Recently a reader emailed me about a big windfall that he received.

“Hi Bob, I recently received a pretty significant windfall… $5 million! To be honest, I’m not sure what to do. I want to invest all the money rather than spend a portion of it on a fabulous vacation. Should I consider dividend growth investing and set up a passive income portfolio? Or should I look at private investment firms and consider alternative investment options?”

First of all, congrats on receiving such a big windfall. That’s definitely large enough money to set you and your family up for a very good future. However, it is important to have some investment strategies so that money can grow.

Let’s not forget that people who receive a large sum of money, from winning the lottery, for example, are likely to lose all their winnings and declare bankruptcy within three to five years. There are abundant researches that underscore this sad reality.

I certainly don’t want that to happen to this reader.

So as a fun exercise, here’s what I’d do with a $5 million windfall.

What to do with a $5 million windfall

With a $5 million windfall, the most important factor is not only to preserve the capital and make sure it can grow to a bigger amount in future years. Furthermore, it’s important to have the $5 million working hard for you so you don’t have to.

Since the reader doesn’t want to spend any of the $5 million and wants to invest it all, I will base my windfall deployment plan according to this wish.

So what would I do if we were to receive a $5 million windfall?

First, I’d divide the amount into 3 budgets – two buckets with $1 million each then another bucket with $3 million. Each bucket is to be used for a different purpose.

Let me explain the purpose of each bucket.

Bucket #1 – Donation Machine

It has been a dream of mine to write a $1 million cheque and donate it to a local charity. But instead of just donating this entire sum all at once, wouldn’t it be better if I set up a perpetual donation machine?

To keep life easy, I’d invest in one of the top Canadian dividend ETFs. Considering all the available ETFs, the MER fees, and the distribution yields, I’d pick XEI over other dividend ETFs.

At the time of writing XEI has an MER of 0.22% with a distribution yield of 4.84%. The top ten holdings are BCE, Telus, TC Energy Corp, Enbridge, Canadian Natural Resources, Royal Bank, TD, Fortis, Bank of Montreal, and Suncor. We own all these companies in our dividend portfolio so I’m comfortable with the structure of XEI. Since its inception date of April 12, 2011, XEI has had a total return of 7.05%.

At a 4.84% yield, this bucket with $1 million would generate $48.4k per year. I’d then donate the entire distribution to a charity of choice each year. My expectation is that the value of this bucket will appreciate over time and the annual distribution amount would as well.

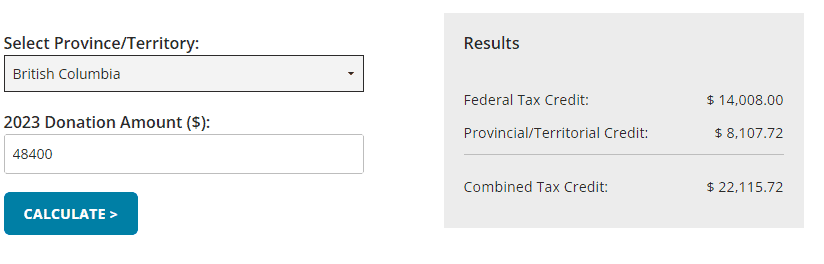

Per the Canadian Red Cross’ donor tax credit calculator, donating $48.4k per year will provide a federal tax credit of $14,008 and a provincial credit of $8,107.72. The combined tax credit of $22,115.72 can then be used to reduce any income we’d have in the same tax year.

Bucket #2 – Speculative investments

The $1M in bucket #2 will be used for alternative investments, potentially higher risk and more speculative. What kind of alternative investments do I have in mind?

Well, investments like venture capital funds, hedge funds, private equity funds, small businesses, or even pre-IPO private companies. For these alternative investments, usually, you’d need to go through a private wealth management firm. All of these firms have a minimum investment amount and $1M is usually the required minimum amount.

The idea for this bucket is to speculate and potentially turn the $1M into something much bigger. Because of the speculative nature, there’s a high probability that we might lose a significant portion of the money. The goal is to have a few home runs out of all the investments to make the big gains.

Alternatively, I can skip the alternative investments idea and just invest in 10 mega international companies in equal weighting ($100k CAD each, or whatever USD equivalent is). The companies I’d invest in are:

- Apple – one of the most well recognized companies in the world generating billions of revenue each quarter.

