Well, Algonquin Power & Utilities Corp (AQN.TO / AQN) sure has seen better days in the past. On November 11, AQN reported their Q3 earnings, and the stock fell by more than 19% that very same day, then another 14% the next day. Clearly, the market did not like what the company said in their latest earnings report.

As you can see from the chart below, AQN has performed extremely poorly year to date.

Down 45.15% year to date. Ouch! As a fellow AQN shareholder, I certainly felt that pain.

In recent days, many readers have left comments and sent me emails asking what I think about AQN. Is AQN still a buy? Is the dividend safe?

I used to believe that at around $15, AQN was underpriced, despite its debt level. I also believed that AQN’s dividend was safe. But do I still have the same beliefs after the Q3 earnings?

Thus, what a better exercise for myself and readers by going through Algonquin Power & Utilities Corp’s Q3 press release, earnings report, and investor presentation and answering the following key questions that many readers, us included, have in mind:

- What happened that caused AQN’s price to tank?

- Is AQN still a buy at the current price?

- Is AQN’s dividend safe?

For those readers that missed it, you might want to take a look at the post I wrote a while ago on how to read annual and quarterly reports. To be able to read annual and quarterly reports and dissect all the info from the reports is a useful and vital skill to have if you want to become a better investor.

AQN Earnings Summary

So what happened in AQN’s Q3 earnings that spooked the market and had investors dumping their AQN shares like hot potatoes and resulting in a massive share price slide?

First, let’s take a look at the Q3 press release and the earnings call script.

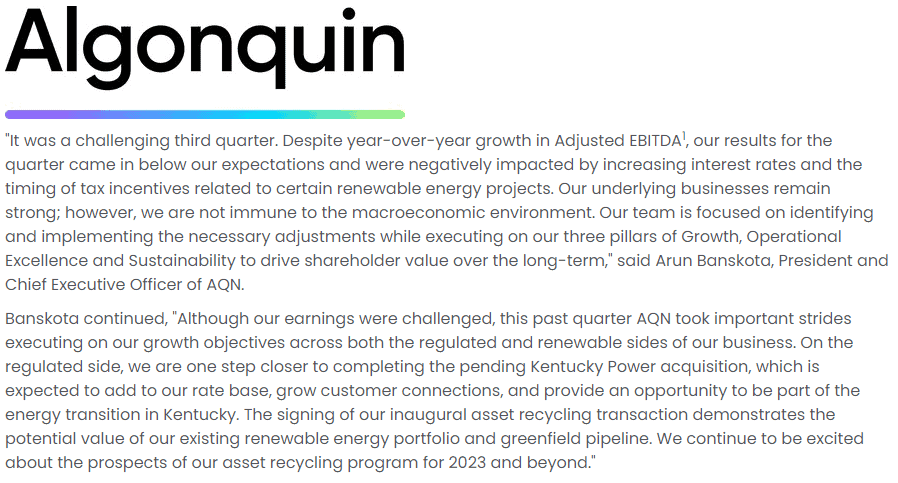

“It was a challenging third quarter. Despite year-over-year growth in Adjusted EBITDA, our results for the quarter came in below our expectations and were negatively impacted by increasing interest rates and the timing of tax incentives related to certain renewable energy projects. Our underlying businesses remain strong; however, we are not immune to the macroeconomic environment. Our team is focused on identifying and implementing the necessary adjustments while executing on our three pillars of Growth, Operational Excellence and Sustainability to drive shareholder value over the long-term,” said Arun Banskota, President and Chief Executive Officer of AQN.

“Looking ahead into 2023, broadly speaking, we expect pressure from increasing interest rates and broader macroeconomic conditions to impact our earnings. Although we are not providing 2023 guidance, our current view is that we will continue to drive growth in our regulated operating profit, albeit with some regulatory lag, while our renewables business is expected to be relatively flat as new program growth is tempered by lumpiness in our development pipeline. In light of the changing environment, we are reviewing our plans and targets for 2023 and beyond. We expect to provide further details at our upcoming Investor Day in early 2023.”

So from the press release and earnings call, AQN showed some positive things but also clearly stated that there are a lot of challenges ahead. More importantly, AQN painted a very bleak picture with the adjusted earnings per share.

