Earlier this year, I asked several dividend growth investing (DGI) bloggers and asked them to pick three of their favourite Canadian dividend stocks based on total growth (i.e. a combination of growth, dividend growth, or both). The picks from the DGI community were very interesting and closely mimic my selection of the 13 best Canadian dividend stocks and the 10 best Canadian monthly dividend stocks.

While Canadian dividend stocks have a good yield and solid dividend track record, many of these stocks fall in either the financial or oil & gas sectors. This is why geographical and asset diversification is extremely important. One way to diversify your dividend portfolio is to hold US dividend paying stocks.

Best US Dividend Stocks

It’s an understatement that there is a lot more dividend paying stocks in the US compared to Canada. For example, there are currently 101 Canadian dividend all stars (+5 years dividend streak) while there are 129 US dividend champions (+20 years dividend streak), 314 US dividend contenders (10-20 years dividend streak), and 309 US dividend challengers (<10 years dividend streak).

There are a lot of US dividend stocks available to pick from and it can get very overwhelming to go through the US champions list if you are not familiar with the US market.

So, what are the top US dividend stocks you should consider holding in your portfolio? With that question in mind, I reached out to the DGI community and asked DGI bloggers to pick their 3 favourite US dividend stocks.

Dividend Growth Investing Bloggers

Before we go through the picks and analysis, let’s go through the DGI bloggers that helped to pick out their top three US dividend stocks. I really appreciate them sending me their picks.

Dividend Diplomats

Lanny and Bert started Dividend Diplomats around the same time as me so we have been following each other’s dividend investing journey for the last seven years. Hopefully, I will get to meet Lanny and Bert in person one of these days.

The Dividend Guy

Mike is the brain behind The Dividend Guy. He is a passionate investor and founder of Dividend Stocks Rock (DSR). He has a bachelor’s degree in finance & marketing, owns an MBA in financial services, and worked as a financial planner with a CFP title for 10 years.

All About The Dividends

Matthew from All About The Dividends has been an active member of the Canadian DGI community. Matthew has built up a sizable dividend portfolio generating over $550 per month.

Dividend Earner

Dividend Earner hails from the Metro Vancouver area and has been a dividend growth investor for a very long time. His picks are not dividend income picks but dividend growth as well. The focus is consistent high dividend growth. Once the Chowder Score was tested, he focused on the tollbooth business and the future of the business.

Simply Investing

A seasoned dividend investor, Kanwal runs Simply Investing where he demonstrates ways to have your money work for you, so you don’t have to.

Get Rich Brothers

Rick and Ryan are the Get Rich Brothers. The two brothers share a common goal of bringing straightforward talk about finances to the masses.

Retire Before Dad

I started reading Retire Before Dad before I started blogging. It was one of the blogs that inspired me to start writing about personal finance.

Freedom Thirty Five

Liquid from Freedom Thirty Five Blog reached financial independence last year and has been utilizing a similar investment strategy as me. He believes his three best US dividend stocks can really help lay the path to financial independence.

Another Loonie

Another Loonie is a fellow Vancouverite, although I haven’t had the chance to meet him in person yet. AL has grown his net worth significantly in the last few years.

Passive Canadian Income

Rob is the brain behind Passive Canadian Income. He is a landscaper from Ontario and a true Maple Leaf and Blue Jays fan. Just like us, he and his wife have two young kids.

Reverse the Crush

Graham from Reverse the Crush is part of my Ultimate Canadian Dividend Blog Directory List. He writes about building income streams through blogging and dividend investing to reach financial independence.

Sure Dividend

Ben is the founder of Sure Dividend. He and his team help individual investors build high-quality dividend growth portfolios for the long run.

Dividend Growth Investor

Dividend Growth Investor has been blogging since 2008 and has been educating investors and sharing his experience with dividend growth stocks since then. He is a well-respected blogger within the DGI community.

Settling Nomad

Mr. R and Mrs. M from Settling Nomad are originally from India and immigrated to Canada in 2013. They are using the blog to write about their pursuit of financial freedom.

26 Best US Dividend Stocks – A round-up from the DGI community

Please note, these top US dividend stocks are picked by fellow bloggers from the DGI community. None of us are professional and these picks are simply our opinions. Please use this list as a suggestion.

Always purchase dividend paying stocks based on your own research. How to research? A good way is to learn how to read quarterly and annual reports.

Polaris Industries (PII)

Founded in 195, Polaris has been making high-quality, breakthrough products and broadening the view of powersports, including snowmobiles, ATVs, military vehicles, and 3-wheel moto-roadsters. While the company operates in a cyclical industry, it has a surprisingly long streak of 26 consecutive years of dividend increases.

- Sector: Consumer Discretionary

- Dividend Yield: 2.11%

- Dividend Payout: 26.4%

- PE Ratio: 12.55

- 5 Year Dividend Growth Rate: 2.97%

- Dividend Increase Streak: 26

Sure Dividend:

Polaris managed to compound its adjusted earnings-per-share at a 10.3% annual rate from 2011 through 2020. Adjusted earnings-per-share increased in 2020 – a surprisingly positive result during a difficult period. We conservatively expect annual earnings-per-share growth of 5% ahead, but results could exceed this estimate.

Polaris seems like it would not hold up in difficult economic periods – but its results say otherwise. This perception might be why it’s trading for a low price-to-earnings ratio of just 12.55 times our expected adjusted earnings-per-share of $9.48 for fiscal 2021. For comparison, the company has regularly traded for a price-to-earnings ratio of around 20 in the past. If Polaris were to return to our fair value estimate price-to-earnings ratio of 16.0 over the next five years, this would add 4.6 percentage points to annual returns.

Polaris has a history of growth, with more growth likely in the future. The company’s stock appears undervalued at current prices. The stock currently offers investors a 2.11% dividend yield as well. Altogether this adds up to expected total returns of over 11% annually.

Aflac Incorporated (AFL)

Founded in 1955, Aflac is the largest provider of supplemental insurance in the US and provides financial protection to more than 50 million people worldwide.

- Sector: Healthcare

- Dividend Yield: 2.89%

- Dividend Payout: 25.9%

- PE Ratio: 8.99

- 5 Year Dividend Growth Rate: 8.54%

- Dividend Increase Streak: 39

Simply Investing:

- AFL is currently undervalued because its current dividend yield (2.89%) is higher than its 20-yr average dividend yield (2.03%).

- AFL has been paying dividends since 1973.

- AFL has had 39 years of consecutive dividend increases.

- AFL is the biggest supplier of supplemental insurance in the U.S. and also one of the biggest insurance companies in the U.S. by assets.

- AFL’s payout ratio is 25.9%, there’s room for future dividend growth.

- P/B ratio is a low 1.1.

