It’s hard to believe it’s already November and there are only two months left in 2023. Given that the stock market has been extremely volatile, many Canadian dividend stocks have seen better days. I bet many investors are wishing for a greener 2024.

But let’s not forget that a bear market should be what you wish for if you are still in the accumulating phase. You want to purchase stock at a discounted price; not paying a premium!

I really wish the market would stay volatile at least until early January so we can use the new TFSA contributions to buy some discounted dividend paying stocks.

Side note: While not official, it looks like 2024’s TFSA contribution limit will be increased to $7,000.

Like other months in 2023, we have kept ourselves busy throughout October.

The arrival of fall meant we harvested many apples, plums, and pumpkins from our backyard garden. Mrs. T then made chutney and soup for consumption later.

For me, something amazing happened in October. I attended a Tool concert! This was my fourth time seeing Tool live. Given Tool is my favourite band and the last time I went to a Tool concert was over 13 years ago, I was beyond excited.

Tool rocked for over 2 hours and played 12 songs in total. It was an amazing experience with lots of cool visuals.

Here’s a video from the concert that someone recorded:

Hopefully I don’t have to wait for another 13 years to see Tool live…

We also did a really big thing as a family in October – we took a surprise trip to Anaheim to check out Universal Studios Hollywood, Disneyland, and California Adventure! This was a trip that Mrs. T and I had been secretly planning for months. None of our friends or family knew.

We told Kid 1 and Kid 2 that we’d stay at the YVR airport hotel for the weekend. When we arrived at the airport, we gave the kids a coded message to decode.

Needlessly to say, both kids were more than pleasantly surprised when they found out we were going to Disneyland.

We woke up at 6 AM the second morning to give us enough time to do rope drop at Universal Studios Hollywood. Beating the crowds helped us to ride many attractions without having to wait too long.

Overall, we thought Universal Studios Hollywood was neat, especially Harry Potter Land and Super Mario World. But we got a bit nauseous from many of the virtual reality rides. Since we stayed in Anaheim, we also didn’t enjoy riding in an Uber and getting stuck in LA traffic for 1.5 hours in the morning and end of the day.

For this trip, we stayed at the new The Westin Anaheim Resort using Marriott Bonvoy points and saved close to $4,500 CAD for hotel accommodation (accommodation was insanely expensive when you stay nearby Disneyland!). The hotel room itself was very spacious. We even got upgraded to a park view room with a large balcony. I tried to push my luck and asked to be upgraded to a suite but I ran out of luck.

The Westin was a 15-20 minute walk to Disneyland/California Adventure entrance which allowed us to come back to the hotel in the afternoon and rest.

Thanks to my Marriott Bonvoy Platinum Elite status, we were able to get breakfast and hors d’oeuvre each day at the Westin Club lounge. This helped us save even more money. In fact, we only spent $1,122.86 CAD on food for this 7-day trip for all four of us or $160.41 per day. This is a very low amount considering foods in theme parks are typically very expensive. Furthermore the USD to CAD exchange rate was almost 1.40 so buying anything in the US was terrible for us Canadians.

This is why we continue to collect Marriott Bonvoy points whenever we can. An easy way to earn 55,0000 Marriott Bonvoy points is through my American Express Bonvoy credit card referral link.

We did two days at Disneyland and one day at California Adventure. Arriving early and doing the rope drop on all three days helped us avoid big crowds and we were able to finish many rides in the first couple hours of the morning.

Although Genie Plus cost an additional $30 USD per person per day, it was totally worth it. We were able to reserve our spots at specific time slots and get on the rides in under five minutes. Some of the popular rides like Indiana Jones, Matterhorn, Spiderman, and Haunted Mansion consistently had forty minute or longer wait times. It was nice not having to wait in line so we could experience the different attractions and riding our favourite ones multiple times.

