The accumulation phase is a major focus within the financial independence retire early (FIRE) movement. People focus on how they can accumulate enough assets to reach financial independence and eventually retire early. But the accumulation phase has a few basic principles – live within your means, widen your spending-saving gap, avoid lifestyle inflation, and invest your money in appreciating assets like index ETFs or dividend growth stocks.

The decumulation phase, unfortunately, doesn’t get as much attention. People quickly glance over topics like the 4% safe withdrawal rule and which tax advantage account(s) to withdraw first. The usual approach is that people think they will figure out the decumulation phase later.

I have been spending more and more time writing about the decumulation phase lately. Since we are planning to live off dividends from our dividend portfolio in 2025 or earlier, I want to start planning the decumulation phase a bit. Or at a minimum, have some plans with our early withdrawal strategies.

Technically we can be financially independent but decided to prolong our FI journey. We are very fortunate and blessed to have such an option. I feel it is important for me to share our knowledge and help other people to improve their finances through this blog. In addition, helping and improving our communities through charity work is just as vital.

- Our Early Withdrawal Strategies – How to keep more money

- Early Withdrawal Strategies – A reader’s discussion

- Revisit our financial independence assumptions

A lot of our early withdrawal strategies are developed based on what I have read online and running simulations in Excel spreadsheets. But doing simulations and considering things like a sustainable portfolio, government benefits (i.e., CPP and OAS), defined benefit pension, tax efficiency, estate planning, etc. can get very tricky.

There are many retirement calculators available online (heck I have a spreadsheet one). One would input the balance of their TFSA, RRSP, taxable accounts, other assets, a “desired” retirement income, and a retirement age. The retirement calculator then gives you a generic statement of whether you’ll be ready to retire or not.

But these online retirement calculators are all very vanilla and way too simplistic, mine included. There’s nothing on how to draw down your portfolio in a tax-efficient way, the best account order you should withdraw money from (i.e., taxable, RRSP, or TFSA first). Furthermore, if you are like us and plan to live off dividends and create a future legacy by passing down the investment portfolio, the online retirement calculators can’t plan for that.

Fortunately, smart folks at Cashflows & Portfolios started an awesome, low-cost Retirement Projections service for Canadians.

Cashflows & Portfolios – Retirement Projections

Most readers are probably not familiar with Cashflows & Portfolios because it’s a relatively new site. But the founding members are two very well-known bloggers from the Canadian personal finance blogosphere, Mark from My Own Advisor, and Joe (aka FrugalTrader) who founded Million Dollar Journey.

I have been reading Mark and Joe’s writings for over ten years now (probably longer). They are a big reason why I started this blog and an inspiration to me. Both Mark and Joe are in their 40’s, manage their own investment portfolios, and deploy the same hybrid investing strategy of index ETFs and dividend growth stocks as we do.

Mark and Joe started Cashflows & Portfolios and their Retirement Projections service because they feel they can help Canadians in a major way. They are currently using professional financial projections software for their own retirement projections – and with their extensive DIY investing expertise, success as DIY investors, they are offering their time and knowledge to help others.

According to Mark and Joe, there is a huge gap between fee-only planners who can advise people and those people who simply want extra personal confidence in their retirement drawdown approaches. In Canada, most fee-only advisors or planners charge $1,500 to $8,000 for any complete financial plan. On top of that, many advisors want your money to manage: some would charge another 1% or more annually to manage your investment portfolio. Those costs can add up.

With Cashflows & Portfolios’ Retirement Projections service, Mark and Joe will not be offering any advice but they can offer a very comprehensive personal report by taking your inputs, your assumptions, running your tailored projections, and delivering a report customized to your needs and goals.

I was very intrigued when Mark and Joe reached out to me about this service. Although I have done my fair share of spreadsheet simulations I was very intrigued about their service not to mention I wanted a fresh set of eyes to take a look at our numbers. So I was quick to agree to be a client and try out their Retirement Projections service.

What I really liked about Cashflows & Portfolios’ Retirement Projections service is that Mark and Joe asked me a lot of questions and took in a lot of numbers – based on what I needed. They were very open to my concerns, any questions, and specific requests of running multiple scenarios based on different incomes, retirement ages, and whether to leave an estate or not. We went back and forth many times for assumptions and clarifications. This made me feel like it was going to be a comprehensive tailored report – and it was.

Mark and Joe provided me with their service and a couple of reports free of charge as a way for me to try it out and write this article, but I would not hesitate to sign up for their Platinum Membership given the overall value delivered – which includes time with them whereby you can ask them anything!

Cashflows & Portfolios – Membership Options

There are three different Casfhlows & Portfolios membership options – Bronze, Gold, and Platinum. To get your detailed and personalized report and retirement projections, you need to sign up for either the Gold or Platinum membership. The Platinum membership costs only a fraction more than Gold, but the value it provides is both a retirement stress-test (with any historical returns) AND a 1-hour phone/online call with Mark and Joe to ask any questions about your report or beyond.

