I was talking with a good friend of mine the other day about work, money, and life. Due to the professions he and his wife are in, they both work long hours. He mentioned that he worked 6 days straight and his wife worked 7 days straight the past week and they often don’t see each other for days. I could tell that he was not enjoying this type of working arrangement and wanted to step back a bit.

“How much do you need to retire at age 45?” My friend asked.

“Is a million dollars enough? Two? Three? How much is enough?”

Contrary to popular belief, I don’t think the how much question can be answered by a set dollar amount in your bank account. As J. Money ingeniously stated, the most important factor determining your “number” is your SPENDING. A family spending $20,000 per year will certainly not need as much money to sustain similar lifestyle in retirement compared to a family spending $150,000 per year.

While I have calculated that we can reach financial independent in about 10 – 15 years based on The Early Retirement / Financial Independence Spreadsheet, it doesn’t tell me exactly how much money we need in our bank account (or rather, our investment portfolio) to retire early. So I decided to run some projections based on our spending from the last few years.

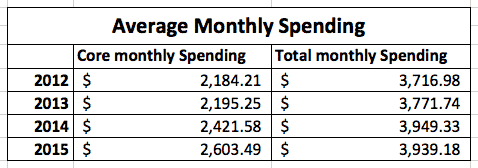

Since mid-2011, we have been tracking all of our expenses via a spreadsheet that we created. Below are our monthly core spending and total spending averages (2011 is not included because we didn’t have numbers for the full year). Some explanations first… By core spending I mean housing expenses, utilities, food, insurance, gas and other essential expenses. Expenses like donations, eating out, entertainment, educational courses, vacations, and some one time big items like a baby stroller have been excluded from core spending. I consider these expenses discretionary spending. We can probably reduce the number of vacations or how much we eat out in order to cut back on these discretionary expenses. But we spend money on these discretionary expenses as a way to enjoy our lives. I don’t believe you can enjoy life fully with extreme saving methods like eating ramen noodles every single day, or avoiding vacations by never setting foot outside of your home. Yes you can definitely save a lot of money but are you enjoying your life? Life is all abut having the right balance. Anyway, as I was explaining, the total spending amount includes these discretionary expenses. As you may know from my recent interview with Mr. 1500, I am a part time photographer and Mrs. T and I are operating a cookbook business. Mrs. T also has other business projects that she’s working on. Since some of these expenses are one time occurrences and the amounts are different each time, to keep things simple, we have excluded these business expenses from the total spending and track them separately.

From 2013 to 2014, our core spending have increased by 9.3%; from 2014 to 2015 the core spending increased again by 7.5%. Similarly, the total spending increased by 4.7% from 2013 to 2014 but stayed about the same from 2014 to 2015. The monthly core spending increase over the last couple of years can be contributed to having another person in the family, higher housing expenses when we moved from an apartment to a house, higher insurance cost, focusing on eating healthier, and some one time expenses like buying a chest freezer, LED light bulbs, and garden tools & plants. Ideally I’d like to see both our core spending and total spending monthly averages go down a bit this year. 🙂

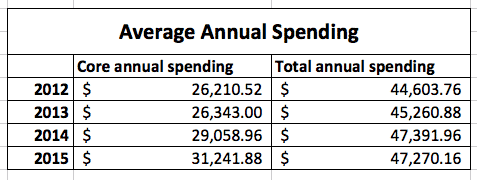

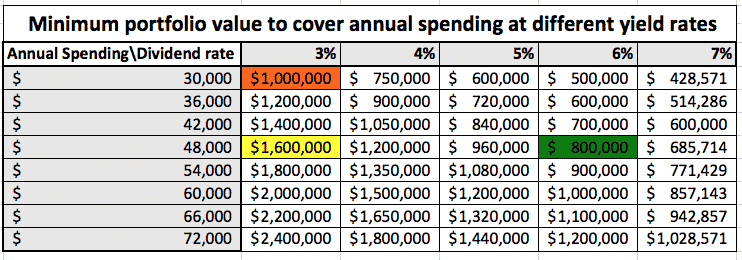

Based on these monthly average spending, our annual spending looks like this.

So an annual income of $32,000 will roughly cover our core expenses and we’ll need roughly $48,000 to cover all of our expenses, excluding business expenses. Since these two numbers are after tax amount, the actual pre-tax income needed to cover the total annual spending will be higher, depending on the income tax percentage.