Before the trip, we knew that we needed to use Universal and Disneyland apps to check for attraction wait times and to order food. Instead of paying a $14 per day roaming fee, we decided to get an Airalo data package (save $3 USD by using my referral code). The 2GB data package was only $8 USD which was way more affordable than paying for the daily data roaming charge.

Thanks to a combination of travel hacking, using points, and deal hunting, the 7-day trip was under $4,500. Although it’s quite a bit of money, the experiences and memories we gained were totally worth it. This is exactly why the die with zero concept makes a lot of sense.

Dividend Income – October 2023

Back to dividend income. In October we received dividend pay cheques from the following companies:

- Algonquin Power & Utilities (AQN.TO)

- Alimentation Couche-Tard (ATD.TO)

- BCE Inc (BCE.TO)

- Bank of Nova Scotia (BNS.TO)

- CIBC (CM.TO)

- Canadian Natural Resources (CNQ.TO)

- Capital Power Corp (CPX.TO)

- Granite REIT (GRT.UN)

- Coca-Cola (KO)

- SmartCentres REIT (SRU.UN)

- Telus (T.TO)

- TD (TD.TO)

- TC Energy Corp (TRP.TO)

- VICI Properties (VICI)

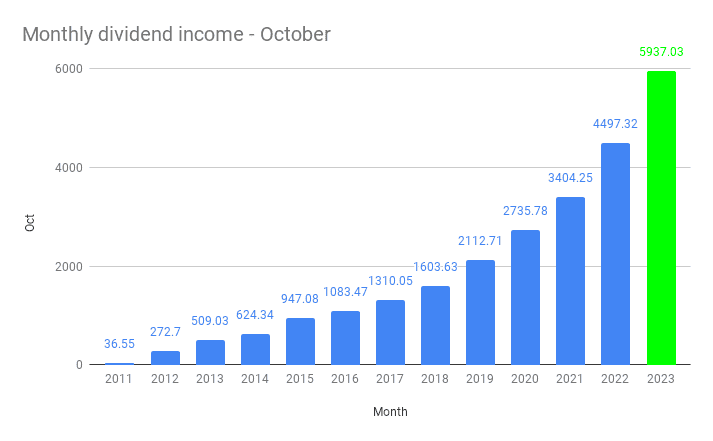

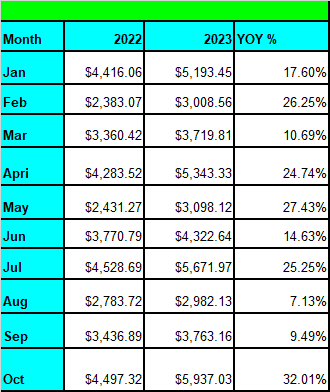

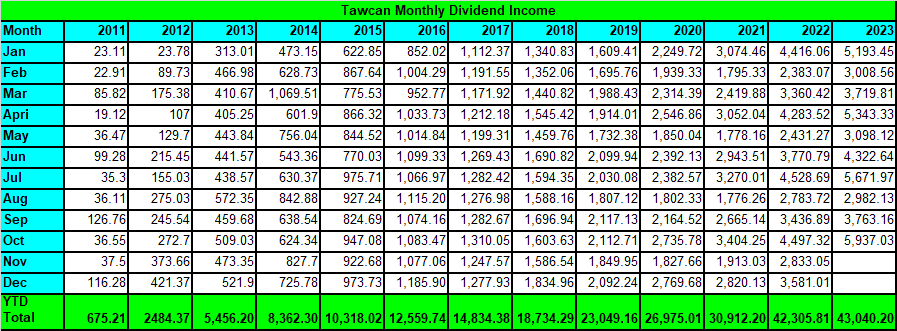

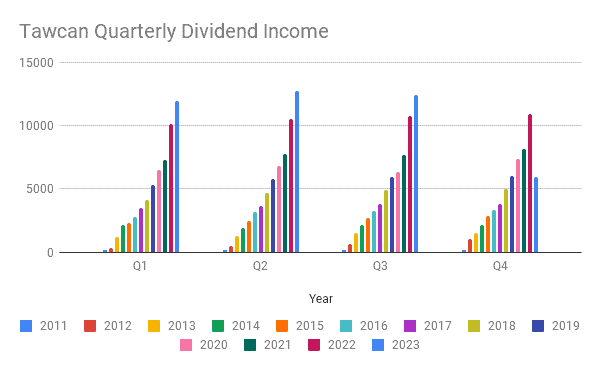

The 14 pay cheques added up to $5,937.03. A new monthly dividend income record. Woohoo!

We went from $5,193.45 in January to $5,343.33 in April to $5,671.97 in July to $5,937.03, setting new monthly dividend income records along the way. Given how the market has done in 2023, this was a very encouraging trend.

Compared to October 2023, we saw a YoY growth of 32.01%! This is the highest YoY growth number so far in 2023. We were very pleased to see this amazing increase.

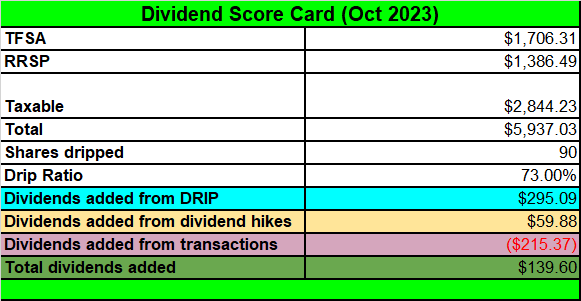

Out of the $5,937.03 received, $297.05 was in USD and $5,639.98 was in CAD. October was one of those CAD heavy months. Long time readers will recall that we do not convert USD to CAD when reporting our dividend income. The main reason is to avoid fluctuations in our monthly dividend income reports due to sudden changes in the exchange rate.