Through our discussions, I received some pricing details from Mark and Joe. I was pleasantly surprised to learn the Gold and Platinum memberships were MUCH cheaper than any $1,500 entry price listed above (i.e., it was in the very affordable 3-figure range). The duo at Cashflows & Portfolios want their members to be 100% happy so they try to be very responsive – answering any questions thoroughly and promptly.

Cashflows & Portfolios Retirement Projections Review

Please note, Mark and Joe offered me their retirement projections service for free so I could try it and write an honest and personal review.

My quick take is the Cashflows & Portfolios Retirement Projections service is an awesome value that Canadians should definitely consider.

Here’s my detailed review.

Cashflows & Portfolios offer their projections services for individuals but they generally recommend that you do a projection with a spouse or partner (if you have one), if you want a more comprehensive family report. This allows them to provide better accuracy for any reports returned including tax optimization between couples or partners. Since Mrs. T and I have joint accounts and we treat our finances as one big account, we ran the projections together.

Originally I thought everything would be done via emails but I was pleasantly surprised the confidential financial information is shared via an encrypted online form. I also signed a liability waiver which basically states that any information shared with me is for my personal educational purposes only, it is not professional advice or recommendations. Everything is essentially my decision. It’s pretty standard stuff and similar to the disclaimer I have for my own coaching service.

The online form asks for personal information like:

- Date of birth (although you don’t have to use this – you can be approximate)

- Employment income (again, you can approximate as you wish)

- Business income

- Other income

- Savings account balance

- Taxable account balance and asset allocation

- RRSP/RRIF balance and asset allocation

- LIRA/LIF balance and asset allocation

- TFSA balance and asset allocation

- Annual TFSA and RRSP/RRIF contribution

- TFSA and RRSP contribution room remaining

- Real asset (i.e. houses)

- Liabilities

- Life insurance details

- Your intended retirement age

- When you intend to take CPP and OAS

- Defined benefit pension

- Other retirement income

What I liked is Mrs. T. and I could use approximate values – for anything we wanted to. This was our report and Mark and Joe reminded me that anything I didn’t want to share, I didn’t have to. There was an input form I needed to complete and I was provided multiple opportunities to add as many comments or questions as I wanted to.

After filling out the form, Cashflows & Portfolios took my data provided, calculated my projections, and delivered a personal, comprehensive report based on the scenario of my choice within 7-10 business days like they said they would. In fact, I got a few reports based on a long list of questions and various options!

I asked for retirement projections based on these three scenarios:

- Can we be financially independent by 2025 with $60k per year after-tax income from our investment portfolio?

- How much we can spend in 2025 if we utilize both dividend income and portfolio withdrawal and deplete our investment accounts to almost $0 while leaving our house to the estate?

- What happens if we continue contributing TFSAs and RRSPs until age 55 and retire then. What would our retirement look like?

All of these scenarios assume that Mrs. and I will continue working part-time and earn $25k a year (we don’t plan to just retire and sit on the beach and drink pina colada all day).

I was very interested to see whether we are on track to start living off dividends by 2025. I was also very curious to see what our retirement income would look like if we were to make withdrawals from the portfolio and if account withdrawal orders would make any difference.

The rates used in the projections were 2% inflation, 6.5% investment return (for 100% equity that is), 1.5% cash interest, and 2% house appreciation. Mark and Joe reviewed these values with me and then performed the calculations. Those projections were tightly aligned to the 2021 returns recommended by FP Canada Standards Council. Alternatively, they can change any values you wish – another reminder to me this was my personal, customized report that includes any rates of return, inflation or other values I feel strongly about.