What dividend portfolio value do you need to retire?

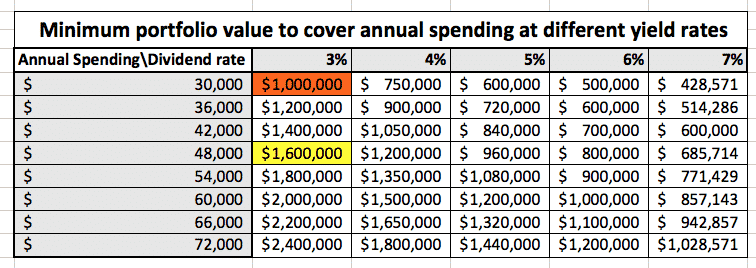

As we plan to use dividend income to cover most of our expenses once we reach early retirement (aka financial independence), let’s see how much money we need in our dividend portfolio to cover our annual spending. Below I ran a few different scenarios using different dividend yield rates.

When it comes to dividend income, one key point to note here is that dividend income is very tax efficient, as dividend income does not get taxed at the same rate as your typical working income here in Canada (US too, I’m unsure about other countries though). FrugalTrader has pointed out recently that BC does not tax anything on eligible dividend income until over $100,000, assuming the income is split between the couple. The beauty here is that, unlike earning income from a regular 9-5 job, divided income is taxed at a much lower rate. That means we only need the actual amount (i.e. $48,000) to cover all of our expenses from dividend income versus what we would need from a regular job, say with a 25% tax for example (i.e. ~$64,000).

[the_ad id=”1878″]

At a conservative dividend yield rate of 3%, we’d need $1.6 million (highlighted in yellow in table above) to cover our annual expenses of $48,000. Not going to lie, that number seems extremely big to me. But what if we look at core spending only? The portfolio needed, at 3% dividend yield, to cover our core expenses of $31,000, would reduce to about $1 million (highlighted in red in table above). That’s definitely a smaller number to aim for.

This is great, but how the heck are we suppose to save $1 million dollars?

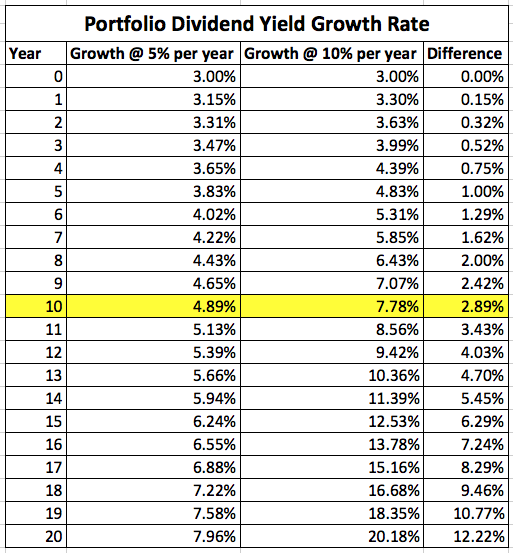

Well, here’s the reason why I love dividend growth investing. The dividend stocks that we hand-picked for our portfolio should increase the dividend payout each year. Solid dividend stocks like Johnson & Johnson, Target, Wal-Mart, have increased dividend payout for over 40 years. Our dividend portfolio may only yield at 3% today, this number should increase as demonstrated below.

As you can see from the table below, if our portfolio dividend payout grows at a 5% rate per year, the yield on cost will be 4.887% in 10 years; if our portfolio dividend payout grows at 10% rate each year, the yield on cost will be 7.781% in 10 years. The power of compound interest takes off as time goes by. Notice that the percentage difference between the two growth models becomes very significant after year 12. Can you imagine 20 years from now having a dividend portfolio with a 20% yield? Wow! This is without having to touch the principal at all. Furthermore, the yield on cost will continue to grow each year as long as the dividend stocks raise their dividend payout. Pretty amazing stuff if you think about it.

