Since having our financial epiphany in 2011, we have changed how we view our finances and most importantly, how we invest our money. Dividend growth investing and index investing became our focus. As a result, the value of our dividend portfolio grew over the years and our dividend income went from $675.21 in 2011 to $42,305.81 in 2022. This year we’re on track to hit $49,00 in dividend income.

That’s a lot of progress in 13 years. Starting this blog and sharing our financial independence journey has been one of the best things I’ve done. I’m amazed at how many like-minded people I’ve been able to connect with and meet.

Many people are fascinated with our financial journey. I’m also very thankful for all the encouragement I have received from readers and other bloggers. Now, a small minority may consider that by writing about our FI journey and dividend income, I’m boasting about our financial success and being arrogant.

It’s unfortunate that some people think that way. Quite frankly, I don’t have the power to decide how people think about me or about this site. However, the reason I’ve kept writing this blog for over nine years is definitely not to boast about our financial successes. I wanted to chronicle our FI journey, help other people, connect with other like-minded people, and show it is possible to reach financial independence by having and sticking to a plan.

When I reflected on why some people may think that I’m being arrogant, I realized that perhaps I’ve been writing too much about our financial successes. Let me get something straight here. While we have had financial successes, I definitely have had my share of investment mistakes and failures as well.

Here are some of these mistakes and failures.

Buying mutual funds

One mistake I’ve made is buying mutual funds instead of buying dividend paying stocks or index ETFs.

Although I started investing early in my early 20s, I was buying mutual funds that bank financial advisers were recommending. I knew that minimizing Management Expense Ratio (MER) was a good idea but I’d often get persuaded by these “financial advisers” to go with actively managed funds. Simply because these funds had better historical returns.

Unfortunately, the actively managed funds also happened to have much higher MERs than mutual funds that tracked the different indexes. For some odd reason, I kept repeating this mistake again and again, even after reading books like “A Random Walk Down Wall Street.” I was not willing to do my homework and take charge of my own finances.

Instead, I wanted someone to look after my money and manage it for me so I didn’t have to.

I was lazy. I didn’t want to take the responsibility for my money.

Investing in actively managed mutual funds meant I was paying a large amount of fees.

What I should have done instead, was to invest my money in dividend growth stocks or simply invest in index ETFs. If I had purchased dividend stocks like Royal Bank, TD, Visa, and Johnson & Johnson over 15 years ago, I’d be sitting at a very comfortable yield on cost for these stocks, collecting great dividend payouts every quarter.

Likewise, index ETFs have much lower MER than most mutual funds. Even a small 0.5% difference in fee can make a HUGE difference in the long term.

If I were in my early 20s and starting to invest today, I’d forget about mutual funds and simply invest my money in one of the all equity ETFs.

One of the important lessons I learned as part of this failure is that the best person to manage your own finances if YOU, not someone else. Take charge of your own finances today. Don’t rely on someone else.

Not having a long term view

Another major failure I made in my early 20s was not having a long term view. I was too impatient.

When I entered the workforce after graduating from university, life was good. I was making more money than I ever had before. Since I had money left over each month, I decided to start investing money in the stock market by purchasing mutual funds (big mistake, see failure above).

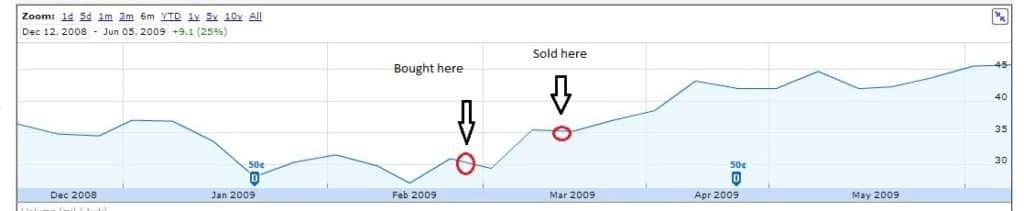

Then the financial crisis hit in 2008. As a result of the financial crisis, the stock market crashed. Since I had some spare cash lying around, I thought I’d take advantage of the down market by buying some top Canadian dividend stocks. One of the stocks I purchased was Royal Bank.

I purchased Royal Bank (RY.TO) at a heavily discounted price. My original plan was that I’d wait for the market to recover.

In case you’re wondering, I bought 100 shares of Royal Bank at $26.92 on Feb 26, 2009. I thought I purchased at an all-time low. All I could think of is to sell Royal Bank at a later date and get a nice profit.