- Microsoft – another well known tech company with solid growth in the cloud business and starting AI.

- Alphabet – Can you imagine life without Alphabet products? I can’t.

- Amazon – another tech company. I really like Amazon’s cloud business.

- Coca-Cola – there’s a reason why Warren Buffett continues to invest in Coca-Cola

- Costco – people will continue to shop at Costco for many years to come

- Visa – another well known name with global power

- Waste Management – I love the garbage business

- Tesla – EV evolution and Tesla is way ahead of its competition

- BlackRock – generating revenues from ETFs

Since most of these stocks pay very little in dividends or no dividends at all, I wouldn’t worry too much about US dividends and the 15% withholding tax in a non-registered account.

Bucket #3 – Passive Income Machine

After taking care of the donation and speculative portion, I’d use the last $3 million in bucket #3 to create a passive income machine.

The idea is to generate enough passive income for us to live off dividends, allowing us to have the ability to decide what we want to do with our free time. Essentially we’d have a work optional life (or financial independence work on my own terms, FIWOOT). We can focus on spending time on our passions, regardless of whether these passion projects generate money or not.

Since we plan to live off this passive income, I’d want to be more hands-on, but at the same time, keep the portfolio as simple to manage as possible. Asset diversification and geographical diversification will be very important for this portfolio.

The entire $3 million would be invested inside a non-registered account, so tax efficiency will need to be taken into consideration too.

How would I construct this passive income machine portfolio? For the most part, I’d mimic this portfolio very closely to our current dividend portfolio by utilizing an index ETF and some of the best Canadian dividend stocks.

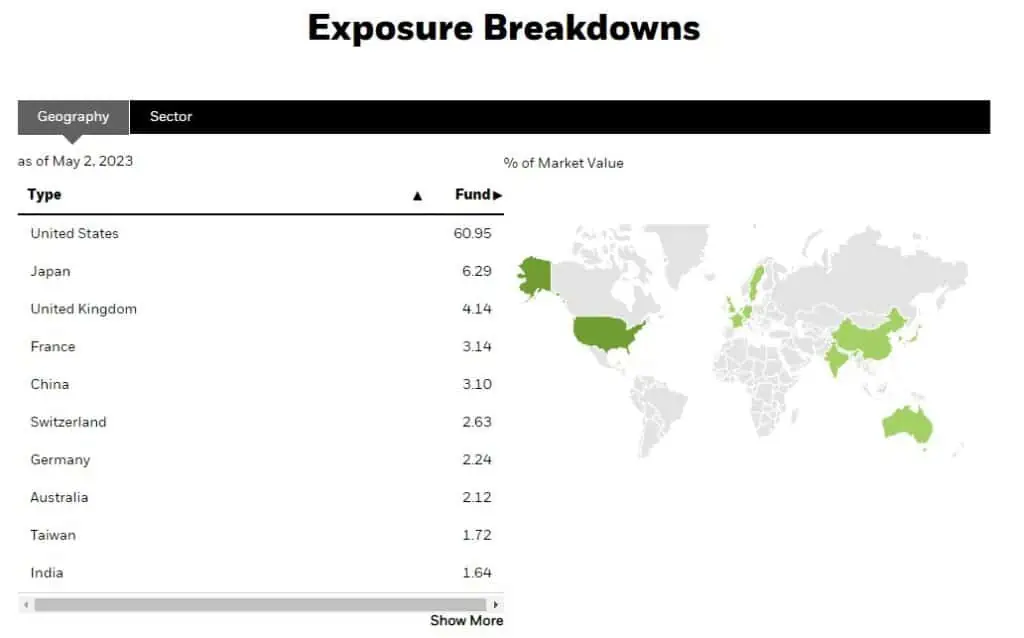

First, I’d allocate a third of the $3 million, or $1M for investing in a diversified index ETF. My choice of the index ETF would be XAW, the iShares ex-Canada index ETF, to provide international exposure.

XAW currently has 60.95% exposure to the US market, 6.29% to the Japanese market, 4.14% to the UK market, and 3.14$ to the French market. Since there are many multi-billion international companies based in the US, the high exposure to the US market shouldn’t be a concern.