- AFL is currently trading below its Graham price of $74.36.

- Long-term debt to equity ratio is 23.6%.

- In my opinion, AFL is recession proof.

- AFL passes all my 12 Rules of Simply Investing.

Johnson & Johnson (JNJ)

For more than 130 years, JNJ has kept people well at every age and every stage of life. It is the world’s largest and most broadly-based healthcare company with a very impressive dividend increase streak of 59 years.

- Sector: Healthcare

- Dividend Yield: 2.60%

- Dividend Payout: 63.8%

- PE Ratio: 24.35

- 5 Year Dividend Growth Rate: 6.05%

- Dividend Increase Streak: 59

Dividend Diplomats:

Dividend King, over 50+ years of increasing their dividend, COVID-19 vaccine, strong brand recognition and a consistent dividend growth stock!

Price to Earnings ratio is typically below 20x forward earnings and they have a perfect dividend payout ratio.

All About The Dividends:

I’m a big fan of Johnson & Johnson. I own this stock personally!

Johnson & Johnson has three big business units and they are Consumer Health Products (Tylenol, Benadryl, Aveeno and Band-Aids), Medical Devices and Pharmaceutical Products. JNJ is in our lives on a daily basis and I don’t see this changing.

This company has been around for 130 years and is on the dividend aristocrats list. JNJ has raised their dividend for 59 consecutive years, and currently has a yield of 2.65%.

Their last eight increases have been in the range of 4.9% to 7.1%. With JNJ’s history, we can expect increases like these to continue for some time into the future.

Reverse The Crush:

Johnson & Johnson owns a portfolio of healthcare brands that we all know and use regularly – Band-Aid, Tylenol, and Benadryl, to name a few. Given there is an ageing baby boomer demographic, there will be more needs for JNJ’s products for years to come.

Furthermore, JNJ has been paying dividends to its shareholders for decades. Investors can visit their website to see the dividend history all the way back to 1972.

At a current dividend yield of 2.60%, dividend investors will receive $4.24 annually for each share of JNJ they own. Based on their track record of raising the dividend as well as the need

for their products, JNJ is one of the best US dividend stocks out there.

JNJ is a core US dividend stock for income investors to own.

Freedom Thirty Five:

This company makes consumer, pharmaceutical and medical products. Many of its brands are number one in their categories. Household names like Band-Aid, Listerine, Motrin, Splenda, and Tylenol, are all part of the Johnson & Johnson family.

Prospects are looking much better now than last year as the class action lawsuits against it have been settled.

Earlier this year the healthcare company announced a dividend increase, making it the 59th year in a row of dividend raises. As a dividend king, JNJ represents a steadily growing company with a long history of increasing shareholder value.

The company boasts a rare triple-A balance sheet and rewards investors with a 2.60% dividend yield. The price to earnings ratio is not considered cheap at 24 times, but it is fairly valued relative to the broader market. With the steady track record that JNJ has had over the decades, I think it has proven itself to be a safe anchor for any dividend portfolio.

Passive Canadian Income:

One of the best dividend kings out there. Day to day millions of people use their products and the good thing is that their stock price is at a good price at the moment.

This is one of two AAA-rated companies in the US. Gotta love that. JNH produces products people need, triple-A credit rating and 59 years of continuous dividend raises.

This is a stock every dividend growth investor should have in their portfolio.

Pfizer (PFE)

Pfizer is a research-based, global biopharmaceutical company. The company is getting a lot of attention lately because of its effective COVID-19 vaccine.

- Sector: Healthcare

- Dividend Yield: 3.07%

- Dividend Payout: 47%

- PE Ratio: 15.3

- 5 Year Dividend Growth Rate: 5.84%

- Dividend Increase Streak: 11

Retire Before Dad:

Pfizer (PFE) has paid a quarterly dividend for the past 82 years. Though the company cut it during the 2008-2009 financial crisis, it has grown the dividend by 7% over the past decade and currently yields more than 3%.

Pfizer may be a large established pharmaceutical company, but it was incredibly nimble developing and deploying its COVID-19 vaccine. Revenue from the drug in Q2 2021 was almost $8 billion, and the expected full-year revenue is $33 billion. That’s on top of multiple existing billion-dollar drugs and a thriving pipeline. Pfizer will invest proceeds of its COVID-19 vaccine and leverage the technology to fuel growth.

Lockheed Martin (LMT)

Lockheed Martin is a global security and aerospace company that employs approximately 114,000 people worldwide. The company is primarily engaged in the research, design, development, manufacturing, integration, and sustainment of advanced technology systems, products, and services.

- Sector: Industrials

- Dividend Yield: 3.28%

- Dividend Payout: 51.7%

- PE Ratio: 15.75

- 5 Year Dividend Growth Rate: 9.6%

- Dividend Increase Streak: 19

Dividend Diplomats:

Another dividend growth stock with a solid track record of high dividend growth. A yield over 2x the rate of the S&P 500, with a dividend growth rate that averages 9.6% over the last 5 years.

Almost a dividend aristocrat and another dividend stock with a low payout ratio that is showing signs of undervaluation.

All About The Dividends:

Lockheed Martin is one of the big defence contractors in the United States. Lockheed has four business units Aeronautics, Missiles & Fire Control, Rotary & Mission Systems and Space.

Aeronautics is the biggest unit and more well known as the unit’s main product is the F35 5th Generation fighter aircraft.

Several years ago the United States military selected the F35 to be their newest fighter aircraft and currently have plans to purchase 2,376. There are also 13 countries involved in the project and Lockheed is expecting about 3,000+ jets to be eventually ordered. So far over 690+ have been delivered, so plenty more years of production are expected.

Lockheed Martin has been paying a dividend for years and increasing it every year. The stock currently yields 3.28%, the last 8 increases have been in the range of 8.3% to 15.6%. I expect the future dividend increases to continue to be in this range.

Passive Canadian Income:

Maybe not a stock for everyone but defence stocks are not going away anytime soon.

Lockheed Martin is cheap right now. I have been buying more of it, people think the Republicans will cut defence spending but that ain’t gonna happen. I watched a show about AI and China using it for their military and I found it a little scary.

There will be some massive changes in the next 10 years in the industry and I think LMT will benefit from it. The US can’t afford to cut defence spending when China is stepping it up.

LMT has reduced their share count by 26.23% since 2010 and raised its dividend for the last 19 years! Low PE ratio and also a low payout ratio, this is one stock I plan on buying more at these prices.

Dividend Growth Investor:

Lockheed Martinis a key defense contractor for the US Defense, spending for which is very important for National Security purposes. The company has increased dividends for 19 years in a row and has a ten year annualized dividend growth of 14%. LMT has managed to grow earnings from $7.81/share in 2011 to $24.30/share in 2020. The company is expected to earn $22.14/share in 2021 and $27.89/share in 2022.

