A few readers have asked me why we don’t invest in rental properties and invest in real estate investment trusts (REITs) instead. There are a few reasons why we prefer investing in Canadian REITs rather than rental properties.

First, Mrs. T and I already have our hands full on a daily basis, we don’t want to have to worry and take care of all the potential pitfalls of rental properties like frozen pipes, broken toilets, or leaky roofs. Sure, we can use a property manager to deal with all that but that comes at a cost.

We’ve heard quite a few bad encounters from our friends who have had to deal with problem tenants. It seems that the BC rental laws are more favourable to tenants. Having to deal with potential bad tenants is a major headache that we don’t want to deal with. Lastly, the high property values in BC, and in Canada for that matter, makes the one percent rule difficult to achieve.

So after evaluating all the potential upturns and downturns of rental properties, Mrs. T and I decided that it is best for us to invest in real estate through REITs. Please note, this is our personal decision but for some, rental properties may make sense, especially if you’re very handy and love to do handy DIY projects.

Even if you do own rental properties, investing in REITs is a great way to diversify your real estate portfolio and gain exposure to different types of properties that you may not be able to own otherwise. Best of all, investing in REITs typically means higher dividend yields than regular dividend paying stocks, resulting in slightly higher dividend income each month.

What are some best Canadian REITs? Are the largest REITs always the best picks?

What is a real estate investment trust?

Before I dive deeper, let’s find out exactly what a real estate investment trust, or REIT is.

A REIT is a company that owns, manages, operates, or finances income-generating real estate properties. Like mutual funds, REITs pool capital from investors and use that capital to purchase or acquire properties under company ownership.

REITs typically have higher dividend yields than regular dividend paying stocks. Due to the business structure of REITs, anywhere from 80 to 95% of the income after expenses are passed directly to shareholders without being taxed at the corporate level.

This means dividends from REITs are typically considered as ineligible dividends and thus are not eligible for the Dividend Tax Credit. In fact, distributions received in a non-registered account are usually counted as a combination of normal income and capital gains, and taxes can be applied accordingly.

Therefore, to directly address one of the earlier questions above, if you do invest in REITs, it is best to hold them in tax-advantaged accounts like TFSA or RRSP.

List of all Canadian REITs

As you can imagine, there are many REITs available on the Canadian market. Usually, when people think of REITs, the first thing that comes to mind is retail REITs or companies that manage and operate shopping malls and retail spaces. But there are other REIT segments over and above the retail segment. In fact, there are seven different REIT segments:

- Industrial

- Healthcare

- Hotel

- Office

- Retail

- Residential

- Diversified

Note, senior residential REITs typically fall under the Healthcare segment.

Some companies can own a mix of segments, for example, office, retail, residential, and healthcare properties, making them diversified REITs.

Below is a list of 38 different Canadian REITs I could find. Note, I used the list from REIT report as my starting point, and then used data from the Canadian Dividend All Star list, Morningstar and Google Finance.

| Company | Ticker | Segment | YIELD % | Market Cap | Div Streak | 5 Yr DGR % |

|---|---|---|---|---|---|---|

| Allied Properties | AP.UN | Office | 3.83 | 5.42B | 10 | 2.5 |

| American Hotel Income Properties | HOT.UN | Hotels | 0 | 324.8M | 0 | 0 |

| Artis | AX.UN | Diversified | 4.64 | 1.68B | 0 | 0 |

| Automotive Properties | APR.UN | Diversified | 5.60 | 570.4M | 0 | 0 |

| Boardwalk REIT | BEI.UN | Residential | 1.72 | 2.59B | 0 | n/a |

| BSR REIT | HOM.UN | Residential | 2.09 | 746.8M | 0 | n/a |

| BTB REIT | BTB.UN | Diversified | 7.19 | 300.6M | 0 | -28.6 |

| Canadian NET REIT | NET.UN | Diversified | 3.82 | 167M | 10 | 13.3 |

| Canadian Tire REIT | CRT.UN | Retail | 4.86 | 1.84B | 9 | 3.9 |

| Canadian Apartment REIT | CAR.UN | Residential | 2.68 | 9.86B | 10 | 2.7 |

| Chartwell Retirement Residences | CSH.UN | Healthcare | 5.14 | 2.9B | 7 | 1.3 |

| Choice Properties REIT | CHP.UN | Retail | 4.89 | 4.7B | 0 | 1.4 |

| Cominar REIT | CUF.UN | Diversified | 3.07 | 2.14B | 0 | -81.6 |

| Crombie REIT | CRR.UN | Diversified | 4.99 | 1.8B | 0 | 0 |

| Dream Industrial REIT | DIR.UN | Industrial | 4.31 | 3.79B | 0 | 0 |

| Dream Office REIT | D.UN | Office | 3.67 | 1.19B | 0 | -20 |

| European Residential REIT | ERE.UN | Residential | 3.55 | 385.6M | 0 | n/a |

| Firm Capital Property Trust | FCD.UN | Diversified | 6.62 | 262.6M | 10 | 3.8 |