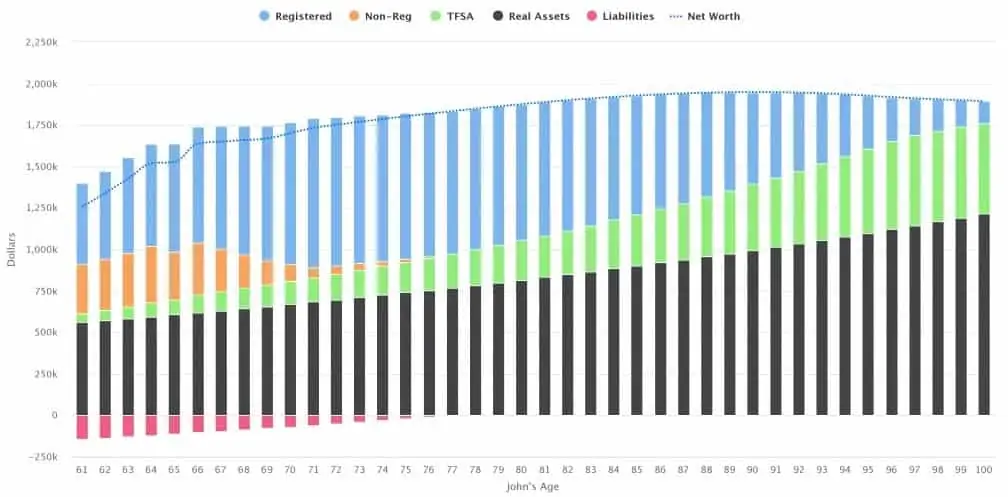

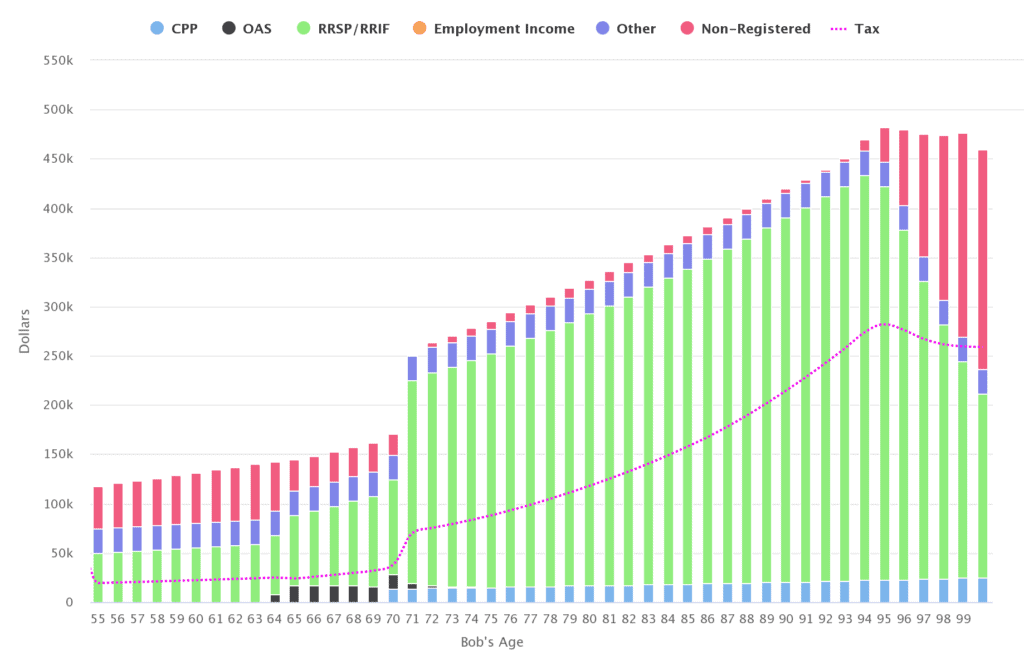

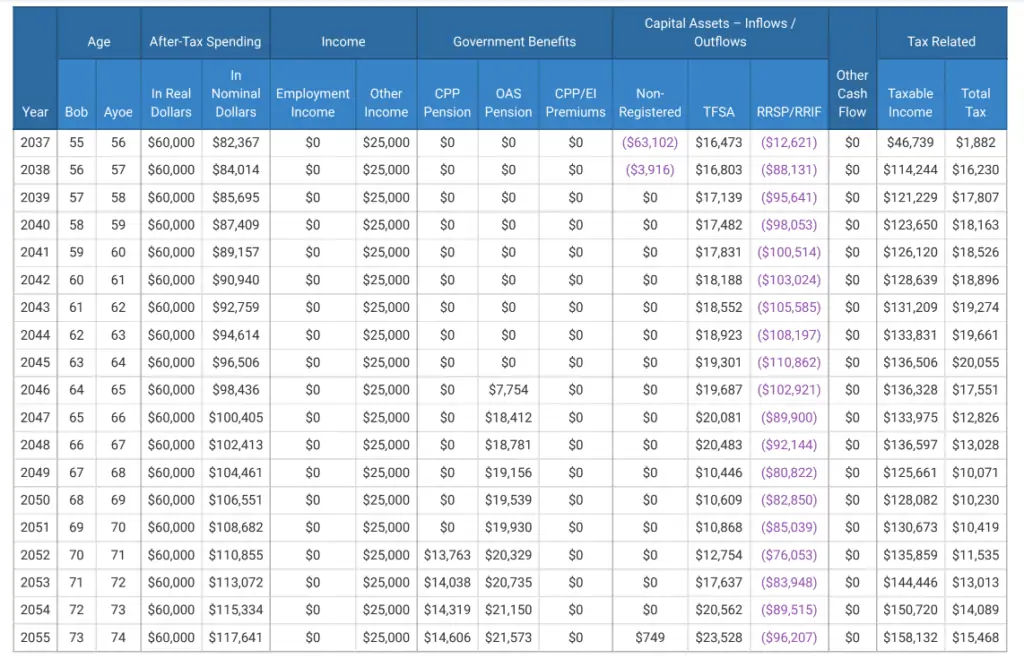

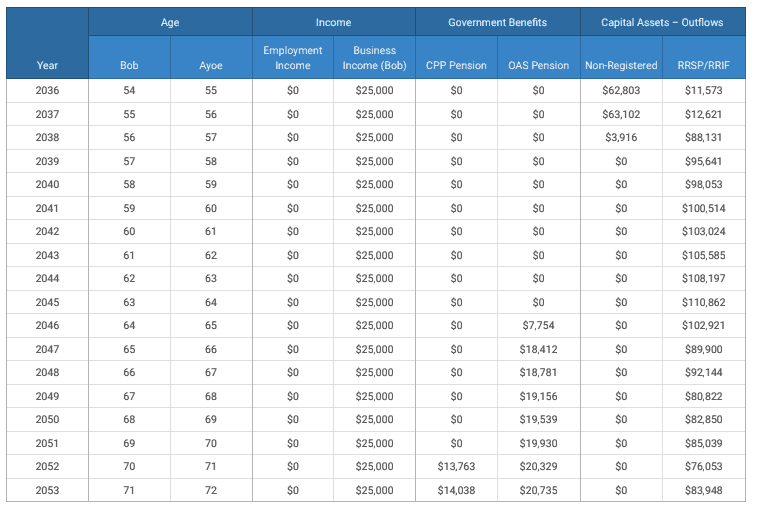

The reports that I received had net worth and income in nominal dollars up to age 100. I really like that the reports showed different sources of income, both taxable and non-taxable, and estimated taxes year-over-year.

So, what are the projections for the three scenarios I listed above?

For Scenario 1, I was pleased to find out in my report that we can “retire” in 2025 with $60k after-tax annual spending, take out CPP at age 70 and OAS at age 65, and result in a final estate value of $29.5M after-tax at age 100. In today’s dollars, that’s roughly $8.6M. This is absolutely fabulous! It also gives me assurance that I just might be able to write a cheque for $1M and donate to a charity one day.

Please note, for this scenario, we are not only living off dividends. We will withdraw a small amount of money from our portfolio each year. The most optimized withdrawal order for us in this scenario was non-registered first, RRSP second, then finally TFSA.

Now, those are big numbers so I should share a few things since I asked for this scenario. One, I assumed we never sold our house. So, living in Vancouver, that house value is going to appreciate quite a bit over the next 60 years based on my assumptions. Two, we never spent a penny from either of our TFSAs even to age 100. I’m not sure how realistic that is. There’s a very good chance that we’d be touching both TFSAs before then.

Having said that, Mrs. T and I feel extremely blessed that we are doing well financially and that we are tracking toward our financial independence plan. Given many people are facing financial difficulties, especially during this difficult global pandemic, we feel that we need to provide a helping hand whenever possible by donating money and time to local charities. You may want to consider donating securities to charities to maximize tax benefits.

