3 years ago, I first wrote about our financial independence assumptions where I estimated how much we would need to be financially independent. Later, I wrote a post on what our income tax might look like when we are financially independent. I created 3 different scenarios with different levels of income. The conclusion I had was that if we rely mostly on our dividend income to cover our expenses when we are financially independent, we would be paying very little taxes.

Now 3 years later, I thought it would be worthwhile to revisit this topic. I would like to compare these assumptions to our historical annual expenses and determine if the assumed numbers are still valid. Since I’m a numbers nerd, as a fun exercise, I would examine the different income tax scenarios again.

Our Financial Indepence Assumptions

Below are what we assumed our core expenses per month might be when we are financially independent.

- House property taxes $350

- House maintenance $50

- House insurance $100

- Utilities $100

- Internet & cellphones $100

- Groceries $800 – two growing kids

- Healthcare $150

- Household supplies $100

- Clothing $100

- Car insurance for 1 vehicle $120

- Gas for 1 vehicle $50

- Car maintenance $50

- Buffer $200

Total: $2,270.

Since our core expenses do not include things like eating out, charity donations, entertainment, vacation, etc, we will add $950 per month to cover these non-core expenses.

This results in $3,220 per month in expenses, or $38,640 per year. For simple calculation, we will round this number up to $40,000.

So, to be financially independent, we need our dividend portfolio to produce $40,000 per year. While we do plan to continue some part-time work when we are financially independent, dividend income will be the primary source of income.

Our Historical Annual Expenses

Let’s take a look at our historical annual expenses over the last 7 years.

| Total Necessities Spending | Core Necessities Spending per Month | Total Annual Spending | Total Spending per Month | |

|---|---|---|---|---|

| 2012 | $26,210.52 | $2,184.21 | $44,603.76 | $3,716.98 |

| 2013 | $26,343.00 | $2,195.25 | $45,260.88 | $3,771.74 |

| 2014 | $29,058.96 | $2,421.58 | $47,391.96 | $3,949.33 |

| 2015 | $31,256.88 | $2,604.74 | $47,270.16 | $3,939.18 |

| 2016 | $29,831.40 | $2,485.95 | $4,7566.96 | $3,963.91 |

| 2017 | $33,887.68 | $2,823.97 | $51,144.77 | $4,262.06 |

| 2018 | $31,840.75 | $2,653.40 | $57,231.99 | $4,769.33 |

For the last 3 years, we have been averaging $2654.44 per month in core expenses. That’s about $400 more than our FI assumption core expense. This is not too far off, considering we assumed that when we are financially independent, either of us would be working full-time. So some expenses, like car-related expenses, for example, should go down.

In the last 7 years, we have never spent less than $40,000 in a year. While I do think $40k a year annual expenses is achievable, I want to be realistic. When we are financially independent and working part-time (or not working at all), we probably will be travelling more. This will most likely increase our overall spending.

Therefore, for all intents and purposes, let’s run a few different scenarios using the following annual expenses

- $40,000 a year

- $50,000 a year

- $60,000 a year

Income Tax Comparisons

For calculating income tax, I used the trusty 2018 tax calculator by SimpleTax. All the calculations are based on BC residency. I also assumed that there were no tax deductions available.

If you are earning income via employment, below are the employment income you need to earn to supplement the 3 different annual expenses.

| Annual Expenses | Employement Income Needed | Taxes | Average Tax Rate | Marginal Tax rate |

| $40,000 | $50,776.00 | $10,776.00 | 0.21% | 28.20% |

| $50,000 | $65,003.00 | $15,003 | 23.08% | 28.20% |

| $60,000 | $78,930.00 | $18,930.00 | 23.98% | 28.20% |

In comparison, below are the dividend incomes you need to supplement the 3 different annual expenses.

| Annual Expenses | Dividend | Net Income | Taxes | Average Tax Rate | Marginal Tax Rate |

| $40,000 | $40,000.00 | $40,000.00 | $0.00 | 0% | 28.20% |

| $50,000 | $50,000.00 | $50,000.00 | $0.00 | 0% | 28.20% |

| $60,000 | $60,000.00 | $59,797.00 | $203.00 | 34% | 31% |

As you can see from above, The Canadian tax system is very favourable to people that rely on their dividend income. If you are earning income via employment, your income is taxed way higher than dividend income.