- Earnings per share (EPS) of $0.11, down 27% vs. 2021

- Adjusted Net Earnings of $73.5 million, down 25% vs. Q3 2021.

- Revenue of $666M, up 26% vs. 2021

- Adjusted EBITDA of $276.1 million, up 10% vs. Q3 2021.

- Revised 2022 guidance for EPS – from $0.72-$0.77 to $0.66-$0.69

- Adjusted Net Earnings per common share of $0.11, a decrease of 27% vs. Q3 2021

While adjusted EBITDA, net earnings and revenue are up compared to 2021, the biggest kickers here are the severe decrease of adjusted net earnings per common share (down 27%) and the revised guidance for EPS (down 9.4% if we use the midpoint of the EPS guidance for calculation)

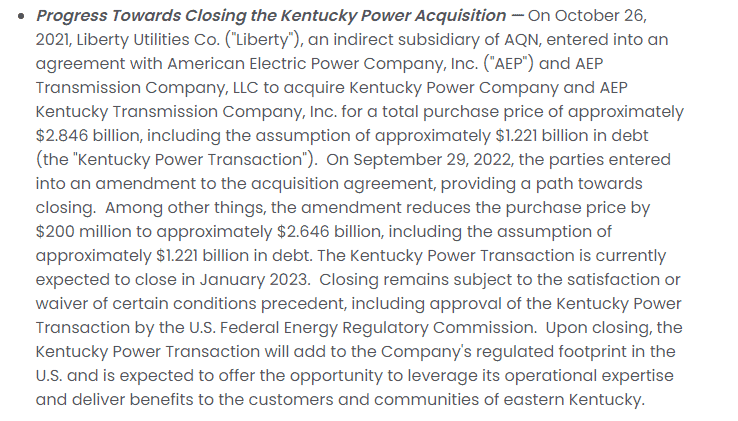

In addition, Algonquin Power & Utilities Corp is working to close the acquisition of Kentucky Power by January 2023.

While this acquisition cost came down from $2.846 billion to $2.646 billion, it will add approximately $1.221 billion in debt for Algonquin Power & Utilities Corp. For AQN shareholders, this basically means more debt, and more shares, which will further dilute the important valuation metric – EPS.

The rising interest rates – How that’s impacting AQN

Unless you’ve been living under a rock, you probably have heard that the Fed, the Bank of Canada, and central banks around the world have been raising interest rates as a way to combat the high inflation rates we’ve been experiencing.

Unfortunately, AQN has a lot of debt. The acquisition of Kentucky Power also brings a lot of uncertainties. Just how much the rising interest rates have impacted AQN?

According to AQN, while the company has approximately $2.1 billion of available liquidity, at the end of Q3, approximately 22% of the consolidated debt outstanding is subject to variable interest rates. According to Darren Myers, CFO of Algonquin Power & Utilities Corp, a 100 basis point increase (1%) in the variable interest rate would impact AQN’s interest expense by approximately $16 million annually.

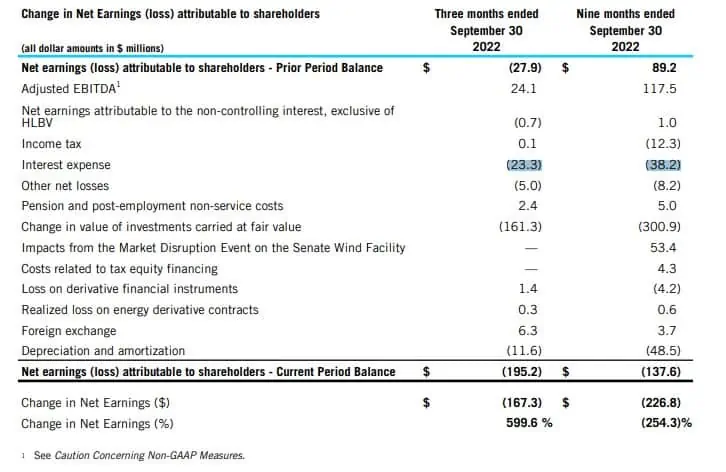

The effect of the rising interest rate is already seen in AQN’s balance sheet. According to the Q3 earnings report:

In the three months ending September 30, 2022, interest expense was $23.3 million. While in the nine months that ended September 30, 2022, interest expense was $38.2 million. So the interest expense almost doubled in Q3 alone ($14.9 million in Q1 and Q2 and $23.3 million in A3)! This, however, shouldn’t come as a surprise given the US interest rates look like below, clearly indicating a sharp increase in the last three months.

