First of all, I want to apologize for posting the October dividend income update so late. While I do spend a lot of time writing new posts and replying to emails from readers, sometimes I have to pay more attention to higher priority things in life, such as Mrs. T, two growing kids, housework, my full-time job, Scouts, etc.

As I write this post, it seemed that October was a distant memory. October was a tale of seasons. The first half of the month, it was sunny and warm in Metro Vancouver. For a few days, I walked around in a t-shirt and shorts. Then the rain came and it got cold and wet quickly. However, given the drought and the forest fires, the change in weather was welcomed.

One day in late summer, Kid 1 noticed something hanging on one of our trees. Upon a closer look, it was a black hornet nest! We thought about calling the professional and getting it removed. After doing some research, we learned that the hornets would die in the winter, leaving an empty nest.

We figured we’d cut the tree branch and remove the nest when it’s cold out. Throughout October, we started noticing birds pecking away at the hornet’s nest, tearing the outer membrane apart. The nest then fell down when it was windy one day.

It seemed that nature took care of itself and solved the problem for us. 🙂

It was really neat to see the nest up close. Kid 1 even took the nest to his school for a show and tell.

In typical October fashion, we also harvested a lot of pumpkins from our backyard garden. I’m sure we’ll be having a lot of pumpkin soup, pumpkin pies, and other pumpkin food items for the rest of the fall and throughout the winter.

Last year just before Christmas, we had to put down our beloved cat, Perlemus. We still miss her dearly and the house just doesn’t seem the same without a cat (Kid 2 would cry at night from time to time, saying she misses Perlemus). One of our neighbours recently got a cat and he has been visiting us quite frequently. Both kids always got excited to see him. Perhaps we should consider getting a cat in the near future?

On a lighter note, Mrs. T has been trying vegan alternatives to eggs. We found out that aquafaba (chickpea water) could be whipped up to make fabulous meringue. I wasn’t able to differentiate between egg white meringue and aquafaba meringue.

Needless to say, these treats were very popular with both of our kids.

Dividend Income – October 2022

Back to the main topic of this post…dividend income.

In October, we received dividends from the following companies:

- Algonquin Power & Utilities (AQN.TO)

- BCE Inc (BCE.TO)

- Bank of Nova Scotia (BNS.TO)

- CIBC (CM.TO)

- Canadian Natural Resources (CNQ.TO)

- Capital Power Corp (CPX.TO)

- Dream Industrial REIT (DIR.UN)

- Granite REIT (GRT.UN)

- Coca-Cola (KO)

- RioCan REIT (REI.UN)

- SmartCentres REIT (SRU.UN)

- Telus (T.TO)

- TD (TD.TO)

- TC Energy Corp (TRP.TO)

- VICI Properties (VICI)

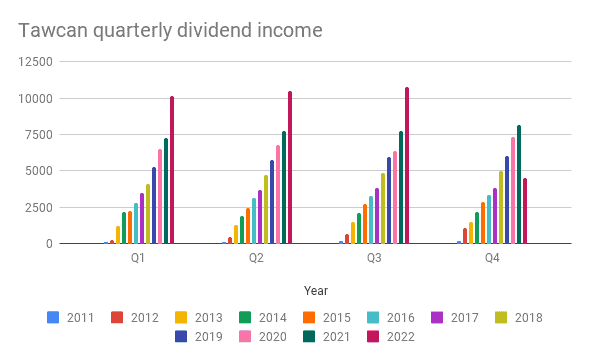

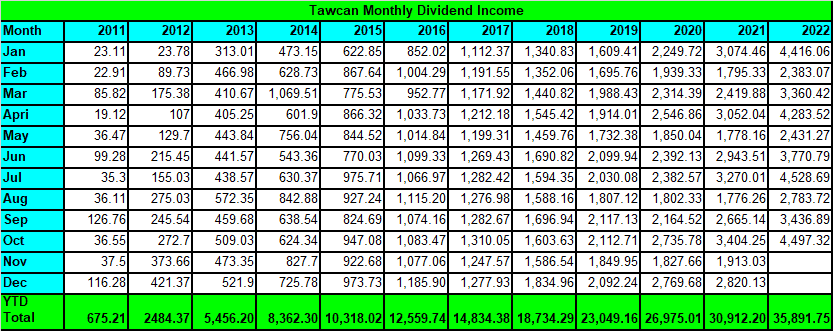

Although we only received 15 dividend pay cheques in October, the total amount added up to $4,497.32. Another fantastic month! October dividend income was the second-highest amount so far in 2022.