Our Dividend Income Breakdown

In 2018 we received a total of $18,734.29 in dividend income. The dividend breakdown from the different accounts was as follow:

- $7,062.92 from RRSPs or 37.7%

- $6,802.49 from TFSAs or 36.3%

- $4,868.88 from taxable accounts or 26.0%

In our previous financial independence assumptions, we assumed that Mrs. T and I would have a 40-60 split in dividend income. Was this realistic? Let’s take a look at a further breakdown of our 2018 dividend income.

| Accounts | Mrs. T | % | Tawcan | % |

| RRSP | $1,182.61 | 6.3% | $5,880.31 | 31.4% |

| TFSA | $3,154.81 | 16.8% | $3,647.68 | 19.5% |

| Taxable | $1,616.62 | 8.6% | $3,252.26 | 17.4% |

| Total | $5,954.04 | 32% | $12,780.25 | 68% |

So our 2018 dividend income was more of a 30-70 split between the two of us.

Because Mrs. T didn’t become a Canadian permanent resident until 2011, she did not have TFSA contribution rooms for 2009 and 2010 ($10,000 in total. As you may recall, we had mistakenly over-contributed her TFSA and had to beg the CRA for mercy). Therefore, it makes sense that her TFSA doesn’t generate as much dividend income as my TFSA.

Since I already have a sizable RRSP, thanks to working for 12 years at the same company, we have started a spousal RRSP for Mrs. T in recent years. I have stopped contributing money to my self-directed RRSP. Instead, I am now contributing money to Mrs. T’s spousal RRSP. Our ultimate goal is that one day our RRSPs would roughly have similar in value and generate similar amount of dividends.

Ideal Dividend Income Breakdown

Given that I’m the primary income earner in our household (for now), it might not be realistic to assume that our dividend income would be a 50-50 breakdown. I think a 40-60 breakdown as we previous assumed is more realistic.

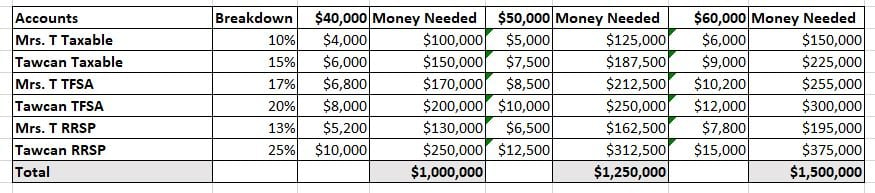

Based on 2018 dividend income breakdown, and the fact that we are slowly adding more money to Mrs. T’s spousal RRSP and her taxable account, below is the ideal/assumed account breakdown when we are relying on dividend income cover our expenses.

| Accounts | Breakdown |

| Mrs. T Taxable | 10% |

| Tawcan Taxable | 15% |

| Mrs. T TFSA | 17% |

| Tawcan TFSA | 20% |

| Mrs. T RRSP | 13% |

| Tawcan RRSP | 25% |

Based on the above breakdown, below would be the dividend incomes we expect to receive in the different accounts.

| Accounts | Breakdown | $40,000 | $50,000 | $60,000 |

| Mrs. T Taxable | 10% | $4,000 | $5,000 | $6,000 |

| Tawcan Taxable | 15% | $6,000 | $7,500 | $9,000 |

| Mrs. T TFSA | 17% | $6,800 | $8,500 | $10,200 |

| Tawcan TFSA | 20% | $8,000 | $10,000 | $12,000 |

| Mrs. T RRSP | 13% | $5,200 | $6,500 | $7,800 |

| Tawcan RRSP | 25% | $10,000 | $12,500 | $15,000 |

With these numbers in hand, we can calculate the different tax scenarios.

Withholding Tax on RRSP Withdrawals

A very important thing to note regarding RRSP withdrawals is that any withdrawals from your RRSP are immediately subject to withholding tax. The amount of withholding tax is based on how much you are taking out. The final amount you get is then taxes at your marginal tax rate.

Another thing to note is that non-residents of Canada pay a withholding tax of 25%, except in places where the amount is reduced by treaty. So if we decided to live outside of Canada when we are financially independent, we’d be taxed at

Income Tax Assumptions

Below are some of the assumptions I will use for income tax calculations

- All dividends from taxable accounts are eligible dividend income.

