environment and the Bank of Canada having stated that interest rates will continue to go up? Well, I think investors would want to stick with short term bonds.

Government bonds vs. corporate bonds

If you start doing research on bonds, you’ll quickly find out there are two different types of bonds – government bonds and corporate bonds. What are the differences?

Well, the most important difference between the two is the risk profile. Government bonds are typically safer and have higher credit ratings. Generally speaking, it is harder for countries, provinces/states, and municipalities to go bankrupt and default on the bonds that they have issued.

On the other hand, corporate bonds can be issued by companies ranging from multi-billion institutions to small, highly leveraged corporations. Therefore, corporate bonds are usually riskier than government bonds and are more volatile. To entice investors, corporate bonds usually have higher yields than government bonds.

Why do you buy bond ETFs instead of individual bonds?

Why do you buy bond ETFs instead of individual bonds?

Simplicity.

It can be complicated to buy individual bonds, especially corporate bonds. Furthermore, typically when you buy individual bonds, you’d hold them until they mature because they are harder to sell compared to bond ETFs.

Since bond ETFs are traded on the stock exchanges, it is easier to purchase and sell them. If you use a discount broker that offers commission-free trading, like Questrade or WealthSimple, investing in bond ETFs becomes even simpler and cost-effective.

Best Canadian Bond ETFs to buy today

Given the current low interest rates environment, I believe it is best to stick with short term bonds. For investors looking for a little higher yields, I think it may be wise to have a mix of corporate and government bonds. Here are my top 5 best Canadian bond ETFs to buy today.

- iShares Canadian Hybrid Corporate Bond ETF (XHB)

- BMO Aggregate Bond Index ETF (ZAG)

- Vanguard Canadian Aggregate Bond Index ETF (VAB)

- Vanguard Canadian Short Term Corporate Bond Index ETF (VSC)

- Vanguard Short Term Bond Index ETF (VSB)

Please note that for simplicity sake, I am completely ignoring taxes for this analysis.

| Ticker | Name | Holdings | MER | Yield | Average duration | Average maturity |

| XHB | iShares Canadian Hybrid Corporate Bond ETF | 503 | 0.50% | 4.13% | 5.68 yrs | 8.86 yrs |

| ZAG | BMO Aggregate Bond Index ETF | 1428 | 0.09% | 3.45% | 7.54 yrs | 10.35 years |

| VAB | Vanguard Canadian Aggregate Bond Index ETF | 1137 | 0.09% | 2.75% | 7.6 yrs | 10.4 years |

| VSC | Vanguard Canadian Short Term Corporate Bond Index ETF | 339 | 0.11% | 2.66% | 2.7 yrs | 3.5 years |

| VSB | Vanguard Short Term bond index ETF | 477 | 0.11% | 2.08% | 2.6 yrs | 3.0 years |

Best Canadian Bond ETFs

Here are more details of the five best Canadian bond ETFs that I selected.

iShares Canadian Hybrid Corporate Bond ETF gives Canadian exposure to Canadian corporate bonds, with a maturity of at least one year with a credit rating of BBB or below. I picked this bond ETF because of the slightly higher yield compared to other bond ETFs. XHB has a much higher MER compared to other four bond ETFs on this list but we’ll get into that later.

You may think that I’m trading yield for risk but XHB’s top issues are from the likes of Bell, TransCanada Pipeline (aka TC Energy Corp), Telus, Rogers, Enbridge, Pembina Pipeline, Air Canada, Parkland Corp, etc. Most of these companies (or all of them) are solid companies that are part of the Best Canadian dividend stocks list.

The weighted average maturity of XHB is 8.86 years and the average duration is 7.54 years, so I’d categorize XHB as a medium term bond ETF. One thing to note is that more than 20% of the corporate bonds that XHB holds have a maturity date of 10 years or more.

As I pointed out earlier, while the XHB’s yield is much higher than the rest of the Canadian bond ETFs on my list, investors will pay a little bit higher MER of 0.5%. This is roughly 0.4% higher than the other four bond ETFs I have listed. A 0.4% difference with $10,000 invested is $40 per year, while a yield difference of roughly 1.5% corresponds to a difference of $150 per year. Essentially, you’re trading for a higher MER for a higher yield.