I was really hoping our October dividend income beat our monthly record of $4,528.69 from July. So I was slightly disappointed that we fell short of this wish.

Oh well.

The important part is I’m 100% sure we will break this monthly record by early next year.

Thanks to all the new cash we have added and organic dividend growth, we saw a 32.11% year over year (YoY) growth compared to October last year. I’m really pleased with the dramatic jump in the chart above.

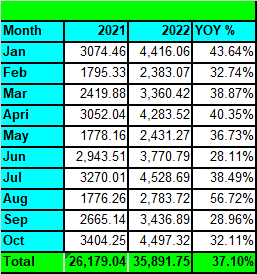

What’s even more amazing is that we are averaging a 37.10% YoY growth after 10 months. Crazy right?

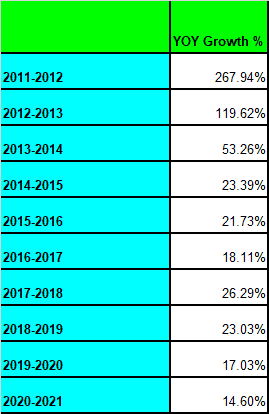

It’s very unlikely we will be able to keep up this kind of insane YoY growth in 2023. Looking at our historical YoY growth below, I’d guess that we probably will go back down to around 15% YoY dividend growth next year.

Out of the $4,497.32 received, $275 was in USD and $4,222.32 was in CAD. October was one of those months that was CAD dividend heavy.

Long time readers will remember that we do not convert USD to CAD when reporting our dividend income. This is because we want to keep the math easy and avoid fluctuations in our monthly dividend income caused by changes in the exchange rate.

The top five dividend payers in October were Algonquin Power & Utilities, TD, CIBC, BCE, and Bank of Nova Scotia (not in order). The dividends from these five payers added up to $3,197.56 and accounted for 71% of our October dividend income.

Dividend Reinvestment Plans (DRIP)

As many readers know, we try to enroll in dividend reinvestment plans whenever we’re eligible. This allows us to get additional shares either every quarter or every month. This compound effect really starts to add up once you have sizable shares, as you can drip more shares at each dividend payout.

In October we dripped the following shares:

- 37 shares of AQN.TO

- 8 shares of BCE.TO

- 9 shares of BNS.TO

- 7 shares of CM.TO

- 1 share of CNQ.TO

- 1 share of CPX.TO

- 1 share of DIR.UN

- 1 share of KO

- 2 shares of REI.UN

- 5 shares of SRU.UN

- 8 shares of T.TO

- 7 shares of TD.TO

- 5 shares of TRP.TO

- 2 shares of VICI

It’s hard to beat dripping 94 shares without paying any trading commission! By enrolling in DRIP, we immediately reinvested $3,560.07. Furthermore, because TD honours DRIP discounts, we were able to obtain shares between 1% to 5% discount of the market share price.

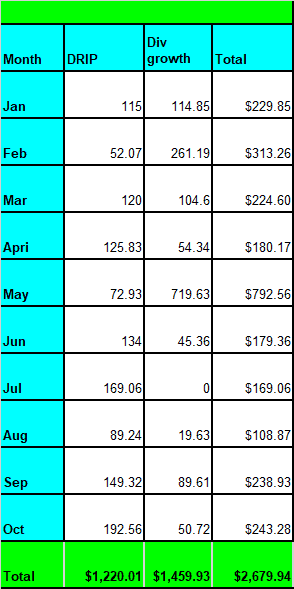

Dripping 94 shares in October added $192.56 toward our annual dividend income. At a 4% dividend yield, that’s equivalent to adding $4,814 worth of new cash.

Dividend Increases

In October, the following companies announced dividend hikes:

- McDonald’s (MCD) increased its dividend payout by 10% to $1.52 per share

- Visa (V) increased its dividend payout by 20% to $0.45 per share

- AbbVie (ABBV) increased its dividend payout by 5% to $1.48 per share

The three dividend hikes added $50.72 toward our annual dividend income. It’s not a lot of money but a raise is better than no raise at all.

In case you’re wondering, after ten months, we have grown our forward dividend income by $2,679.94 thanks to DRIP and organic dividend growth. In other words, on average, we have increased our forward dividend income by $267.99 per month.

