Growing up, I used to spend a lot of time playing with LEGO. I had received LEGO sets as presents over the years and kept the pieces from these sets in a big plastic container. For some reason, after finishing building each LEGO set, I would take it a part, and try to make my own structures by combining the different pieces together. My favourite things to build were spaceships and submarines. I would build a spaceship or submarine and play with it in my imaginary world. I was able to keep myself entertained for hours by playing with LEGO. It also helped that my younger brother was as enthusiastic about LEGO as I was.

Since Mrs. T is from Denmark, it shouldn’t come as a surprise that she had a similar upbringing with LEGO as me. We both think LEGO is a great toy for kids. So, when Baby T1.0 was around 2, we purchased a few Duplo sets for him to get him started. After he turned 3, Mrs. T and I, and our family started giving him small LEGO sets for birthday and Christmas presents. At 4 years old, he now has multiple different LEGO sets. Although the recommended age for some of these sets are 6 and up, we took a very liberal approach and just let Baby T1.0 play with the LEGO sets with some adult supervision. When he was 3, we had to find the pieces and helped him with the instructions. It would take days to finish building a set. The process of LEGO set building has gotten much easier since he turned 4 late last year. He is now able to follow the build instructions more or less by himself and sometimes look for the pieces himself. As a parent, it has been very cool to see such progression.

LEGO building

Baby T1.0 has a tendency to build the different sets per the instructions, plays with the sets for a few days, then takes them apart. We got him a plastic container to keep all the different LEGO pieces in. Once he deconstructs the different sets, he tends to build his own LEGO structures (i.e. planes, cars, ships, buildings, etc). After he plays with his own constructions for a while, he takes them apart and builds the different sets per the instructions again. This cycle repeats itself over and over. (I wonder where he got that from).

I often spend father & son quality time playing LEGO with him. When he is in the “building per the instructions” phase, I usually help him out by finding LEGO pieces he needs from the plastic container.

Because there are a few different sets in the container, there are many small LEGO pieces. It often takes me a few minutes or longer to find the specific piece that Baby T1.0 needs.

The other day, Baby T1.0 and I were building a camper car from scratch. After the first few sets of instructions, I had to look for the trailer hitch piece, which was very small and black in colour. (When Baby T1.0 read the instruction, he said, “oh daddy, this is a tricky piece to find”). After spending 5 minutes going back and forth in the container, I couldn’t find the piece. I ended up spending probably another 5 or 10 minutes going back and forth in the container before I could find it. The trailer hitch piece looked the same as many other parts, so it was extremely difficult to find. During the time that I was digging through the plastic container, I sensed a bit of anxiety, frustration, and discouragement.

As we continued building the camper car, taking out more and more LEGO pieces from the plastic container, it became easier and easier to find the other pieces we needed, because there were less LEGO pieces in the container. Therefore, our construction progress went faster and faster as we built.

LEGO & the FIRE journey

During the process, I couldn’t help but compare this experience to the financial independence retire early (FIRE) journey.

Trying to find a LEGO piece in a large container took a long time at first. But as we started taking out more and more pieces from the container, it became easier and easier to navigate the container and finding the pieces we needed. This is a little bit like compounding. It can take several years of saving, getting out of debt, and investing before you start seeing the effect of compounding. After compounding starts kicking in, that’s where the magic happens.

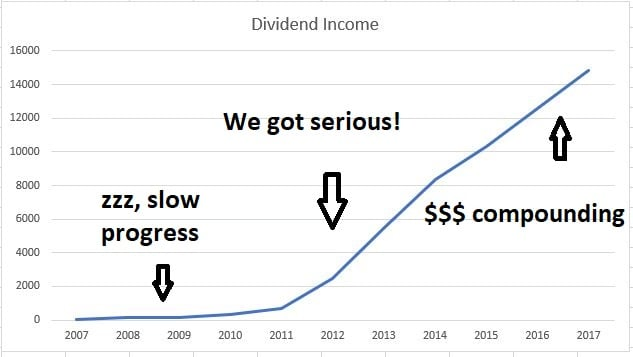

This is certainly the case for our dividend income. From 2007 to 2010, dividend income was not our prime focus. The dividend income was relatively flat as a result. We started getting serious in 2011 and started investing large sums of money into our dividend portfolio consistently. As we invested more and more money into the portfolio, the dividend income started to pick up. We are now receiving over $1,300 of dividend income each month. By utilizing dividend reinvestment plan (DRIP), organic dividend growth, reinvesting dividends received, and investing of new capital, we are seeing the magical compounding effect each month.