The stock is attractively valued at 13 times forward earnings and yields a solid 3.2%. This is a well covered dividend, coming from an earnings base that would likely grow in the high single digits over the next decade.

Verizon Wireless (VZ)

Verizon is the largest US wireless network operator with 121.3 million subscribers. Verizon currently has two business segments, Verizon Consumer and Verizon Business. The company has been heavily investing in the new 5G network and infrastructure.

Verizon’s dividend growth rate is around 2% over the last ten years. Although it doesn’t have the highest dividend growth rate, it does offer a juicy +4% initial dividend yield. Verizon might be a good choice for investors that are looking for short term income rather than long term dividend growth.

- Sector: Telecommunications

- Dividend Yield: 5.03%

- Dividend Payout: 48.12%

- PE Ratio: 9.56

- 5 Year Dividend Growth Rate: 2.16%

- Dividend Increase Streak: 17

Dividend Diplomats:

The 5G powerhouse, Verizon announced another consistent dividend increase of 2%. They currently yield over 5%, the payout ratio is below 50%, with a price-to-earnings ratio below 12x forward earnings. It’s hard to find a leader in this industry with these stock metrics.

Intel Corporation (INTC)

Founded in 1968, Intel is the world’s largest semiconductor chip manufacturer by revenue. Its processors can be found inside most PCs.

- Sector: IT

- Dividend Yield: 2.81%

- Dividend Payout: 27%

- PE Ratio: 9.61

- 5 Year Dividend Growth Rate: 6.27%

- Dividend Increase Streak: 7

Simply Investing:

- INTC is currently undervalued because its current dividend yield (2.81%) is higher than its 20-yr average dividend yield (2.29%).

- INTC has been paying dividends since 1991.

- INTC has had 7 years of consecutive dividend increases.

- INTC is the largest semiconductor company in the world by sales.

- INTC’s payout ratio is a low 27%, there’s room for future dividend growth

- Long-term debt to equity ratio is 41.6%.

- INTC passes all my 12 Rules of Simply Investing.

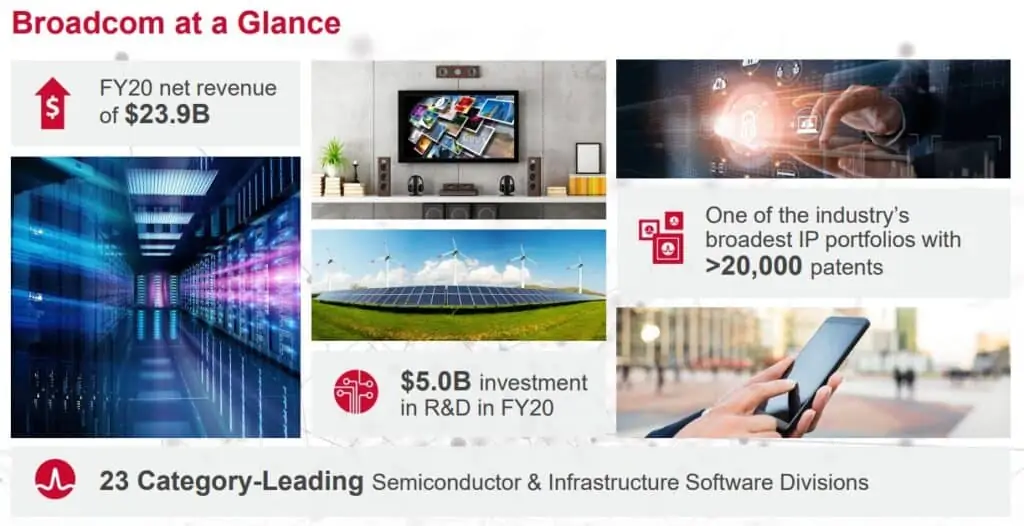

Broadcom (AVGO)

Broadcom is a global infrastructure technology leader built on 50 years of innovation, collaboration, and engineering excellence. Broadcom focused on technologies that connect our world. In 2020, Broadcom debuted the industry’s first 5nm ASIC for data center and cloud infrastructure.

- Sector: IT

- Dividend Yield: 2.53%

- Dividend Payout: 106%

- PE Ratio: 42.13

- 5 Year Dividend Growth Rate: 50.01%

- Dividend Increase Streak: 12

A high growth sector, Broadcom has been raising its dividends at a very stunning rate over the last decade. Given that many companies use Broadcom’s products in communication devices, servers, and high-performance connectivity, Broadcom isn’t going away anytime soon.

The Dividend Guy:

Broadcom is in a bowl of growth. It manufactures one of the best RF filters used by all high-end smartphones to improve connectivity. Companies, like Apple, would not risk their connectivity, right? AVGO’s large size brings economies of scale and enables it to build millions of filters.

Its growth-by-acquisition strategy has also turned it into an expert in integrating companies. In a decade, AVGO went from $2B to nearly $24B+ in sales. Broadcom’s expertise and technology will be required across multiple fields such as data center, internet of things, artificial intelligence, and cloud equipment.

Broadcom isn’t a classic dividend payer. It needs lots of cash to finance its fast growth and the R&D required to keep its edge. Still, the company has successfully increased its dividend yearly since 2010.

The payout ratio seems quite hectic and out of the norm (over 100% many times). This is caused by multiple charges related to its acquisitions and other events. It is better to investigate their investors’ presentation or follow the cash payout ratio.

The cash payout ratio is under control (under 50% over the past 5 years). As expected, shareholders received another dividend increase in late 2020 (from $3.25 to $3.60 +10.8%).

Apple (AAPL)

Apple is the most well-known brand in the world and the world’s largest technology company by revenue. Although the company specializes in consumer electronics like the iMac desktop, MacBook laptops, iPhones, TV, and iWatch, Apple has slowly evolved into an online services company.

Apple is in the process of transitioning from Intel-based CPU Macs to Apple designed solutions. This transition will mean that many existing customers will upgrade their laptops and desktops in the upcoming years.

- Sector: IT

- Dividend Yield: 0.55%

- Dividend Payout: 17.2%

- PE Ratio: 31.44

- 5 Year Dividend Growth Rate: 9.42%

- Dividend Increase Streak: 9

Dividend Earner:

While Microsoft is about business to business, Apple is about consumers. The mobile business has settled into 2 players with iOS and Android and iOS tends to cater to more affluent consumers.

With a massive consumer based needing and willingness to update their phones, Apple can operate almost like a subscription with phone upgrades followed by actual subscriptions with all the additional services such as Apple Music, iCloud, Apple TV+ and so on. A recent bundle I saw is almost a no-brainer if you already have an Apple Music family plan.