How powerful is the ability to grow dividend income without having to do anything? Well, at a 4% dividend yield, that’s the equivalent of investing $66,998.5.

So instead of having to invest almost $67k worth of new cash to generate $2,679.94, our portfolio is doing that for us automatically. It’s like a snowball rolling down the hill, getting bigger and bigger. More importantly, when we actually do invest $67k worth of new cash, we’d generate an additional $2,700 in forward dividend income.

BOOM!

This is a perfect example of having your money working hard for you so you don’t have to.

Financial Independence Journey Update

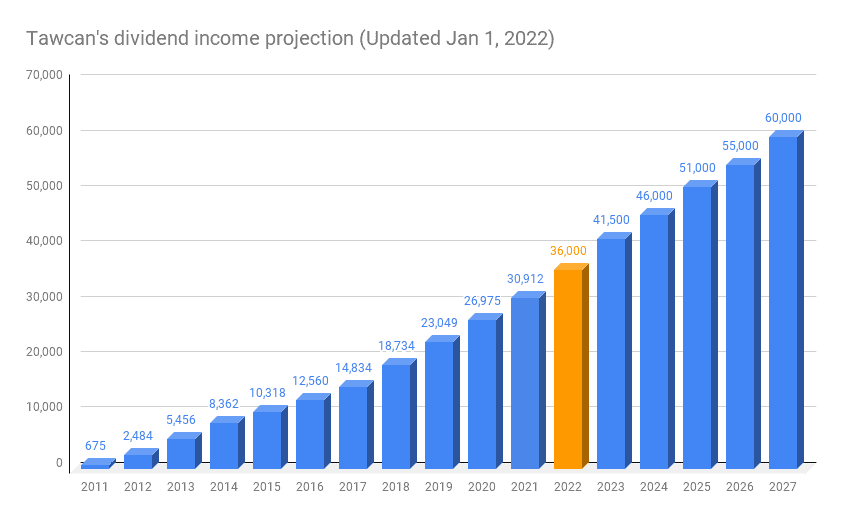

With ten months down, our dividend portfolio has generated $35,891.75 for us. It always bewilders me when I look at the chart below and how much progress we’ve made in the last 11 years.

Long term readers will know that it is our plan to live off dividends in the near future. Living off dividends, however, does not mean we won’t ever sell principal. In the early years of early retirement, living off dividends and not selling any shares should provide some margin of safety, especially when there’s a prolonged bear market. But later on, I think it’s important to consider selling some shares for either additional income or for tax efficiency/estate planning purposes.

So where are we on our financial independence journey? After ten months we have spent a total of $34,607.30 or $3,460.73 per month under our Necessities account. This means that our dividend income covered 103.7% of our essential expenses like property tax, food, house insurance, car insurance, life insurance, utilities, clothing, car gas, internet, phone, household items, etc.

One thing to keep in mind is that essential expenses do not include expenses like eating out, entertainment, charitable donation, vacation, day camps, and other so called “non-essential” expenses.

Compared to other years, we have spent a bit more so far in 2022. But this perhaps shouldn’t come as a surprise considering the higher inflation rate and two growing kids.

Historical Tawcan household spending

| Total Necessities | Necessities per month | Total Annual Spending | Total Spending per month | |

| 2012 | $26,210.52 | $2,184.21 | $44,603.76 | $3,716.98 |

| 2013 | $26,343.00 | $2,195.25 | $45,260.88 | $3,771.74 |

| 2014 | $29,058.96 | $2,421.58 | $47,391.96 | $3,949.33 |

| 2015 | $31,256.88 | $2,604.74 | $47,270.16 | $3,939.18 |

| 2016 | $29,831.40 | $2,485.95 | $47,566.96 | $3,963.91 |

| 2017 | $33,887.68 | $2,823.97 | $51,144.77 | $4,262.06 |

| 2018 | $31,840.75 | $2,653.40 | $57,231.99 | $4,769.33 |

| 2019 | $33,199.98 | $2,766.66 | $54,906.02 | $4,575.50 |

| 2020 | $35,511.60 | $2,792.33 | $48,908.74 | $4,075.73 |

| 2021 | $38,950.66 | $3,245.89 | $71,852.02 | $5,987.67 |

Do we have enough to retire in 2023? The short and simple answer is no but we’re getting pretty darn close. Work part time and slowing down a bit is certainly an option as well. Knowing that we’re getting quite close to our FI target is giving us many potential options. It’s always good to have multiple options in life. This also makes me feel a lot calmer working in a fast-paced-massive-layoffs-happen-often-high-tech environment.