2. BMO Aggregate Bond Index ETF (ZAG)

BMO Aggregate Bond Index ETF invests in a variety of debt securities primarily with a term of maturity greater than one year. The key benefit of ZAG is that the ETF invests in a diversified portfolio of federal, provincial, and corporate bonds. In addition, ZAG is a fund of funds, so the management fees charged are reduced by those accrued in the underlying funds.

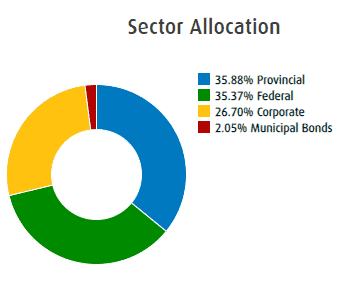

Because ZAG holds a mix of government and corporate bonds, investors get the best of both types of bonds. At the time of writing, ZAG consists of 35.88% provincial bonds, 35.35% federal bonds, 26.7% corporate bonds, and 2.05% municipal bonds.

The key attraction for ZAG is the relatively high yield of 3.45%. Plus, it also has the lowest MER in my list of five Canadian bond ETFs.

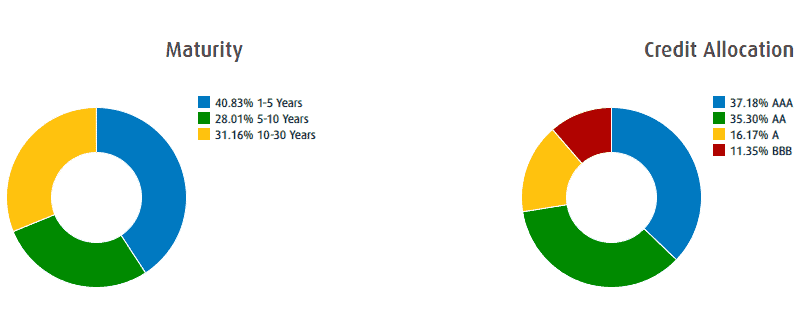

With a weighted average maturity of 10.35 years, I’d categorize ZAG as a medium-term bond ETF. However, over 40% of its holdings mature in less than five years.

3. Vanguard Canadian Short Term Corporate Bond Index ETF (VSC)

Vanguard Canadian Short Term Corporate Bond Index ETF invests primarily in public, investment-grade corporate fixed income securities issued in Canada. The fund employs a passively managed, index-sampling strategy to gain exposure to the short-term corporate bond market.

VSC invests in 339 short-term corporate bonds with an average duration of 2.7 years and an average maturity of 3.5 years. No doubt, I’d definitely categorize VSC as a short term bond index ETF.

Given that VSC invests only in corporate bonds, investors need to pay close attention to the underlying bond credit rating. At the time of writing over 75% of the underlying corporate bonds have a credit rating of A or higher. VSC’s corporate bond mix is certainly different from XHB’s. Because VSC holds higher credit rating corporate bonds, it has a lower yield compared to XHB.

Remember, higher yields usually mean higher risks

Given the high concentration of AA and A-rated corporate bonds, this is probably the reason why VSC has a relatively low yield of 2.66%. But considering that interest rates are rising and VSC’s underlying bonds are very short term, it is very likely for VSC to have a higher yield as interest rates rise.

