This article is inspired by Mark’s recent post on his blog where he revisited their financial independence assumptions. I have shared some numbers on this little blog of mine in the past like the Early Retirement/Financial Independence Spreadsheet Calculator where I estimated that we would reach financial independence between 8 to 15 years.

Today I’ll share a bit more of our financial independence assumptions.

How much is enough?

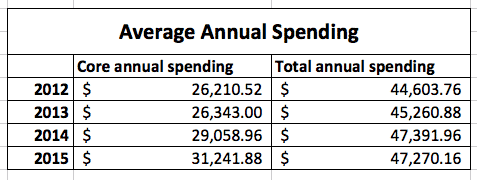

Based on our past 4 year annual expenses, our annual core expenses, which include housing expenses, utilities, food, insurance, gas and other essential expenses are roughly $32,000. That number adds up to roughly $48,000 if we include everything like vacations, dining out, charity donations, and business expenses.

But these numbers will most likely change given we have two growing kids. Let see take a quick look of what we need to cover in our future based on today’s expenses with some buffer designed-in.

Core expenses per month estimate

- House property taxes $350

- House maintenance $50 – luckily our house maintenance cost is low

- House insurance $100

- Utilities $100 – water, electricity, and natural gas

- Internet & cellphones $100

- Groceries $800 – two growing kids

- Healthcare $150 – based on current BC MSP premium. Only paying a small fraction of this today since my work pays for the majority of it

- Household supplies $100

- Clothing $100 – mostly for the growing kids. Mrs. T and I buy new clothes very rarely.

- Car insurance for 1 vehicle $120

- Gas for 1 vehicle $50 – probably will be driving less when reaching financial independence

- Car maintenance $50

- Buffer $200

Total: $2,270.

As mentioned, our core expenses do not include expenses like eating out, charity donation, entertainment, side-business expenses, vacation, and education saving for the kids.

We estimate about $950 per month to cover non-core expenses.

So that means a total of $3,220 per month in expenses, or $38,640 per year, which is significantly lower than our average expenses in the last four years.

Because these numbers are just estimates, they will probably change. It’s tough to estimate how much the two kids will eat, especially once both are teenagers (both Mrs. T and I ate a lot as teenagers).

Expediting financial independence

One of our goals, after achieving financial independence, is to travel around the world. This may involve living in a country for an extensive amount of time. For example, Mrs. T and I have talked about moving to Taiwan and Denmark in the future and living there for a couple of years while exploring the surrounding countries (obviously we would need to figure out Visa situation). Our overall expenses will change depending on where we live. Living in Taiwan or South East Asia will probably be a lot cheaper than living in Vancouver or Denmark. Another option is to move to a small town in Canada and live off the land like what the Frugalwoods are doing in their homestead. Since Mrs. T grew up on a farm, raising live stocks and living off them is not out of the question (I’ll have to learn how to be a farmer 🙂 ). Living somewhere else than Vancouver with a lower cost of living can certainly allow us to expedite our journey to financial independence.

One key thing to keep in mind is that we’re not set on our post-financial-independence plans. We are flexible and are willing to work around the circumstances. I truly believe this is a very important factor. Life is fluid and things can change on a daily basis. Setting a rigid plan simply doesn’t work.

How to fund retirement?

Since we are in the accumulation phase of our dividend portfolio still, we are adding a lot of new capital each year. When we reach financial independence, we don’t anticipate adding as much new capital, if anything at all. We will, however, continue investing in kids’ education funds (RESP). Why don’t we anticipate adding more capital in our dividend portfolio? First of all, because we don’t plan to withdraw the principal and only plan to live off dividend income, as long as our expenses are below the dividend, we are set. Second, we anticipate the dividend income to grow as companies continue raising their dividend payouts each year. Therefore, our dividend income should keep up with inflation. While we plan to pass the entire dividend portfolio to our kids and future grand-kids (exactly plans to be determined), it may make sense to withdraw a small amount of principal each year once we are in our 60’s or later.