Growing net worth takes time

The same thing happens with our net worth as well. When I graduated from university in 2006 and entered the work force shortly after, it took me months to get my net worth to the $20k level. I distinctly remembered patting myself on the back for reaching $20k net worth. I had purchased on Honda Civic when I started working and the car cost about $20k once all the purchasing costs were added. At $20k net worth, that meant I had enough money to buy a Honda Civic with cash if I wanted to. It felt like a small financial victory to me.

However, going from $20k net worth to $100k net worth took a while (almost 3 years, by then I was 27 years old). It was during the financial crisis when I reached this milestone. During this turmoil time, I had wondered if my net worth would ever increase, as my investments kept decreasing in value. At times, I was frustrated and discouraged because the bear market and my net worth was going in the negative direction. My work had laid off about 20% of the work force. Those us that didn’t get laid off were told that our salary would remain the same and the salary increase over the next few years would be extremely low. It didn’t matter what I was investing in, mutual funds, GIC’s, or stocks, they weren’t performing that well at all. I felt like it was OK to panic and to scream at the top of my lungs to express my frustrations with my finances.

Going from the $100k net worth milestone to the next few-hundred grant milestones took a while. It took a lot of declines and hard work to make sure my net worth would keep growing. I read about the magic of compounding and totally understood the math behind it, but I wasn’t seeing the magic of compounding working for net worth. I felt frustrated and discouraged. I was saving for the future, while many people I knew were living it up, practicing YOLO. It was hard keeping myself in check and not jump to the YOLO side.

It was quite interesting that during our LEGO building process, I had similar feelings as how I felt when I first started building my net worth. I was frustrated and discouraged because I couldn’t find the piece we needed. But I decided to stick to my plan, continued looking for the LEGO piece, and eventually found the piece. If we had given up when I felt frustrated and discouraged, Baby T1.0 and I wouldn’t have been able to complete building the camper car.

Similarly, it would have been easy to give up on looking after my finances when I first started working. It would have been easy to just practice YOLO rather than saving large amount of pay cheque every two weeks and investing in appreciating assets. It was so easy to give up when I felt frustrated and discouraged during the financial crisis or when my employer decided to freeze my salary.

But I stuck to my gun.

Now, 12 years after I stepped into the work force, my life has changed significantly. I am now married, and have two kids and I am the primary source of income for our family. However, thanks to being responsible with our finances and executing our investment strategies, our net worth has grown significantly. My full time job is generating good income, and our side gigs are bringing in some income too. But what really fuelled our net worth growth are our high savings rate and our commitment to continue investing regardless of what the market is doing.

The compounding effect is now really taking off in the last couple of years due to our investments of different assets, like our house, our stock portfolio, and other investments.

Don’t panic on your slow progress on the financial independence journey

What I am starting to realize is that it takes years to start seeing a significant financial progress. In the beginning, it may feel like you aren’t going anywhere. Don’t panic and don’t get discouraged by this.

I am certainly not the only one that feels this way. Tanja and Mark at Our Next Life felt the same too.

Rather than feeling discouraged, frustrated, and other negative thoughts about your lack of financial progress, congratulate yourself for taking action to improve your financial life. Do tell yourself that you are doing the right thing and you will be much better off financially 10 years from now.

At the beginning it may look pretty bleak, but I can guarantee you that things will get better. The important thing is that you are making improvements. In a year from now, you will thank yourself for starting today.

If you ever need to get a positive lift, reach out to people in the personal finance community and connect with them. One thing I have found is that everyone in the personal finance community, and especially the FIRE community, is friendly and extremely helpful. Connect with people that you feel a personal connection to and help and encourage each other.

It sure is a lot more fun to be on the FIRE journey with other people vs. doing alone.

PS. For the last few weeks I have been participating in the Rockstar Rumble at Rockstar Finance. My post “How my struggles with English taught me about financial literacy” has made it to the final 8!

Today the final 8 posts are battling it. I am up against Jim Wang from Wallet Hacks. I would really appreciate if you can vote for “Literacy” in Game 3 to help me get to the semi-final! Thank you!

Again please vote for “Literacy” in Game 3 by clicking here. Thank you!

It’s neat to read more of your story Bob – growing up with Lego’s myself, I enjoyed building things from the instructions and making my own creations. I had a submarine with a shark canopy and little crane arms with magnetic hooks. It was awesome!

Last month I also crossed net worth of 20k! It was a great feeling 🙂

Congrats on crossing the $20k net worth milestone! That’s awesome!