My biggest reason above all is the iWatch and the health angle Apple is targetting.

Reverse The Crush

I picked Apple because I know the company well and they have a low dividend payout ratio. According to Morningstar, the payout ratio is 17.2%, so I expect years of dividend growth to come from AAPL. So, that will make up for the lower yield which is currently listed at 0.55%.

Apple is a strong brand with pricing power. Like Starbucks, its customers are extremely loyal to the brand. The company has a sticky ecosystem that is hard to leave, and a growing service business.

Despite the large market capitalization and diminishing growth prospects, I still think Apple is a top US dividend growth stock.

Settling Nomad:

Apple is the biggest company by market-cap with nearly $2.4 trillion valuation and also the most innovative company since 2005. In the last 5 years, the price appreciated nearly 400% and boasts a dividend yield of 0.62% with the last 5 years dividend growth rate of 9.42% and a payout ratio of 17.2%.

With nearly every other person boasting its product, be it an iPhone, iPad or a MacBook, it is one solid company to own for a long long time.

Gentex (GNTX)

Gentex manufactures automatic-dimming rear-view mirrors, camera-based driver assistance systems, and the HomeLink Wireless Control System for the global automotive industry. The company also provides commercial smoke detectors and signalling devices as well as dimmable aircraft windows. About 98% of Gentex’s net sales are derived from the sale of auto-dimming mirrors to every major automaker in the world.

The advance of autonomous vehicle technology means the need for more advanced imaging systems, Gentex’s 20+ years of experience in CMOS imager development and supply puts the company in a good place for future growth and profitability.

- Sector: Consumer Discretionary

- Dividend Yield: 1.31%

- Dividend Payout: 27.6%

- PE Ratio: 21.07

- 5 Year Dividend Growth Rate: 7.15%

- Dividend Increase Streak: 11

The Dividend Guy:

Gentex is the industry leader and its products are on the way to becoming industry standards. GNTX also shows a stellar balance sheet with virtually no debt and tons of patents. It can weather any economic storm and could become an interesting candidate for a merger.

GNTX also benefits from being the first to offer this high-quality product. This leads to higher margins for early adoption and puts Gentex #1 in automakers’ minds for future orders. We appreciate the company’s effort to diversify its business model and not remain a “one-trick-pony”.

The company is expanding its product offerings to toll modules, airplane windows, and in long-term healthcare applications such as lighting for operating rooms and iris identification and smoking detection for the interior of autonomous vehicle fleets. Gentex is set to continue its growth for at least a decade.

GNTX has increased its payouts each year since 2011 but has not increased it in 2021 yet (July 2021). We were disappointed by the 2019 increase (+5%) and 2020 (+4.5%), but we can expect steady growth in the next few years. Current payout and cash payout ratios allow room for future increases.

Gentex is sitting on a pile of cash (over $456M as of March 31st, 2021) and has virtually no debt. Expect mid-single-digit dividend growth numbers for the next decade. Management will also continue its share buyback program.

Don’t mind the company’s DDM valuation; low yielding stocks must show double-digit growth to show any value using this model.

Franklin Resources (BEN)

Founded in 1947, Franklin Resources is a financial services company that is consistently at the top of my free Dividend Aristocrats ranking system.

- Sector: Financials

- Dividend Yield: 3.23%

- Dividend Payout: 46.3%

- PE Ratio: 14.33

- 5 Year Dividend Growth Rate: 14.87%

- Dividend Increase Streak: 41

Retire Before Dad:

The company has raised its dividend annually for 41 years, increasing about 15% each year over the past decade.

BEN is perceived to have missed the passive investing trend (index investing) but has a sticky customer base and is not afraid to make acquisitions, recently acquiring O’Shaughnessy Asset Management. BEN has a strong balance sheet with nearly $4 billion in cash, and only about $4 billion in debt, which is rare in this low rate environment.

Microsoft (MSFT)

When one mentions personal computers, Microsoft and their operating systems usually come to mind. But Microsoft has evolved to a company that produces more than just computer software. The company now produces consumer electronics and other computer-related services like the Microsoft Azure Cloud. Microsoft is considered as one of the big five companies in the US IT industry, along with Google, Apple, Amazon, and Facebook.

- Sector: IT

- Dividend Yield: 0.72%

- Dividend Payout: 27.7%

- PE Ratio: 38.35

- 5 Year Dividend Growth Rate: 9.452%

- Dividend Increase Streak: 19

At a PE ratio of above 35 and a dividend yield rate below 1%, Microsoft might not be the first US dividend stock that many dividend investors consider from a yield and value point of view. But the company has shown continued innovation and revenue growth. MSFT’s total return over the last decade has been very impressive. With such a low dividend payout ratio, the dividends should continue to grow as well.

All About The Dividends:

I imagine I don’t really need to tell people about Microsoft, they are such a massive company. Everyone probably has used their software to operate their computer or played Xbox.

Looking at Microsoft’s yield of 0.72% you’re probably yelling at the computer “Why is Matthew selecting Microsoft as a top dividend stock?”. Well, always look at total returns as an investor, Microsoft has been raising their dividend for years in the 7 to 21% range and we’ve also seen good returns on the company’s share price.

Microsoft has been spending billions of dollars in the last few years buying LinkedIn, GitHub, Affirmed Networks, ZeniMax Media and the planned purchase of Nuance Communications which should be completed by the end of this year. Even after making these purchases Microsoft still has billions of dollars left sitting in the bank to either make more purchases or to reward shareholders. I expect both to happen!

In a new pandemic world where more and more people are working from home, I believe Microsoft would make a great addition to anyone’s portfolio.

Dividend Earner:

MSFT is by far the best performing stock in my portfolio. When you look at Microsoft, it’s not about your personal experience, it’s about the business to business. That’s where Microsoft shines.

Office is still the go-to business application and has been for years. Cloud computing is a growing business and Microsoft is competing with the big players in that space.

Passive Canadian Income:

The tech giants are monsters, are they getting too big and powerful? I don’t know but for sure you want to have them in the portfolio.

Microsoft is the other triple A rated company. They have been growing at a solid pace and I don’t see that changing anytime soon. AI and technology, in general, is the future and Microsoft is a dominant force, not to mention the cloud and all the reoccurring revenue they bring in.

Microsoft has a massive stack of cash and will continue to put that to work. Recently they raised their dividend 10% and announced a 60 billion dollar stock buyback plan. Microsoft is very shareholder friendly.

Is the stock a buy at the moment? Some people say it’s overvalued but they have been saying that since the stock was at $200. The future is bright, covid has only accelerated things in the tech space.

Get Rich Brothers:

The part of Microsoft that most excites me is its Intelligent Cloud division which contains its Azure cloud computing platform. This division routinely grows at a healthy double digit rate (often ~50%), as it delivers services across diverse industries including healthcare, financial services, manufacturing, and within governments.