For Scenario 2, it was interesting to see that we can spend more – over $86k a year and still retire in 2025. Mark and Joe also stress-tested our portfolio using the worst historical 20-year returns (and repeating in the coming decades). If that scenario were to happen, then our max spending actually drops quite a bit from $86k per year to $63.7k/year after-tax. That stress-test was important to factor in given market history can repeat sometimes. The most optimized withdrawal order for Scenario 2 was non-registered first, TFSA second, then finally RRSP.

For Scenario 3 (if we continue contributing to our TFSAs and RRSPs until age 55), we will encounter “too much RRSP” and face OAS clawback.

Sidenote: Mark and Joe recently wrote about Can you have too much in your RRSP?

This scenario showed that to avoid a full OAS clawback, we should consider some early RRSP withdrawals (versus starting any forced RRSP/RRIF withdrawals when we turn age 71). If we were to spend $60k a year and retire at age 55, this would leave an estate valued over $15M (today’s dollars) at age 100. Now if we were to spend down our capital by age 100, our annual spending would jump to $179k/year after-tax. Again, in this scenario, for that large estate value, I should highlight we never sold our Vancouver home and we did not spend any TFSA assets for the coming 60 years.

My Scenario Summary

For all my scenarios (and I asked a lot of questions to try out the service and see what might be possible), it was comforting to see that we will be doing very well financially whatever we decide to do. We feel extremely fortunate and blessed. More than ever, I think Mrs. T and I need to provide more financial help to people in need and put more focus on philanthropy and making this world a better place.