I think too many people compare themselves to their similar-age group peers in life financially. But the simple reality is that life isn’t a straight line. Some people who are ahead of you right now might be behind you later in life. Slow and steady wins the race.

Our first few years out of college it felt like we weren’t making much financial progress. We were paying off our student loan debts, saving for a down payment, and paid $10k for our wedding. But eventually we started seeing our savings and earnings pay off and our net worth grow. I love the analogy with the legos!

Thank you Mrs. Kiwi. When you are paying off debts, saving for a down payment, and paying for a wedding, it can be discouraging because you aren’t seeing much progress. But soon after you’ll see the savings really compounding. That’s the beauty.

Wow great graph. Massive growth once you became serious. It would probably be hard buying in a bear market for sure. Like you said though worked out great long term.

Keep it up

Thanks man, it was hard to be buying in a bear market. 🙂

One step at a time … if you work at least 15 years before retirement you will receive a national and provincial pension ….. if not you need to build up your own pension only by yourself…. which affects those non resident Canadians overseas to who don’t meet the 15 contribution minimum

That’s true about the federal & provincial pension, something to think about. 🙂

I think things like lego and doing puzzles are great training for a path to FI. You start out and it looks like you’re going nowhere, a piece here and piece there, no real structure. Then one day it starts looking real!

I was big into model cars as a kid, kinda the same thing. They had a thousand pieces and it took persistence. Great teaching tool.

Good call on puzzles too, especially ones with a few hundred pieces. It certainly takes a long time to get started and making some small progress.

What a great post Bob, love the LEGO reference! It can absolutely be discouraging when you are just getting started with either paying off debt or building wealth because it can be just a slow process. It does pay to stick with it though and after consistently putting money away it will start to build on itself making the progress more and more exciting.

Thank you Sarah. If you stick with it long enough, it does pay off. That’s why it’s so important to look at the big picture.

Yeah it is a slow go at the onset but on the flip side it is the only time you brag your annual dividend is increasing in massive triple digit percentage jumps 😀 Today I throw a couple thousand at the portfolio and it barely hiccups an increase.

Haha you’re right, the triple digit percentage jumps are nice to see at the beginning.

Totally agree! It’s a bit frustrating at the start, no doubt about that, but if you stick with it it will pay off 🙂 Honestly I am a big ‘set it and forget it’ fan and find that I don’t even care about the slow progress anymore haha

That why making every automatic is a great idea (i.e. pay yourself, invest regularly, etc)

Ahhh, the magic of DRIP and compound interest!

I can understand getting frustrated with slow progress but I hope those that do, trust in the process. As you said “tell yourself you’re doing the right thing.”

Good luck in the Rumble!

Trust in the process. Love that! 🙂

Great post Bob, the feeling of slow process to FIRE is mutual. it’s hard to keep focussed for a long time while seeing “little” progress. Have not found out how to make this feel better yet myself! Albeit the occasional trip or mini break does help make it more “bearable”!

It can be hard to stay focused for such a long time but you need to keep reminding yourself the end goal to stay motivated, especially when you feel discouraged. 🙂

Lot of truth in this post. When I first read about FIRE it took me a good year or two to start saving and changing things. First I got a higher paying job and then started to bike to work. It all continued from there.

I think the panic while saving can also be addressed by living in the moment. While quitting your job or travel keeps you motivated, your day to day life must be lived today. I think that helps me forget about the money management until my next payday.

It does take a few years to feel that you have made some changes.

Living in the moment is great but you want to consider the future too. It’s finding that right personal balance.

Piling money in during a bear market had to be so frustrating. Good for you for continuing to slog on even when you didn’t get the automatic awesome returns we’ve seen over most of this decade. I’d say you’re better set up to weather the next downturn because of it though.

Voted for you! 🙂

Thanks Angela. It was tough to continue to slog and invest during the downturn, but it paid off years down the road.

Ah, yes, discouragement can some in many forms, even around dividend investments. The very slow start and the seemingly paltry sums that we first get can seem like all downers.

But if we persist, we seem wonderful rewards. I engaged in dividend reinvestment too.

Some ways I took to beat discouragement:

1. I keep a spreadsheet with one page for each investment, plus a summary page. This allows me to look back and see the differences between when I started and now.

2. I set goals for myself. Like, in any one investment, for example, set a goal for one new share per year.

Then when that is achieved, set a goal for one new share per quarter.

And so on!

Good luck!

The slow start can be a downer and it’s definitely a good idea to persist. 🙂

I love the keeping a summary page, it shows precise progress and can give encouragement along the way. 🙂