The top ten XAW holdings are Apple, Microsoft, Amazon, Nvidia, Alphabet, Berkshire Hathaway, Meta, United Health, and Exxon Mobil. All of these are US based companies.

XAW currently has a distribution yield of 1.66%. So with $1M invested, that’d result in $16.6k in distribution annually.

For the rest of the $2 million, I’d then pick 20 Canadian dividend stocks and divide the money equally across the 20 holdings, or $100k per stock.

The 20 Canadian dividend stocks I’d pick and my reasoning:

- Royal Bank (4.03% yield) – the biggest bank in Canada with dividend history from the late 1800s. It’s literally a money generating machine.

- TD (4.71% yield) – another Canadian bank giant with a large exposure in the US.

- National Bank (3.88% yield) – the smallest bank of the Big Six. National Bank has done quite well over the past 5 years and I believe will continue to perform.

- EQB Inc. (2.37% yield) – a 2nd tier Canadian bank that has been growing rapidly with a high dividend growth rate in the past number of years.

- Intact Financial (2.19% yield) – one of the largest Canadian insurance companies with 18 years of dividend growth history.

- Manulife (5.49% yield) – another Canadian insurance company that’s not going away anytime soon. Manulife has solid exposure outside of Canada as well.

- Brookfield Asset Management (3.94% yield) – a leading global alternative asset manager with over 4750 billion of assets under management across real estate, infrastructure, renewable power, private equity, and credit.

- Canadian Natural Resources (4.71% yield) – a solid pick in the Canadian energy sector. CNQ didn’t cut dividends during the pandemic, unlike many of its counterparts.

- Enbridge (6.7% yield) – with a pipeline network of around 192,000 miles across North America and the Gulf of Mexico, Enbridge plays a vital part in supplying North America with natural gas and crude oil. We definitely rely on Enbridge’s services on a daily basis.

- TC Energy Corp (6.68%) – natural gas and crude oil aren’t going away anytime soon and we’ll need to continue to rely on TRP’s services for many years to come.

- Fortis (3.74% yield) – Fortis has been raising dividends for almost 50 years. There’s only one other Canadian company (Canadian Utilities) that has a similar dividend growth streak.

- Emera (4.68% yield) – another solid utility company with 16 years of dividend growth streak.

- Brookfield Renewable Corp (4.0% yield) – we like renewable energy therefore we think it makes sense to invest in BEPC. BEPC is one of the entities under the Brookfield empire so we know it will be well managed.

- Canadian Tire (3.96% yield) – a well known company with many different brands here in Canada and internationally.

- Alimentation Couche-Tard (0.74% yield) – the dividend yield is extremely low but ATD has been raising its dividends at an impressive rate over the few years. The share price also has been on a roll.

- Metro (1.55% yield) – since there aren’t too many Canadian consumer stables to pick from, I thought Metro is a good choice given its 28 years of dividend growth streak with a 15 year dividend growth rate of 14.2%.

- Canadian National Railway (1.97% yield) – an important company for providing transportation services across North America.

- Waste Connections (0.54%) – while the yield is extremely low, WCN has been raising dividends consistently with a 14.4% dividend growth rate for the last 10 years. We’ll continue generating garbage and WCN will be around to clean it up while charge money for the garbage removal service.

- BCE (5.92% yield) – can’t go wrong with one of the big three Canadian telecommunication companies.

- Telus (5.13% yield) – another Canadian telecommunication company that’s generating lots of revenues from our data addiction.

Summary:

| Ticker | Amount | Yield | Dividends |

| RY | $ 100,000 | 4.03% | $ 4,030.00 |

| TD | $ 100,000 | 4.71% | $ 4,710.00 |

| NA | $ 100,000 | 3.88% | $ 3,880.00 |

| EQB | $ 100,000 | 2.37% | $ 2,370.00 |

| IFC | $ 100,000 | 2.19% | $ 2,190.00 |

| MFC | $ 100,000 | 5.49% | $ 5,490.00 |

| BAM | $ 100,000 | 3.94% | $ 3,940.00 |

| CNQ | $ 100,000 | 4.71% | $ 4,710.00 |

| ENB | $ 100,000 | 6.70% | $ 6,700.00 |

| TRP | $ 100,000 | 6.68% | $ 6,680.00 |

| FTS | $ 100,000 | 3.74% | $ 3,740.00 |

| EMA | $ 100,000 | 4.68% | $ 4,680.00 |

| BEPC | $ 100,000 | 4.00% | $ 4,000.00 |

| CTC.A | $ 100,000 | 3.96% | $ 3,960.00 |

| ATD | $ 100,000 | 0.74% | $ 740.00 |

| MRU | $ 100,000 | 1.55% | $ 1,550.00 |

| CNR | $ 100,000 | 1.97% | $ 1,970.00 |

| WCN | $ 100,000 | 0.54% | $ 540.00 |

| BCE | $ 100,000 | 5.92% | $ 5,920.00 |

| T | $ 100,000 | 5.13% | $ 5,130.00 |

Dividend per year from 20 dividend stocks: $76,930

Total annual dividends & ETF distributions: $93,530

Considering that we have been spending around $40k a year in core expenses and we estimate the need for $60k a year in passive income to sustain our current lifestyle, a total annual dividend income of $93,530 is more than sufficient for us.

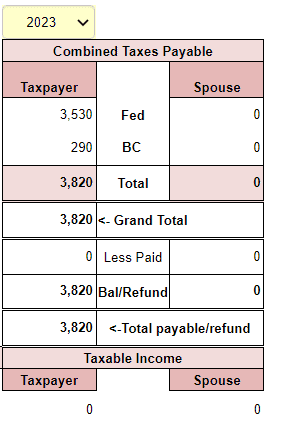

If we put all the dividend income and donations under me and use the Taxtips.ca Tax Calculator (ignoring foreign tax credits entirely and all other possible income), we would not be paying any taxes at all.

Even if we ignore the donation portion entirely, we’d only be paying $3,820 worth of taxes.

In other words, income from the passive income machine is very tax efficient. There are probably additional measures we can take to be even more tax efficient, but for this post, we’ll ignore those.

For the 20 dividend stocks, I did an equal weight distribution. If we really need more dividend income, we can change the distribution slightly and focus more on higher yield stocks.

Another approach is to reduce the XAW exposure and put more money on the 20 dividend paying stocks, but we’d be reducing the international exposure.

Summary – What to do with a $5 million windfall

If we were to receive a $5 million windfall, I’d divide the money into three buckets and invest the money differently and have the money working hard for us in different ways. I invested all $5 million of the windfall based on the reader’s comment of not wanting to spend any of it.

Having said that, if we were to receive a $5 million windfall, Mrs. T and I would likely allocate about $200k or so for a vacation, allowing us to explore different parts of the world. We’d likely set aside some money for real estate investing and helping out families. All that money would come out from bucket #2, leaving us with a smaller amount of money for speculative investing. We’d leave the donation machine and passive income machine amount unchanged.

Dear readers, what would you do with a $5 million windfall? Would you spend or invest it all? Or would you spend it all?

Hi Bob,

Your bucket #3 is exactly what I was looking for in an article. I want to thank you for this article.

I have a question about the article though, I ran the numbers in TaxTips.ca for the case ignoring donations. I am still puzzled on how you get such a low tax amount ($3,820). Here is how I am doing it:

From the dividend per year from 20 dividend stocks: $76,930

$1M ETF Distribution annually: $16.600

Total annual dividends & ETF distributions: $93,530

I reported the $76,930 as Cdn dividends eligible, and the $16,600 as Cdn non-eligible dividends. Did I get that wrong?

Thank you very much,

You’re very welcome Lenny. For taxtips calculation I’m assuming taht the amount is split between me and Mrs. T.

Not sure if this money if from inheritance or settlement if anything, but great steps they are taking for their future! Taking a $10k vacation or so is no problem out of the $5 million, and the steps you lined up including the donation machine/Donor Advised Fund are good recommendations.

Agree that using the money for a vacation is a good idea. 🙂

Great article! I enjoyed reading what you would do with 5 million. Having income generated from the 1 million for donations is a very cool idea.

However, personally, I would not allocate 1 million to alternative investments. That is 20% of the money is very high risk investments. I guess I would have a more conservative approach.

Thanks for this thought provoking article.

Thank you Jyoti.