Microsoft is recognized as a top flight operator that can securely provide the necessary infrastructure to keep our digital age booming.

The dividend yield is low—currently sitting at 0.72%—though the growth rate is strong; the recent increase was announced as 10.71%. The reason the yield is low is because the stock price has been steadily rising.

The J. M. Smucker Company (SJM)

The J.M. Smucker Company manufactures jam, peanut butter, jelly, fruit syrups, beverages, shortening, ice cream toppings, and other food products. Founded in 1897, SJM has been family-run for four generations.

- Sector: Consumer Staples

- Dividend Yield: 3.19%

- Dividend Payout: 55.7%

- PE Ratio: 17.48

- 5 Year Dividend Growth Rate: 6.09%

- Dividend Increase Streak: 24

Simply Investing:

- SJM is currently undervalued because its current dividend yield (3.19%) is higher than its 20-yr average dividend yield (2.34%).

- SJM has been paying dividends since 1960.

- SJM has had 25 years of consecutive dividend increases.

- P/B ratio is a low 1.6.

- In my opinion, SJM is recession proof.

- SJM passes all my 12 Rules of Simply Investing.

Merck & Co., Inc (MRK)

Merck & Co., Inc is a healthcare and drug manufacturing behemoth. Over the years, it has produced lifesaving treatments for cancer, diabetes, and other diseases. Most recently, Merck has been working to develop antiviral medications for COVID-19 and vaccines for human papillomavirus.

- Sector: Healthcare

- Dividend Yield: 3.22%

- Dividend Payout: 102.7%

- PE Ratio: 31.88

- 5 Year Dividend Growth Rate: 6.95%

- Dividend Increase Streak: 11

Another Loonie:

As an investor, Merck is attractive because of its steady revenue growth and long dividend history. Not to mention, Merck is well-positioned for future growth as they’ve engaged in an aggressive acquisitions strategy. So aggressive that in 2020 alone Merck made seven major acquisitions, spending over 7 billion dollars.

With this organic and inorganic growth strategy, expect Merck to continue to churn out lifesaving treatments and make a healthy profit along the way.

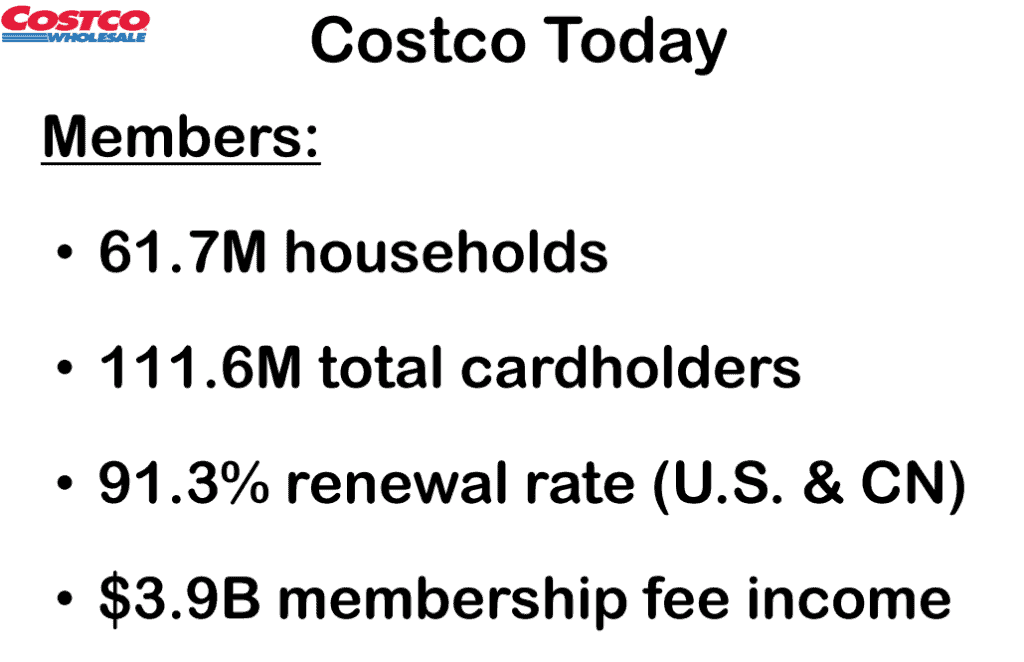

Costco (COST)

Costco is another well-known brand, not just in North America but globally. Unlike other grocery and retail stores, Costco doesn’t make a lot of margin from the merchandise. Instead, Costco makes money from their membership, like the Costco Executive Membership. In the last few years, Costco has improved its online presence in order to battle online retailers like Amazon. Recently Costco partnered up with Instacart to provide same-day grocery delivery service.

- Sector: Consumer Staples

- Dividend Yield: 0.59%

- Dividend Payout: 28%

- PE Ratio: 47.37

- 5 Year Dividend Growth Rate: 11.87%

- Dividend Increase Streak: 17

Dividend Earner:

Costco is also about consumers and what investors need to focus on is the membership subscription. Costco can lose money on some products but that means it retains customers for that and the bulk amount of products gives Costco significant buying power.

Online shopping at Costco works well for many items and the refund policy is just great. All in all, you don’t worry about shopping at Costco which allows them to retain their customers. A small increase in membership can bring a significant profit.

Retire Before Dad:

Costco is my favorite retail store for both shopping and investing. It pioneered the membership subscription model now deployed by some of the most admired companies in the world (e.g., Amazon).

Costco makes most of its money from subscriptions, then provides its members high-quality products and services. The company controls inventory by limiting the number of SKUs (4000 vs. about 80,000 Target) and only sells products that move off the stacks. It also sells gas, vacations, and cars and is ever-expanding through e-commerce.

The stock has run up recently, so we’d all like to see a pullback before acquiring more. But sometimes you must pay up for quality. Costco is a solid low yield, high growth dividend stock with a low payout ratio that isn’t afraid to make significant special dividend payments. The last was $10 per share in late 2020.

Innovative Industrial Properties (IIPR)

Founded in 2016, Innovative Industrial Properties targets medical-use cannabis facilities, including sale-leaseback transactions, with tenants that are licensed growers under long-term, triple-net leases. With cannabis posed for significant growth in the coming years, IIPR is counting that more cannabis facilities will be needed.

- Sector: REIT

- Dividend Yield: 2.18%

- Dividend Payout: 138.6%

- PE Ratio: 59.07

- 5 Year Dividend Growth Rate: 225%

- Dividend Increase Streak: 4

IPPR has had an impressive dividend growth rate over the last four years. The company is targeting a long term payout ratio of 75 to 85% of AFFO. Based on my quick calculation, the AFFO payout ratio is at the low end of this payout target. This means the company should be able to continue to grow its dividends at a high rate.