While I have considered converting USD to CAD in 2024, to keep the math simple and straightforward, I may continue to use the 1:1 exchange rate. Do you agree with this approach? I’d love to hear your thoughts.

Dividend Hikes

October was a nice month for us in terms of dividend hikes. The following companies announced dividend hikes in October:

- Waste Connections (WCN.TO) raised its dividend payout by 11.8% to $0.285 per share

- McDonald’s (MCD) raised its dividend payout by 10% to $1.67 per share

- Visa (V) raised its dividend payout by 16% to $0.52 per share

- AbbVie (ABBV) raised its dividend payout by 4.7% to $1.55 per share

These dividend hikes increased our forward annual dividend income by $59.88. While it’s not a huge amount, a small amount of organic dividend increase is better than nothing at all.

Dividend Reinvestment Plans

We rely on three pillars to increase our dividend income.

The first pillar is by buying more dividend paying stocks with new capital. The second pillar is growing dividends organically through dividend hikes. The third and final pillar is enrolling in dividend reinvestment plans (DRIP) whenever we’re eligible. Enrolling in DRIP allows us to automatically receive additional shares at each dividend payout, whether it’s every quarter or every month.

A bit more info on DRIP… there are two different types of DRIP – full DRIP and synthetic DRIP. Full DRIPs are typically done via each company’s transfer agent like ComputerShare. Nowadays thanks to WealthSimple Trade, you can drip fractional shares even when not using a transfer agent. For example, if you have 10 shares of TD and receive $9.60 in dividends and TD is at $80 per share, you’d drip 0.12 share.

Synthetic DRIP is supported by other discount brokers like TD, Questrade, and RBC. For synthetic DRIP, you can only drip full shares. If you don’t receive enough dividends to drip a full share, the cash is deposited in your account. For example, if you receive $95 dividends from TD and TD is at $80 per share, your discount broker would drip 1 TD share for you and deposit the remainder, $15, in your account.