To summarize, below are our plans to fund our early retirement or post-financial independence lives:

- A dividend investment portfolio around $1 million. This includes all registered (RRSP, TSFA) and non-registered investments. The target dividend income is $40,000 per year based on the assumptions discussed above. We will most likely withdraw a small amount of money from RRSP each year and transfer that money in TFSA or regular account.

- Part-time income. Both Mrs. T and I have established side-businesses. We will continue “working” in our side-businesses in some ways or form. Since I am keen in personal finance, I may pursue in becoming a financial advisor as a part-time job to help other people with their finance.

- Contract work. Reaching financial independence doesn’t mean I have to stop working. I may decide to do contract work with my existing employer or work for other high tech companies. Given that I have both technical and marketing/sales background, my skills are highly transferable.

- Here in Canada we have two government programs called Canadian Pension Plan (CPP) and Old Age Security (OAS). Both provide some income once you are 65. Given that we aim to reach financial independence in our early 40’s, we do not plan to rely on CPP and OAS for income. The way I see it, CPP and OAS are bonus money that we will receive when we are older.

And that’s it! A very simple plan.

There are a lot of assumptions but having a plan is better than not having a plan. The estimates also give us something to aim for. We will continue to work hard to save money and invest in dividend stocks. Given that our net worth has increased by 250% in the last 5 years, we’re doing really well. Our net worth may or may not continue growing at such astonishing rate. Either way, we look forward to the future and are very glad that we had our financial epiphany to get us started on our financial independence journey.

Dear readers, do you have any financial independence assumptions? What are your post financial independence plans? I would love to hear them from you.

P.S. In case you’re wondering, yes that is the $1,000 Canadian bill that used to be available (ceased in 2000 due to concerns with money laundering and organized crime). Once I saw an acquaintance pulling one of these out from her wallet to pay a large group dinner. I was shocked as I didn’t even know the bill existed.

P.P.S. If you like this blog, I would really appreciate and be honoured if you would consider nominating us for the Plutus Award. Thank you!

Hi Bob, as a parent who has gone through the expensive years (2 kids as well) I’d suggest you could perhaps double your estimates. But it all depends on how you live of course and the experiences that you deliver to your kids.

Our food monthly food bill was in the area of $1200-1400 while our daughter was away at University – we paid for her ongoing groceries, fuel for car and cell phone stuff. The boy was working out and gaining weight – lots of proteins, ha.

Our utilities (and plus all of the cell phones and data and more for family) likely in the range of $700 per month.

Our greatest expense, more than our mortgage, was sports and kids’ activities. Some years likely $13,000 – $14,000 annual with team trips and travel.

House repair budget the estimate near $500 monthly.

Car replacement and repairs $400 monthly.

RESP contributions $400 monthly.

Very easy to get to a doubling of estimates and then beyond.

Life with kids is much more expensive that many will think.

When I had changed jobs (to Tangerine Investments) I was in a negative cash flow situation for a few years, I had to drain my savings and spend small inheritance.

Hope my experience helps a bit 🙂

Dale

Good suggestions, it’s always good to know your experience. Will have to reconsider these numbers then. 🙂

I’d allocate more money for home maintenance and repair. When things break (between 12 and 15 years of age), they can get expensive. For ex: appliances, hot water tank, furnace, etc. I speak from experience.

Eventually, you’ll need to replace the roof, update the windows and fix other small things. $100 a month isn’t going to cut it… I recommend upping that # to at least $350, or replace / repair / maintain all big ticket items prior to leaving your day-time job.

Good point about housing related maintenance. It’s an area we’d have to save up before reaching financial independence.

Sounds like a plan similar to ours. Especially the part where you consider doing some work after hitting your number.

Very neat that our plans are similar. 🙂

If one is taking about $1Mil of invested dollars, not market value dollars and if you’ve invested with DG stocks, buying or adding when prices are down, then probably your yield will be more than 4% by the time you are ready to retire. I’m sure if you track your current yield on investments, they are growing. Setting & monitoring goals is the way to go.