- We will make withdrawals from our RRSPs on the full amount listed in the table above.

- No tax deductions (i.e. charitable donations, RRSP contributions, business expenses, etc).

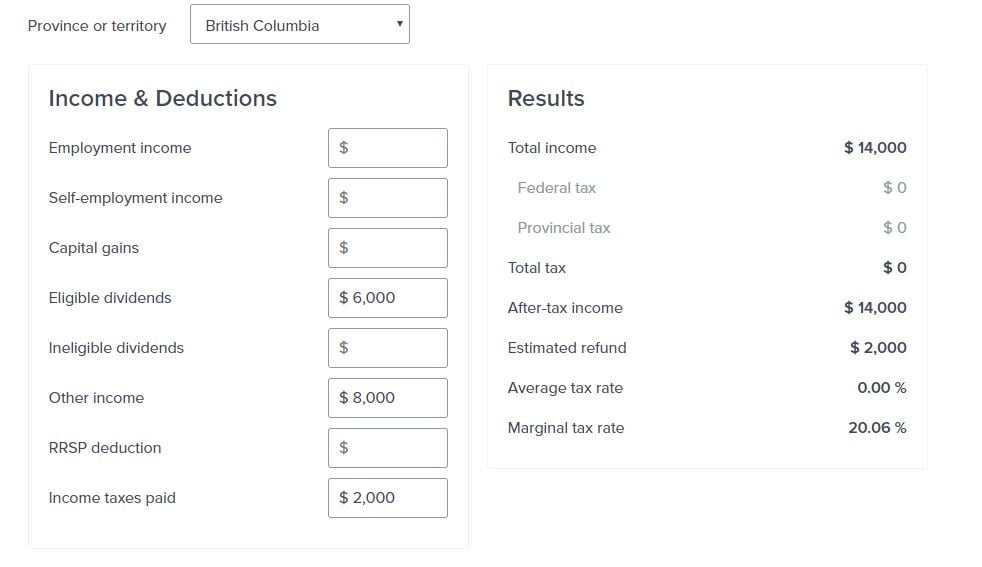

Scenario 1 – $40,000 Tax Calculations

What happens to our income tax if Mrs. T and I were to receive a combined $40,000 in dividend income from the different accounts?

| Accounts ($40,000 Scenario) | Mrs. T | Tawcan |

| Taxable | $4,000 | $6,000 |

| TFSA | $6,800 | $8,000 |

| RRSP | $5,200 | $10,000 |

| RRSP Witholding Tax | $1,040 | $2,000 |

| Net RRSP | $4,160 | $8,000 |

| Est Refund | $1,040 | $2,000 |

| Average Tax Rate | 0% | 0% |

| Marginal Tax Rate | 20.06% | 20.06% |

| Net Income | $16,000 | $24,000 |

| Total Income | $40,000 |

We wouldn’t pay any income tax. Pretty cool! This was expected.

Scenario 2 – $50,000 Tax Calculations

What happens to our income tax if Mrs. T and I were to receive a combined $50,000 in dividend income from the different accounts?

| Accounts ($50,000 scenario) | Mrs. T | Tawcan |

| Taxable | $5,000 | $7,500 |

| TFSA | $8,500 | $10,000 |

| RRSP | $6,500 | $12,500 |

| RRSP Witholding Tax | $1,300 | $2,500 |

| Net RRSP | $5,200 | $10,000 |

| Est Refund | 1300 | 2500 |

| Average Tax Rate | 0% | 0% |

| Marginal Tax Rate | 20.06% | 20.06% |

| Net Income | $20,000 | $30,000 |

| Total Income | $50,000 |

Once again, we would be paying $0 in taxes if we were to receive $50,000 in dividend income and use that money to cover our expenses. This was what I expected.

Scenario 3 – $60,000 Tax Calculations

Below are the calculations if we were to receive $60,000 in dividend income.

| Accounts ($60,000 Scenario) | Mrs. T | Tawcan |

| Taxable | $6,000 | $9,000 |

| TFSA | $10,200 | $12,000 |

| RRSP | $7,800 | $15,000 |

| RRSP Witholding Tax | $1,560.0 | $4,500.0 |

| Net RRSP | $6,240.0 | $10,500.0 |

| Est Refund | 1560 | 4500 |

| Average Tax Rate | 0% | 0% |

| Marginal Tax Rate | 20.06% | 20.06% |

| Net Income | $24,000 | $36,000 |

| Total Income | $60,000 |

I’ll be honest, I wasn’t expecting to pay $0 in taxes for scenario 3. I was expecting that we would need to pay a small amount of taxes.