Summary

It’s pretty much a guarantee that we will beat our annual dividend income goal of $36,000 in 2022. In fact, I’m pretty certain that we will end up with more than $40,000 at the end of this year The question is how much we will end up with. Can we beat our 2023 dividend income projection of $41,500?

Who knows, there might just be a chance. 🙂 If that happens, it would be pretty amazing to expedite our projection by a whole year.

To put our dividend income into perspective:

- After 304 days, our dividend portfolio generated $118.06 per day or $4.92 per hour.

- After 45 working weeks, our dividend portfolio generated an equivalent of $159.52 per day or an hourly wage of $19.94. This is $4.29 higher than BC’s minimum wage.

We continue to feel blessed and appreciative of our dividend portfolio. As Christmas is just around the corner, it is important for us to remember to help out people in need by donating to charities.

Dear readers, how was your October dividend income?

Thank you for sharing all of this. Your monthly updates on dividends convinced me to put all of our data into your spreadsheet template to track our dividends (much better than checking TD projected dividends). And this brings me to my question. When do you decide to sell stocks? We have some non-dividend IT stocks and I think we would be better off selling some of these to buy dividend stocks in other sectors to give us a more rounded portfolio and more dividends. Do you have a blog post on rules of thumb for when to sell stocks or tips on balancing your portfolio?

Thank you Karen. For the most part, when we own a dividend stock, we try to hold it for as long as possible. We don’t typically sell, but for the most part we’d consider selling if:

1. The stock price has stayed flat for the last few years

2. No dividend increase or minimum payout increase

3. Dividend cuts or suspensions

4. Dividend cuts or suspensions are anticipated because of deteriorating revenues

5. Fundamental change in the business and/or in its leadership.

You may find this post interesting – https://www.tawcan.com/dividend-investing-lessons-reviewing-every-dividend-stock-transaction-2020-2022/

Hi Tawcan,

A little over 3 years ago, I was finally able to return to stock market investing with the hopes of supplementing my projected meager pension that I will be starting in 5 years (or less). It was such a daunting task at first, picking stocks on my own. I wish I had found your info earlier but as the saying goes – better late than never! It’s been tremendously helpful that you are a kind enough person who is willing to share your results which, in turn, enables me to measure the effectiveness of my portfolio – even though it is significantly younger.

To answer your question:

My Oct was down about 18% y/y. $2K vs $2.5K (ish) (approx 14% ROI).

That being said, my very first Oct back in 2019 brought in just $800ish so I’m not going to complain (much).

I’ve also been trying to rebalance as I was very heavy on the J/A/J/O quarterlies (eg TSE:LIF) so I’m trying to spread it around more.

My question(s) back to you is(are) how much do you worry about balancing monthly/quarterly values? Should I care if my F/M/A/N returns are quite a bit lower than J/A/J/O?

Thanks again for sharing your valuable knowledge – very much appreciated!

I’d be careful being too heavy on LF as the dividend is very volatile.

I wouldn’t worry too much on the monthly/quarterly values IMO. Dividend income can get somewhat lumpy due to the dividend calendar (https://www.tawcan.com/canadian-dividend-calendar/). I’d focus on the 6 month running average instead.

By the way, great work achieving another milestone, Tawcan! I often refer your website to my friends for such amazing and inspirational works you had done. I think what you are doing will help thousands people out there. I truly believe your strategy works because I started the same strategy back in 1999. Way to go Tawcan!

Appreciate it and thank you, Stan.

Congrats on hitting these milestones! Ever since I found your website several years ago, I’ve learned a lot about dividend investing and creating passive income from dividends. Thank you very, very much for creating your awesome charts. I’ve used them as a template to track my own progress. For the first time ever, my annual dividends will cross the $30,000 mark and I’m quite thrilled about this! To date, the dividends I’ve earned in 2022 have covered 99.7% of my total expenditures, both necessities and luxuries. It’s a great feeling!

Hi Blue Lobster,

Thank you for following along on our journey. Really appreciate it. Amazing that your annual dividend income will cross the $30k mark. Congrats!

do you regret putting so much in aqn?? you got clobbered already in stock price. likely going to get hit again when they cut their dividend soon. they cant sustain it with their debt and rising interest rates. oil and gas for the win!