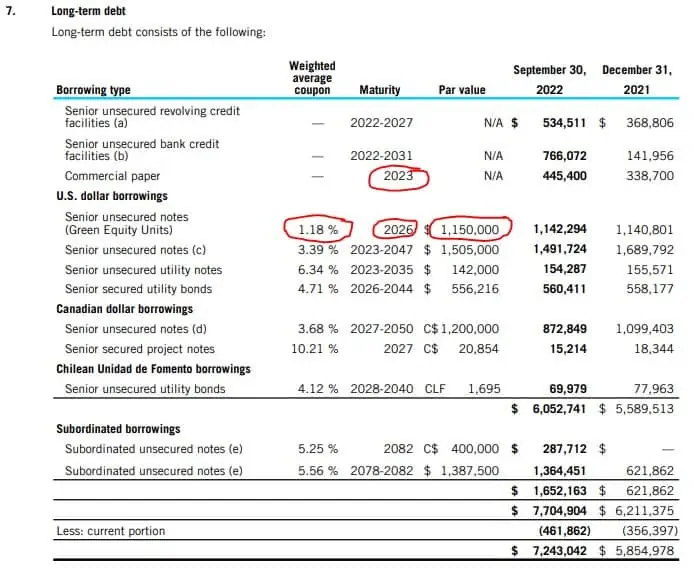

To make matters worse, AQN has several term facilities and approximately $100 million of long-term debt maturing throughout 2023. With the rising interest rates, it will mean higher interest expenses for AQN, unless they can find alternative sources of financing at lower rates (probably unlikely).

This brings up a good question, what happens to AQN’s long term debt? When is AQN’s long term debt going to mature? If the long term debt will mature in the near term and AQN needs to refinance at a higher rate than previously, this definitely will result in an even higher interest expenses.

As we can see, AQN has senior unsecured notes of $1.15 billion at a rate of 1.18%. Will the interest rate be below or near 1.18% by the time these notes mature and AQN needs to refinance them? This could be a potential problem for AQN in the next few years.

Selling of renewable assets

In the Q3 earnings press release, AQN also announced it has entered into an agreement to sell ownership interests in a portfolio of operating wind facilities in the US and Canada for $277.5 million USD and $107.3 million CAD (~$358 million USD total) to InfraRed Capital Partners which is part of Sun Life. This is AQN’s way to unlock profit from existing assets and use the proceeds to invest in additional growth.

Because InfraRed has no interest in operating these facilities, AQN will continue to oversee day-to-day operations and provide management services to the facilities. This arrangement should and will allow AQN to generate on-going revenues.

Whenever a company sells assets, it always raises concerns and worries about whether the company is selling assets to pay simply down debt. What is even worse, selling assets or taking on more debt so it can continue to pay out dividends (we’ve seen that in the past, like Encana).

In this case, it is not unusual to see companies making this type of move. I think the selling of these wind energy assets by AQN is actually a smart strategic maneuver. It should help the company to reduce its overall debt. Generating profit from existing assets and using the proceeds to invest in additional growth or pay down debt is a strategic move that many companies deploy.

Is AQN still a buy at the current price?

So we come to the million dollar question – is AQN still a buy at the current price?

Well, I think investors are freaking out because of the reduction in EPS guidance. On top of that the decrease in adjusted earnings per share, the high level of debt AQN is carrying, and the uncertainty over the Kentucky Power acquisition certainly cause a lot more worries and concerns for many investors and analysts.

I believe investors and analysts do have valid concerns. AQN’s financial picture certainly isn’t all that rosy.

But I truly believe the recent steep drop in the share price is a complete market overreaction. A drop of ~9.4% in EPS guidance shouldn’t result in a drop of around 32% in share price. This is a utility company that we’re talking about here and utility companies typically don’t see such steep share price drops. Now if it was a high tech company like Apple, Tesla, or Alphabet, or a highly volatile stock like Zoom, Peloton, or Coinbase, such a price drop would be more expected.