Since Rome wasn’t built in one day, neither will your dividend portfolio. If you build your dividend portfolio over time and allow the dividend payout to grow, I believe a 6% dividend yield is not unlikely in 10 years time. This is one of the reasons why we’re focusing on high growth dividend stocks nowadays whenever we buy a dividend stock. Given a yield on cost of 6% for our dividend portfolio 10 years from now, we’d only need $800,000 (highlighted in green below) to cover our $48,000 annual spending. This is significantly lower than the original $1.6 million estimate earlier – a $800,000 or a 50% difference! At this point we can call ourselves financial independent. The dividend income will sustain our expenses. We don’t need to sell any stocks to pay for our expenses. In other words, there’s no need to consider what withdraw rate to use in retirement. Furthermore, the dividend income should continue to grow, as dividend paying companies in our portfolio continue to raise their dividend payouts. In the ideal situation, we would never need to sell any stocks and just live off the dividend income. But we can always sell some stocks to cover one time expenses. Dividend growth investment strategy provides flexibility in retirement years.

What are the key lessons for dividend investors?

- You don’t need millions of dollars to retire early – no you really don’t, especially if your expenses are low. If you have no idea what your annual spendings are, it’s a great idea to start tracking it today. If your annual spending is high (i.e. in the hundred thousands range), you may want to look at the lesson below.

- Reduce & optimize your expenses – a $5 daily expense means an annual expense of $1,825. At 3% dividend yield, you’d need $60,834 in your dividend portfolio to generate enough income to cover this $5 daily expense every year. One way to reduce the core expenses is perhaps consider moving to a cheaper city. This is why Mrs. T and I are planning to travel around the world one day with our kids.

- Focus on dividend growth rather than initial yield – dividend growth rate is more important than the initial yield if your retirement timeline is 10 years or more. However, if you’re planning to retire in a year or two, perhaps you need to focus on the initial yield. When I first started investing, I definitely fell for the dividend yield rate trap. I purchased some stocks that didn’t have the fundamentals to sustain high dividend yield rate. Instead of growing dividend payout each year, some companies couldn’t grow their dividends, some even had to cut their dividends.

Based on all the numbers provided in the multiple table and your annual spending amount, can you determine the magic number that you need to reach financial independence via dividend income?

P.S. Aren’t spreadsheets awesome?

P.P.S. : As pointed out by some readers, YOC may not be 100% accurate since your new investments may not grow at the same rate as original/older investments. The key point of this article is that given the need of $48k annual dividend income to cover our expenses, we don’t need $1.6M in our dividend portfolio. Since we will investing over a long period of time, dividend growth means the actual amount of money needed to generate $48k annual dividend income will fall somewhere between $800k and $1.6M.

“But we spend money on these discretionary expenses as a way to enjoy our lives.”

Like you said, it’s all about finding balance. Sort of minimizing how much you need to spend in order to be happy. The rest, save it. Reach FI. Escape if you want.

The math is easy, finding what works for you is hard.

Thanks for sharing 🙂

Great rundown! I especially like your use of core and non-core spending. I do the same and use the 80/20 rule to keep me focused on managing the spending that is most impactful – home, transportation, health insurance (ugh), food, and taxes – while keeping budget management relatively stressfree.

Lively discussion on YOC. Both Matt and Tawcan are correct. For instance, Tawcan’s last sentence is correct “Since we will investing over a long period of time, dividend growth means the actual amount of money needed to generate $48k annual dividend income will fall somewhere between $800k and $1.6M.”.

Put it another way. Say over a period of 10 years, you’ve accumulated $1 million of stocks. The yield in your portfolio is a mixture, potentially ranging from 3% (most recent investments) to 6% (investments you bought 9, 10 years ago at 3% initial yield, but which now yields 6%). So, your dividends is going to fall somewhere between $30K to $60K..

Good points ys. The last sentence wasn’t in the original post, added in to reflect Matt’s points. 🙂

Thanks, Tawcan and Matt. When I see articles like the one below from WSJ, it reminds me of being even more committed to the goal.

“Retirement was a 20th-century invention, but it’s kind of gotten out of control,” says John Shoven, an economist at Stanford University.

Direct quote from the article below. Can’t make this stuff up!

https://www.wsj.com/articles/how-to-get-people-to-delay-retirement-1458525863

Great progress Tawcan. I agree with Matt on YOC though. I am on a similar journey as you. I moved to be DGI investor just 2 years ago from being a pure indexer for over a decade for many of the same reasons you mention on your site. I am 44, and currently generate $42K dividends on a $1.07 million portfolio of 35 stocks, so nearly 4% yield. Dividends cover 125% of our expenses already. My goal is to achieve 6% DG each year with no further contributions. I hope to grow this to nearly $75K annual dividends in 10 years with no contributions and also no withdrawals. After that, my wife and I plan to start living off dividends exclusively from my age 54 onwards. In US, if you file taxes jointly as my wife and I do, you can shield the entire dividend income at these levels to have zero taxes so all of it is spendable money.