We enroll in synthetic DRIP whenever we’re eligible. Thanks to synthetic DRIP, we were able to add the following shares automatically in October:

- 13 shares of BCE.TO

- 14 shares of BNS.TO

- 16 shares of CM.TO

- 2 shares of CPX.TO

- 2 shares of KO

- 6 shares of SRU.UN

- 11 shares of T.TO

- 12 shares of TD.TO

- 12 shares of TRP.TO

- 2 shares of VICI

The depressed market meant we were able to drip more shares than usual. Some readers will notice that we didn’t drip any AQN.TO shares. We decided to turn off the drip for our AQN position as we began trimming and closing out the position throughout October (more to come later).

Thanks to drip we added 90 shares automatically and increased our forward annual dividend income by $295.09.

Dividend Transactions

Let me start off by saying that Algonquin Power & Utilities has been an absolute disaster. The stock has been down 43.29% in the last five years and has cut its dividends by 50% last year (with another cut rumoured to be coming in Q1).

Looking back, we committed two mistakes by investing a ton of money in the renewable hype and secondly by ignoring the large debt that AQN had. A third mistake was not to close out the position earlier and reduce the amount of loss.

Having said all that, we started trimming AQN shares throughout October and closed out our AQN position by the end of the month and ended up with a 40% loss, not including dividends.

Ouch!

With the money from closing out AQN, we purchased the following dividend paying stocks:

- 30 shares of Royal Bank

- 60 shares of Alimentation Couche-Tard

- 150 shares of BCE

We decided to take advantage of the depressed pricing for both Royal Bank and BCE. Long term, I believe both will recover nicely. We also added more ATD shares because the share price just keeps going higher and higher. I really like what ATD is doing in terms of global convenience store presence, as I noticed many Circle K convenience stores in Hong Kong on my recent business trip.

After all these transactions, we lost $215.37 in forward annual dividend income.

Although it’s never ideal to lose dividend income, I think it was better to take the loss on AQN and reinvest the money elsewhere.

Dividend Score Card – October 2023

Here’s our dividend score card from October:

Overall, we did quite well given the new monthly dividend income record. While it’s annoying to lose forward dividend income due to closing out of AQN, it was a long overdue move. We should have closed out AQN probably more than six months ago, if not longer. I had thought that AQN would have gotten their balance sheet in order by existing the Kentucky Power acquisition and cutting dividends by 50%. But clearly, the company is going through some pains and will take much longer than anticipated to right the ship.

Will AQN recover to its former glory? Or will someone like Brookfield Renewable Energy acquire AQN? I’m not sure what the answers would be but what I do know is that it is time to move on and reinvest the money elsewhere.

Dividend Income – October 2023 Summary

It’s quite exciting to have a new monthly dividend income record. What’s even more exciting is the fact that we have already exceeded our 2022 annual dividend income!

With two more months to go, I’m pretty certain that we’ll crash our $49,000 dividend income goal for this year. In fact, I’m confident that we’ll end up with over $50,000 in dividend income at the end of this year. This itself is pretty amazing considering that four years ago we received less than $25,000 in dividend income.

To put things in perspective, $43,040.20 after ten months is equivalent of:

- $141.58 per day or $5.90 per hour

It’s nice to know that our dividend portfolio is generating enough money per hour to get us a cup of Starbucks latte.

- $978.19 per working week or $24.45 per hour after 44 working weeks

It’s nice to see that our dividend portfolio is generating more than BC’s minimum wage of $16.75 per hour. However, we are actually paying very little taxes on our dividend income because of the following reasons:

- 26.3% of our dividend income to date came from TFSAs, so it’s not taxed at all

- 28% of our dividend income to date came from RRSPs and it’s tax deferred until withdrawals are made

- The remainder of 45.7% came from taxable accounts and it’s split about 40-60 between Mrs. T and me. Given that dividend income inside taxable accounts gets preferential tax treatments, we’re paying very little taxes.

For now, we are sticking to our BORING strategy – earn money, save money, invest regularly, and repeat.

How was your October dividend income?