So, is AQN still a buy at the current price?

For us, we already own quite a bit of AQN, over 2,500 shares in fact. And as you could see from our October dividend report, we managed to drip 39 shares of AQN.

Despite owning quite a high number of AQN shares, the actual dollar amount of AQN is only about 2% of our overall portfolio value. In other words, a relatively small position compared to our top 15 holdings in our dividend portfolio.

Because we already own such a large number of AQN shares, we do not plan to add more at the current price. And because we are enrolled in DRIP, our plan is to dollar cost average AQN shares via DRIP. If AQN’s share price were to stay low at around $10 or even below, it’d allow us to drip more shares and dollar cost average quicker.

But what about other investors that may not have as many AQN shares or just starting to look at AQN?

Well, if you fall into this category, I think the current price may be an attractive entry price but do know the associated risks as I’ve outlined above. If we were to hold only a few hundred shares of AQN, I would seriously consider adding more shares to bring down my cost basis. Overall, I still believe that AQN is a strong company with a lot of future growth.

I would like to point out that I cannot predict the future, so I have no idea what the share price will do in the next little while. Who knows, AQN’s share price can continue to drop like a falling knife. It can also stop falling and hold flat for the next little while. Or it can surprise everyone else and go up quickly (very unlikely).

Having said that, if you’re in for the long term, I think eventually you will be rewarded.

Is AQN’s dividend safe?

Now for the biggest question on every dividend investor’s mind – is AQN’s dividend safe?

Unlike typical dividend stocks, for utility companies, you can’t just divide dividends by earnings per share to get the payout ratio. This is because utility companies like Algonquin Power & Utilities Corp, Fortis, Emera, and Enbridge for that matter, typically invest a lot of money in assets each year, so earning per share isn’t a good metric to use when calculating the payout ratio.

Don’t believe me? Let’s quickly calculate the payout ratio for these four companies mentioned:

- AQN – 105.6% (using mid point of EPS guidance and $0.713 per share for dividends)

- FTS – 83.7%

- EMA – 92.5%

- ENB – 126.9%

You certainly wouldn’t expect any of these companies to raise dividends every year given the high payout ratios. But they continue to do so.

To figure out the true payout ratio for AQN, we must look at adjusted funds from operations or AFFO.

In other words, if we are to calculate the payout ratio for 2022 and 2021, using the numbers provided in AQN’s Q3 earnings report, we get a payout ratio of 59.7% for 2022 and 57.4% for 2021. Here’s a nice summary table:

| 2022 | 2021 | |

| AFFO | $606.1 | $535.8 |

| Dividend | $361.9 | $307.6 |

| Payout ratio | 59.7% | 57.4% |

Around 60% payout ratio is relatively normal for dividend-paying stocks. For example, Rogers (RCI.B) has a payout ratio of 64.2%, Power Corp (POW.TO) has a payout ratio of 65.3%, and Transcontinental Inc (TCL.A) has a payout ratio of 65.1%.

So, based on the payout ratio calculated from AFFO divided by the dividend, I’d say that AQN’s dividend is safe. I wouldn’t expect AQN to cut its dividend, I also wouldn’t expect AQN to raise the dividend payout in the next little while. Even if AQN does decide to increase the dividend payout to keep its dividend streak next year, I would expect the raise to be very little.

But given the high dividend yield of over 9%, raising dividend payout by a very little amount is totally expected.

Interestingly, CFO Darren Myers stated this in the earnings call.

“We have previously stated a target of 80% to 90% payout and there is always going to be, and I think the company has done a nice job of talking about this in the past. So there can be dislocation from year to year on where that target comes in — where it comes in relative to that target.”

I’d assume that Myers wasn’t referring to the AFFO payout ratio but another payout ratio calculated by AQN internally. But from what Myers stated, it seemed that the current payout ratio is roughly in line with the company’s target. So even with the lowered EPS guidance, the dividend should be still within the 80-90% payout target.