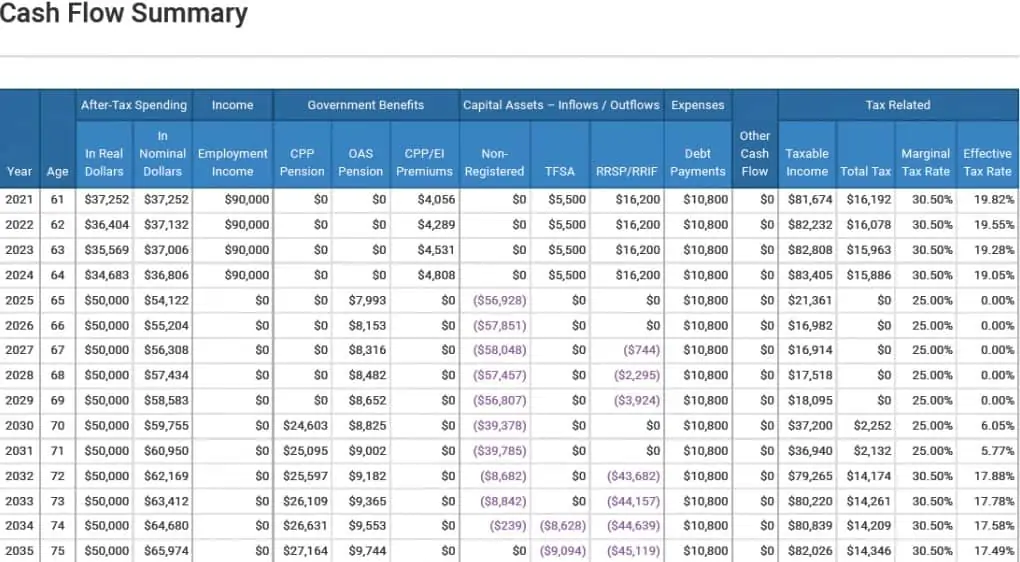

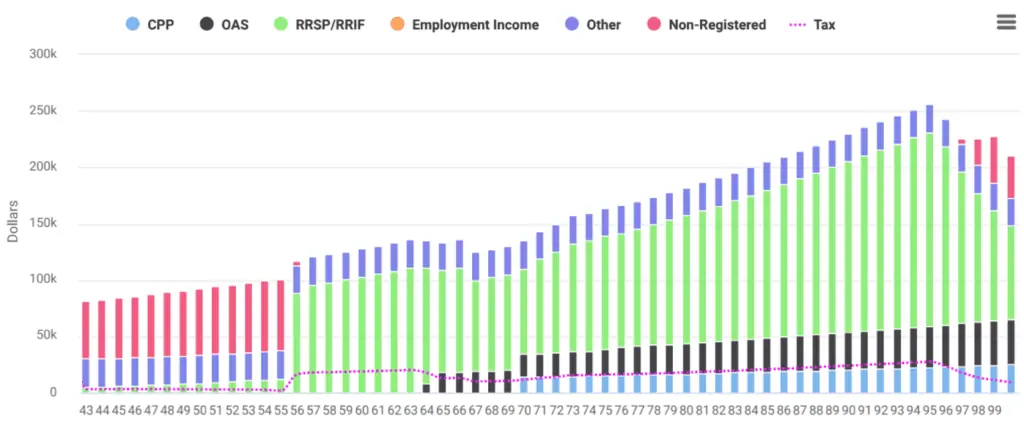

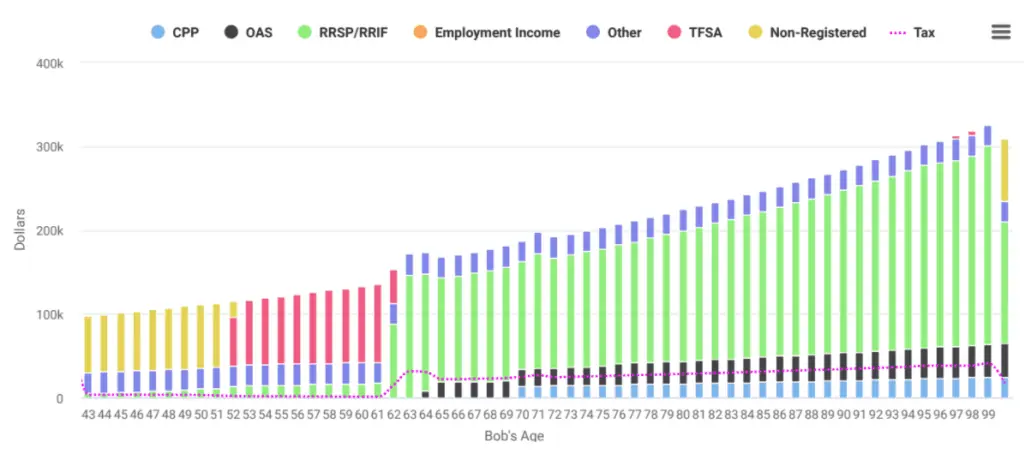

Back to the reports. The projection reports include both charts and yearly data. The charts are great if you’re a visual person and want a visual summary. My favourite sections in the reports are Cash Flow Summary and Income Details.

The Cash Flow Summary lets you see some actual numbers by person. It tells you your after-tax spending, where the money is coming from (i.e., non-registered, TFSA, RRSP, CPP, OAS, other pensions, etc.), capital assets inflows and outflows, as well as marginal tax rate and effective tax rate.

The Income Details show where your income is coming from, whether it’s employment income, business income, government benefits, or capital assets. While we have never counted on OAS and CPP in our FIRE plans, it’s nice to see how much we can potentially receive in OAS and CPP when we are older than 65.

Even after the projection reports, I was able to ask Mark and Joe several questions and run the projections again by tweaking some numbers and assumptions. The iterative process with them was extremely helpful and valuable.

Cashflows and Portfolios Retirement Projections – My Thoughts

So what are my thoughts on the Cashflows & Portfolios Retirement Projections service?