| First Capital REIT | FCR.UN | Diversified | 2.37 | 3.91B | 9 | 10.7 |

| Granite REIT | GRT.UN | Industrial | 3.08 | 6.31B | 11 | 4.4 |

| H&R REIT | HR.UN | Diversified | 4 | 3.75B | 0 | -42.3 |

| Inovalis REIT | INO.UN | Diversified | 8.65 | 330.4M | 0 | 0 |

| InterRent REIT | IIP.UN | Residential | 1.71 | 2.26B | 10 | 7.1 |

| Killam Apartment | KMP.UN | Residential | 3.11 | 2.54B | 5 | 2.8 |

| Melcor REIT | MR.UN | Diversified | 6.87 | 89.8M | 0 | -29 |

| Minto Apartment | MI.UN | Residential | 2.26 | 877.5M | 0 | n/a |

| Morguard North American Residential | MRG.UN | Residential | 3.56 | 745.2M | 0 | 3 |

| Morguard REIT | MRT.UN | Diversified | 4.42 | 354.9M | 0 | -75 |

| Nexus REIT | NXR.UN | Diversified | 5.14 | 710.4M | 0 | 0 |

| NorthWest Healthcare Properties | NWH.UN | Healthcare | 5.83 | 3.03B | 0 | 0 |

| Plaza Retail REIT | PLZ.UN | Retail | 5.81 | 449.8M | 0 | 1.5 |

| Pro REIT | PRV.UN | Diversified | 6.66 | 404.8M | 0 | 0 |

| RioCan REIT | REI.UN | Retail | 3.86 | 7.44B | 0 | -29.2 |

| Slate Grocery REIT | SGR.UN | Retail | 5.65 | 717.8M | 0 | 1.8 |

| Slate Office REIT | SOT.UN | Office | 7.95 | 403.6M | 0 | -47.2 |

| SmartCentres REIT | SRU.UN | Retail | 5.44 | 4.47B | 0 | 2.2 |

| Summit Industrial Income REIT | SMU.UN | Industrial | 2.42 | 3.9B | 5 | 2 |

| True North Commercial REIT | TNT.UN | Diversified | 8.28 | 652.8M | 0 | 0 |

I think dividend investors should not use yield as the key indicator for determining whether to invest in a stock or not, especially when it comes to REITs. It is important to invest in REITs with larger market caps since that usually means a larger portfolio holding, more real estate assets under management, and normally results in better overall asset diversification.

From a segment point of view, the 38 REITs are broken down as below:

- 3 Industrial REITs

- 2 Healthcare REITs

- 1 Hotel REITs

- 3 Office REITs

- 6 Retail REITs

- 8 Residential REITs

- 15 Diversified REITs

Interestingly enough, 42% of the REITs are diversified, meaning the companies own and manage properties in different segments. This, however, shouldn’t come as a surprise since holding properties in the different segments typically means the company is less susceptible to changes in a specific segment. Investing in a specific REIT segment can mean potentially more volatility.

For example, many workers, including myself, have been working from home for the last two years, so many offices are sitting at near empty capacity. As a result, the office REIT segment has not been doing too well since the start of the global pandemic.

Interestingly, we own both Granite REIT and Dream Industrial REIT, or two out of the three Canadian REITs in the industrial segment. Industrial REITs own and manage logistics, warehouse and industrial properties. Many of these properties are in high demand due to the popularity of online shopping. In fact, many financial experts suggest that the online shopping phenomenon, already a major economic force, will grow going forward. Therefore, I remain bullish on the industrial REIT segment.

What valuation metrics to use for REITs?

Because of the way REITs are structured, we cannot just evaluate REITs by looking at the standard financial valuation metrics like net income, PE ratio, and payout ratio.

The best way to assess REITs is to use metrics like:

- Funds from operations (FFO)

- Adjusted funds from operations (AFFO)

- Price to FFO ratio

- FFO payout ratio

Think of FFO like a REIT’s earnings. This is by far the most important number for REITs. As an investor, you want to see a growing FFO over time.

AFFO is like adjusted earnings. This allows REITs to offset any one-time expenses and provide a true picture of how much money the REIT is making. In other words, you can consider AFFO as free cash flow.

The price to FFO ratio is essentially like the PE ratio. It gives you an idea of how expensive the REIT is relative to other REITs. In the same way that you should not compare PE ratios between different economic sectors (i.e. Canadian Banks vs. high tech), it is best to compare the price to FFO ratio of REITs in the same segment.

FFO payout ratio gives investors an idea of what percentage of the REIT’s income after expenses are paid out in distributions. Each REIT typically sets an FFO payout ratio range target. Monitoring the FFO payout ratio can give investors an idea of whether or not the distributions are safe.