Having said that, RBC analyst, Nelson Ng forecasted a 38% dividend cut in 2023 while a TD Bank analyst forecasted zero dividend increase for a few years (from a reader comment).

I searched the internet further and found some analysts’ reactions (from Globe and Mail).

Per Nelson Ng:

“Management has an opportunity at its upcoming Investor Day to reset its strategy,” said Mr. Ng. “We believe Algonquin will need to cut its dividend, reduce its capital program and growth targets, explore additional asset sales, and keep equity needs to a minimum. The shares of AQN could be range-bound until there is more visibility. We are downgrading our rating to Sector Perform (from Outperform) and reducing our price target to $12 (from $17) to reflect the many uncertainties, including a potential dividend cut.”

And per BMO Nesbitt Burns’ Ben Pham:

“After dropping almost 20 per cent on Friday following the reduction in 2022 EPS guidance (and signals around an upcoming reset of long-term 7-9-per-cent EPS CAGR), AQN shares are trading at depressed levels that offer attractive value (approximately 12.5 times P/E vs. 17x times utility peers),” said Mr. Pham. “This is despite its diversified mix of essential service utility and renewable power plants. However, there are likely increasing risks of a ‘strategic’ dividend cut and funding needs are still high. Given this balance, we are lowering our rating.”

What do I truly think? Well, despite what the AFFO payout ratio tells me, and what AQN’s CFO said in the earnings press call, I truly believe a small strategic dividend cut early in 2023 is the responsible and the right thing to do.

Yes, a dividend cut would hurt all AQN shareholders, us included, but it’s way better to make sure the company is in good financial shape with a strong balance sheet.

It simply doesn’t make sense to continue paying dividends when the balance sheet is completely out of whack. That’s like trying to build a skyscraper with a poor foundation… it’s not going to work in the long run.

Even if AQN were to cut dividends by 50%, at the current share price, it’d still be yielding at more than 4%. This is certainly attractive enough for many dividend investors.

Furthermore, I believe a dividend cut by AQN will help the stock price to recover over time.

In fact, I’d actually be more concerned if AQN management decides to keep its current dividend payout. Even worse if AQN management decides to raise the dividend payout slightly in 2023. This would demonstrate that the AQN management is completely out of their mind! If this does happen, I will probably look for ways to sell our shares and close out our position in AQN, unless something convinces me otherwise.

So where do we go from here?

As mentioned, we plan to continue to hold our AQN shares and dollar cost average via drip. I want to see AQN finish the Kentucky Power acquisition and integrate the company successfully. Since the acquisition is expected to close in January 2023, we should be able to get a better view by early 2023.

Given AQN has successfully finished many acquisitions in the past few years, I’d give AQN management the benefit of the doubt that the Kentucky Power acquisition will be a successful one.

I also want to see AQN showing ways on how it can reduce its debt and cut down its interest expenses. This will be key to improving AQN’s balance sheet. As the company has shown with the selling of wind facilities that resulted in millions of proceeds, I’d love to see AQN continue to explore such strategic sales of its existing assets (it’d be best if AQN can continue the day-to-day operations to bring in revenues). Hopefully over time, this will drive a stronger guidance, maybe not in 2023 but perhaps in 2024.

Most importantly, investors need to remember to ignore short term noises and look at the long term picture.

Overall, I think there are a lot of risks associated with AQN but it’s certainly not as risky as holding cryptocurrency in one of the sketchy crypto exchanges (sorry I couldn’t resist).

Algonquin stated that it will host an investor and analyst day in early 2023 so hopefully we will get a better view of the company by then as well. I suspect there’s going to be a big stock price movement on investor day as the market gets more clarity about the company’s direction.

The AQN situation reminds me a lot of what Inter Pipeline went through not too many years ago. I’m certainly having a bit of a deja vu moment. In case you don’t recall, Brookfield Infrastructure ended up acquiring Inter Pipeline at a discounted price. If AQN’s share price stays at $10 or below for an extended period of time, who knows, maybe someone may just decide to acquire AQN.

Last time I checked, Brookfield has a tendency to gobble up companies that are severely undervalued and are in a financial tailspin. If I have learned one thing through my DIY investing career is to never say “never”. Stranger things have happened in the past and they probably will continue to happen.