It was interesting to see that we can receive $60,000 in dividend income combined without paying any taxes. On the other hand, we’d need to pay around $14,000 in taxes if one of us were to earn $60,000 in employment income. We’d need to pay around $6,500 in taxes if one of us were to earn $36,000 in employment income.

Note: Although we wouldn’t be paying any income taxes in these 3 scenarios, we would still be paying taxes like GST, PST, property tax, carbon tax, transportation tax, etc. We wouldn’t be “freeloading.” 🙂 😉

Scenario 4 – $60,000 living abroad Calculation

Since we plan to live abroad like Taiwan and Denmark when we are financially independent, what will happen to our income tax? For this scenario, I will assume that we receive $60,000 in dividend income.

| Accounts ($60,000 living abroad) | Mrs. T | Tawcan |

| Taxable | $6,000 | $9,000 |

| TFSA | $10,200 | $12,000 |

| RRSP | $7,800 | $15,000 |

| RRSP Witholding Tax | $1,950.0 | $3,750.0 |

| Net RRSP | $5,850.0 | $11,250.0 |

| Est Refund | $1,950 | $3,750 |

| Average Tax Rate | 0% | 0% |

| Marginal Tax Rate | 20.06% | 20.06% |

| Net Income | $24,000 | $36,000 |

| Total Income | $60,000 |

Wow, that was interesting! Even if we were to live abroad when we are financially independent, and pay 25% in withholding tax for RRSP withdrawals, we would still net $60,000. Very cool!

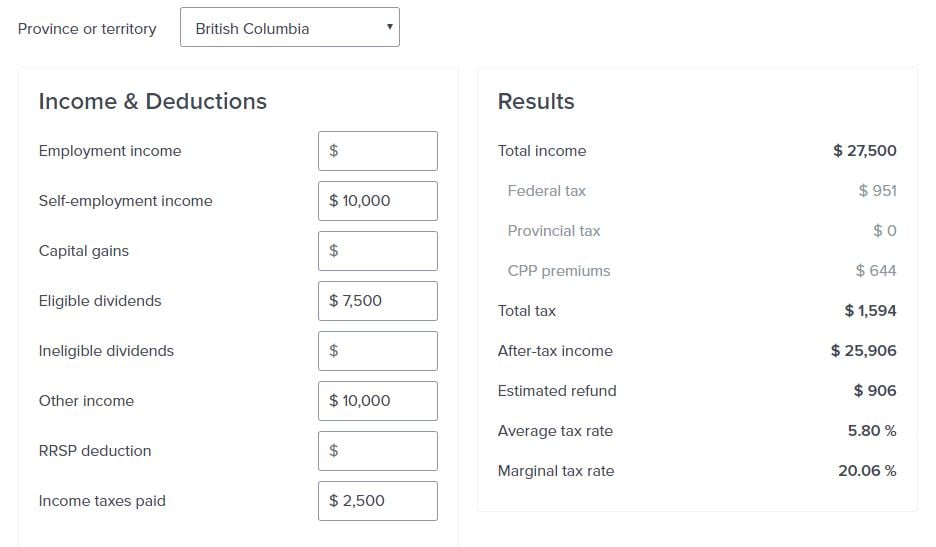

Scenario 5 – dividend & working calculation

Just for fun, what happens if we were to receive $50,000 in dividend income and we were to work part-time? Let’s assume that we made $10,000 each in part-time income from our side businesses ($20,000 in total). For simplicity, we will assume that we have no business deductions.

| Accounts ($50k Div + $20k Bus) | Mrs. T | Tawcan |

| Taxable | $5,000 | $7,500 |

| Employement Income | $10,000 | $10,000 |

| TFSA | $8,500 | $10,000 |

| RRSP | $6,500 | $12,500 |

| Total Income | $30,000 | $40,000 |

| RRSP Witholding Tax | $1,300 | $2,500 |

| Net RRSP | $5,200 | $10,000 |

| Est Refund | $875 | $906 |

| Average Tax Rate | 4.33% | 5.80% |

| Marginal Tax Rate | 20.06% | 20.06% |

| Net Income | $29,575 | $38,406 |

| Total Income | $67,981 |

We would be paying $1,781 in taxes combined at a marginal tax rate of 20.06% and average tax rates of 4.33% and 5.80%. These are pretty small percentages if you were to ask me. In reality, we could probably deduct a lot of business expenses to reduce the amount of taxes we have to pay.