Since there isn’t as much focus on the decumulation phase, even for the FIRE community, I am so happy that Mark and Joe are offering these great services to Canadians at very reasonable rates for folks at any retirement income level. Like I mentioned at the beginning of this post, I believe many people gravitate to safe withdrawal rates and other generalizations when it comes to retirement planning, and because of that, they don’t take the necessary time to look at all the combinations of what is possible for any retirement drawdown plan.

For me, it was very assuring and comforting to see these projections in real numbers and in detailed reports showing the tax rates. I know we are very fortunate and blessed to be doing so well financially. As we continue my FI journey, I think it is more and more important for Mrs. T and me to focus on philanthropy. I also want to help people in improving their finances and making their lives better via this blog.

I believe the service being offered is targeted mostly at those people that are close to retirement, planning for their retirement, or already retired but want to optimize any portfolio withdrawals. I also think this service is beneficial to anyone on their FIRE journey to get a more comprehensive picture of how things fit together including any future government benefits.

There’s really nothing to lose given Mark and Joe are offering a 100% no-risk money-back guarantee. There’s no time limit with this guarantee either. They are simply offering their time and knowledge to Canadians based on the work they are already doing with their own retirement and semi-retirement planning.

Cashflows & Portfolios Retirement Projections – Discount and Summary

If you ever want to see your personal drawdown strategy, or what your net worth, estate value or taxation might be in any retirement scenario – subscribe to the Cashflows & Portfolios free newsletter and contact Mark and Joe about their services. They post regular content on the site and if you become a member they even have a forum to interact with other clients.

They also highlight some retirement case studies now and then to share what is possible for any income earner at any age. All free content.

Here are some posts I’ve really enjoyed:

- Can this 60-something retire on a lower income?

- How much does this couple need to save to retire by age 50?

- When should you consider taking CPP in retirement? Read on here.

Mark and Joe are kind enough to offer all Tawcan.com readers a 15% discount on their Cashflow & Portfolios Retirement Projections services until Dec 31, 2021. To get the discount, all you have to do is to mention Tawcan, or Tawcan.com in the “How Did You Hear About Us” part of the form.

After this date, their services will be back to the regular pricing. Even without the 15% discount, I’d be happy to pay them because it’s money so well spent.

In summary, I think this is an awesome service for Canadian DIY investors. You’ll get unbiased, unfiltered reports based on your own assumptions, your own inputs, and your own personal plans about retirement. You’ll also get to pick the brains with two of the most established DIY investors and bloggers in Canada – with over 25 years of combined experience.

That was certainly the case for us.

Dear readers, did you find this review of Cashflows & Portfolios Retirement Projections useful? Regardless if you use their services, what are your decumulation plans? What are your early withdrawal strategies? Do they align with any of my dreams or thoughts for estate planning and passing any assets to the next generation?

Cashflows and Portfolios (CAP) uses a platform called Adviice. They charge $27/month for a DIY service where you input and manage the data and scenarios yourself. This is 3X the price that Adviice charges for the same thing, plus CAP charges a whopping $447 to enroll in the first place. Save your money and get a 30-day trial period for $9 directly from Adviice, the platform provider, with an ongoing fee of only $9 per month. There is a user forum on Reddit where the vendor personally answers your questions. They also give free webinars.

I’d argue that it’s not as simple as just running the program yourself. Mark and Joe also bring years of personal finance and FIRE knowledge to help CAP clients. Let’s be fair here.

HI Bob. Thanks for a great article. I would also highly recommend a fee-based advisor for retirement and decumulation planning. In addition to an income spreadsheet you probably also received one for Net worth.

Considering you have 2 kids and will probably be interested in estate planning as well, I would also recommend looking at a scenario where one or both of you pass away earlier than 100. For example, if both you and your spouse die at age 75, how does that affect estate planning? Based on my experience, if you follow scenario 2 and leave RRSP drawdown to the end, you will potentially have a huge tax burden on your estate and potentially lose out on hundreds of thousands of dollars.

Thanks, I realized leaving RRSP drawdown to the end it will create tax burden on our estate. Estate planning is very important.

I was initially going to comment to say that NewRetirement has a very good retirement calculator that factors in cash flow in retirement. However, I started to read gerhard’s comments and I’m going to have to put aside some time to read and process them – LOL.

I don’t want to take anything away from Cashflows and Portfolios especially because FrugalTrader and I go way back. It looks very interesting.

Great stuff. FrugalTrader is also an inspiration to me Lazy Man!

All the best,

CAP

Hey Bob

Wonder if Reader B and his wife would have used such a service considering they started their investment journey decades ago.

In those days, we used to leave our mother’s houses at 8 years old in the summer, go fish the Capilano River all day and were told to be home for supper, asking someone on the river what time it was, so as not to be late.

Used to be dropped off at the Grouse Mountain Gondola on a Saturday morning, with a packed lunch and 50 cents for a hot chocolate and told to be down at 6pm, to be picked up.

When I started working, used to ask the guy with the Province paper on the construction site if I could borrow it to read the finance section (the Sun was an evening newspaper). Only limited stock information, but it was a start.

Nowadays seems everyone needs their hands held because they do not want to put in the time and effort and would rather PAY someone. Amazing how people cannot figure out, when is enough, actually enough and think that some computer generated projection will give them that answer.