I hope you enjoyed this analysis on AQN. Let me know what you think by leaving a word or two in the comment section.

Note: I’m not a professional advisor. What I’ve written here is purely my opinion. Please always make buying and selling decisions on your own after proper research.

I noticed AQN’s price drop (didn’t own any at the time) and talked about it with my partner. He thought that it looked like a decent buy at around $10, and I did buy 200 shares at that price. Now, of course, it’s closer to $9. Oops. Well, I’m going to hold, and if/when the price starts going up, I’ll get some more.

I hope you’ll do an update on AQN in early 2023. I’d like to hear your thoughts.

We’ll see what happens with AQN, hopefully get some clarify when the company gives an update in early 2023.

Rhonda , AQN is a Solid company faced with a couple not so good quarters and the Kentucky Power deal that was not liked by the street from the word ‘go’ , and may not be approved ( just as well) from the USA regulators as well ( that may be a blessing in the short term ) . For me, I am buying it … too good of a deal at a book value 12.04, great pipeline of growing income and basically a infrastructure company with exposure to wind and solar as well .The green side of the portfolio is fickle with the Hydro electric, water sewer, and other sides are very solid . So, short sellers have entered the pictures too . In the interim I see short sellers trying to make a buck , uncertainty from the street due to a couple off quarters and The Kentucky deal in flux. Hence the lower price . This too shall pass in my estimation . Much too good of a company to remain sideways for too long . Another thing , there is a VERY LARGE possibility of a hostile take out. Many conglomerates and Infrastructure companies are looking . IF a deal were to be made for AQN it would be in the range of 15-17+ CAD in cash and stock from 3rd party company . Quite a premium to current values – they aren’t stupid either , buying controlling interest AQN at Book value plus 10 or 15 % for AQN is a very good deal – the company split up has a book value of far greater than Aprox 12.00 per share now . I hear the Executive are concerned about a buy out at this opportune time – as AQN is low . Now one has a Crystal Ball, just reasoned opinions based on past, market, sector and net value to other companies . Happy New Year for 2023 !

If the price stays low for an extended period of time I can see other companies try to buy AQN. It’d be similar to what we saw with IPL.

Yes , IPL is very similar in many ways . AQN is bruised right now … making it an even better take out target . Large Cap conglomerates know its value !

Stay away of renewables. Was a good advice in 2021, 2022 and for 2023 is going to be also

Strictly speaking, this company is not an absolute renewable. Hydro electricity for sure but the renewable aspect has different connotations to it. Also, a lot of revenue comes from what are utility, sewer, utility, and other like utilities . I hope you understand. Hence , AQN is very diverse in the “utility space” more than renewable per se .

The rising rate environment isn’t friendly to renewables it seems.

One item mentioned “albeit with some regulatory lag” is affecting quite a few electric utility companies that lean heavy into the regulated market. In my immediate area we have two providers already submitting a 50% increase in rates to our regulatory commission.

As the lag catches up it should normalize earnings again but as everyone else has stated les debt load would make this more attractive. As far as myself I am still holding AQN.

Yes reducing debt level would be one of the keys for AQN.

I like the Analysis and appreciate you sharing it all at no cost. My feedback on the analysis would be some details on projected revenue or net income of the acquition given the debt they will take on. Secondly some points on AQN ability to pass on higher interst rates to consumer given a large portion of the business is regulated would also help to see their ability to mitigate some risk. Will appreciate your thoughts.

Thanks for the feedback. The thing with projected revenue or net income is that they’re projected, hence we purposely stayed away from that. Good point on passing the higher interest rates to consumers. However, AQN needs to get their balance sheet in order first.

Thanks for this detailed analysis, I was really curious to get your feedback on AQN.

I will hold my position and wait to see what is coming in 2023. If they cut their div, we might see another drop…

I’m long term, so I’ll sit back and relax for now.

You’re welcome Guillaume.

Thank you Bob for this detailed analysis, I have about 1600 shares and I’m not going to add more but I’m holding and dripping at a discount price , like you said let’s hope they’ll cut the dividends and clean their balance sheet and get back on their feet and if not I’m sure a bigger fish will be happy to gobble them up!