Thank you. I woild like the article corrected so people are not misinformed.

Nice work on the portfolio by the way.

Hi Matt,

I’ve already made a note at end of the post.

Hi PMV,

Very cool, that’s awesome your dividend income is already covering expenses. At 6% DG each year, that just means your YOC will be higher than 4% in the future.

Yes, his YOC will go up, but his yield will not. Tawcan, you need to understand this. YOC has no relationship with how much money you need to save for the income you need. None. That update is still incorrect.

Congratulations on baby Two btw.

In other words, your Yield on COST may well go up – but your actual portfolio yield – will not.

I am a dividend Growth Investor, I love quality companies that are going to be around for a long time and pay juicy dividends. 🙂

That said, the conclusion of this article is exactly wrong and is an example of why the YOC can be a troublesome metric if used incorrectly, like it is here.

If you want a dividend income of $30k from a portfolio that yields 3% – you will need 1 million invested to produce that. There is no getting around this – including ‘YOC’.

All YOC calculates is the yield of THE ORIGINAL investment. It doesn’t mean you will be able to have a lower total portfolio value in order to get the yield you want. The only way to get a higher portfolio yield is to bring your portfolio yield up – which can in some cases, also increase risk.

You can’t fake math. Spreadsheets can be a great thing, but using a metric in the incorrect way can lead you and others into believing incorrect conclusions.

Frankly, I am surprised no one else has picked up on this mistake.

Tawcan, if you want a portfolio that yields $48k at 3% – you will indeed need a portfolio value of $1.6 million.

Hi Matt,

I see your point but the point I’m making is that portfolio yield will increase over time if the dividend stocks that you own continue increasing their dividend payout over time. Yes the new purchases you make may not be yielding at 6% but over time they may.

I don’t think you understand what I am saying. I am saying $800k will NOT give you a yield of a 1.6 million portfolio because of Yield on Cost. Your conclusion is incorrect.

Yield on Cost is a backward looking metric – it doesn’t magically make your total investments worth more than they are. an 800,000 portfolio built over 20 years is worth exactly the same as an 800,000 portfolio that you built from lottery winning that you invested yesterday. Absolutely no difference. You are using YOC to make incorrect conclusions.

What an escalating YOC WILL do for you is lessen how much you need to save over the years to get that portfolio value that you need.

I hope you understand what I am saying. You need to correct your article as it is misinforming people about how much they need to have for retirement.

Matt

I agree, I think he’s making the assumption that dividend yields will continue to grow. You have to assume a ceiling at some point. There’s no way Walmart will grow their dividend to 20% or even 5% or 6%. Stocks with those dividend yields are have them for a reason – you’re trading risk for yield.

Determining how much you need to retire really needs to be modelled using something like one of the Monte Carlo simulators in https://www.caniretireyet.com/the-3-best-free-retirement-calculators/

Even these tools have their deficiencies, so don’t blindly accept the results.

Please don’t misunderstand what I am saying. Dividend Growth investing is what I do. I think it is wise to choose high quality companies that pay sustainable, growing dividends. It just doesn’t change how much you need to have – to live off of dividends. Look up the payouts of the dividend champions, compound growth of the dividend with reinvestment is an amazing thing.

YOC simply doesn’t change how much you need to have in your account to have the yield in $$ that you want. $1.6 million is $1.6 million. $800k, is $800k , YOC simply doesn’t affect the calculation of the amount needed for retirement. It is a dangerous metric as you can see from the incorrect conclusions drawn in this article.

A rising YOC will lessen how much you need to SAVE to get to your retirement goal but has absolutely nothing to do with how much capital you need to generate the yield you want at retirement.

This is 100% factually incorrect Tawcan

“Given a yield on cost of 6% for our dividend portfolio 10 years from now, we’d only need $800,000 (highlighted in green below) to cover our $48,000 annual spending. ”

You WILL need 1.6 million for $48,000 annual spending at your stated yield.

New follower to the site and I’m always eager to read more about retirement income strategies since its really under-investigated.