Back then I didn’t know the power of dividend growth investing so I didn’t pay any attention to the fact that Royal Bank was paying a juicy yield.

The stock recovered a bit in early March but then the market started dropping again. Panicked, I decided to sell all 100 shares on March 3 at $29.05 to take in a small profit. I thought I was a genius.

Little did I know that the stock price would continue to climb after my sale. (Side note, after years of DIY investing, I learned that you simply cannot predict the bottom or the top of a stock).

Today, Royal Bank’s share price had appreciated by over 4.5 times if I had kept those 100 shares. I would have also received a nice amount of dividends since 2009. At the current dividend payout of $1.35 per share, that means my cost on yield would have been a jaw-dropping 18.6%!

Looking back, I definitely wish that I had held onto Royal Bank and used all the cash I had available to buy all the big 5 Canadian bank stocks during the financial crisis.

There are a few mistakes I made with this example of not taking the long-term perspective. One, I failed to realize that the likes of Royal Bank, The Bank of Montreal, CIBC, The Bank of Nova Scotia and TD all have been paying uninterrupted dividends since the late 1800s. I didn’t do my homework to learn about this important fact.

Furthermore, I failed to look at the big picture and the macroeconomic picture. While the financial sector was heavily hit during the financial crisis, Canadian banks were very well managed and didn’t have any danger of collapsing, unlike their American counterparts. I should have used the financial crisis as an opportunity to load up on Canadian banks.

Had I adopted a more patient, long-term view, I would have realize the all the major banks would have recovered, saw their stock prices rise substantially, and their dividends grow considerably. It is essential that you adopt that kind of long-term view if you are to be a successful investor.

Fortunately, I learned from this mistake and decided to take full advantage of the COVID-caused-market-melt-down in 2020.

Chasing yield

For some reason, I seem to keep making this mistake over and over again. Perhaps setting an annual dividend income goal somehow makes me chase higher dividend yield, higher risk dividend paying stocks subconsciously.

Back when we started investing in dividend paying stocks, we purchased the likes of Liquor Store and EnergyPlus. Both were yielding north of 5%, possibly higher. Not very knowledgeable back then, I didn’t realize such a high yield was not sustainable.

I made the same mistake around 2019/2020 when I started loading up on Inter Pipeline. While I knew Inter Pipeline had some debt issues and was facing some headwinds with the Heartland Petrochemical Complex Project, I ignored the potential warning signs, convinced myself the high yield was sustainable, and purchased more shares of Inter Pipeline.

When the crude oil price started dropping like a stone and the entire oil & gas sector started to crumble during the COVID-19 pandemic lockdown, it became obvious that Inter Pipeline’s only solution to improve its financial outlook was to reduce its dividend payout significantly.

The 72% dividend reduction by Inter Pipeline didn’t come as a surprise to me but it did hurt us by reducing our annual dividend income by over $1,000, due to the high number of shares we held.

The saving grace, somewhat, was Inter Pipeline getting aquried by Brookfield Inferstracture, which caused IPL’s stock price to increase slightly when we eventually closed out the position.

Similarly, I made the exact same mistake with Algonquin Power & Utilities. When I first started researching AQN, I was also surprised by the amount of debt AQN had. But I ignored that warning sign because so many other dividend investors were buying AQN at the time.

Just like Inter Pipeline, ignoring Algonquin’s considerable debt was a major failure on my part. They also were in the process of acquiring Kentucky Power which would require them to take on even more debt. Compounding the problem was that quite a bit of the company’s consolidated debt was subject to variable interest rates. When interest rates started going up, this negatively impacted AQN’s financials.

In AQN’s case, there were quite many red flags that I was ignoring. I was too focused on the high yield, which bit us in the rear end when the company announced a dividend cut…

Paying too much attention to analysts

Another failure I made was paying too much attention to analysts and believing all the things they said. Much of that commentary is simply ‘noise.’ For example, one-year price targets are really wishful thinking a lot of the time.

When I first started DIY investing, I used to look at analysts’ estimates, price targets, and recommendations. Is the stock a buy, a hold or a sell? I would then base my buying decision solely on these analysts’ recommendations.

More importantly, I would pay so much attention to the target price and believe that the stock would absolutely hit that target price. I’d make plans in my head about selling the stock and how much profit I’d make and how I’d spend that money.

I was way ahead of myself!