You’re welcome Gus. Hold and drip seems to make sense.

I don’t own shares in Algonquin Power and Utilities but after reading the facts, being a highly leveraged Company amid a rapid rising interest rate environment makes this a risky bet right now.

I would pass on this opportunity and look at other more stable dividend paying stocks for the long term.

I would agree with those posters who commented that this one is a probable candidate for a dividend haircut. I’ve been here before and I would place a small wager on that happening in Q1 2023.

At a 6.35% dividend yield, I feel much better having a position in Freehold Royalties (FRU.TO). For those looking to move money, may want to consider this investment strategy.

Good luck to all.

Don’t know much about Freehold Royalties so can’t comment much about it.

It’s all part of inflationary environment we’re in.

AQN will just raise the rates after approval by governments. I don’t see massive profits but stability.

So I’m keeping my AQN as well .Not buying any as I have a lot of FTS my US account has SO and some European RWE for diversity

Keeping AQN sounds like a good plan right now. Let the dust settle.

Freehold is focused on providing investors with lower-risk returns and growth over the long term. Freehold pays dividends from a high-netback portfolio of mineral titles and royalties on oil and gas properties across North America.

Currently paying 6.92% or .09 monthly. I initiated a position in 2001 and have been adding yearly.

You’re talking FRU ? Yes , like it . I will hold on to the shares I have ….BUT , buying now it appears “I missed the party” . When oil goes down to sub 50.00 WTI , I’ll start looking at oil again . Just sold half my SHELL oil ( over 130% profit from where I picked it up 3.5 years ago ) and working on selling the rest and Exon ….CPG , BTE and SU are going to get sold too when WTI pops through 110.00 WTI . I use oil as a cyclical program . I dont fall in love with them . Oil as a commodity is tricky to invest in and high costs to extract . People need oil and Nat Gas – so I like that aspect . I like Mid streams – but they have not come off in some time .

Considered purchasing in the past, but the balance sheet, debt and continual dilution of shares scared me off. Also read some folks saying beware of this one. I bought FTS instead when it went over 4% yield. 49 years of divy increases is a pretty darn good record. Also have BEPC & CPX in this sector.

Yea, there are better stocks in the utility sector than AQN right now.

This is not a company but more like a giant CDO. It’s borrowed money that over paid for assets and now its valuation needs to be reset.

To roll over this house-of-debt they must maintain their “investment grade” debt rating which is already on a cliff edge. Faced with a down grade by the debt rating agencies they will have to cut the dividend. A 9% dividend is telling us that. When you say to yourself a cut would make sense – trust your instinct.

Likely also why previous management parachuted out of there not that long ago.

This dividend cut is likely not yet “priced in”. When those giant etf bond and dividend funds roll over their algorithms will auto-dump this stock and it could kiss the pavement. Think ATT or PPL.

It is true that Brookfield may come calling but that is speculating not investing.

There are likely better places to be now. This company has broken a sacred bond with its investor base and may take years to earn back trust and forgiveness and rebuild new investors. Look at the charts of the majority of companies – dividend cuts usually never end well.

Either way tax loss sellers are likely dumping this thing heavily right now.

I find it best to never put too much weight on what analysts say. Many are paid to essentially rope-a-dope and pump and dump. Some were heavily pushing widows and orphans to buy this dog and now they’re saying hold. Hold often means Sell in “analyst speak”. So here’s a so-called “safe utility” comes off near 50% and nobody saw that coming – there’s nothing safe about that.

Having said the above it’s a better price now than it was a few months ago. I don’t own it but If one is holding they could consider taking a tax loss and getting back in if they feel they see nothing better. If one doesn’t hold they could consider initiating a small position but adding carefully and mostly after it begins to form a bottom (which may be a while).

With stocks one makes money when buying not when selling. You over pay you never recover no matter how good the assets are. Valuation still matters despite the so-called “green revolution” or whatever the fad of the day happens to be. And debt ratings still matter too.

We’ll see what happens with AQN. 🙂

Thanks for your thoughts Richard. I decided to take the tax loss. I may get back in or I may choose add to other utilities I hold. I’ll wait the 30 days & decide

Smart move imho. You have the tax loss and can repurchase AQN before its ex dividend date.