Remember, REITs typically distribute 80 to 95% of their income after expenses to shareholders. So if the FFO payout ratio is below 80%, there’s a good chance the REIT will increase the payout. If the FFO payout ratio is close or above 95%, there’s a good chance a cut may be coming.

Please note, it may not be possible to find these valuation metrics on sites like Google Finance, Yahoo Finance, or Morningstar. However, REITs will disclose these metrics in their quarterly and annual reports. In other words, one must search quarterly and annual reports and learn how to read them.

Other factors to consider

In addition to the valuation metrics mentioned, investors also need to consider other factors when it comes to picking out the best Canadian REITs.

For example, since REITs generate income by collecting rents from tenants, occupancy rate and rent collection rate are both important factors to examine. I certainly wouldn’t want to invest in a REIT that has an above 5% yield but has both occupancy rate and rent collect rate in the 80% range.

It is also important to go through the financial reports and understand the key tenants and tenant base. Generally speaking, you want to invest in REITs with a diverse tenant base or one with strong ‘anchor tenants.”

For example, you want to have some big name tenants that wouldn’t close down a store after a short period of time. These big name tenants typically bring high foot traffic to the area, which is beneficial for other retail stores. Big retail names like Home Depot, Walmart, Superstore, and Costco, can all be considered as anchor tenants.

I also like to go through a REIT’s portfolio and see if there are properties near me that I know of. I then use my “be an owner approach” to evaluate the REIT. Take RioCan for example, I have been to three RioCan managed retail locations in Metro Vancouver and all three retail locations. I have observed that all three locations have high shopper traffic and all the stores are occupied with some major retail names like Home Depot, SportsChek, Indigo, and Mark’s.

Best Canadian REITs for 2024

Below are my pick for the 5 best Canadian REITs based on the metrics and factors outlined above. Please note, I’m not a professional financial advisor so take these as suggestions. Always do your own research before buying and selling any stocks.

1. Allied Properties REIT (AP.UN)

The office REIT segment has had a lot of challenges throughout the global pandemic. However, I believe Allied Properties is well positioned for a strong comeback.

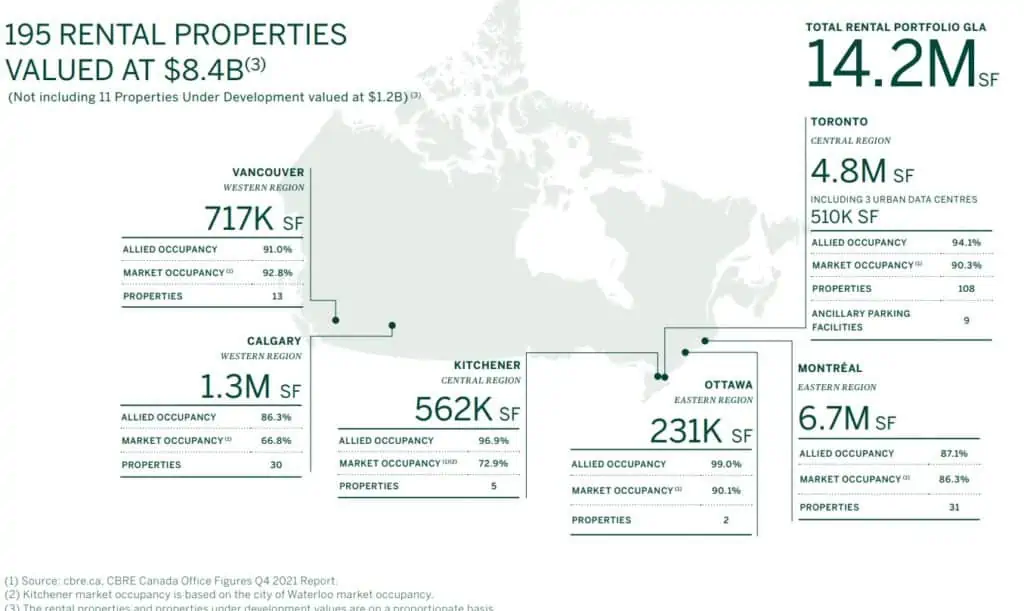

Allied Properties, unlike many Canadian office REITs, did not cut its distribution over the last two years. Instead, the company increased its dividend payout by 3.1%. This is largely due to having office properties in key Canadian cities. Allied Properties has 195 rental properties valued at $8.4B with 14.2M square feet of gross leasable area. In addition, it has 11 properties under development valued at $1.2B.

As you can see from below, all of AP.UN’s properties are located in major Canadian cities with the majority of the properties located in Toronto and Montreal.

