Let’s be honest here, inflation is real. Very real! Despite being as frugal and careful with our expenses as possible, we are seeing an increase in our living expenses; arguably, just like everyone else.

Unfortunately, many of these expenses are completely outside of our control…

- We were just informed by the city that our property tax increased by 11.5% this year

- Our monthly equalized Fortis-BC payment increased by 20% due to natural gas rate adjustments

- Gas prices recently hit over $2 per litre

- Groceries cost way more now. I mean, a bag of Hardbite chips is over $5, and avocado costs $2 at regular price? What is this, highway robbery?

Let’s not forget the rising interest rates, leading to higher mortgage payments.

And those are just core expenses. Now if we consider discretionary expenses as well…

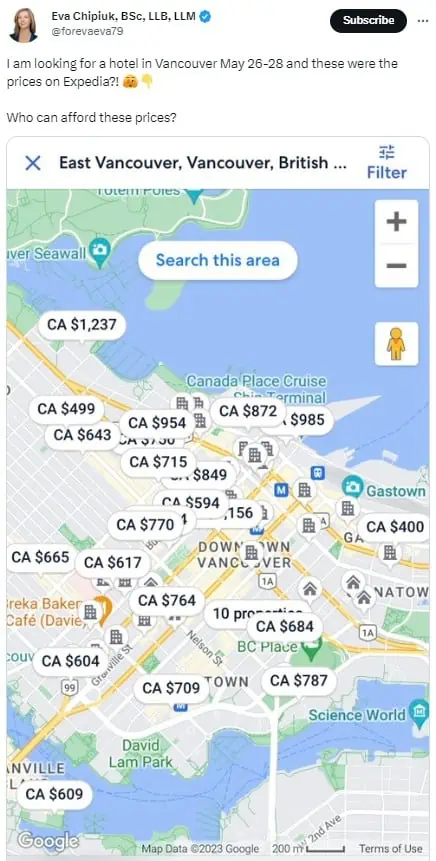

- It’s not unusual to see hotels at over $250 per night, or even over $300 and even $400! In fact, recently a lawyer complained about the hotel prices in Vancouver. And is not alone!

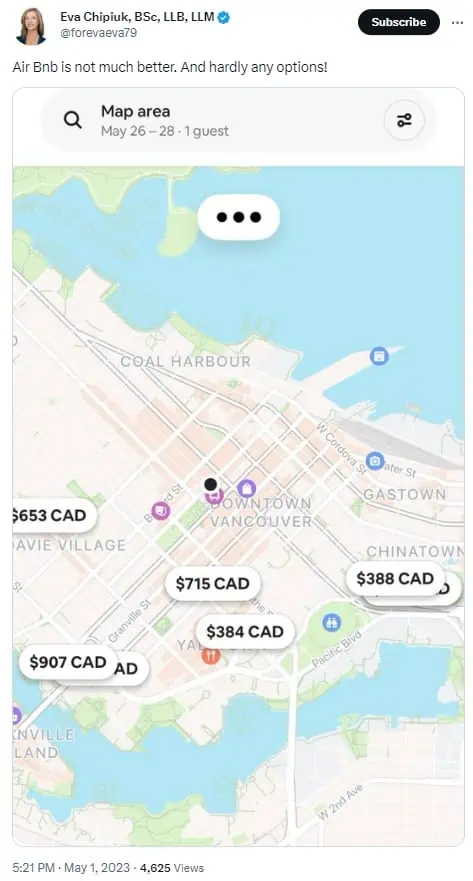

- Staying at an Airbnb is just as costly and sometimes it costs even more than staying at a regular hotel

- Airfares are far more expensive than pre-COVID. Good luck finding tickets to Europe for under $1,000 per person.

- Dining out is more expensive. A bowl of ramen costs close to $20 with taxes and tips added. We spent over $120 for the four of us dining out at a local White Spot last month, and we only had burgers, a couple of milkshakes, and a dessert to share.

You get the picture. At this point, I wouldn’t be surprised that our 2023 annual expenses will be considerably higher than the previous years.

Feeling frustrated with our expenses

The other day I was looking at our budget/expense tracking spreadsheet. To my horror, I noticed that we have been overspending in our Play account by a significant margin. To be more specific, we have dined out far more so far in 2023 than in other years. We have had three months where we spent over $1,000 on dining out! (On average, we usually spend around $350 on dining out per month)

While I know we’ve spent big money on a few occasions, like Kid T2.0’s birthday dinner with 15 people, a big dim sum lunch with 9 people, dinners a few times in Whistler with Mrs. T’s family, Mrs. T’s birthday lunch with 11 people, and celebrating our wedding anniversary, I was surprised to see that we spent over $1,000 on dining out for May.