Over time, I realized the analysts may not know all that much more than the average investors like you and me. These analysts are using financial numbers and tools to come up with their recommendations. But even with all that knowledge, the analysis is right only 50% of the time.

I learned that it is vital to do my own research and analysis. It is also very important to understand if the company has any moats to fight off competition. Being able to look at the big picture (i.e. macroeconomics) is important as well.

I also realized that most of these analysts are analyzing stocks and providing recommendations from a short term point of view. They might be providing a “sell” recommendation simply because the stock price is trending down, not because the company is facing some macroeconomic challenges and most likely will recover a few months down the road.

Summary – My investment mistakes & failures

I certainly have had my share of investment mistakes & failures. This is totally expected. As investors, we will always make mistakes and have failures. Just as no investor has a 1.00 (i.e. 100%) batting average, none can accurately predict a stock’s low (in order to buy it) or a stock’s high (in order to sell it) all the time. The key is to limit them and limit your losses.

More importantly, it is important to learn from your mistakes and failures so you don’t repeat them and continue to lose money as a result.

Dear reader, have you made any investment mistakes & failures that you’d like to share?

Hi Bob,

My husband and I also were lazy and paid a fee-only investment advisor to handle our money but I realized that we paid him regardless if we made or lost money so after reading your blogs for the last two years I decided to do it myself. I even had a conversation with you over the phone and because of that and your blog I took the courage to manage our investments myself. I do not find your blogs being boastful, I learnt a lot from them and I appreciate what you do for this community. Please don’t give up.

Thank you for your kind words Marta.

Its like we walked through the same minefield together as I too started with mutual funds and made similar mistakes. Only difference was other than retirement savings I had no objective for my savings.

In hindsight, I should have searched for a mentor to help guide and focus my investments for varying goals in life. Now I am in a position to be a mentor to my young adult children. The bonus is it also gives us an opportunity to stay connected.

Thank you for sharing.

You’re welcome. I think you’ll find that many of us made the same mistakes.

Thanks for the retrospective and lessons that comes with time and experience It resonated a lot with me as my journey started around the same time but I was a decade older so I got the mutual fund mistake out of the way before I was able to really start saving for retirement. I too suffer from chasing yield even when I remind myself it’s total return that matters. Even today I have to stop myself from buying the stock with a higher yield when given the choice between two positions in the same sector. I owned all 3 examples you listed in that part of the post.

I bought LIQ years ago and held on even after the dividend cuts and renaming to Alcanna.

IPL was my first pipeline so I made out well. Not all our investing mistakes cost us financially.

And in a similar vein not getting rid of AQN when rates climbed and debt servicing became an issue. Even though I was cautious of payout ratio I learned the lesson of ensuring companies do not have a high D/E. More importantly, I have started watching a company’s credit facility and loan renewals. I am avoiding companies that have a lot of debt coming due in the next few years. A couple years ago I could care less about D/E especially for capital intensive business. Keep up the good work and all the best on your way to FI!

Yea we used to hold LIQ as well but closed it out way before the dividend cuts (phew).

Sounds like you have had some good tough investment lessons as well.

Thank you for sharing.

I bought-in the 1999 .COM craze losing around 1/3 of my net worth. I concluded the stock market was a casino. From then on, my savings languished in bank accounts and GICs for 20 years. I did briefly consider starting to buy the SPY etf in the fall of 2008, but was focusing on my career at the time. Thus losing out on the 0% interest era and the dream of an early retirement. With 2020, I started nibbling at Berkshire Hathaway and a few dividend stocks. Today I rejoice at buying GICs yielding above 5%.

Interesting that you’ve been investing in GICs for so long. Unless you plan to use GICs for short term investment, I’d caution about using GICs as long term investments.

Despite first buying SBUX 2007, I don’t feel like I’ve learned much. I’ve tried to but nothing seems to stick or be there when it comes to knowing to buy a stock. Some did well, some were doing well but I lost when I had to move Sept ’20 when lots had tanked due to covid, as well as losing $100,000 on the condo I had to move out of.

I currently have 32 stocks. Only 8 have gained (losses are everywhere I know…ENB, BNS, TD, AAPL) Three have lost a full 100%. Last Oct I bought FRO after reading someone’s article about it, which has gained 65% and pays 17% dividend. One of my luckiest..for now. But if you want a stock to fall, let me know. I’ll buy it and chances are good it will drop.