- Sector: Office REIT

- Dividend Yield: 3.83%

- FFO Dividend Payout Ratio: 70.6%

- 5 Year Dividend Growth Rate: 2.5%

- Dividend Increase Streak: 10 years

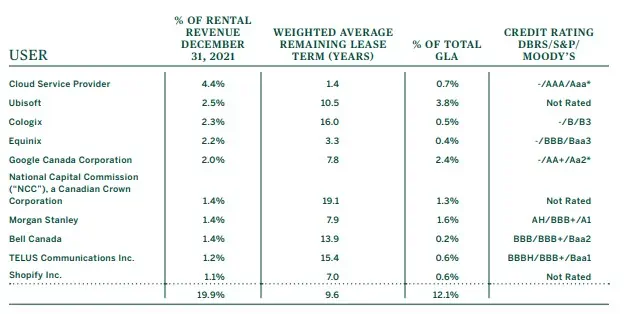

What I particularly like about Allied Properties is the occupancy rate is higher than the market occupancy rate (with the exception of Vancouver). I also like that the top 10 tenants are all well known companies. Best of all, no tenant makes up more than 4.5% of the rental revenue.

Although how we work has changed due to the pandemic, companies will continue to need office spaces. Many meetings are simply more efficient and effective when done face to face. This was probably one of the many reasons why Bruce Flatt, the highly respected CEO of Brookfield Asset Management, argued strongly that the pre-pandemic office environment will return.

By having properties in urban centres and continuing to develop and update these properties, I believe Allied Properties will continue to grow in the future.

2. Granite REIT (GRT.UN)

Granite REIT is a Canadian-based real estate investment trust engaged in the acquisition, development, ownership management of logistics, warehouse and industrial properties in North America and Europe.

- Sector: Industrial REIT

- Dividend Yield: 3.08%

- FFO payout ratio: 76%

- 5 Year Dividend Growth Rate: 4.4%

- Dividend Increase Streak: 11 years

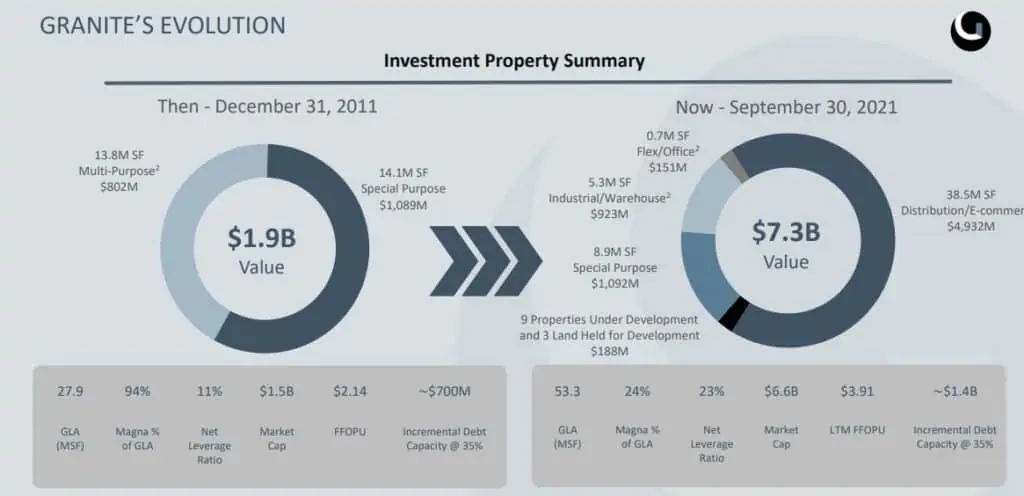

GRT.UN’s portfolio consists of 118 investment properties representing almost 51.3 million square feet of leasable area with an occupancy rate of 99.6%. These numbers are very impressive for a REIT. I have come to really like Granite REIT for its global footprint as well as its focus on institutional-quality assets in key distribution and e-commerce markets.

As you can see from below, Granite REIT has grown by $5B in value in the last ten years. With the popularity of online shopping and online retailers like Amazon and Wayfair needing logistics and warehouses in major cities to store merchandise, I believe Granite REIT will continue to grow.

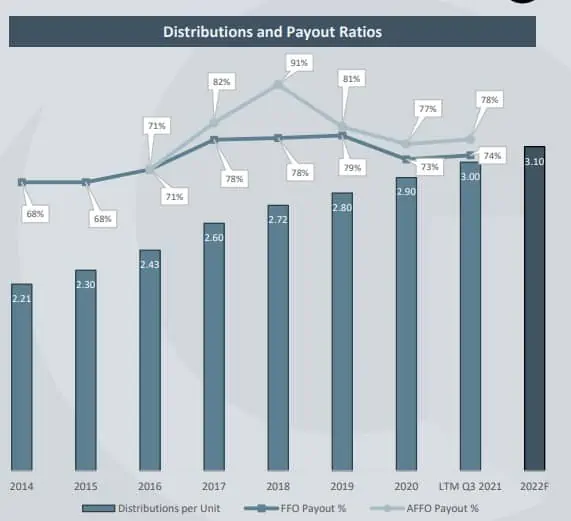

Granite REIT has a dividend increase streak of 11 years with a 5 year DGR of 4.4% and a 10 year DGR of 14.3%. Given the relatively low FFO to payout ratio, I believe Granite REIT will be able to continue raising its dividend payouts for many years to come.