How much do we need?

While going through these different scenarios, I began to wonder how much money is needed to generate the required dividends in the different accounts. Below

For my TFSA, the accumulated total amount is $63,500 from 2009 to 2019. For Mrs. T, the accumulated total amount is $53,500 from 2011 to 2019. Looking at the different scenarios, at $6,000 contribution each per year, it would take quite a number of years to hit more than $170k in our TFSAs. Maybe our assumptions are not realistic?

It’s tough to answer this question. One thing to note is that the values indicated in the table above are portfolio values rather than total contributions. Therefore, it may not take as many years to hit these numbers as our portfolio value should increase thanks to dividend income and capital appreciation.

In general, I am encouraged to see these number breakdowns. The money needed is roughly in line with what we anticipated. Again, these are “portfolio values.” Thanks to organic dividend growth and DRIP, we may not need to contribute over $1M as I explained previously.

Final Thoughts

Phew, that was a lot of numbers that we just went through! From the 5 different scenarios, I have validated once again that dividend income is very tax efficient. In fact, we wouldn’t be paying any income tax if we were to rely purely on dividend income to cover our expenses. I was quite surprised that this is the case even in the $60,000 per year dividend income scenario. Even if we were to work part-time, earning $20,000 a year between the 2 of us, we would be paying a very small amount of income tax. And I am totally OK paying taxes, given that we would be using the great social benefits available to Canadians.

When I originally created 3 different scenarios in 2016, I was quite worried about the withholding tax on RRSP withdrawals. Therefore, in those scenarios, I made the RRSP withdrawals to be below $5,000. In this post, I have demonstrated that we don’t really need to worry about RRSP withholding tax when our combined dividend income is below $60,000. This was quite unexpected.

Another interesting thing to note is that even if we were to decide to live abroad when we are financially independent and living on $60,000 of combined dividend income a year, we would be getting all the withholding tax back when we file for income tax.

Therefore, I continue to believe that dividend income can be quite tax efficient, especially during FIRE years when one is not earning employment income. Relying on dividend income provides a margin of safety, too, as we wouldn’t need to touch our principal.

Dear readers, what do you think about my assumptions? If you see any holes in my calculations and assumptions, I would very much love to hear from you.

Hello!

Yes I sold my house a few years ago but just living nomadicly for the moment rather then having taken up residence in any one country but it is my understanding that if I were to do that all my Canadian investments would be subject to a 25% withholding tax which is really the only reason I hold Canadian Stocks VS US stocks / international stocks

I guess If I were to take up residence somewhere else I would probably consider switching from Canadian to US stocks (ETFs) which also have a withholding tax but are a much more diversified market to invest in

Hi Bob!

I”m just curious if you took into consideration where your primary residency would be when you moved abroad and the tax implications of this?

As someone who’s also considering doing something similar it is my understanding that when you take up residence in another country

A) all your cap gains are calculated as of that day and you owe the difference. (The day you are no longer a resident for tax purposes )

B) Dividends are no longer eligible for this tax credit and now there will be a 25% withholding tax

Just wondering if I understand this correctly or if I missed something

Hi Brian,

Hmm good question, to be honest, I haven’t look into that yet but I believe you might be right on the withholding tax. That’s why it is especially important to have dividend income from TFSA.

In terms of residence, are you talking about selling your primary house and moving to another country?

When your kids become older, I think your core expense will be higher. I pay more than $400 a month for piano lessons, for example. I also need to buy books, pay for exams, twice a year tune up of the piano…… Adding soccer, swimming, scouts, etc. to that.

Also, I was told today that going to University of Toronto cost between $50K-$60K a year, quite a shock for me. I have planned for $30K a year and now I have to double that budget.

Still, I think you will reach FI very fast. Just want to prepare you so that you will not be surprised. LOL. Kids are little machines burning money very fast.