I guess it can be both invested dollars or market value dollars, whichever will produce $40k per year of dividend income. Setting & monitoring goals is the way to go for sure.

Any idea how these plans will change with kids? Would you raise them as a Denmark citizen for example?

The plans already include the kids, they will be able to get Danish citizenship and can live there if they want to.

Great post here! And we seem to be on the same page….ideally, we would absolutely love to move to Ireland, that’s where our families are from, so we’d be going back home in a way. And while we do have a daughter, 12, we hardly have to spend any money on her, so what we’d spend goes right into an account for her, so she has quite a bit saved up. (Grandparents spoil her to death! She’s the 1st and only grandchild for now). And we do have some good stocks that we’ve invested in together when we 1st got married, and he has had some from before….so our portfolio looks very good. (He invested in what you’d call penny stocks when he was single……they’re “penny” no more). Good, sound advice here for anyone.

http://letstakethisonline.com/how-to-make-and-use-a-practical-budget-part-two/

Hi Ann,

That’s cool that we’re on the same page when it comes to FI assumptions. Sounds like the grandparents have been spoiling your daughter a lot. 🙂

It’s always refreshing to read about a straightforward, simple plan like yours, Tawcan. I’m also glad to see that your vision of FI/early-retirement still involves working part-time. When I tell others about my FIRE plans, they usually look at me like I’m crazy (some would argue that I am!). When I toss in the caveat that I plan to work in some capacity, they’re usually a bit more understanding.

Hi FinanceSuperhero,

Thanks. Too many people look at us that have a FI plan like we’re crazy. That’s why it’s so cool to talk to like-minded people.

Canada is really a good place and I believe it is a low-cost living country, you’d definitely enjoy. Which part of Canada are you planning to go?

No particular plan set yet, a small town in BC would be nice.

I just nominated you 🙂

All the best

From Denmark

Thanks Potofgold!

Hi,

I don’t see an expense item for mortgage, so I assume you have a fully paid home? Moving to Taiwan is a good idea. I enjoyed the culture there. I thought about this as well, because the cost of living is lower there. Health care is pretty good there as well. I truly dread health insurance in America. Not having a job in America means I have to pay for my own health insurance.

I plan either to move to Vancouver, Taipei, or Seattle post FI and spend more time with my family. The plans are still fuzzy but it’s consolidating. Dividends will likely cover most of my expenses. My pretax account, I have yet to decide what to do with it. Currently it’s stuck in company’s mutual fund, but once I’ve figured out post-tax account portfolio, I will move towards the pre-tax account. I don’t plan to withdraw until I’m 65, so I’m planning to rely my post FI expense on my post tax accounts. I view my pretax account to be my longer term investment and emergency fund.

Hi Pon,

We are assuming that our mortgage would be gone by the time we reach FI. 🙂

For the RRSP amount tied with my company I’ll probably just move them into self-managed RRSP and purchase more dividend stocks with that money.

There are definitely a lot of assumptions in there, but who cares. They aren’t unreasonable. I’m sure you were on the more conservative end of the spectrum anyway. I love how you discussed the need to be fluid and adapt since you don’t know what early retirement will bring. Isn’t that the point of financial independence, to have the freedom to do what you want, when you want, and where you want? Life would be boring anyway if you had every detail and minute planned out.

This also serves as a great roadmap for me as I go through a similar exercise with my wife! Thanks for the great read.

Bert

Hi Bert,

Exactly, like I said, having some estimates is better than no estimates and just give a blank look when someone asks. 😀

Would be interesting to see your assumptions.

1. “A dividend investment portfolio around $1 million.”

I like it 🙂 That should basically cover most expenses for the rest of your life and then some with barely touching the capital. This is our plan. We are ~42% of the way towards our goal. I hope to hit 45% by the end of this year. Fingers crossed.

2. Contract work. Smart.

3. CPP and OAS. With this, and a $1 M portfolio and no debt, you will be set.

Keep it up.

Glad I could inspire!

Mark

Thanks Mark for the inspiring post. 😀

Wow ~42% toward that 1M portfolio goal and 45% by end of this year. That’s totally awesome!