The Dividend Guy:

The cannabis industry is developing quickly these days, but it’s not happening without the occasional hiccup. A good way to enjoy part of this potential is to go through a REIT that specializes in medically licensed marijuana growers. You won’t get the full hype (as compared to a grower), but IIPR is looking to grow. U.S regulated cannabis sales are expected to go from $12.4B in 2019 to $34B in 2025. Both their funds from operations (FFO) and dividends are following the same trend recently.

The REIT paid its first dividend in 2017. At this point, the company’s dividend graph looks like a launching ramp. Although we appreciate IIPR’s growth potential, we have used more conservative numbers for our DDM calculations. At the current price, you will also enjoy a solid 2.18% yield. Expect the yield to decline further as the stock price continues to break new records. Management seems confident in the company’s future as it grows both its business and its dividend at a similar pace. The REIT targets a 75-85% AFFO payout ratio. So far IIPR shows an amazing dividend triangle.

JP Morgan Chase & Co (JPM)

JP Morgan Chase & Co is the largest bank in the US and the fifth-largest bank in the world with total assets of $3.684 trillion USD. The bank operates in over 100 global markets and employs more than 250,000 people.

- Sector: Financials

- Dividend Yield: 2.49%

- Dividend Payout: 26.68%

- PE Ratio: 10.73

- 5 Year Dividend Growth Rate: 15.39%

- Dividend Increase Streak: 10

Freedom Thirty Five:

JP Morgan is one of the best run banks in the world. Right now it is being carried by the hot capital market sector. But the bank has a lot of intrinsic value from internal operations that are sustainable and growing. With an expanding economy, new loans will grow the bank’s books.

If we see higher interest in the future it will only help JP Morgan’s net interest margins.

JPM is trading at just 11.38 times price to earnings, which is cheaper than competitor Bank of America. But JPM has a higher earnings per share growth rate making it clearly the more undervalued stock out of the two.

The dividend yield isn’t very high at just 2.49%, but the distribution has been growing over the years. The company didn’t cut dividends even in the stock market correction of early 2020. There are tremendous growth opportunities abroad. And some analysts are expecting future ROE to be in the mid-teens for JPM.

Abbvie Inc (ABBV)

Abbvie was formed in 2013 when Abbott Laboratories separated into two public traded companies. Under this new operation, Abbvie operates as a research-based pharmaceutical manufacturer. With over 48,000 employees, Abbvie focused on a new approach to address today’s health issues from life-threatening illness to chronic conditions.

- Sector: Healthcare

- Dividend Yield: 4.85%

- Dividend Payout: 134%

- PE Ratio: 27.67

- 5 Year Dividend Growth Rate: 18.09%

- Dividend Increase Streak: 49

Freedom Thirty Five:

This is one of the best research-based pharmaceutical companies out there. Abbvie has the lowest forward PE ratio among its competitors at just 9.17 times. And it has a dividend growth record of 49 years.

Sixty eight percent of shareholders are institutional investors which means many hedge funds and large investment firms see Abbvie as a profitable, long term asset they can rely on for their clients.

The company is developing new growth drivers to diversify away from Humira, a treatment for Crohn’s disease that goes off patent in 2023. With a wide economic moat and a dividend yield of 4.85%, ABBV is a dependable household name to hold for any dividend investor looking for a relatively high yield but also safety.

Settling Nomad:

Abbvie’s infamous product Humira has been the number one selling drug in the world since 2015 and last year it brought in nearly $20 billion in revenue for Abbvie.

In the last 5 years, Abbvie’s stock price appreciated about 80% with a juicy dividend yield of 4.85% and a 5 years dividend growth rate of 18.09%.

Sure Dividend:

AbbVie is a Dividend Aristocrat with 49 years of consecutive dividend increases, including its dividend history prior to its spin-off from parent company Abbott Labs (ABT). AbbVie is a large independent biotechnology company with a $191 billion market cap.

Adjusted earnings-per-share have increased every single year AbbVie has been a stand-alone company (fiscal 2013 was its first stand-alone year). Adjusted earnings-per-share have compounded at an impressive 18.9% annually from fiscal 2013 through fiscal 2020.

While historical growth has been impressive, the high growth rate is unlikely to be replicated. That’s because AbbVie’s Humira will lose its patent protection in the U.S. starting in 2024. With that said, AbbVie has greatly expanded its operations with its recent large Allergan acquisition. AbbVie’s management believes revenue will actually be higher in 2025 than in fiscal 2020, despite the Humira patent cliff.

The market is well aware of Humira’s patent cliff – and has priced AbbVie stock accordingly. The company’s stock currently trades for a price-to-earnings ratio of just 8.86 times our expected fiscal 2021 adjusted earnings-per-share of $12.57. And, the stock has a high 4.65% dividend yield.

We conservatively expect just 3.0% annual growth in adjusted earnings-per-share for AbbVie over the next five years. If the company’s stock sees its price-to-earnings ratio rise to a still-low 10.0 over the next five years, this will give AbbVie shareholders expected total returns of around 10% annually, including the high dividend yield.

Get Rich Brothers:

AbbVie is a biopharmaceutical company. Its products run the gamut within the immunology space as it services rheumatology, dermatology, and gastroenterology. Likewise, it has leading positions in hematologic oncology, neuroscience, and aesthetics.

While it is expected to face a sales decline in 2023 with its big-ticket Humira drug losing patent protection, it currently has a solid pipeline of other blockbuster drugs and products. It purchased Allergan last year which brought with it Botox, a household name in the neuroscience space.

Given the current macro environment related to COVID-19 and the general desire globally for additional and improved healthcare treatments, AbbVie has an endlessly long runway to continue innovating.

The company currently sports a healthy 4.85% dividend yield. Since being spun out of Abbott Laboratories (ABT) in 2013, ABBV has increased its dividend annually. The most recent increase this year was 10.17%.

When you combine a high starting yield with a demonstrated ability and willingness to increase that dividend in the double digits, it is a winning combination for shareholders.

Scotts Miracle Gro (SMG)

The Scotts Miracle-Gro Company manufactures, markets, and sells consumer lawn and garden products in the United States and internationally. The company operates through three segments: U.S. Consumer, Hawthorne, and Other.

- Sector: Materials

- Dividend Yield: 1.59%

- Dividend Payout: 29.3%

- PE Ratio: 18.43

- 5 Year Dividend Growth Rate: 5.70%

- Dividend Increase Streak: 12

Dividend Growth Investor:

SMG is a dividend achiever with a 12 year history of annual dividend increases. SMG has managed to grow dividends at an annualized rate of 12.30% over the past decade, though growth has slowed down to 5.7% in the past five. SMG has managed to grow earnings from $2.54/share in 2011 to $6.81/share in 2020. The company is expected to grow earnings to $9.16/share in 2021, but shrink a little to $8.63/share in 2022.