Sure we ate out multiple times during our recent 4-day trip in Calgary, but that was around $500 in total. I couldn’t explain how we spent the other $500.

I was frustrated and bummed out about spending so much money dining out yet again. For the life of me, I couldn’t figure out how we spent the other $500. I did recall having takeout sushi for about $120 but I couldn’t think of other dining-out occasions.

After going through the credit card statements and spreadsheet, I realized we have had many smaller dining out expenses. $20 here and there, $30 here and there, and the amount quickly added up.

During this frustrated & annoyed state, the only thing I could think of was that we needed to take some extreme action.

“No dining out or take-outs for June!” I declared to Mrs. T.

“And what do you plan to spend our money on?” Mrs. T asked.

I couldn’t answer her question at all. All I could think of is that we need to reduce our spending, so we can save more. I think deep inside I was worried that we’d run out of money because of the increase in our overall expenses.

Even with me writing about having a save-spend balance (i.e. spending money to enjoy the present moment and saving money for the future), all I could think of are…

Save! Save! SAVE!

Unfortunately, my save, save, save, and save some more mentality was creeping in very quickly.

What the heck is going on here?

I went to bed frustrated and annoyed due to how much we’d spent on dining out, but more because I couldn’t answer Mrs. T’s question.

My realization – Points to consider

After a bit of pondering and soul searching, I questioned myself – Am I too focused on the end goal?

What do I mean by that?

Am I putting the goal of becoming financially independent and living off dividends by 2025 on a pedestal? Because that date is on the introduction of this blog, do I feel pressured in some sense that we are obligated to hit this target date? If not, am I a failure in the sense of readers and the FI community? And therefore am I putting a lot of pressure on myself, despite saying repeatedly that we don’t care whether we reach FI by the year 2025 or not?

Was I feeling frustrated with our expenses because that meant the $50-60k annual spending target is all of a sudden a moving target, which means we can never reach financial independence?

What exactly are we saving money for?

Even though I wrote about dying with zero, am I still thinking too much about my future life and my Taiwanese background and culture are pulling me toward the tradition of passing wealth (i.e. inheritance) to my kids and the future generations?

Am I valuing future life more than present life?

All these questions circled in my head and I was stuck in an endless loop.

Coincidentally Carl at 1500 Days wrote about What If You Run Out of Life? The post hit me right in the head. It was neat to get some insight from someone that’s ahead of us in the FI journey. That’s one of the reasons why I love the FI community so much.

As Carl puts it:

My goal is to optimize for right now, even if it means having a lot less money later on.

Would you rather have really rich experiences when you’re 50 or be really rich when you’re 80?

This makes me think about all the dining out experiences we had recently and put them into perspective:

- Mrs. T, Kid 1.0, Kid 2.0, and I had dinner at Barbarella in downtown Calgary. The food was awesome. We enjoyed ourselves, had a great time, and wrapped up our Calgary trip on a high note.

- Eating out with my parents, my brother’s family, and Mrs. T’s family, for a total of 15 people for Kid 2.0’s birthday was something we should really cherish. There aren’t too many chances that all of us could get together and have a big meal together.

- Celebrating our wedding anniversary made me realize how quickly time has passed by. I’d rather celebrate our anniversary every year with Mrs. T than not celebrate at all, meaning we aren’t together anymore…

- Celebrating Mrs. T’s birthday with my parents, my brother’s family, and our family was great. For the time being, we live relatively close so we can have meals together regularly, whether we eat at one of our homes or dine out. Years from now, we may not be able to have too many chances to eat meals together. I should enjoy these moments and get together opportunities.

Some more points to consider

We will reach financial independence. For us, it’s no longer a question of if we can reach financial independence. It’s a question of when. Perhaps there’s no need to focus and worry about the when. Enjoy the journey, we’ll get there when we get there.

We are not getting any younger. Mrs. T and I are in our early 40s. Neither of us is getting any younger. Both kids are at an age where they’re still young but can play by themselves for an extended period of time. They’re also at an age where they still want to hang out with us. Gaining memorable experiences now will be money well spent.

We are doing well financially. Instead of focusing on how much we spend, focus on how much we save for investments. We are doing well financially. Our dividend portfolio is on track to generate $49,000 in dividends this year. We have also invested quite a bit of money so far this year, most of that thanks to my company stock shares (we got acquired by another company so the equities I held got paid out) and last year’s annual bonus (we’ve been getting close to 0% bonus the last few years so it was nice to get something this year). I’m grateful & thankful for doing well financially and able to save and invest money.