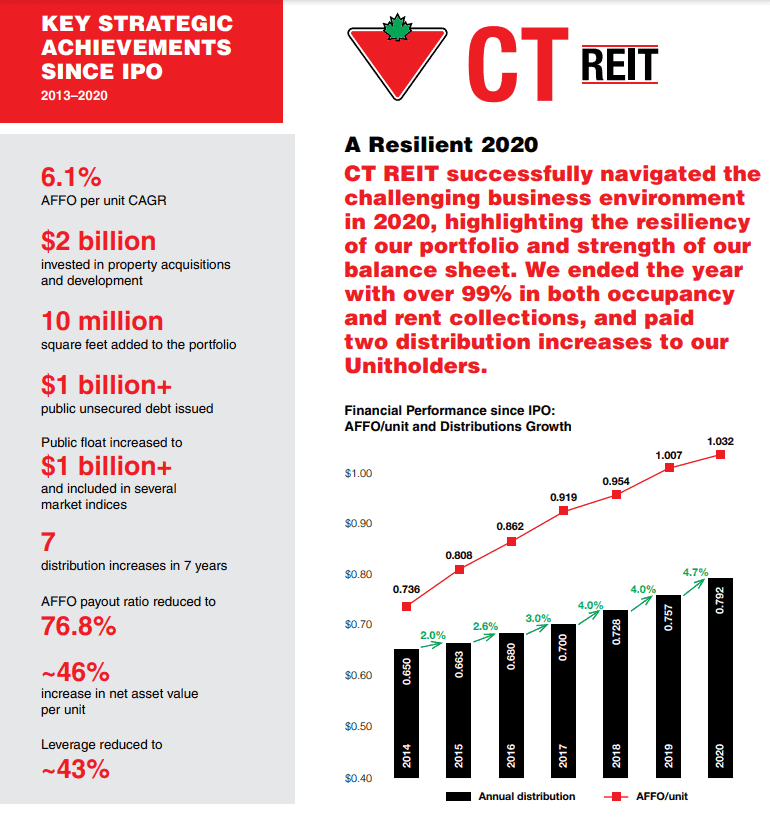

3. CT REIT (CRT.UN)

CT REIT owns a Canada-wide portfolio of high quality assets leased primarily to Canadian Tire Corporation with annual rental growth built into long term leases. This relationship is very unique because it gives CT REIT insight into Canadian Tire Corp’s long term plans and allows CT REIT to shape its strategy and plans accordingly.

This tightly knitted relationship also means CT REIT has been able to successfully navigate the challenges the COVID-19 pandemic has caused. CT REIT ended 2020 with over 99% in both occupancy and rent collections and managed to come through with two distribution increases for shareholders. Considering many REITs were forced to cut dividends through the pandemic, this was a very impressive feat.

- Sector: Retail REIT

- Dividend Yield: 4.86%

- FFO Dividend Payout Ratio: 73.8%

- 5 Year Dividend Growth Rate: 3.9%

- Dividend Increase Streak: 9 years

As of September 30, 2021 CT REIT had 986,000 square feet of gross leasable area under development, of which approximately 96% is subject to committed lease agreement. This is an improvement of 1% on committed lease agreement compared to the previous quarter.

At the same time, the company also announced nine new investments. When completed, they are expected to represent approximately 449,000 square feet of incremental gross leasable area and earn a weighted average cap rate of 6.31%.

CT REIT is continuing to expand. The unique relationship with Canadian Tire means CT REIT will benefit from Canadian Tire’s corporate expansions.