Nice write-up Bob ! I hold AQN too , as does so many institutions . They will get their books in order and Kentucky Power will get brought into line . I would NEVER bet against AQN . Greta company with great assets and leadership team . Im impressed with the staff too and their technology and engineering . NEVER bet against AQN . We have a once in a decade opportunity here at 10.00 . I have gone from .5% position to 2.25% position over the last week ! Even IF the Div is dropped , I have a good low position at about 13.00 . remember they pay their DIV in USD and they have raised Div’s at regular intervals …..PLUS we get the Div TAX CREDIT , IF you have it in an exposed account ( cash account ) – I would buy in this range … NO hesitation mid to long term ! Happy investing guys ! Thanks Bob . James – currently at my house in the Philippines- lovely ! ….back on Vanc Island in May ! 🙂

Thank you James. Hopefully the management will give us more clarity in early Jan. 🙂

AQN is a capital intensive business. In a rising cost of capital situation like now (moreover for a company with that level of debt) and rising inflation, their amortization rate is most probably way too low to reflect the underlying reality, hence the payout ratio on earnings that is too high. AFFO is at least as tricky a metric, because the company chooses what to include and exclude. These days I tend to stay clear of capital intensive businesses because it is very difficult to know if their assessment of assets replacement cost is sound or not. And if this company is as good at forward guidance as it is for AFFO and amortization, there may be lying the answer as to why the stock fell 40-50% instead of the 10% change in forward guidance.

Good point on AFFO is a tricky metric. 🙂

I’m in the same camp as you. holding but won’t add until we hear about the dividend cut (let’s be honest it’s coming and is already priced in)

I guess the main question is how deep will the cut be with the Kentucky acquisition right there. It’s going to cost alot to fix that up.

ipl all over again, exactly! Just hope bam doesn’t buy them at these prices.

I think algonquin was the first company showing the effects of rising rates, soon enough we will see others as well.

There’s alot of high debt companys trading on the market for the same price as before rates started rising.

Time will tell. holding and dripping!

cheers Bob

Yea, I think the market already has the dividend cut priced in, so it’d be nice to get some clarity from the management, rather than the usual side step talks.

I think you’re right, we probably will see a lot more companies getting affected by the rising rates.

Nice, thorough and extensive summary Bob. Thank you. We are in a similar boat where our overall allocation of AQN is under 1.5% in our portfolio, so not panicking right now. Instead we are staying put for now and embracing the expected dividend cut. Such measures seem necessary to help their bottom line. Rather than DCA more AQN, there are other attractive renewables we’d rather expand upon, like CPX where management seems to have their ‘stuff’ in order.

Overall, like you said, utilities shouldn’t be this volatile and at the same time offers opportunity for a scenario of an M&A from another player in the space….let’s see!

Josh

You’re welcome Josh. Right, there are other attractive renewables available. 🙂

Thank you for your your most informative analysis on AQN- the best review I have seen to date. Do you provide analysis on other TSX stocks.

Thank you. I haven’t done a specific stock analysis in a while.

Hi Bob,

I enjoyed your article, but not enjoying owning this stock. Your article was thorough, yet clear and concise. It does seem like a dividend cut is in order as much as I hate to say that. I would like them to scale back on spending and growth and focus on their debt levels. The only thing I disagree with is if the dividend was cut by 50%, I don’t think it would be attractive to a lot of investors who already own the stock. Yes, if you bought it today or 2018 or before you would still have a decent yield on cost, but if you bought in the last 2 years prior to Q3 earnings like me you likely wouldn’t. My average is $17.81 and I was continuing add in the 14s and 15s, but I’m holding and not considering buying any more until there is much more clarity offered by the company. It just seems like gambling at this point and frankly frustrating to have to wait until next year’s investor day to find out more. The guidance or lack thereof is about the worst part for me. There are other buys out there in terms of individual stocks and ETFs.

Hi Lawrence,

Thank you. I agree with you, I’d like to see AQN get their books in order and focus on reducing their debt.

Right, if the dividend was cut by 50%, many investors may dump the stock, but I’d argue a lot of investors have dumped the stock already, hence the price drop.

At this point, some clarity from the company would be nice.