Now, you talk about favourable taxation of Canadian dividends and then then later say ” Solid dividend stocks like Johnson & Johnson, Target, Wal-Mart, have increased dividend payout for over 40 years.” – but those are not Canadian stocks and will not be issuing eligible dividends, right?

I’ve been searching for more information on what qualifies and it seems pretty hard to find out. For example, will a TSX listed ETF that invests in US dividend stocks issue eligible dividends? I would think it wouldn’t but can find no definitive answer. Likewise with Canadian stocks with major offshore holdings -its unclear to me.

This might be a good topic for a post in the future.

Another point, you talk about living off dividends during retirement. Are you planning to have no RRSP income and all investments would be in taxable accounts? Because withdrawals from RRSPs whether based on dividend income or not will count as regular income.

Hi Matt,

Very good points, let me see if I can answer your questions.

I listed J&J, Target, and Wal-Mart because people know these companies better. I suppose I can listed RY and TD instead. US dividend stocks do not issue eligible dividends but us Canadians do we foreign tax credits.

On TSX listed EFT that invests in US dividend stocks, I think VGG would fall under this category. However I don’t believe it’s considered eligible dividends. Not a tax expert myself but I don’t think it’s possible to do.

We plan to slowly withdraw RRSP once we reach financial independence. Maybe $2000 or so in-kind transfer per year and put the stock(s) to TFSA or regular accounts. Our “active” incomes should be pretty minimum in that time phrase so the RRSP withdraw penalty should be very low.

Hope this helps. Thanks for the follow!

Mark says he’s not a fan of YOC, but that’s really what this topic is about. YOC is the total of the money you’ve invested over time and the reinvested dividends. Each time one adds funds your YOC changes, hopefully it will rise. As you said, if the companies increase the dividend than your yield will raise, but not on a straight line as your chart shows, because one has not invested the total in a lump sum.

Having said that, your YOC will go up over time (and the longer the better) and easily be double the the current yield if one has 10 to 15 years. So 6% on your YOC is very obtainable and one will be able to retire on a lessor amount than the lump sum projections.

Just ask any retired DG investors who have followed the strategy for years.

It’s good to hear that my 6% YOC is very obtainable. Better to be conservative when it comes to estimated projections. 🙂

Tawcan,

Great article there, and I do love the spreadsheets. It is great to see all those numbers and be able to visualize the progress. I was in the same boat as you, targeting higher yield, but now my game plan is to look for growth in the yield itself. There is a happy medium to be sure, but my time frame is 10-20 years, not 5 so I can plan for that.

Nice job,

Gremlin

Hi Gremlin,

Thanks. Spreadsheets are awesome aren’t they? Growth is very important but finding a happy medium between growth and high yield is just as important. 🙂

Hi Tawcan,

You make some good points and the main one being your spending. Your spending is the main number you need to know in order to figure out what you will need in retirement. I’m trying to get my spending down now and it’s tough. I’m just going to have to work harder and invest more to try to cover my expenses. Keep up the good work!

Hi allaboutinterest,

Spending is a major contributor in your FIRE formula. Cutting down spending can be tough but look at areas that you can minimize or optimize. Good luck!

Now i have a dream – to travel to india in 30 days and i need to raise $800 with no time and i think how to get them

That’s great to have a dream Sharon.

Good article Tawcan.

Dividends are very, very good for retirees in Australia. With a $70 dividend, investors get the company’s 30% tax refunded with it, so they get a $100 dividend in total – that’s the case for all investors, but retirees don’t have other income so they get the tax back on their tax returns. I really should do an article on how it works soon.

I don’t have a number in my mind, I’m 24 so $1,000,000 now will be much smaller in 40 years. $2M? $3M? I’m not sure. But I do know that we’re aiming for as big a number as possible while enjoying our life too.

The dividend/earnings growth is definitely a life lesson people should take note of. Even people moving into retirement at the age of 65 have many decades of life ahead, they should invest in good growth shares too.

Tristan

Hi Tristan,

That’s very cool that dividends are very good for retirees in Australia. Does Australia tax foreigners like me if I live in the country? It’s great that you’re so young and starting DGI this early.

Taw, your post made me realize that I am really left behind with regard to my savings and retirement. I gotta catch up and save more and more!