In TFSA and RSP I have five stocks in each, all of which are below purchase price. I think I’d have been better off with someone managing, paying MERs, cuz I’m not coming out ahead here. Retirement was supposed to be in three years (i’m 62) but it’s not going to happen..

Sorry to hear that you are seeing only 8 out of 32 stocks with gains. Are you reinvesting and dollar cost averaging at all? Can’t say I know anything about FRO but if it’s paying 17% dividend I’d be careful with such high yield.

FRO is an international shipping company for oil and oil products. Today it is up 68% since I bought it in April 2020. I reinvest dividends, saving some for taxes. The one other thing I have that is not at stock in a mortgage investment company, paying about 9% per year since I first bought it about 12 years ago.

In his book The Little Book of Behavioral Investing,3 James Montier explores the

folly of forecasting. It seems that, as humans, we just aren’t very good at it.

Economists have failed to predict the last four recessions, he writes, and

investment analysts are staggeringly wrong—two-year forecasts are wrong 94

percent of the time, and even 12-month forecasts have a miss rate of 45 percent

copied from the book 52week low Formula…pg29

That’s a great book to read. 🙂

Great stuff my friend. Will add for my upcoming Weekend Reading.

Funny, I wrote this in 2014. So much remains true. 🙂

https://www.myownadvisor.ca/financial-advice-younger-self/

I don’t know of any successful DIY investor that hasn’t made a few mistakes. Life is a learning process, investing is just a small sliver of that.

Continued success to you!

Mark

Thanks Mark. Funny how we think alike. 🙂

My biggest mistake was not understanding and feeling overwhelmed with all the stocks, GICS, mutual funds, and money market. When I started getting into stock investing, I was basically going with what everyone else was doing, such as buying weed stocks, bank stocks when it was an all time high and it just seems to be going higher, FOMO…

Right now, Im basically trying to keep my stock portfolio within 20 with a focus on dividend aristocrats and a couple of growth stocks. I also get annoyed with theres corporate buy outs or mergers, I never did get lucky with those and end up losing money… 2020 was challenging seeing huge drops in the overall net-worth, and nervous on buying more. Too many unknowns.

In the meantime, 18k in dividends per year so far, not bad considering I started in 2018.

With the lessons learned about AQN and IPL, I am stumped on how to fully understand how to avoid problems like this for the future. Considering all companies have a debt ratio and theres always some sort of growing pains involved as well.

I love reading and following your blog, It helps me be more proactive for my semi retirement in 8 years when I turn 50. My end goal is to enjoy my relaxing week and just work on weekends. Keep up with the awesome blog and happy Thanksgiving.

Edmonton Canada Post Mailman.

Jason

Congrats on the $18k in dividend income! We all make mistakes, it’s important to learn from them. 🙂

I started serious investing around 2007 and came across the great recession which left my belief in the Financial system shaken. I sold a lot of my stock when it started to recover after 2009, so missed out on a lot of gains. However, I dont have a lot of confidence in the Financial markets and I still am very bearish overall and fear a big collapse owing to many reasons such as debt, global interdependence, inflation & risk of deflation. Overall I see theres lot of manipulation in the stock markets which gives me jitters putting my hard earned money into it.

I get your point, some of us do get the jitters for putting money in the stock market after experiencing crashes. My suggestion would be making sure you’re properly diversified across the different asset types (i.e. stocks, bonds, savings, etc).

My brother’s biggest mistake was not having given anyone power of attorney. When he had a massive stroke ten years ago, he became a ward of the provincial government. They sold all of his stock portfolio and replaced it with Canadian savings bonds. He went from $60k/yr in dividends to $10k/yr in interest, and no change in principal. He’s still angry.

Everyone needs to assign a power of attorney, especially people who are not married.

Sorry to hear about your brother. Yes, designate power of attorney and have a will are very important.

Can u explain more on power of attorney if you have accounts in questrade with a beneficiary are you not covered?

Beneficiary and power of attorney are two different things.

Power of attorney = someone that can make decisions for you while you are capable of making decisions

Beneficiary = person or entity that you legally designate to receive the benefits from your financial product

Who do you designate when you have no partner/children/extended family or friends younger than you? Most of my friends are all 10 years+, and I’m 63.

That’s a good question, I’m not 100% sure if you’re able to designate a charity of choice. Suggest you look into this with the financial institution.

I follow a number of successful personal finance bloggers and they’ve all said (somewhere in one or more of their posts) they get naysayers and it can get them down. Whether these naysayers be trolls, envious or just bad in giving constructive criticism, please don’t let them discourage you. Reading about your approach and thought process during your journey towards FI is a valuable service. I personally appreciate the effort you put out (even if I disagree with some of it).