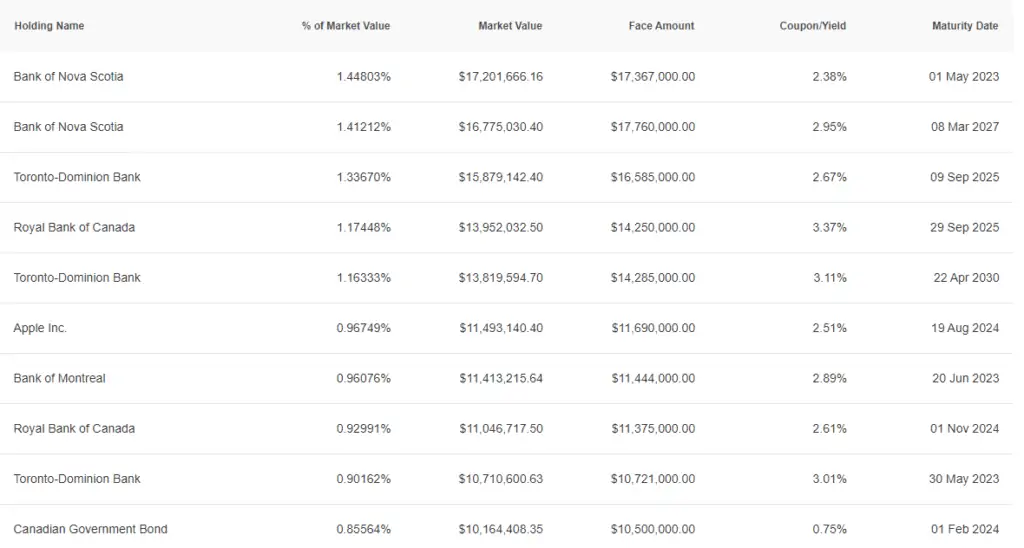

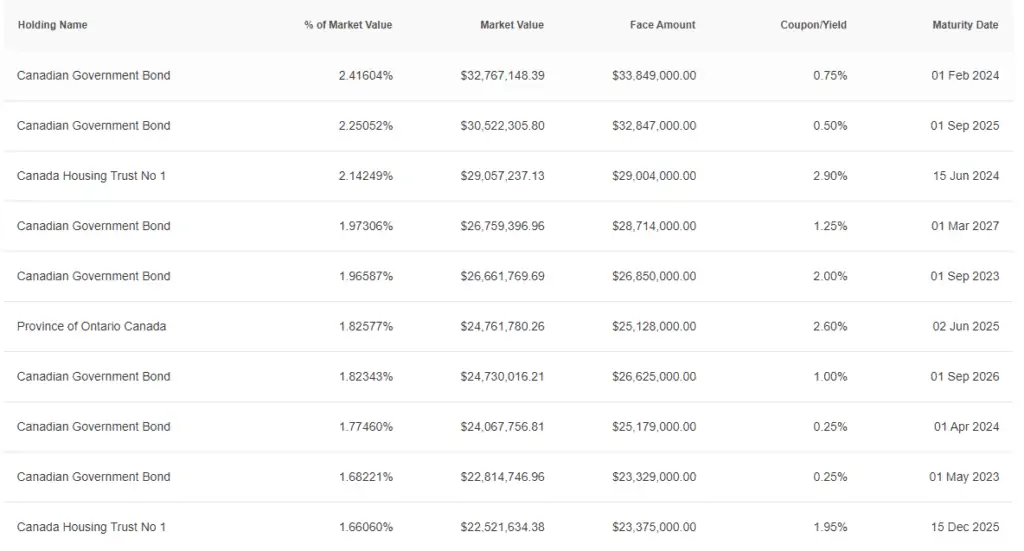

If we look at VSC’s underlying issuers, we’ll see that the top ten issuers are all well-recognizable corporations like Bank of Nova Scotia, TD, Royal Bank, Apple, and Bank of Montreal. Interestingly, despite VSC’s name, it has the Canadian Government Bond listed as one of the top ten issuers.

4. Vanguard Short Term Bond Index ETF (VSB)

Vanguard Canadian Short Term Bond Index ETF seeks to track the Bloomberg Global Aggregate Canadian Government/Credit 1-5 year Float Adjusted Bond Index and primarily invests in public, investment-grade fixed income securities issued in Canada.

VSB holds 477 bonds with an average duration of 2.6 years and an average maturity of 3.0 years. Like VSC, VSB is considered a short term index ETF.

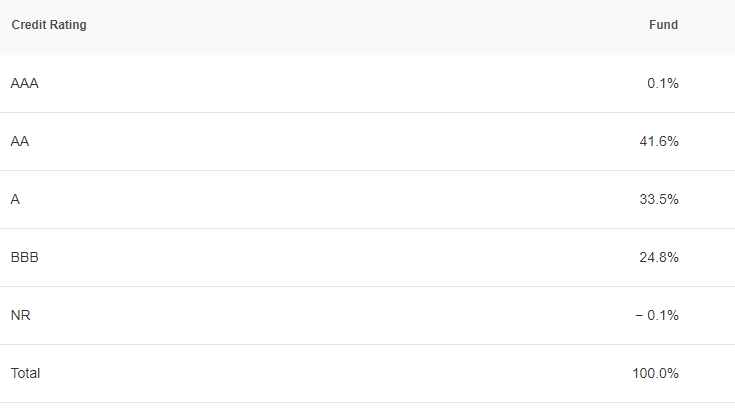

At the time of writing, VSB holds 46.8% AAA rated bonds, 31.5% AA rated bonds, and 12.2% A rated bonds. In other words, I’d say VSB provides a steady fixed income with high credit quality.