Hi Jayson,

Save and save. 🙂

Love the breakdown Tawcan! It is really pretty simple…if you don’t spend a lot, you don’t need as much to retire. And if you spend a lot, you better be saving because you are going to need a big nest egg!

Every time I read one of these posts detailing DG investing I get a little more tempted to try it!

Hi Thias,

Yup if your expenses are low then it’ll be easier to achieve FI for you as you’ll need less.

This is an incredibly thorough breakdown Tawcan, and yes – spreadsheets are awesome! I’ve always liked how there is no particular magic number for everyone to reach financial independence. It really is dependent on lifestyle, location, family size, spending habits, etc. That’s what makes it fascinating. It didn’t cross my mind that dividend income is tax efficient and that is definitely something I need to start looking into. Right now, the dividend income I am making is very little per year – but it is certainly something to consider for retirement flexibility.

Hi Generation YRA,

Totally, lifestyle, location, family size, and spending habits are major contributors on how much you need. This is why everyone’s number is different. You can’t just give out a number without knowing all these factors.

Thx for running a step by step numbers guide on how to define the amount you need in early retirement via DGI. Today, I index. The main reason is that the Belgian system is not so dividend efficient.

Let’s say I get 100 USD dividend from a stock, then I will get about 62 pct net on my account. OUCH…. That means getting 3pct net translates to 4,8 before taxes…

For now, this confirms my choice for indexing, at least from a tax point of view.

Some other Belgian bloggers have a different view. This is what makes the blogging world so nice…

A lot of food for thought!

Hi ambertreeleaves,

Yeah I’ve heard a few times from No More Waffles that the Belgium tax system is not very dividend efficient. Too bad about that. But is the system tax efficient with capital gains?

Capital gains are tax free after 6 months. Before that, you are taxed at 33pct, unless it is an ETF… complex rules overhere…

The rules make it that myself, NMW and many others invest in capitalizing trackers… They keep the dividend internally and by more stock. This way, we have a sort of DRIP effect without the dividend taxes.

Boy that’s certainly a very complicated tax system. 🙂

Wow! Nice post!

Always thought the famous 4% rule was too conservative as many of us can achieve better than a 10% total return in the long haul. There’s got to be a viable long term alternative between only safely cashing in on dividends and carelessly withdrawing all capital.

Your detailed presentation kind of confirms I was on the right track…I’ll still have to take some time to completely digest your numbers and compare then to ours.

And yes! Spreadsheets are truly awesome…or at least yours are!!!

Thanks 12-Minute. 4% withdraw might be conservative if you retire in your 70’s but for early retirees, the withdraw amount may need to be adjusted based on market condition. Either way I think the dividend approach is safer in the long run where you don’t touch the principal.

Interesting post and good one! I’m not a fan of the yield on cost metric since the same could be said/done for ETFs or any investment, not just dividend paying stocks.

That aside, I believe we need:

1) an investment portfolio of $1M +

2) a paid off home (therefore zero debt) +

3) our pensions (of >20+ years) to “retire on”.

Those are our magic numbers anyhow – your mileage might vary 🙂

We will consider CPP and OAS “gravy” because we intend to stop working before we can collect CPP and OAS. We won’t be old enough to collect income for either government income program. Besides, people who think they will get the max of both CPP and OAS are kidding themselves!

We hope to hit all those marks within the next 8-10 years, and it looks like we’re on our way.

Best wishes and keep up the great work!

Mark

Hi Mark,

True that yield on cost metric can be said/done for ETFs but with ETFs it’s tougher to predict what the growth rate would be as it’s a basket of stocks.

Sounds like you got your magic numbers figured out. We don’t have pensions so we definitely need to count on our investment portfolio. We consider CPP and OAs as gravy as well.

Tawcan

I realy liked your post. what I will need eventually to be financial freedom from worrying about if I will be able to pay alimony is: $270,000 in my dividend portfolio. so I’m trying to find the best companies with a better yeild and growth.

Hi divorcedff,

That just means your expenses are very low. Way to be able to keep them really low!

You’ve really hit on the Key to DG Investing. It’s the Income your portfolio generates that is what will count in the long run. Stick to solid DG stocks, avoid High Yield, cyclicals and those with short DG histories. You’ll get to your goal slowly without any hickups!