Money vs. experience. “Nex time” is one of the most dangerous phrases in the world. There may not be a next time to have an experience. Appreciate the opportunity. It’s not all about money. Fear of missing out (FOMO) and saving every penny are two extremes. Find somewhere in the middle and the right balance.

Money vs. time. Value time more. We only have limited time in this world. Time is important.

When is money more impactful to kids. Paying for kids’ post secondary education, giving them a few thousand dollars when they enter their adulthood, or helping them out financially when they start a family will be way more impactful than giving them an inheritance when they are much older.

I keep coming back to these two things in my mind…

#1. When we visited Denmark for Christmas, we attended the local church service on the afternoon of the 24th (Denmark tradition). After the church service, we chatted with the owner of the local cheese store. Mrs. T used to work there when she was a teenager so she and the owner knew each other for a very long time.

One morning in February, Mrs. T was visibly upset. She found out that the owner of the local cheese store passed away due to an accident. He got pinned down by a forklift while moving some cheese blocks. His wife found him when he didn’t join for the daily afternoon hygge…

#2. We lost our beloved cat Perlemus just before Christmas 2021. It was really hard for all of us, because she lost her mobility so quickly, forcing us to have to make the tough decision to put her down. I have never experienced losing a pet until Perlemus. From time to time, I still think about her and how perhaps we took her for granted and could have spent more time with her.

These two things just reinforce the idea that we need to enjoy the present moment more and we absolutely can’t take life for granted. Everything we love will go away. Kid 1.0 is almost close to my shoulder height. In a few years, he will be a teenager. Similarly, Kid 2.0 is growing up fast and maturing in front of our eyes. Both will grow up and start their own lives. They’re not babies anymore.

Sadly, my parents and Mrs. T’s parents won’t be around forever. The time that we can spend with them is limited. Furthermore, as they age, it is less and less likely that we can do extended family trips together.

A few months ago my brother threw out the idea for my parents, his family and the four of us to go on an Alaska cruise together this summer. Initially, Mrs. T and I balked at the idea, because it was a lot of money and we didn’t think spending a week on a cruise was all that enjoyable.

But once we thought about the limited occasions we can find the time to do an extended family trip together and that life is extremely precious, we reconsidered.

Spending money now to gain memorable experiences makes a lot of sense.

So I shouldn’t get hung up on the big dining out expenses. Reduce how much we eat out but there’s no need to stop dining out completely. Eventually, things will balance out.

I’ll end this post with what Carl wrote which resonated a lot with me.

The ultimate call to action may result from thinking about growing old and death. Once you do this, it makes your time feel much more precious and urgent.

- Your kids will grow up and move out.

- Activities you love now like biking or skiing will become hard.

- Travel will eventually become difficult.

- Live long enough and you won’t even be able to walk.

To those who say this:

What if I run out of money?

I answer:

What if you run out of life?

When I was in my early thirties I created a plan to retire when I was 52. I was well on my way when I had a significant health event at the age of 47. After a serious conversation with my wife I decided to quit my high income/high stress job and take one I truly loved that allowed to spend more time at home at 50% of my former pay. We were able to live on my reduced income but could no longer save additional funds to our retirement accounts. I let what I had saved continue to grow and thanks to the magic of compounding was able to comfortably retire at 62 years. I have never regretted my choice even though it meant working 10 years longer than I had originally planned on.

one of best pieces of advice I have received is to recognize the value of plans but write them in pencil. Over the course of a life unplanned circumstances almost certainly will arise. Do not be afraid to change plans when circumstances change.

Thank you Paul for your feedback, always appreciate hearing from people that’s ahead of us on the journey.

You are fortunate to get food for 4 people in $120. In Northern BC, we spend that much for a dinner for just my spouse and I. When we visited Vancouver, we were shocked to find eating out to be so much cheaper than we are used to.

I can only imagine how expensive it is dining out in Northern BC. Things sure are getting more expensive.

I have more than doubled my eating out spending in the last year. I realized as well that it is the top social and networking thing that my wife and I do together. It is one of the top ways we enjoy spending time together but also it is how I network with & support my local community.

I also read Carl’s article and it is an important one to read, I am mindfully embracing that balance of planning for the future but living my life to the fullest. Thanks for linking to it Bob.