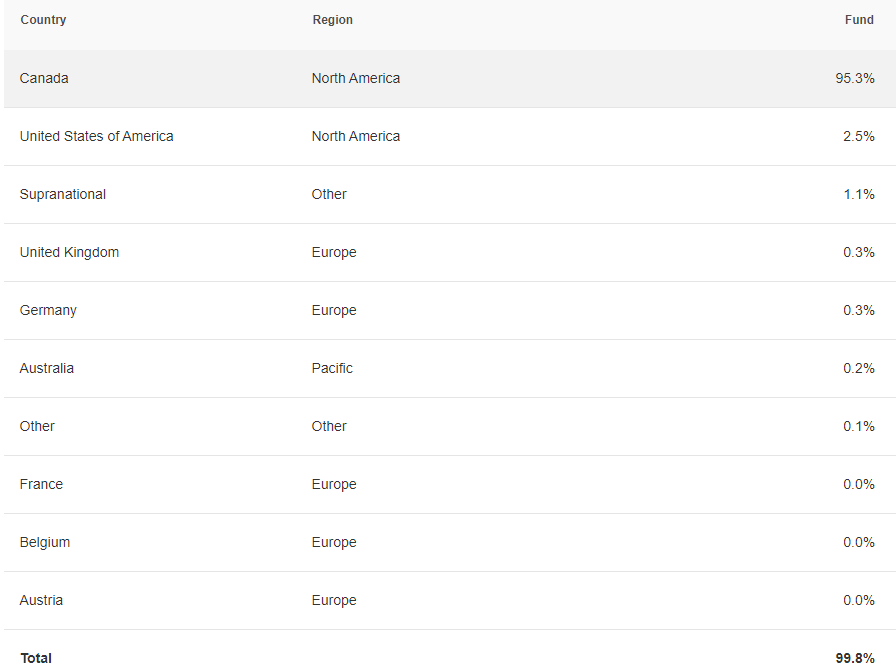

As expected, the top 10 issuers of VSB are either federal or provincial governments.

VSB has the shortest average duration and maturity out of all five bond ETFs compared, so it makes sense it also has the lowest yield. However, I believe VSB’s yield will increase quickly as the Bank of Canada increases interest rates and more short term government bonds with higher yields become readily available.

5. Vanguard Canadian Aggregate Bond Index ETF (VAB)

Vanguard Canadian Aggregate Bond Index ETF invests primarily in public, investment-grade fixed-income securities issued in Canada. Like BMO Aggregate Bond Index ETF, VAB invests in a mix of federal, provincial, municipal, and corporate bonds with an average weighted duration of 7.6 years.

The only difference between VAB and ZAG is that VAG does have a slight exposure outside of Canada whereas ZAG has a 100% exposure to the Canadian market.

VAB holdings have a credit holding of BB and higher, with the majority of its bond holdings with a credit holding of AA or higher. Given the high credit ratings, it is less likely for these bonds to default. So I’d rate VAB as a relatively safe bond ETF to invest in.

Which Canadian Bond ETF is the best?

After examining these five Canadian bond ETFs, you might wonder, which one of them is best?

Well, that depends on your goal. If you’re looking for a steady fixed income, then the iShares Canadian Hybrid Corporate Bond ETFs 4.13% yield becomes quite attractive. The key thing to consider with XHB is that the majority of its underlying bonds only have a BBB credit rating. So it is more likely that some of the underlying bonds won’t be able to pay their principal and interest in a timely fashion.

If I had to pick one Canadian bond ETF that has a decent yield and good credit rating, I would go with either the BMO Aggregate Bond Index ETF or the Vanguard Canadian Aggregate Bond Index ETF. Since I want a steady fixed income for bond investments, I’d probably pick ZAG over VAB given ZAB has a slightly higher yield of 3.45%.

Should I invest in Candian Bond ETFs or go with an all-in-one ETF?

Over the last few years, I have come to really like the all-in-one ETFs that Vanguard, iShares, and Horizons offer. The beauty of these all-in-one ETFs is that the funds keep the desired bond-to-stock mix and rebalance themselves regularly.