This is great.. I love your blog and keep reading it every week.

I was reading up on BCE, and is there instances where you would still hold on to the stock but just turn off DRIP ?

Greetings Bob – I’ve been eyeing ATD as well for the growth portion of my portfolio. Check out what they are doing on their website in Norway with EV charging stations – looks like they are preparing for that change. Keep hoping I can catch it on a dip but doesn’t seem to happen. Other CA growth stocks I’ve purchased in the last year: CSU, DOL, FFH, EQB, EFN. Spoke to you last May when I sold my house. Ended up doing a portfolio that is 60/40 & 50/50 growth/dividend for the 60 equites. Dividend stocks are banks (TD, RY), insurance (MFC), utilities (only regulated – FTS, EMA) & one pipeline (TRP (ouch!)) & one nat. gas (TOU). I don’t know about the Bogleheads when it comes to the Canadian market. It’s small enough you can examine every needle. look forward to reading your updates, Thx!!!! Glen

ATD might be one of those stocks you just need to bite the nail, purchase, and forget about it.

Sounds like you have a solid portfolio of dividend stocks.

Great newsletter, as always! I’m also very annoyed with AGN. My position is small, but I wish I would have closed it out long ago instead of waiting it out hoping for better. Ouch!

Thank you Carly.

Yea, wish we had sold AQN months ago. 🙂

Interesting read!! Quick question, do you do your own taxes? Do you know of a good tax program that I can use as I would like to do my own taxes this year?

Thank you. We do our own taxes, we’ve been using Wealthsimple Tax for many years now.

I have been doing my own taxes using Quicktax for last 30 years. Love the software. Buy the basic version for about 35 dollars and you are good to go. You can create 20 files in it.

A very encouraging newsletter. Well done.

Excellent. Your kids must have had a blast. Your spending at Disney must have been the reason my daughter’s DIS stock went up a couple of dollars last few days. That daily room rates must have been close to $1000 or more?

I’ve done some tax loss selling on AQN too. Luckily never had it in RRSP or TFSA

My favorite newsletter! Love the Disney trip. I have taken that trip! So much fun.

Thank you!

You note that your taxable account is joint, but doesn’t the broker issue taxable receipts (e.g. T3, T5, etc.) to the primary account holder (I assume that is you)? If those records go to CRA, how do you back them out and claim half between you and your wife?

The actual accounts are not joint. I have a taxable account and Mrs. T has one as well. We’re just reporting our dividend income together on here.

First, congrats on your investment journey and sharing your experiences.

I always enjoy reading and feel inspired by the Dividend growth. Can you elaborate more on how you calculate your taxes? I maxed out my TFSA and RRSP but I am having a hard time figuring out how to calculate taxes based on my non-registered stock investments.

Also if you can recommend some readings about this it would be awesome!

Thanks in advance and keep up the good work! 😉

Hi Caio,

Thank you. We’re ignoring taxes right now when it comes to our dividend income tax report because we’re not making any withdrawals yet. Yes, the dividend income in our taxable accounts are taxed each year but the actual tax amount is quite minimal.

It’ll be more interesting to calculate the tax consequences when we are living off dividends.

I love my DRIPs too! While I have quite a ways to go before my portfolio generates as much money each month as yours does, I’m still quite pleased that I’m earning a solid-though-modest 4-figure amount every month. (My PADI will be a hairs-breath under $40K in 2023.) Starting early, investing from every paycheque, using DRIPs, and letting time do the heavy lifting is one of the very best ways I’ve found to build a cash machine for my retirement years.

Again, thank you so much for all that do in sharing your family’s financial goals – and photos of some of how you’re rewarding yourself along the way! (I can definitely see the benefits of the Die With Zero philosophy. I’m not all the way there yet, but I’m getting better.) You’re an inspiration and a great example of what is possible.

It takes a while to get a sizable monthly drip so just be patient. Congrats on PADI of $40k. That’s amazing!