One last thing I want to leave here in the comments section, more as a commentary to the readership and not to you directly Bob. For many months now I have been doing weekly street walks and cleanups in the areas of town most impacted by our most at risk community from homeless to addicted and mental health issues to those squeezed by the cost of living and now on the edge. In this it has made reading a lot on twitter feeling disconnected for me and especially in the personal finance realm, it would do us all good to put our insane quality of lives, good fortune and immense privilege in check with some self reflection and realization that our lives are most likely the best they have been in history. With that privilege I hope we can consider ways to spend a little (even via taxes) to lift up those around us, especially because they have run out of money and worry every day if they will run out of life.

Chris you made a good point, it’s about supporting local community and local businesses as well.

Totally agree with you, we that are doing well financially can do more to help our community. Give back is important.

While well meaning, this is just adding fuel to the inflationary fires raging across our country. Most of us in general don’t need to be reminded to spend our money, we do plenty of that and the hotel prices you quoted are testament to that. We are at a time we need to remind ourselves to cut back and save more instead of YOLO’ing at every opportunity lest we miss out on an experience. Happy for you and your family enjoying your time, but it’s important to remember very few are in a position to say they can retire in the next couple of years.

That’s very true Michael. Thanks for that reminder.

Sounds like you and Mrs. T are a good balance for each other. Sometimes we need reminders to pull back and look at the big picture (in any direction really).

This post is a great reminder. We’ve been having similar conversations in our family and with our parents lately too.

Thanks Maria. Mrs. T gives me good advice and keeps me in check. 🙂

At first when I read the title I was like wait, Carl already wrote about this? but appreciate you expanding on the article, and catching ourselves when we aren’t “saving enough” without giving thought to the matter of what is it really all for, and does it matter if you reach your goal a little later so that you can enjoy the gift of presence now? Money doesn’t give you promises of life and vitality in the future.

Haha, I feel bad for stealing his title post idea. :p

We have also had some similar revelations of late. We booked our 25th anniversary trip to Newfoundland – our last maritime province to visit. At first I was reluctant to spend the money but now we’re super excited about going!

As for eating out, we find it more and more difficult to have a great experience. Restaurants are either too loud, too expensive, or the food is not great. But, we have become more willing to pay for premium ingredients and prepare more elaborate and enjoyable meals at home (notably, a result of my ability to continue working from home, and my love for cooking).

We are trying to take a more “here and now” approach instead of saving away every extra $0.01 and I think we are all better for it. There’s definitely a balance to strike and we are working to figure out where that is.

Hi James,

Newfoundland should be lots of fun. That’s the last Canadian province I haven’t been yet.

We’ve been doing a lot of takeout and only eat at restaurants here and there.

You have inspired me to book a river cruise. We are coming up to our 40th anniversary and I thought this would be a good way to celebrate. But I have been procrastinating because of the cost. No more, I will book it now.

As someone much older than you I am in awe of your journey. I wish I had realised at a younger age how to invest. We are comfortable but not rich. Decumulation is much harder than the saving!

That’s awesome I was able to inspire you to book a river cruise Christine. Interesting that decumulation is much harder than the saving, I’ve heard that from quite a few ppl ahead of us on the FIRE journey.

I really liked this article as I also noticed that our eating out has increased quite a lot and sometimes I feel frustrated. But in the end living your present is really important as you rightly said “what if you run out of life?”

Thanks

Thank you Raj. It sure is getting expensive out there. 🙂

I loved this article!! We all have that friend that everyone says is “cheap” but at the same time they miss out on many memory making activities. Our kids (11/13) are still at the age where hanging out with us is ok but it’s very near where friends will take priority. Anyway, just wanted to say enjoyed the article. I frequently have to “check myself” when going over our expenses and remind myself to live in the “now”. Yes I wish we saved more (which itself is getting harder with all the rising costs) but wouldn’t give up watching the kiddos excel at their activities they are in or talk excitedly about a recent adventure.

Well done, all the best!

Thank you Chris, appreciate your kind words. Living in the now is important for sure. It’s about finding that right personal balance and that could be hard from time to time.

Thank you for this extremely important post. Tomorrow is promised to no one. I have to remind myself that there are no guarantees, that money is meant to be enjoyed, and that saving incrementally more won’t make me outrageously happier should I live to be very, very old. Finding the balance between spending today and saving for tomorrow is a never-ending challenge for me. Running out of life is gradually becoming the bigger concern!

You’re very welcome. It’s important for me to have this realization from time to time as well.

how about running in laps? first lap is to ensure FIRE, second is to strengthen your relationships with everyone, third is to up your game and really enjoy life, and the fourth is to ensure a better future for your family.

That’s a good way to think about it. But I’d argue that strengthen your relationships with everyone doesn’t have to wait until you reach FIRE.

Well thought out.

Thanks.

Thank you Ted.