I’ve lost on penny stocks, not selling losers like Nortel and Blackberry and falling for the averaging-down theory on stocks with no real hope. Most recently I am finding companies like CI Global Asset Management are changing the structure of their funds and then refusing to answer questions, yet I haven’t sold off the units. Greed and emotion is often a common denominator of failures I’ve experienced.

That’s too bad about CI Global Asset Management, hopefully you’ll get answers from them soon.

Hi Mr. T.

I am so thankful for your Monday e-mails. I appreciate you sharing your knowledge with us, your readers. I am happy for your good fortune in investing and you are paying it forward by sharing what you have learned. Thank you! Happy Thanksgiving.

Happy Thanksgiving to you too Diane. I really appreciate your kind words.

I always thought investing in stocks was a major gamble. Years ago, I would add to my RRSP and buy whatever the company mutual fund was recommended. I can’t even tell you how much I lost along the way with the dot com crash, 2008, etc. I didn’t have the time or patience to do the research, being busy with my career and raising young children – I was lucky to get a good night’s sleep. In the early days, it wasn’t easy so I think we all fell victim to the mutual fund system. Once it became easier (internet, blogs, questrade/wealthsimple), I was too busy running my own company so I wanted someone to manage it. Even with all the failures I still had enough of a portfolio for it to be actively managed by Wood Gundy but their cut of 1.5% is ridiculous. I finally started to try to invest on my own, and compare their results to mine. During the covid crash I moved everything, and was able to tax harvest the losses. But still, I was afraid to do it all myself so some of it was moved where I have a Bank “manager” helping me. What I didn’t realize when I bought ETFs that they are really MFs in disguise. I’m waiting for things to crash again so I can sell my non-reg at a loss and move over to manage 100% on my own. I’m slowly getting there…and I look back at what I didn’t know. I actually worked for a couple of the banks and they matched if you bought their stock. If I only held onto BMO and CM, my yield would be crazy now. But of course, the fund managers sold it all and invested in their pricey MFs. It’s made me very skeptical about the experts and now I don’t trust any of their advice. LOL

Because I didn’t know what I was doing, I followed a couch potato portfolio of ETFs. With the losses I experienced in the past, I was a 60/40 investor. Another mistake because I could have earned so much more during my accumulation phase. And you can imagine what happened to my 40% bonds, that really hurt my portfolio as interest rates went up. I still have a chunk in bonds that I’m hanging on to with a hope it will improve one day – I am in it for the long haul. I want to retire soon (early) so I’ve been focusing on buying dividend paying stocks – and I fell into the BTSX strategy so I can get an income even when the market is down. I’ve lost with AQN as well, I didn’t see it coming – I thought they’d be solid as a utility and also was inclined to go with a company involved in renewables. In the last couple of years most of my dividend stocks aren’t doing well – interest rates are doing a number on the banks, utilities and telcos. I just have to be patient for things to bounce back! The good news is I’ll generate dividend income even if things stay stagnant – as long as they don’t cut their dividend!

I think many of us fell for AQN and now are hurting because of that. As investors we all make mistakes. The key is to learn from these mistakes so you can limit the number of mistakes you make in the future.

Hi Bob. This is one of the best articles I’ve read on investing. We have all made mistakes and your efforts to share them with others is very commendable and most appreciated. I have shared this article with my children. Keep up your excellent work. I wish you well and give blessings. How appropriate that it’s Thanksgiving. Keep well

I really appreciate your kind words Kevin.

Mutual funds: What a scam!

My biggest mistakes: Being lazy and fearful, not doing my homework (i.e. learn how to trade stocks with Questrade, which started in 2009, I believe). What saved me? A discipline of iron; I would invest in a GIC just about every month, always 5-year terms, getting 8, 9, 10 % return in the 80s and 90s.

So glad I found your blog!

Thank you Pierre. We all live and learn.

I also made mistakes in my investment journey. I used a broker when I first started. When I got my annual phone call, it was always what I should sell and what I should buy with the proceeds. As my portfolio got a little larger, I started reading personal finance newsletters (there were no blogs back then). I did not pick up the idea of buy and hold stocks as they were always touting what to sell and what to buy instead. After I read MoneySense magazine, I learned about diversification and ETFs based on indexes. It was then that I started with TD’s online broker to look after some investments myself. As they started to make sense to me and my broker could not answer some questions, I switched my entire portfolio to my online accounts. After a while, I learned about dividend growth investing and haven’t looked back since. I still have an ETF based on the SP500 but my Canadian investments are all in stocks paying dividends. The personal finance world continues to evolve so instead of calling them mistakes, I view it as my education curve. Happy Thanksgiving.