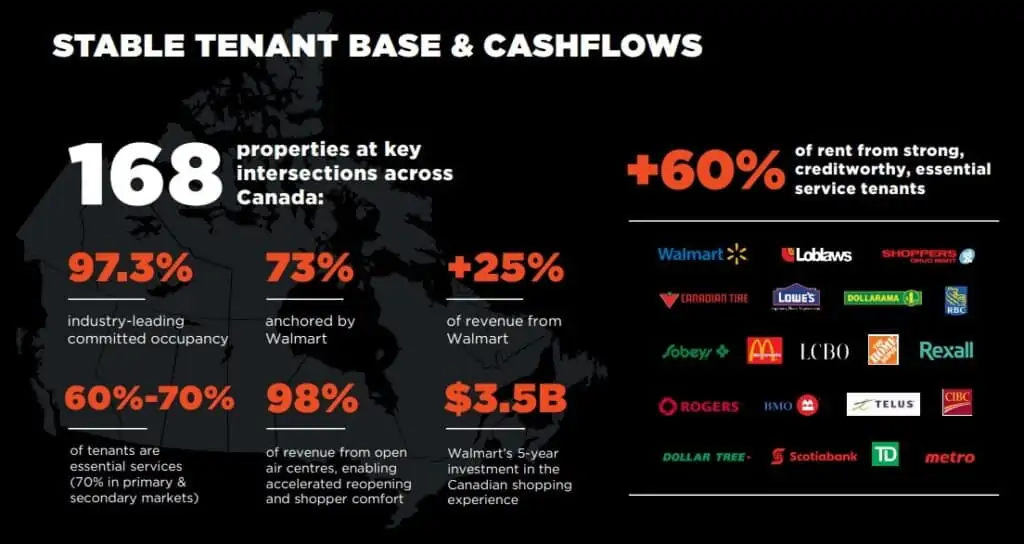

4. SmartCentre REIT (SRU.UN)

SmartCentres REIT is one of Canada’s largest fully integrated REITs, with a portfolio featuring 168 strategically located properties in communities across the country. The company has $10 billion in assets and owns 34.2 million square feet of income producing value-oriented retail space with an industry-leading occupancy rate of 97.3%, on 3,500 acres of owned land across Canada.

Unlike some of its peers in the retail REIT segment, SmartCentre REIT kept its dividend payout throughout the pandemic and did not cut its distributions. This shows SmartCentre has a good tenant base that continues to pay rents despite the hard time encountered through the global pandemic.

- Sector: Retail REIT

- Dividend Yield: 5.44%

- FFO Payout Ratio: 84.6%

- 5 Year Dividend Growth Rate: 2.8%

- Dividend Increase Streak: 7 years

Walmart is a big tenant for SmartCentre REIT with 73% of its properties anchored by Walmart and more than 25% of revenue coming from Walmart. The nice thing about being anchored by Walmart is that Walmart provides a lot of stability. When was the last time you saw a Walmart store closing? It is very rare for a Walmart store to close. Usually, once a Walmart location is opened, it stays at the same location for a very long time. Furthermore, Walmart acts as an “anchor” by increasing foot traffic to other retail outlets located in the same mall.

SmartCentre does not have the highest dividend growth rate but this is more than compensated by the higher than normal initial yield. If you like the retail REIT segment, SmartCentre REIT is a great choice.

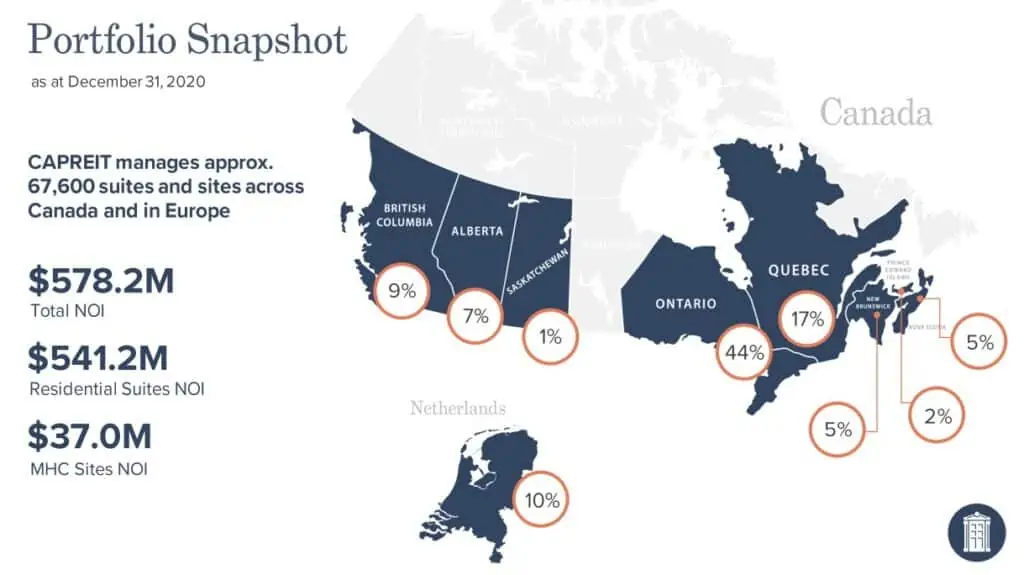

5. Canadian Apartment REIT (CAR.UN)

To keep my list of Best Canadian REITs diversified, I thought it would make sense to pick a residential REIT. When it comes to the residential REIT segment, Canadian Apartment REIT is the largest REIT in the segment with a market cap of almost $10B. In comparison, the second largest Canadian REIT in the residential segment has a market cap of $2.59B.

As of December 31, 2021, Canadian Apartment REIT manages approximately 67,600 suites and sites across Canada and Europe.

Across Canada, Canadian Apartment REIT has seen an increase in occupancy rates in all the provinces. The company saw a slight decrease in occupancy rate from 98.4% in 2020 to 98.2% in the Netherlands. The increasing occupancy rate across the different regions is a great sign for the shareholders.

Overall, the company has an occupancy rate of 97.9% across all of its properties, which is a solid occupancy rate for residential REITs.