I have no assumptions as far as retirement goes because I want to be married by the time I reach financial independence so my current consumption is not reflective of consumption during retirement. I would like to have less stress after being independent. I think you have some well thought out reasonings behind all of your numbers and I learned something about the Canadian bill today!

Hi Finance Solver,

Interesting. Do you except to stay in FI once you are married? I’d assume things would change slightly.

We also treat college funds separate from our assets and planned withdrawal rate. I get the picture of a much lower cost of college education in Canada compared to the US. Is that assumption correct?

And planning for kids expansion – food consumption, cool clothes, sports gear, sports activities, perhaps a phone etc all add up. We wrote about future expenses and the “known unknowns”. But gotta start with best guesstimates to get the plan starting to roll.

My sense is it will be more that is required and having significant buffers from side income or a pension or a <4% withdrawal rate or all of the aforementioned will be key ( of course appreciating you have a dividend strategy).

Nice work.

Yes generally speaking university/college education in Canada is cheaper than the US. As far as I know Danish post secondary education is free so more reason to get the kids to study there.

Right I didn’t really put too much thoughts about cool clothes, sports gear, sports activities and such but figure the $300 buffer is sufficient. Or just give the kids a basketball or soccer ball and tell them to go nuts (that’s what I did when I was a kid).

Perhaps more is needed but the current estimate gives us a good start. 🙂

It’s impressive when you factor in how a little side income can change the equation.

If you want to have $50,000 to spend each year, and side income is $20,000, now you only need 25x the remaining $30,000 = $750,000 to be FI with income.

I am realizing this as I begin to monetize my blog. The future’s so bright, I gotta wear shades. You should turn that into an Amazon affiliate link to the song.

Cheers!

-PoF

Hi PoF,

Side income will greatly change the equation for sure! Every little bit counts. I have monetized this blog but probably not as effective as yours, currently just relying on Media.net and Amazon affiliate links.

We have a similar plan. Trying to plan for kids is a WAG at best, lol. This past 4th of July we did a cookout at my Mother-in-laws house and the cousins and their 6 tween kids were there and we planned for them to eat like kids, not teens, and man did they pack away the food. I remember I did a lot as well, so we’re not looking forward to that stage when the groceries increase. Plus, what about activities, what’s a good amount to plan for if any at all? Yep, lots to think about.

Our core and non-core spending is similar to yours, in that our non-core we’re around $50k/yr and core is closer to $30k/yr ish… That’s with some buffers put in as well, and not counting any potential side income, so we’re pretty good with that plan.

It looks like you’re in a similar boat as well, and at least you have established side businesses prior to FIRE. Way to go!

Hi Mr. SSC,

Baby T1.0 is only 2.5 years old but sometimes he eats way more than me. It’s kind of scary to think how much he will eat when he’s a teenager. 🙂

Sounds like we have similar spending. Your expenses will probably cut back quite a bit by not using any day-care.

I continue to enjoy your write-ups and they mirror some of my own thought processes. One question: it appears that you’ve left off income taxes in your budget. At low income like this they are not too significant (5-7%?) but probably shouldn’t be ignored. Personally I use the estimator at simple tax to plan for this.

40K in dividend income and estimated expense of $38640 seems to be cutting it a bit fine. Personally I plan for at least a 10% buffer.

Hi Matt,

Really appreciate your comment. I left off income taxes in my FI budget because we anticipate our tax rate to be very low. Large portion of our investments are in TFSA so that will be tax free. Since dividends are very tax efficient, we don’t anticipate paying too much income taxes, if any at all, especially considering we plan to split the $40k between Mrs. T and I.

Well written and I did nominate you for a Plutus award. Just a couple of questions. When you talk about increasing your net worth 250% over the last five years are you including the value of your home.

Your FI goal is to build a $1MM portfolio of dividend paying stocks that will generate $40M in dividend income but what will be the inflation adjusted amount of your core expenses at that point in time ie will it be enough?