It sucks to be down so much but if we are to be constantly regretting with our investment decisions, we wouldn’t be very far at all. I feel that the share price already has the dividend cut anticipated. An actual cut may actually increase the share price IMO.

We shouldn’t regret of such investment decision. AQN is component of TSX 60 and it is top stock now on the BTSX portfolio because of its lucrative yield. We all made mistake along the journey and this will not exclude the legendary investor like Warren Buffet. We all did overlook on the balance sheet side of AQN. AQN senior management made terrible mistakes by stretching the balance sheet ever the years with more and more debts. It also dilute the shareholder value by issues more shares over the years. I took heavy capital loss by exiting two third of my position now. I’m not confident at all on the outlook of AQN. I think Tawcan should seriously reduce the position on AQN. There could be turnaround story but I think the turnaround is extremely slim given the fact of such terrible balance sheet.

I have now completed my first year in the stock market and it has been interesting. I jumped in when the banks were offering little more than a fraction of a per cent interest for GICs. I am glad I did. Your advice and others about investing in dividend stocks I followed and it has served me well. We will be preserving our savings with these stocks and more recently 1 year GICs with 5% returns. Having a balance with stocks and GICs give a little more safety and security. Dividend returns on investment is 8.1%. Value of investments is down 5.9% but are recovering. I am now reviewing stocks and reinvesting in stocks with dividends greater than GIC 1 year rates. I now have more than 35 Canadian stocks. Thank you for your positive perspective thru a declining market. It helped!

Hi Dianne,

A combination of dividend paying stocks and higher rate GICs is a good idea. What the right mix will depend your risk tolerance. Happy investing.

Does your monthly necessity cost include Mortgage, property tax, utilities. I find that monthly expense s amount is very low.

Yes, includes all you’ve mentioned.

So your Monthly mortgage payments, property taxes, utilities, food etc., just equates to about $2k / month 🙂 Which part of Canada are you living in? 🙂

It’s not $2k/month, more like ~$3,400 per month.

Yeah, I misread your expenses from earlier years. $3,300 makes a bit more sense 🙂 But still great job keeping your necessities down.

Thank you, we try. Having said that, that’s just the necessity cost, it doesn’t include other extra stuff like eating out, entertainment, etc.

Hi, I think you may be under calculating your necessities. A lot of other expenses which are necessities such as Home and Auto insurance, Home and auto maintenance, Auto financing/leasing, Petrol costs, Internet, Mobile, and clothing (Especially for kids) etc., when included add up to a lot more than the $3,300 that you are counting.

I reckon that essential costs for an average family (with a house payment) easily exceeds 5k per month). Add in some other non-essential (but important) costs such as dentist, organized sports, etc., can add up atleast another $500-$800.

Hi there,

Nope, all of those you’ve mentioned like home and auto insurance, home and auto maintenance, gas, internet, mobile, clothing, etc are included in our necessities, including health expenses. We have many different categories under necessities. Definitely not missing anything that we deemed “essential” to us.

Non essential expenses include things like eating out, charity donations, massages, vacations, big planned expenses, courses, etc.

Wow, your home mortgage payments must be really low then for you to keep all your essentials around $3,300. Plus you must be controlling your grocery expenses a great deal.

Great news. I must admit a highlight of my week is looking at dividend transactions with my brokerage accounts and ringing the cash register.

Also if there is a choice to buy a product I always choose the one I own as I know one of the fractional cents will come back to me.

Also a good excuse to buy happy meals at MCD , soft serve from BRK’s DQ and Cadbury’s from MDLZ for my 5 year old

It’s fun seeing dividend pay cheques getting deposited for sure. 🙂

I’m curious about your plans for Algonquin after its weak quarterly report and outlook comments.

Best wishes

Hi Stephen,

A good question, I have a post about AQN scheduled for this Friday (Nov 25). Stay tuned.

Looking forward to the post.

Congrats on an amazing month! Man, you are getting closer and closer to full financial freedom! Keep it up! 🙂

Thank you, My Dividend Dynasty.

Congrats, Bob! Great month and nice to see that incredible YoY October growth. Are there any new holdings you are eyeing to pick up in the new year? Also what are your thoughts on AQN, given your current position?

Josh

Thanks Josh. We’ll probably focus on the low yield high dividend growth stocks in the new year. In terms of AQN, I have an analysis scheduled to go live this Friday. Please stay tuned.