LOVE the concept of Passive Income Machine / Donation Machine!

Thank you Pierre.

Glen: The GIC suggestion is fabulous. I just checked with my Bank Manager at the BNS, and he has a GIC at 4.5% for two years. However, it’s not locked in, and you can take out any amount of money at any time (amazing!) and not pay a fee or lose any of your interest. I’m contemplating a purchase, but can’t decide how much vs. equities. What would be a decent amount vs. equities for a total purchase of $85K?

Hi Laurie,

Definitely consider the tax consequences between investing in equities vs. GICs. GICs are taxed at your marginal tax rate where as capital gain is 50% of your marginal tax rate.

What an interesting approach to a good problem to have . Great article which anyone even without this windfall can adopt to

Thank you Naveena.

Personally for me Bob, if I inherited 5 million, I would clear off all debt including my house mortgage, car loans and of course, locs and credit cards. I know some may feel paying off a mortgage is a crazy thing…but again this is just me.

Why do I think this? Because all debt assumes the future. And in my personal life experience there have been some significant health challenges with my spouse and other family members that have strongly reinforced that point. I’ve also heard it said that almost everyone who goes bankrupt has debt they can’t pay. I’m a big fan of owing no one anything.

Second, I would have several so called smaller buckets such as maintaining a chequing balance bigger than any cheque I would ever write over the course of a year. I like the idea of having 10 or 20 thousand as a balance.

Thirdly, I have a friend who is a successful trader and he has put aside three years of living expenses in short term bonds at his bank that roll over every three months. He is also debt free. My friend tells me that these two steps have given him and his wife a peace of mind that they have a hard time describing. There is something about having three years of expenses already accounted for that would make me feel good about the next few years. I have a feeling I would feel differently about things knowing that if everything crashed I would be just fine for a few years.

Fourthly, I would do the dream vacation and see the things I’ve always wanted to see and take family with us. There is a difference between looking at something in a book and seeing it in front of you.

Lastly, I would invest in solid dividend stocks and establish that ongoing income stream while paying attention to my geographical exposures and tax implications.

I like things simple. And I like no stress. Being debt free including my home with lots of money in various buckets and a solid passive income stream would free me up mentally to really focus on those important things like friends and family without having all the regular stresses impacting those relationships.

Lastly, having money to give away is the real bonus once my personal situation is fully taken care of. And if one is able to also donate some time as well as some money to worthy causes, one can make a real impact.

Great article Bob. Always enjoy your posts. Have a good day.!

I love your ideas in addition to Bob’s. Now I just need the $5M!

Hi Sean,

I guess I forgot to mention that the assumption is that all the debts are paid off.

I like the idea of having some money around in case you need to write a cheque for anything big during the year. Interesting idea about short term bonds, something to consider for sure.

I don’t have 5 million dollars, but I love your 20 stocks suggestion.

Thank you Fil.

Nice problem to have! Don’t ignore fixed income, eg. GICs ~4-5%.

Very true especially the rate going up higher and higher. However, need to consider how GICs are taxed at the end.

Loved this article.

Very interesting “bucket lists”, well thought out.

Congrats to the lucky reader who reached out for your advise. I’m sure he will do very well given his wisdom in seeking to invest it.

I strongly believe in charity and have always found that giving to others less fortunate, church, etc, is the most rewarding way to spend one’s money. Liked your comments on this Tawcan….with an interesting twist with the tax perspective.

Thanks Garry. The tax credit is just extra gravy IMO.

Fabulous article, and even though I don’t have a $5 million windfall, the advice still appears sound for a smaller amount, like the $85 k that I’ve just inherited. Many thanks.

You’re welcome Laurie.

Great article.

I’ve always wondered what to do with a windfall.

The big question is when to buy?

All of them at once now ? Or wait for a correction? Wait for tax loss selling in December?

Some of those names like MSFT are at all time highs .

But good thing with 5% money markets , it pays to wait .

I always believe “charity begins at home “ but those tax credits for donations can be helpful . Is there not a limit for donations?

Thanks

Thanks. There are lots studies that indicate it’s better to just buy everything at once, but that’s very difficult to do psychologically. It comes down to know yourself as an investor.

Don’t believe there’s a limit for donations but I could be wrong.