- Sector: Residential REIT

- Dividend Yield: 2.68%

- FFO Dividend Payout Ratio: 61.6%

- 5 Year Dividend Growth Rate: 2.6%

- Dividend Increase Streak: 10 years

Although both the initial dividend yield and 5 year DGR are not very high, I like Canadian Apartment REIT’s solid track record and its well diversified asset portfolio, as well as the fact that rental residential spaces will continue to be scarce, and likely to become even more so, especially in large urban areas.

Best Canadian REITs – Final Thoughts

It was interesting to go through the 38 Canadian REITs and pick out 5 for my best Canadian REIT list. I continue to like Canadian REITs as a way to invest in real estate rather than actually buying and managing properties ourselves.

It is important not to only look at dividend yields when it comes to determining which REIT to invest in. There are many financial metrics and factors you may not be able to find on the typical stock research sites. Therefore, it is very important to go through the quarterly and financial reports of the companies themselves. It is also important to go through the investor presentations to understand how the business is doing.

Looking for more information? Below are some articles that you might find useful:

- Want to track your portfolio? Take a look at my Google Spreadsheet Dividend Portfolio Template.

- Best Canadian dividend stocks

- Which discount broker should you use? Check out my Questrade vs. Wealthsimple Trade review.

- Geographically diversify your portfolio via one of the low cost ex-Canada ETFs like XAW.

If you don’t want to hold individual REITs, you might want to take a look at one of the Best Canadian REIT ETFs instead.

Are you looking to re-balance your portfolio regularly, regardless of whether you hold index ETFs or dividend paying stocks? Some smart folks created Passiv to do that for you automatically. With Passiv, the tool can put your portfolio on autopilot. You can build your own personalized index, invest, and rebalance all through a click of a button. Passiv can even calculate and execute the trades needed to keep your portfolio balanced. Essentially, Passive makes investing super simple! A community user account is free to sign up. The elite member account is $99 per year…but it’s free for Questrade clients! Make sure to check out Passiv.

Note: This blog post represents my opinion and not advice/recommendation to purchase these stocks. Before you buy any stocks, please consult with a qualified financial planner.

Hi Bob,

Thank you so much for the information! I believe I have read that you invest in Canadian REITs in a TFSA rather than an RRSP for tax reasons, is that correct? Not sure if I am understanding why holding them in RRSPs would not be as advantageous? Or have I completely misinterpreted? Thanks as always!

Hi Stevey,

We used to invest Canadian REITs in both TFSA and RRSP, now only TFSA. TFSA is tax free where as RRSP is tax deferred. This means when you withdraw from TFSA, everything is tax free and with RRSP you have to pay taxes upon withdraw. Hope this helps.

RioCan REIT REI.UN

what’s your opinion o it?

Used to own it but closed our position due to dividends not back to the pre-pandemic level yet.

One of the larger more popular names. With the interest rates rising and developments such as this (REITS ) heavily dependent on interest rates, you may have to wait and be patient before the ship corrects itself. The tide is out right now. Real estate as in any commodity, or service has its cycles. Generally real estate is inversly proportional to interest rates. Keep that in mind. It is expensive, and in good times it will grow. May be a good value at 20% less it’s current market value IMHO . Happy investing. Seek Safe Harbour . James V

I invests in a private Reit Skylineliving. It’s been voted best rental provider in Canada 2023, one of best managed company as well. Dividends are great with a diverse portfolio.

No need to buy REITS if you own the banks ( which any dividend investor will), they own all the property anyway.

I guess that’s one way to see it. 🙂

REITs are a finicky group and you definitely have to be on your toes, more than other investments.

I hold SmartCentresREIT and RioCan. I wouldn’t mind some industrial reit exposure at some point. Yet I’ll never allocate a sizeable portion of REITS to my portfolio. I just don’t trust the ROC component which can be quite drastic over time.

Again – not a big deal if held in TFSA/RRSP etc., otherwise you run the risk of a larger than expected capital gain (or smaller capital loss) in non-reg. accounts.

I like the industrial space as well… but expensive right now ( very much in fashion over the past 2 year s) – they will come off eventually as the market seeks lower levels in pace with Canadian economy . The Canadian economy is in dire trouble . Watch what happens if the prime rate goes to 6% , as the BOC wants it !

I might just target other sectors for now, we have lots of opportunities coming our way. It certainly seems like it’s going to get worse before it gets better.

I’ll take little bites when I’m ready (energy/financial/telcom etc.).

Great article. I had a question that I wondered if someone had some thoughts on.

I notice that many of these REIT’s dividends are comprised of Return of Capital (ROC). On one hand, I could consider that as positive as it provides preferential Cdn text treatment. On the other hand, if its just artificially propping up their dividend payment, then I should be concerned.

Since it seems common across the REITs, I wonder whether there is some fundamental reason they are doing this. I.e. when they trade properties and take gains, do they take these gains and flow them through as ROC i.e. its actual value that they are distributing vs “an artificial propped up dividend” by returning your book value.