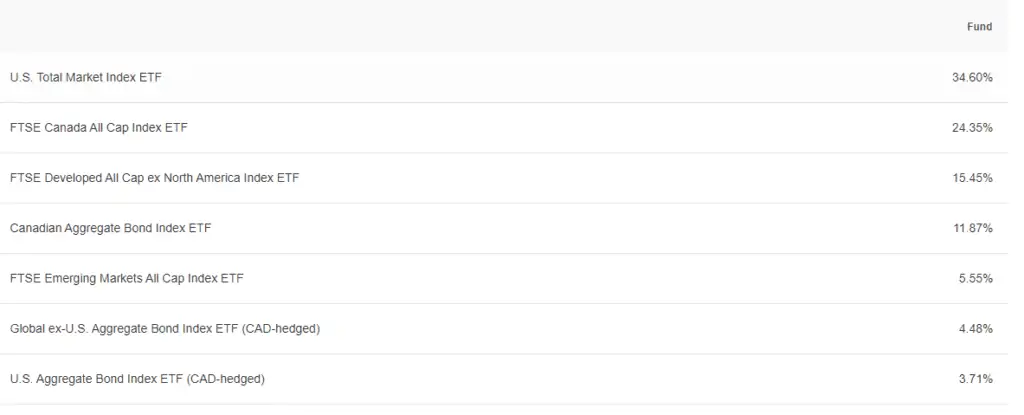

If we take the Vanguard Growth ETF Portfolio, VGRO, as an example, we’ll see that VGRO has roughly 80% in equities and 20% in bonds. What does VGRO invest in the underlying Canadian bond portion?

As you can see, VGRO holds VAB for its Canadian bond portion.

This begs the question, should you invest in Canadian bond ETFs or go with an all-in-one ETF?

Well, I think that completely depends on your investing style. If you want to be entirely passive and don’t mind paying a slightly higher MER, I think using one of the all-in-one ETFs is a great idea.

If you are like us and hold a mix of individual dividend stocks, index ETFs, and growth/speculative stocks and want to increase your exposure to bonds as you get closer to retirement, I believe investing in one of the five Canadian bond ETFs listed above makes a lot of sense. For us, we’d most likely pick ZAB as the bond ETF to hold as part of our portfolio.

Here are some articles you might want to check out:

- Best Canadian monthly dividend stocks

- Best Canadian utility stocks

- Best Canadian REITs

- Best Canadian REIT ETFs

- Best Canadian dividend ETFs

- Best Canadian Renewable Energy stocks

Remember, personal finance is personal so you must build your portfolio to fit an investment style and strategy that makes sense to you.

What are your thoughts now that we are coming to the time where the US will be cutting interest rates… what US bond ETF’s would you be looking at to take advantage of that? I would assume you would want long term treasuries 10-20yrs out to invest in given these should see the biggest jump in value?

In general I don’t think bonds are good investments especially if you’re young. If you’re in retirement already, bonds might be OK for you to consider.

What do you think of XLB.TO?

Given the rising interest rates, I’d stay away from long term bonds at this moment.

Hi Bob,

Thanks for the insightful article on bond ETFs and also for sharing comparison of these. I have a few questions or points below. Need your inputs/thoughts on these.

1) Based on the Bond ETF yields and other information. I believe a reasonable yield to expect would be 2.5% to 3.5% per year – ofcourse it can vary depending on performance. So roughly one ends up with close to 3% yield/return before tax. Lets say yield after tax works out to 2.5%. If we try to estimate returns after inflation it would be flat or close to zero. Probably this is good to preserve principal or capital not for returns. Please share your thoughts on this.

2) For anyone that is not close to retirement (say in 30s or 40s age group) and working professionals. Does it make sense to consider bond ETFs? Or are there better options out there that are bond-like say like blue chip dividend stocks, REIT ETFs or mortgage investment corporations that can be considered close proxy for safety.

Hi Sridhar,

Right, when you taken tax into consideration and inflation, the real purchasing power might be limited, but that’d be the case for GICs too.

As mentioned in the article, we don’t really hold any bonds in our portfolio right now. For us, we see some blue chip dividend stocks as a bond replacement. But people close to retirement may want to consider bonds to protect their investment portfolio.

This article on bonds clearly outlines an approach which goes hand in hand with “Value Investments”. Bravo for taking a complex subject and presenting a clear manageable approach.

You’re very welcome.