I believe that the stock has been punished severely in the past 6 months, going from overvalued at the beginning of the year, to undervalued.

Seagate Technology Holdings plc (STX)

Seagate Technology crafts precision-engineered data storage and management solutions. The company has been a harddrive technology leader since it was founded as Shugart Technology in 1979.

- Sector: IT

- Dividend Yield: 2.78%

- Dividend Payout: 40.9%

- PE Ratio: 14.71

- 5 Year Dividend Growth Rate: 1.27%

- Dividend Increase Streak: 18

Another Loonie:

Ten years ago, you’d be hard-pressed to find a reasonably priced technology company. Not to mention finding one that pays a sizable dividend. But these days, we have a few options, and there’s one specifically I’d recommend for yield-hungry investors: Seagate.

You’re probably familiar with Seagate as the hard drive manufacturer you see on the shelves at Best Buy and elsewhere. What you probably didn’t know is that Seagate is a 19 billion dollar “mini-stalwart” that has hiked its dividend just about every year since 2003. These days, Seagate’s shares earn investors a healthy 2.78% dividend yield – far higher than one would typically expect from a technology company.

Perhaps best of all, Seagate is well-positioned for growth in a world quickly moving more and more online. With the recent supply shortages of hard drives and other computer components, expect Seagate’s profit margins to increase as customers increasingly adopt their state-of-the-art solid-state drives.

Archer-Daniels-Midland (ADM)

Archer-Daniels-Midland is the largest publicly traded farmland product company in the United States thanks to its $34 billion market cap. The company’s business includes the processing of cereal grains and oilseeds, as well as storage and transportation for agricultural products. The company is a Dividend Aristocrat and has an impressive streak of 46 consecutive years of dividend increases.

- Sector: IT

- Dividend Yield: 2.27%

- Dividend Payout: 32%

- PE Ratio: 14.14

- 5 Year Dividend Growth Rate: 4.71%

- Dividend Increase Streak: 46

Sure Dividend:

Archer-Daniels-Midland is not typically a rapidly growing company. Adjusted earnings-per-share have only increased by 19% from 2011 through 2020, but recent results are better.

The company generated $2.72 in adjusted earnings-per-share through the first 6 months of fiscal 2021 versus $1.49 in the same period a year ago. We expect adjusted earnings-per-share of $4.77 in fiscal 2021, which is 32.9% more than fiscal 2020.

The market has not caught up with Archer-Daniel-Midlands recent results. It is currently trading for a price-to-earnings ratio of 14.14 using our expected fiscal 2021 adjusted earnings-per-share estimate of $4.77. For context, the company’s historical average price-to-earnings ratio over the last decade is around 15.5.

If the company were to return to a price-to-earnings ratio of 15 over the next five years, this would add over 3% to annualized total returns. On top of that, we expect earnings-per-share growth of 6.0% per year after fiscal 2021. This growth combined with valuation multiple expansion and the stock’s dividend adds up to expected total returns of 10%+ annually over the next five years.

Visa Inc (V)

Visa is a very well known global brand. Its payments technology connects consumers, businesses, banks, and governments in more than 200 countries and territories, enabling them to use digital currency instead of cash and checks. Visa has completely transformed how we purchase merchandise.

- Sector: Financials

- Dividend Yield: 0.575%

- Dividend Payout: 36.1%

- PE Ratio: 48.37

- 5 Year Dividend Growth Rate: 85.52%

- Dividend Increase Streak: 13

Although Visa has a very low dividend yield and the dividend growth rate has slowed, the stock has provided solid returns for its shareholders.

Settling Nomad:

Visa has about 2.5 billion cards boring their brand name earning transaction fees for them every time their card is swiped/tapped/inserted anywhere and as per 2020 data, a whopping $8.8 trillion transactions were processed by them with net revenue for Visa of $22 billion!

Altria Group, Inc (MO)

Altria Group, previously known as Philip Morris Companies, is one of the world’s largest producers and marketers of tobacco, cigarettes, and related products. The stock currently has an extremely high yield so income investors may be attracted to Altria.

Having said that, we don’t invest in the tobacco industry due to ethical reasons.

- Sector: Consumer Staples

- Dividend Yield: 8.29%

- Dividend Payout: 241%

- PE Ratio: 29.06

- 5 Year Dividend Growth Rate: 8.77%

- Dividend Increase Streak: 12

Another Loonie:

Altria Group, Inc is one of the world’s largest producers and marketers of tobacco, cigarettes, and related smoking products. Compared to the more well-known Philip Morris, Altria has had a less than stellar year, pushing its forward price-to-earnings ratio down to around ten and increasing its dividend yield to over 8%. Despite this, I wouldn’t worry about Altria cutting their dividend anytime soon as their earnings more than offset this impressive yield.

I like Altria because it’s an earnings powerhouse with a long history of reliable dividend growth in an industry that’s fallen out of favour with your average investor. Because of this, I feel that Altria is undervalued despite having immense staying power.

For one, Altria recognizes that it’s in an industry ripe for change and has taken action by investing heavily in the popular e-cigarette maker JUUL Labs. Altria is also working hard on developing its own non-combustible nicotine products.

By investing in these products, Atria ensures that they’ll appeal to a new generation of customers that are far more health-conscious and more knowledgeable about the impact of cigarette smoke than in the past.

United Healthcare (UNH)

UnitedHealth Group Incorporated operates as a diversified health care company in the United States. It operates through four segments: UnitedHealthcare, OptumHealth, OptumInsight, and OptumRx.

- Sector: Healthcare

- Dividend Yield: 1.32%

- Dividend Payout: 36%

- PE Ratio: 27.29

- 5 Year Dividend Growth Rate: 19.6%

- Dividend Increase Streak: 12

Dividend Growth Investor:

United Healthcare Group is the largest health insurer in the US. It has increased dividends for 12 years in a row and has a 10 year annualized dividend growth of 28.10%. UNH can grow earnings over the long term. The company has managed to grow earnings rapidly over the past decade, from $4.73/share in 2011 to $16.03/share in 2020. UNH is expected to grow earnings to $18.75/share in 2021 and $21.60/share in 2022.

The stock is attractive at 27.29 times forward earnings, given the expected earnings and dividend growth. While the dividend yield is not high at 1.32%, I expect double-digit dividend increases over the next decade.

Starbucks (SBUX)

Founded in 1971, Starbucks is a well-known international brand. As of September 2020, the company had 32,660 stores in 83 countries, including 16,636 company-operated stores and 16,023 licensed stores. In addition to offer coffee, tea, and other beverages, many Starbucks stores sell pre-packaged food items, pastries, hot and cold sandwiches, and drinkware.