What happens when, that computer generated projection does not live up to your expectations, do you get a refund or do you pay for another service to tell you when you should be satisfied.

The biggest problem to is that people’s expectations are sometimes so out of line with reality that they can never be satisfied.

Don’t get me wrong, these are your dollars (well actually Bob received this service FREE), that you are spending and if it makes you happy by all means.

We all started our personal investment journeys for various reasons, DIY, not happy with Financial Advisor, do not want other people to know, etc.etc.etc.

We all follow blogs, WHY?

To get advice. To see if we are do things as other people. To negate the fear that we are screwing it all up.

Look Bob this is not a poke at you, I generally agree with what you do.

What would all your followers, fellow investment buddies, do if you were to suddenly

a) disappear, like those Crypto bankers,

b) drop dead, or

c) pull a Forest Gump and stop running remember when he says he’s tired and going home. The guy behind him says, What are we supposed to do now?

People, stand on your own two feet. The investment journey is not about copying someone else or subscribing to another service.

Every dollar spent on someone else’s service is another dollar you need to earn before that magic FIRE number. . Everyone has a different number for FIRE, some $1 million, some $2 million or ex dollars per year for ex amount of years.

Paying someone so they can reach FIRE on your hardearned cash is just wrong.

Fair enough….Thankyou

You’re welcome. Hope my answer was satisfactory.

I must be missing something here. Everyone reading your Blog are money people……Right? Why are you and that website you refer us to not upfront about the price?….As much as the service looks enticing, it is equally suspicious.Why not just say the cost of the service ?????

Hi Chris,

That’s a fair comment. Yes, most of the readers are numbers people, I get that and I’m not trying to be deceiving or making it sound suspicious, that was not my intention. My intention was to demonstrate and show the value of the retirement projection. I didn’t want to focus on the price because that tends to be the number one thing that people focus. What I can say that the service is much lower than $1,500 as what I have indicated in the post. I also wanted to be fair to Mark and Joe and not disclose the exact pricing in case they decide to change the pricing later on (IMO for what they provide, they can easily charge more).

I hope this helps.

Hi Chris,

Great to get these comments, we want folks to be engaged!

See above answer to Court.

We will certainly consider advertising our pricing more over time, however, we encourage folks to visit our page (see below) and understand the process a bit before we “throw” folks just a price.

These are personal projections tailored to your needs, goals, assumptions and more. So, it’s a bit of work on a client’s end as well – not just us – so it’s a process together. So, the more people understand how we approach things overall, we believe that’s better than just a sticker price.

Feel free to check out our page and ask a bunch of questions. We’re here to answer anything.

https://www.cashflowsandportfolios.com/retirement-projections/

CAP

Hi,

What country/region is that on your photo on the main page? (The landscape with the water an the path down to the water.)

I hope it’s not a virtual picture :)…

I believe it’s from England…White Cliffs of Dover.

Thanks!!

Will put a visit on my bucket list. 🙂

Great review Bob.

But what is the actual price for their services??

We had some very analytical FIRE friends create a similar customized product for us and I agree it’s super helpful to see it all broken down with your own actual figures.

Hi Court,

Thanks. Best to check with Mark & Joe on pricing. They want to get to know the clients and highlight their services before providing the pricing.

Thanks Court and a fair question!

We will certainly consider advertising our pricing more over time. Right now, we ask folks to visit our page (see below) and understand the process a bit before we “throw” folks just a price. We believe it’s important that people understand our limitations (can’t offer any advice) but also understand how we approach things overall, these are personal projections tailored to your needs, assumptions, goals – to know what goes into the price and time. That includes any client thinking as well!

Just marketing a price (lower than many fee-only planners by the way) without any understanding of quality, deliverables, value-delivered or other, is not a good model in our opinion.

Happy to discuss further of course!

CAP

https://www.cashflowsandportfolios.com/retirement-projections/

Was the simulation able to easily represent/capture “living off dividends” and the tax consequences? It doesn’t seem like the calculation was considering dividends at all.

Hi Rialb,

Yes, the simulation was able to capture living off dividends and the tax consequences. Both Mark and Joe are planning to live off dividends as well.

Great question Rialb and we can help project various desired spending. If you only want to spend a certain amount from certain accounts, we can include that into the projections for you to see where you end up.

Bob is correct that for myself (Mark), I do intend to “live off dividends” to a certain degree.

I outlined my recent update and path to FI here.

https://www.myownadvisor.ca/financial-independence-update/

Thanks for your question.

CAP

Amazing review, Bob. Thanks for sharing. Now that you’ve had this projection service, are you considering any changes to your FIRE plan?

Hi AL,

No change in our plan for now but it’s nice to know that we have a few options available. Who knows, maybe we can hit the 2025 goal even earlier. 🙂

You absolutely have options and financial flexibility Bob. That’s all you can really hope for as you enter any form or early retirement / semi-retirement / retirement on your own terms.

We wish you the best in your journey and will continue to follow along!