Hi May,

That’s a good point, that’s why I ran the calculations using 3 different numbers. Another thing to consider is that kids are only as expensive as parents allow them to be. 😉 🙂

One interesting feature of BC income tax is that there is a negative marginal tax rate on dividends in some tax brackets. For me, I actually pay less tax with dividend income than I would if I had no dividend income. So in some cases, it would be advantageous to hold Canadian dividend paying stocks in a taxable account rather than in a TFSA! Thanks to the increase to the corporate tax rate and corresponding increase to the dividend tax credit, the marginal tax rate on eligible dividends will decrease further for 2019.

Yes, that’s an interesting “feature” indeed. 🙂

Some serious number crunching in there Bob, wow well done.

Thanks Chris.

I love how clear you’ve presented the different scenarios. Indeed, it’s quite difficult to predict the future, but it looks like you made some reasonable assumptions.

I’ am always a bit jealous seeing your advantages on tax from dividends. In Germany that is not the case unfortunately. Here, at individual level, the shareholder is required to pay a flat rate withholding tax on dividends of 25% and an additional solidarity charge of 5.5%

That’s too bad that you don’t have such tax advantage on dividends in Germany. Are there any ways to reduce your taxes in Germany though?

Not many actually. There is a tax-free allowance of € 801 per person and €1,602 for married couples..and that’s it. It’s not attractive to retire in GER if you plan to live from dividend income.

Nice update Tawcan. I totally expect our total tax % will drop too as we rely more and more on dividend income.

Technically we could live without earned income today (our dividend income covers all core expenses), but I don’t think earned income is ever totally go away from our income mix. We’ll likely always have some small hobby businesses.

Cheers!

Thanks Mr. Tako. Dropping tax rate when relying more and more on dividend income is good. Gotta love tax efficiency. 🙂

I have been reading your blog for some time now, but have never commented. I really enjoy your thoughtful analysis and insights into finance, savings, and life. Currently, my family and I live in the middle east, in a country that has no tax treaty with Canada. While my income is 100% tax-free, I do get nailed on the 25% withholding tax on all dividend income from Canada and the US. What gets me really excited is when I repatriate all of my savings, I will be able to live relatively tax-free on dividends from all the money I am able to bank now even if we choose to retire in Canada. Currently, I hit almost $1,000 per month in dividend income, and that is after much of it being taxed at 25%. Unfortunately, I cannot contribute to RRSP, RESP or TFSA while I am a non-resident. That’s fair and I shouldn’t be able to. However, for any expats reading your blog, it is good to note that many of your ideas for future planning are applicable. I steer my friends in this part of the world to you often for ideas and study. Keep up the good work!!!

Hi Expat_Guy,

Thank you for the first comment, I appreciate that. I guess the 25% withholding tax is an issue for living in the middle east where they don’t have tax treaty with Canada. Given that we’re planning to live abroad in the future, I need to take a look at the withholding tax/tax treaty between say Denmark/Taiwan and Canada. Are you planning to move back to Canada in the future so you can take advantage of RRSP, RESP, and TFSA?

Wow, this must have taken some time to write. Thanks for sharing such a detailed breakdown.

I think that you are most likely going to reach your goal very soon. You are putting up some great numbers and like you said you will most likely continue to work part time or something to keep some more income coming in. You’re probably very close there. Reinvesting $1500 a month or so in dividend income sure does help too!

It was actually a lot of fun writing this post and doing all the different simulations. I guess I’m a numbers nerd haha. 🙂

We are hopeful that we’ll reach our goals soon.

Hi Bob!

Very nice and detailed post. And what an advantage on tax from dividends you have in BC. As far as I know here in Europe we do not have any country that has a similar tax advantage.

In moments like this I can really see how geoarbitrage can be important when planning the FIRE.

All the best.

Cheers!

Thanks Odysseus. I haven’t checked tax systems in Europe so I can’t say there aren’t anything similar, I do wonder if dividends are tax efficient in Europe though, as there are quite a number of European DGI’s.

Hi Bob!

Most of the western European countries have a tax on dividends higher than 25% (as the example mentioned by Snugfortune below). Moving towards east Europe you can find countries with lower tax on dividends, such as Bulgaria (5%) and Romania (5%). But then you also have to check the double taxation agreement between the countries in order to check the WTH from the “paying country”. I have heard about people opening companies in Estonia to have a lower tax, but for the moment it looks to much for me.