Welcome thoughts on this.

On ROC for REITs… ROC typically happens when a REIT’s distribution exceeds its taxable income. In other words, REITs can be selling assets and realizing a profit, then distributing this profit to shareholders. Since some REITs changes their portfolio and structures, ROC does and can happen. If there’s a high amount of ROC in the dividends, you may want to take a closer look at the quarterly reports to understand what’s causing this.

Have you ever taken a look at Real Estate & E-Commerce Split Corp. (RS) from Middlefield? What do you think?

No I have not. I typically don’t take a look at slip corp shares since the slipt corp structure is very strange IMO.

A look inside: Top 10

Crombie Real Estate Investment Trust

CT Real Estate Investment Trust

Dream Industrial REIT

Granite REIT

H&R Real Estate Investment Trust

Killam Apartment REIT

Northwest Healthcare Properties REIT

Riocan REIT

SmartCentres REIT

Summit Industrial Income REIT

As a German investor, I would be interested in your assessment of the quality of the split shares. I think you have the overview. Greetings Heiko

Thanks for the suggestion on split shares/coprs. Will see if I can write an article on that topic.

Hi – great article covering REITs! I was if the main advantage of REITs is based on its dividends or if it’s based on its appreciation?

Also, do REITs generally disclose any exit strategies for their holdings (I’d assume they do it through quarterly filings)?

I like having exposure to some concrete real estate but don’t know how REITs so I mostly buy into syndications where they generally are very explicit with an exit strategy (so I can estimate appreciation) while capturing some cash flow (after they take a year or 2 to stabilize a property). My main preference with syndications over REITs is that most syndications will publish a PPM that’s very detailed and good to read and analyze (and the analysis can help you see how good/bad the operator is). Whereas with REITs, I feel like it is a black box where I am not too sure what’s going on.

But I guess the main risk with syndications is they’re generally smaller funds so you get less diversification, and it’s a bit riskier because if you read the numbers incorrectly you could be investing in a very bad fund.

Angie , some REITS are good investments with capital increases over time and increases in unit payment to holders too , and some conglomerates as well – as some hold a lot of realestate … ( Blackstone and the like). Its always ‘buyer beware’ though . If ever in doubt of what a REIT is doing phone their IR – Investor relations department . I have found IR department very good at what they do , in general . they will even forward you a Power Point production of their next steps and the like …. Good luck with your investments . J .

Just to add, you can find a lot of the info you’re looking for on the investor presentation or quarterly and annual reports.

Bob thank you so much for this great article.

I hold SRU from your list but I also hold DIR and NWH , I know they’re not on your list but I like to hear your opinion on them.

Thanks

We hold DIR.UN in our portfolio although only a few shares. NWH is also pretty solid I think but haven’t really done too much research.

Great list and excellent insights as usual. One additional point is to determine the allocation of the dividend across return of capital, capital gains and especially OTHER INCOME that is taxed at the highest rate.

Thanks Bruce, good additional point.

Usually I am in accord with your general philosophy but I find the lack of dividend growth is a major problem. I bought crr.un and chp.un several years ago because of the yield and accepted the fact there would be no dividend growth…but the high yield compensated at that time.

I still have them and the yield on cost is good.

I had to sell HR.UN when they cut their dividend and replaced it with a solid Canadian dividend growing stock with a lower yield.

I hold 41 stocks, 16 are U.S. in sectors Canada does not cover well so I am diversified with good dividend growers with no emphasis on REITs.

The fact that REITs are not taxed favorably in Canada deepens my conviction.

Enjoy your viewpoint.

Gary Lowe

Thanks Gary for your view point. REITs don’t typically have as high dividend growth but do offer higher initial yield. As mentioned, you’re better off holding REITs in TFSA or RRSP.

Gary – great point about REITS not betted well, in non-registered Accounts has a great point. I typically have the same philosophy as you, I do reserve 10% of my portfolio for higher dividend real estate investment trust ( Bought smart REIT at ~ 12.25 in May 2020 ) and a few select business development corporations (BDC’s).

can you recommend a reit etf ?

That’s an article I plan to write in the future. 🙂

I like and have RIT . BUT not at these levels . I would enter at a lower level during a Market correction on a couple weeks . .

Good group of REITS . I own the same core group . Plus I have added two that are in a change-mode that look very positive and have good financials . One being AX.UN and the other Being HR.UN . Both are a minor portion on my REIT collection, but have Bright outlooks given the high market DOW/TSX right now. But nonetheless I thought I would mention it to the group. Thanks for your thoughtful articles as always.

We used to own HR.UN but decided to close out the position due to its high concentration of offices.

Correct, they are more or less concentrating on industrials and other now. They have reformulated the company and have spun out a lot of their non-key core real estate. So it’s basically a recreated company.

Yup, I see they’ve restructured after we closed out our position. 🙂