Starbucks’ global presence is hard to ignore and many people visit Starbucks stores on a daily basis despite there are other choices. Therefore, brand loyalty is not something investors should ignore.

- Sector: Consumer Discretionary

- Dividend Yield: 1.77%

- Dividend Payout: 64.2%

- PE Ratio: 36.26

- 5 Year Dividend Growth Rate: 18.29%

- Dividend Increase Streak: 11

Reverse the Crush:

Of course, I am biased because I love coffee. But Starbucks is an excellent business to own for dividend growth.

They just recently announced a dividend raise of nearly 9% from $0.45 to $0.49 per quarter.

As for the dividend, the company initiated its dividend in 2010 and has increased it for 11 years in a row. At 1.77% dividend yield, SBUX doesn’t offer the highest yield out there, but it’s competitive, the stock still has growth, and dividend raises are likely for years to come.

They do have risks to deal with, as a result of the pandemic. However, their strong brand allows the company to maintain pricing power and develop new products for growth in new markets. You may have already noticed more of their products showing up at your local grocery store.

Despite some of the headwinds the company is facing, brand loyalty remains strong in the U.S. based on their most recent earnings report.

McDonald’s Corporation (MCD)

McDonald’s is one of the biggest fast-food companies in the world. Started in San Bernardino, California, the company has grown into an American icon that serves 6 million customers every day around the globe.

- Sector: Consumer Discretionary

- Dividend Yield: 2.19%

- Dividend Payout: 57%

- PE Ratio: 26.01

- 5 Year Dividend Growth Rate: 7.79%

- Dividend Increase Streak: 46

Get Rich Brothers:

The Golden Arches remain one of the best-recognized pillars of the fast food industry worldwide. McDonald’s both operates and franchises its restaurants.

While the company has been criticized on the basis of the nutritional content in the food it serves, the company has two huge advantages over its competitors:

- It operates at such a large scale and has mastered its supply chain to the point that it can pivot as needed, regardless of how consumer tastes or sentiments shift in the years to come. One example of this was their introduction of McCafé which has been hugely successful with its line-up of specialty drinks, donuts, and muffins.

- It has made great investments in digital technology which are beginning to pay off. This includes both the mobile ordering experience and plans it has with artificial intelligence to improve ordering and targeted marketing.

The bottom line is that McDonald’s is a known and trusted brand to consumers. Anecdotally, the three restaurants in my area habitually have line-ups around the clock, and I don’t see that stopping any time soon.

The company sits on a 2.19% dividend yield and recently announced its 45th consecutive dividend raise this year, clocking in at 6.98%. I love a long track record such as this because it demonstrates the company has staying power. It has been through many business cycles and continued to reward shareholders without fail.

Summary – Best US Dividend Stocks

Wow, this post ended up being way longer than I anticipated. Thank you so much to everyone for submitting their picks for the best US dividend stocks! It was quite interesting to read the analysis and reasoning behind each pick. There were certainly a few stocks like Innovative Industrial Properties that weren’t on my watch list.

While there were many picks, the top picks seemed to be some well-known international brands like Johnson & Johnson, Apple, Microsoft, Costco, and Lockheed Martin. Given all these companies have wide moats, this shouldn’t come as a surprise.

While many dividend investors focus only on dividend income, I believe it is extremely important to focus on total return. More importantly, time in the market is more important than timing the market.

If you don’t want to invest in individual dividend paying stocks, relying on a US dividend ETF might be a good idea. For Canadians, we can also invest in an all-in-one ETF like XBAL and VGRO to ensure geographical and asset diversification. If you already own a large amount of Canadian dividend paying stocks and want to utilize a low cost ETF for international exposure, you might want to look at an ex-Canada ETF like XAW.

I hope this best US dividend stocks post has been useful to readers.

Happy investing everyone!

Divi – Bob, I saw ur article “stock considering for 2024” and that u were going for 100% cdn in the TFSA because unlike in NR accts, the IRA does not reimburse the 15% dividend withholding tax on usa stocks, AND that u were generally in your other two accounts, swinging more to Cdn stocks to avoid FX exchange costs ( Divi comment: and perhaps tracking time and having to concern about checking in on rates regularly to translate how much the “real” unrealized and realized cap gains/losses on cost, actually are in Cad terms ), Given all of that are there still some usa dgr&g stocks that U own and are planning to stay with thru thick and thin and that u would buy again today or for the first time on ones u regretted not buying such as Blackrock, at a reasonable price point opportunity and if so why and what would those be in both of those usa categories? thks

We still plan to buy US stocks in RRSP. Probably not adding new positions but add more shares to existing positions.

ant thoughts on the FWT and the vehicle with which to hold these dividend players in…margin far better than TFSA and RRSP

Generally speaking for Canadians, it’s more tax efficient to hold US dividend stocks in RRSP.

This list is primarily large-cap stocks, but an interesting list all the same! Thanks Bob!

I also see some very large payout ratios here, which is a personal red flag for me. It implies future growth (and future dividend growth) will be quite poor.

Generally I shy away from buying heavy % payout stocks, but to each his or her own. Find what works for you!

Makes sense Mr. Tako. This is a list of the best US dividend stocks and certainly one needs to do more homework before investing one’s own money. 🙂

Awesome post, Bob! It turned out great. Very informative and there a few stocks on here I have not considered. After the recent announcement by $JNJ, I may be inclined to switch my $JNJ pick for $ABBV. Thanks again for putting this together and for including me.

Thanks Graham for participating. 🙂

Thanks for the inclusion in the list.

My top 5 holdings are listed here 🙂 That’s close to $500K. For transparency, my portfolio is here (https://dividendearner.com/dividend-stocks-portfolio/)

I will admit to struggle giving up on the return from my low yield stocks due to their growth. Not many of those on the Canadian side though …

Nice, you must have gotten some nice return over the years. 🙂

Thank you for the post!

Do you have any opinion on manually purchasing dividend stocks vs buying a dividend ETF?

Which dividend ETF do you recommend?

See here

https://tawcan.com/top-us-dividend-etfs-why-i-dont-buy-dividend-etfs/

https://tawcan.com/top-canadian-dividend-etfs-dont/

Hey Bob,

Simply a great article. So many diverse picks from the DGI community.

As you mention, investing south of the border is one of the best ways for Canadians to broaden our holdings. There are many companies in the U.S. that have no real Canadian counterpart, so it’s nice having access to this huge market.

Of the list, LMT and INTC are two I’m going to be taking a closer look at. It has been a while since I’ve cracked their annual reports.

Thanks again for including GRB in this article.

Ryan

You’re welcome Ryan.