All in all it is not so simple as I would like, but from my point of view the European Market is not so strong on Dividend Growth Stocks as US/Canada, what drove me to cross the Atlantic.

You can have a flavor about worldwide tax on dividends checking this table from Deloitte:

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-withholding-tax-rates.pdf

All the best.

Cheers!

Hi Tawcan. I wanted to check something with you. I don’t see all the calculations here but were you accounting for the fact that, for tax purposes, dividend income inside an RRSP does NOT retain its characteristics once withdrawn? It comes out as fully taxable – there is no Dividend tax credit (DTC) on these amounts (although it is eligible for pension splitting as applicable). You will need significantly more income from inside an RRSP to account for the tax inefficiencies of any withdrawals (in comparison to those outside of tax shelters). If you want to simulate this in your calculator assume that the RRSP withdrawals are reported in a T4RSP / T4RIF slip – probably box 22.

Hi Lenny,

Any income coming out of RRSP counts as fully taxable income. This is why in my calculation, income from RRSP is under the “other income” (checked with Simple Tax team before I did the calculations). So yes, there’s no dividend tax credit associated.

Awesome! These numbers look ever better then!

Hi Taw, awesome work! my question is the same as Lenny’s. I don’t see you include your RRSP income in “other income” when you use Simple Tax. Instead, you are report TFSA income in other income, which in my opinion is not right because any income from TFSA should be tax free. Maybe I am missing something here? Thanks!

Hi Sam,

I did report RRSP income as other income but maybe the screenshot is incorrect. Sorry for causing the confusion.

Great point about tax advantages from dividend income. If you invest in eligible companies, you get a nice dividend tax credit to minimize taxes. Also, the child support payments go up if you earn less money.

For sure. I’m waiting for troll to start flaming me for taking advantage of the tax system…. :rolleyes:

Nice work Bob.

What a (tax) difference when you plan and split your income between the two of you.

Cheers

Caroline

Hi Caroline,

Thank you, income splitting is pretty magically when you do it right. 🙂

wow nice breakdown Bob

Its a pretty cool way for us Canadians to envision our retirement years.

I thought there would be more tax implications but you proved me wrong. Sweet!

keep it up man

cheers

Thank you Passivecanadianincome. I thought there would be more tax implications too but I proved it that dividend income is quite tax efficient. 🙂

Amazing and thorough analysis, Tawcan. Extremely detailed and very easy to understand. Good work!

We’ve also been tracking our expenses over the past few years, and we are at roughly $3,500 per month. Or $42K per year. This figure does not include travel.

From our perspective, we’re on pace to pay off our home in 2028 and achieve financial independence simultaneously. So 9 more years!

What’s your target year for FIRE?

Hi R,

Thank you, I appreciate it. Glad that the analysis is easy to understand. $42k per year not including travel is pretty awesome!

We don’t have a specific target year for FIRE. Technically we can be FI if we wanted to be now but we are taking the slow and steady path to FI. We are estimating to be FI by our early 40’s.

Yes, I saw your post regarding that you can technically be FIRE now (congrats!!).

Seems like you don’t really have a target DATE in mind, though you do have a target #. This seems a bit puzzling for me because they both should go hand-in-hand. Unless I’m missing something?

We have a target number in terms of dividend income amount, plan to achieve that in our early 40’s (in 5-8 years from now). 🙂

Unexpected house expenses seem to always get me. 10k roofs, 5k decks. You might be a bit light there. Dental expenses are getting us lately too. Unexpected extraction/Implants were a hit this year LOL. Plus it’s getting more difficult to envision stomaching a 40% loss on equity investments as I get older (next downturn). I don’t know if holding 30% bonds (or more) would cushion the blow. Sometimes bonds and equities are more correlated than one thinks.

I think a good topic for discussion is whether allocating some amount to bonds would help cushion the blow during the retirement phase? Imagine your 1.5m portfolio is suddenly 900k. Would you be able to handle that when you’ve both given up your jobs?

Hi Ryan,

Good point, unexpected house expenses can be a surprise for sure. I suppose that’s where rainy day fund comes in handy. Luckily we are pretty good with dental expenses so far and I do plan to enroll us in extended health to cover these type of expenses.

Yup, agree that bonds is a good discussion point as bonds and equities sometimes are more correlated than ppl think. Something for future writing I suppose. 🙂