Congrats to you Jan for taking charge of your own investment.

Interesting read. I am on the same journey as you in the investing world. I still making mistakes and hopefully your blogs and shared experience can help me to avoid that. Therefore keep your blogs coming.

Thank you Hui.

I was like you, I was into mutual funds with RBC from 2003 to 2015. On hindsight, it was a mistake, but back then investing was not as easy to do on your own like today is. Back then, I don’t recall seeing any online platform like wealthsimple or Questrade in which you could buy ETF’s with no comission. If they did exist, I wasn’t aware of it yet.

My biggest mistake was in 2021 when I sold all my ETF’s and bought a bunch of Canadian dividend stocks, constantly buying in and out of stocks, most likely because I had no strategy. Even worse, it was all Canadian stocks, no International stocks like the US market.

Although I faired ok overall, my portfolio went nowhere because of the “no strategy”. I kept changing stocks like I change clothes on a daily basis.

What saved my portfolio for those 2 lost years was the fact that I was applying the Canadian Couch Potato strategy (basically investing in VGRO) from 2015 to 2021 or else I would have nothing to show for it…I would argue I probably lost most gains I could’ve made through the bull market of 2020-21.

This year is the first year I have a full plan, 80% of my investment each pay goes towards one of my 3 etf’s (VDY, VXC, QQC) and the other 20% goes towards one of my 10 individual stocks and I keep those 10 and only sell if the fundamental of those 10 deteriorates. I also have a personal rule not to add more than 10 stocks in my portfolio for fear that I start doing like in 2021 when I had over 40 companies. Just 10 that I truly believe in for the long term. So far so good and I am loving this plan.

So, all this to say, anyone who never made a mistake with their portfolio is a liar….we all do them.

Agree with you Fil, investing wasn’t as easy as what we have today so relying on mutual funds or brokers make sense then. Having no long term strategy and keep buying in and out is one mistake a lot of us have made.

Hi.

I enjoy your newsletter and find it helpful, even as a retired Wealth Advisor and Chartered Investment Manager (CIM).

I do take issue with a blanket statement saying “you are the only person who should manage your finances “. You better have a mountain of free time to review knowledgeably tax levels and withdrawal strategies, merits of RSP vs TFSA vs HBP vs RDSP vs HBSA vs RESP vs non-registered investing. When and why to take CPP or postpone it years. Dealing with finances and illness, insurance and estate planning. A professional has invested years of full time hours on these topics and can provide guidance and hand holding that more than makes the fees involved good value. Should people be their own lawyer? Doctor?

Anyway, keep up the informative and helpful posts.

Hi Paul,

Thank you.

By “you’re the only person who should manage your finances” I didn’t mean that you shouldn’t rely on experts. What I meant is that you should take full interest/responsibility in managing your own finances instead of relying other people to manage it for you and not pay any attention. There are certainly times that I rely on experts to help me navigate tax planning. It’s the same with doctors, you need to take care of your health yourself. If you’re eating unhealthy and do not exercise regularly, rely on a health professional probably won’t do you any good.

Hope this clarifies the statement.

Your investment journey has been an inspiration to me. Please don’t give the naysayers a second thought. You have passed on your wisdom and experiences to the rest of us and we are very appreciative!

Happy Thanksgiving, we are all so blessed to be living on this wonderful continent.

Thank you Gary.

I love this. We were late to the game with taking charge of our investments and made many of these same mistakes using mutual funds and advisors, and selling good stocks. Covid was certainly an exercise in emotional control when we saw a lot of dips in our portfolio. But armed with new knowledge and blogs like yours, it helped to keep focused on our goals instead of all that “noise” (and reduce the panic selling)

Thank you Alphonse. It’s important to learn from your mistakes. 🙂

Great article. Thanks for sharing! I’m wondering if you think Algonquin might turn around in time? I’ve been trying to decide if I should hold on or exit my position.

Thanks.

Thanks Fiona. We’ve tried to be as patient as possible with AQN but the share price keeps dropping. Certainly doesn’t help the market has been trending down lately. At this point, we might consider trimmer a bit of AQN.