Hi cannew,

Great summary. Avoid high yield is something we need to do more. 🙂

You’ve inspired me to finally get down and figure our average monthly expenses for the past few years. I like your total and core spending. I do something similar but slightly different with total spending vs. non-debt expenses, since I’m imagining spending the same amount in retirement, but with all the debt paid off.

hi Norm,

Great to hear that I inspired you to figure out your average monthly expenses for the past few years. Hopefully that’ll keep you motivated to continue tracking moving forward as well.

Good perspective there. Does it mean that you guys are already reaching FI?

expense < passive income is the key. Sometimes it's hard to control how much you earn at your real job, but you can control the spending to give your passive a boost. :p

We’re on our way to reach FI in 10-15 years. 🙂

Cool overview, and nice to see the ball park numbers you guys are working with. Seems very much possible indeed. It really is a matter of starting to save and invest, keep going, remain focussed and continue to think critical about your spending. The rest should just take care of itself 😉

Save, investing, and keep going. It’s so simple isn’t it? 🙂

Great post! I have to (partly) contradict your third key lesson, though.

In my opinion not only the investment horizon is important but also the total amount of income being produced over this time frame. At some point in time a stock with fast growing dividends will overtake a stock with slow growing dividends but higher inital yield in terms of yield, perhaps even in said time horizon. But even at this point the total amount of income provided by the slow growing higher yielding stock will be higher.

I hope this point is understandable, since I’m not a native speaker.

Cheers,

Ruediger

Hi Rüdiger,

You’re right that the dividend growth may eventual slow down, that’s why you need a mix of high growth low yield and low growth high yield stocks in the portfolio. It’s about finding the right balance to sustain your retirement lifestyle. Another thing to consider is that your retirement expenses will probably reduce as you age, so the a slower dividend growth rate may be OK when you’re in your 70’s or 80’s.

This feels like a post you’d see on MMM’s website. Those guys are frugal (a little too much for my tastes). It is nice to see it all broken down into charts like you have for us though. Visual aids go a long way with money in my opinion.

The thing that I liked most was that you supported that being frugal was a very good idea but that you can’t walk that line forever – it needs to be breached to make sure you’re balancing your overall happiness and not just saving every penny at the expense of actually living (sorry ramen stock…).I think that people can get a little carried away with saving and forget about the living part and end up with an extreme lack of happiness. Don’t get me wrong, there are cheaper/free things to do where you can get both but I definitely don’t advocate for living only off of those things.

Anyways, thank you for another great post. I’ll stay tuned!

-Dividend Monster

Hi Dividend Monster,

Me MMM? I feel honored to be mentioned in the same sentence as MMM. 🙂

Extreme frugality is extremely hard to sustain and is probably not the best practice for long term. Life is about having a balance. As much as ramen is delicious and I totally love ramen, I can’t imagine having ramen every single day.

Like you said, it all depends on a family’s lifestyle Tawcan. For us, I need to consistently generate at least $3k per month through my business……or about $4k per month if I am a W-2 employee). That assumes we are not traveling, and mostly staying around our home town. We really like traveling though, so trips like our upcoming 2.5 months of travel raise those requirements. I believe my family is best served if we make 20% more than we need to spend, thereby providing a cushion, and are still able to live the type of lifestyle we want to live.

-Bryan

Hi Bryan,

Good to hear that you have a clear idea how much you guys need on a monthly basis to cover your lifestyle. Travel typically raises the expenses but if you’re traveling in a cheaper country, perhaps that compensates the airfare cost.

Morning TC;

As you mentioned, it is not how much you need, it is how much are you going to spend which will determine how much you need for that lifestyle.

I know a couple who have only CPP and OAS and live quite well thank you. They hunt and fish (meat on the table) and have no lust for travel. So they can easily get by on what the social security network gives them.

And then there are others, ike myself, who would like to do a bit more than sit in a rocking chair on the porch.

So I figure with my CPP (QPP), OAS and a small company pension I will still need to cough up close to $35K pretax per year. My biggest problem is I have informed my GP that I wanT to live to 200 yreas of wisdom. Not quite sure if my RRSP will get me there. But then, is that not what we had kids for?

RICARDO

Hi RICARDO,

Living off CPP and OAS is definitely possible if you provide a lot of food yourself and have no travel plans. It really depends what your expenses are. Personally we are not including CPP and OAS in our retirement calculations. I see them as a bonus. 🙂

Passing the portfolio to your kids & grand kids is always an option.