I always think about FI as the point in time when my after tax passive income equals or is greater than my annual core expenses.

I have already achieved FI and I still work but at stuff I enjoy. Why would you ever retire from something that you enjoy doing?

Thanks Mike, appreciate for the nomination. 🙂

Increasing by 250% I did include the value of our home. Yes the Vancouver real estate has increased value significantly but we have been quite a bit of increase in our investment portfolio as well.

In terms of $1M portfolio with $40k in dividend income… that’s based on today’s dollar amount. That’s 4% dividend yield. Given that we’re investing already and we anticipate our cost on yield will increase overtime, I believe we should be able to generate more than $40k with a $1M portfolio.

Good point about retiring from something that you enjoy doing. I wouldn’t call it “working” if you’re doing something that you enjoy.

It might be best to view FI as a ratio where % of FI equals after-tax passive income divided by core expenses. Sorry I’m a long time banker and I always think in terms of after tax cashflow. Based on the formula where would you stand today Tawcan? Your core expenses are $32M not sure what you can currently generate in after tax passive income.

Mike

Hi Mike,

Good point on the ratio. I have sort of ignored after-tax passive income because most of our dividend income are from TFSA and RRSP accounts. Receive some income from regular taxable accounts but since dividends are very tax efficient, tax rate is quite low I have to say. The one thing I need to do more investigation is how to withdraw money out from RRSP in our 40s or 50s without paying too high of a penalty.

Given that we are receiving ~$1,000 in dividend income per month and maybe 10% of that amount is received in taxable accounts, the after-tax passive income is probably in the range of $980 or so? At the estimated $3,220 per month FI budget, that means our FI ratio is at 30%. That’s just a rough estimate. Gets slightly more complicated when considering the tax consequences of taking out money from RRSP.

Hi Tawcan,

My wife and I are also planning on moving back to Taiwan to become an “international snowbird” once we reach FI. This allows our child (or children in the future) to establish a tie to his/her heritage, and hopefully picking up Mandarin Chinese while we’re there.

Since you guys are planning to live outside of Vancouver, one thing I think it’s worth considering is try to capitalize on your home, either by renting it out or down-sizing depends on your situation.

We’ve been trying to upgrade from our little town home for the past year, but came up empty in this ridiculous Vancouver real estate market. As a result, instead of taking on bigger mortgage for another 20+ years, we established a new plan to become mortgage free within 5 years and working harder towards FI.

Just like you, I don’t think I will stop “working” once we reach FI. I am planning to become a technical/business consultant within my industry, or lecturing/teaching part-time courses at a post-grad institution. Unfortunately, I do not an artistic person, and I always envy people who can make a money off their passion, talent and interest.

Cheers,

Jack

Hi Jack,

Really appreciate all of your comments so far. Keep them coming!

We’re teaching Baby T1.0 English, Danish and Mandarin. He understands all 3 and can speak all 3. Pretty neat for sure. But you’re right, it would be great to be able to live in Taiwan for a few years so the kids (Baby T1.0 and T2.0 once she’s older) can pick up some Mandarin. Would be great if Mrs. T can pick up some Mandarin too.

We are definitely considering renting out the house or down-sizing. Depends on how we decide to travel, it would certainly be great to have a home base.

We do the same with keeping track of monthly expenses and getting an idea of the average, but also understanding the changes over time (we also have a kid and realizing their expenses is hard to estimate). This is a great idea also to understand what your expected monthly expenses will be post retirement. We’re on the same page!!!

Hi The Green Swan,

Having some estimates is better than having no estimates at all. 🙂

Completely agree here! Putting in the effort to create estimates is not a waste of time. Life is fluid, as you correctly said, and we can always revise our estimates.

For example, I have a pretty good idea about what my dividend income will be for the year because I estimate and make conservative guesses about dividend growth. But there’s all kinds of things that happen (and are happening) since I made the initial estimate of $48k of dividend income.

That’s the beauty of having estimates, you can always adjust them. Last thing you want is to get caught completely off guard. I’d hate that to happen. 🙂