CAP

Hi Bob,

Excellent synopsis of CAP’s services. I am also a client. The reports Mark and Joe provide are very detailed but easy to follow. And at a great price. I would recommend them highly.

Chuck

I was very impressed by the reports provided by Mark and Joe. It’s a very valuable service. Glad to hear you recommend them as well.

Great to see your comment here Chuck – thanks very much! It was a pleasure to work with you and we hope to do so again.

CAP

Thank you for this review. It is very helpful and I will certainly think about this service a little more seriously. I had been thinking about having my retirement plans and cashflows reviewed and this gives me more confidence in their service.

Keep up the good work.

You’re welcome Jan. I feel that the projections were very helpful for us. 🙂

Thanks very much Jan. We hope to help many clients with our service as DIY investors ourselves, looking for an alternative!

Hi Bob

If that all comes to fruition the CRA will love you for your donation to the tax coffers.

As I have stated before, if missing out on your OAS is all you care about wonderful.

I approached FIRE from a different angle, namely, how to keep the CRA from actually getting any of my hard earned savings.

A legacy is a wonderful thing, but my kids will enjoy that long before we are dead and gone.

I for one do not believe in charities. Used to work for Covanta(look it up if you don’t know who they are) and one fellow worker once told me about his friend, who also worked there. Told me that his friend doesn’t need the money, asked why?, told me his wife is high up at United Way and makes 4 times what he does. At that time, we were making 6 figures and that was 15 years ago.

Our will also does not mention charities, they are a leech on society which only benefit those who run them.

As far as paying for someone to tell me how to drawdown my nest egg, my wife does that for us. She needs funds, I give them to her.

You have fun now, you hear.

Will be back in Vancouver in January to settle some issues we have there, other than that, snowing in the ALPS, not like the ATMOSPHERIC RIVER you guys have.

What the heck is an ATMOSPHERIC RIVER, when I was growing up on the North Shore, we called it The PINEAPPLE EXPRESS. ATMOSPHERIC RIVER my left Buttcheek

Hi Gerhard,

Personal finance is personal. We all have our own preferences. 🙂

Hi Bob

See Bob, on that note I agree with you ,Personal Finance is personal, but you have written a blog and have opened your personal finance “thoughts” to the general viewing audience.

I can say, that 100% of investors invest in the hopes of making money, and by doing so are ALWAYS in an ACCUMULATION PHASE. That is what actually drives them, just like looking at your bank account after getting your paycheck and see more in there than last month, that is ACCUMULATION thinking. Most of these investors find it hard to switch to decumulation simply because it goes against everything they would have done for 30 to 40 odd years.

Now add to this FIRE, which in a nutshell means Financial Independence Retire Early and your CPP and OAS(Canadian Pension Plan and Old Age Security) are thrown out the window. Simply because you can not collect OAS till 65 and CPP minimum age 60 and if you achieved FIRE they do not calculate into your equation.

CPP or OAS are 2 things that any FIRE candidate should not even be thinking about, because quite honestly, I am way too young to collect.

The only thing I can tell you, is that by age 75, our portfolio will be wittled down far enough that the Canadian government will be paying for our Pharmacare if need be and also if need be they can stick us in a government sponsored care facility.

Gifting in Canada has no limit, and boy will we be gifting.

Paying taxes is not a BAD thing, it comes down to how much. Remember, you need to make money to pay taxes, FEEL LUCKY TO BE IN THAT SITUATION.

Hey Gerhard,

The way we see it on CAP (Cashflows & Portfolios) – paying taxes is a good problem to have. Sure, you can complain, but usually high taxes mean you have one of two things: 1) a high income problem and/or 2) a high income problem and minimal ways to reduce taxation.

Many clients on our site (CAP) are finding it VERY hard to move into asset decumulation vs. asset accumulation. They’ve been wired to save for 30-40 years and now they don’t have to.

I think if any FIRE/FI 40 or 50-something can ignore, a bit, what CPP or OAS might pay them in retirement then they are usually “good” and have saved enough. If you are worried about whether you have enough to retire including all CPP and OAS, you probably need to do more saving.

Just me! (Mark from CAP)

Happy investing!

I like to give directly to the Canadian Cancer society for Prostate research – Its a great cause in many ways ! I give also directly to poor communities in the Philipines where I grew up as a foreigner kid as well ( hospital donations, school donations , food donations and such ) These are “direct methods ” . As for United way – So true ! you cant believe a word from them , on their administration costs and other . They play some very tricky accounting to say they have a 5-7% Admin cost , when its VERY much higher and more like 30+% , when you look at how they ‘wash trade” their accounts with other charities ( a shell game to lower their admin costs superficially) . I wont give to them – NOT a chance ! There are many good charities , BUT you have to take a look at what they do and WHO they support and what their staff earn . A junior manager earning more than 250K a year plus pensions++, and other for a charity – IS NOT A CHARITY ! Its a business , that happens to give some money to their special cases/causes ( and sometimes this is scandalous ) . Give , but be wise about it and look into salaries .

Definitely a good idea to find out how much your donation actually goes to those in need.