Like many Canadians, early in my investing career, I was investing in high fee mutual funds and the high fees were eating into my returns. I started dabbling in DIY investing but I didn’t get very serious about it until around 2010.

When it comes to DIY investing, I would group DIY investors into two categories. Investors in the first category are people that rely completely on low cost index ETFs. They purchase ETFs on their own and re-balance them regularly. In the past few years, the emergence of all-in-one ETFs like VGRO and XGRO and all-equity ETFs like VEQT and XEQT have significantly simplified the investing process for these investors.

DIY investors in the second category are people that invest in individual stocks and possibly index ETFs as well. These investors study and research individual stocks and make the requisite buying and selling decisions.

As you’d expect, we fall in the second category. We manage our own portfolio and invest in both index ETFs and individual stocks. We have adopted this approach because we want to be more involved with our money and have more control over it. I also enjoy learning about investment-related topics and how to analyze stocks.

I will admit that I have made A LOT of investment mistakes throughout the years. However, investing mistakes are inevitable. The important thing is that we learn from them. That is the absolutely crucial thing as we all make mistakes; it is the learning from those mistakes that distinguishes the good/great investor from the mediocre/poor one.

So, I thought I’d share my learning from my investment mistakes and hopefully help readers to avoid the same mistakes.

Learning from my own investment mistakes

Here are some investment mistakes I have made since I started managing our investment portfolio. They are not specific to only dividend growth stock investing.

Note: These mistakes aren’t in any particular order.

Mistake #1: Not doing proper research

When we first started with dividend investing, I knew very little about how to analyze dividend growth stocks. Like many new dividend investors, I was very much focused on only one metric – high yield. I was not paying any attention to other key metrics like payout ratio, dividend streak, or dividend growth rate. I certainly wasn’t keeping a dividend scorecard.

I stumbled onto a high yield dividend stock called Liquor Store in 2012. At first, I was overjoyed to find a dividend stock in the alcohol industry. Without doing my own research, I assumed that Liquor Store owned and operated all the liquor stores in Canada. I bought $1,500 worth of Liquor Store thinking I had hit the jackpot.

The first couple of years, I was really happy collecting dividends but the share price stayed flat. Upon further research, I learned that I was deeply mistaken. Unlike what I initially assumed, Liquor Store operated privately owned stores. The company operated 230 retail liquor stores in Canada and the US. In other words, the company was competing against Crown-owned liquor stores.

The business certainly wasn’t as rosy as I originally anticipated. The stock price then took a beating when BC introduced legislation to allow licensed grocery stores to sell BC wine.

Due to the deteriorating business environment, Liquor Store cut its dividend in 2016 and we exited this position shortly after, taking around 50% loss, not counting dividends collected.

Although I was deploying the be an owner strategy, I didn’t do my due diligence and learn more about the company. I failed to understand that the company was operating privately owned stores. I also failed to realize the Liquor Store only had a small fraction of the market share and was competing against Crown-owned liquor stores in Canadian provinces.

The biggest mistake? I foolishly assumed that since people would regularly buy alcohol, therefore the company would always be highly profitable, and the dividends would be safe.

I was simply too naive.

What did I learn from this mistake? I learned to always do research about the company regardless of whether I know the company very well or not. Never assume that I know something and never let my ego take over. At a minimum, learn about the company by going over investor presentations that most companies have under their investor relations. It is also important to go over quarterly and annual reports or consult websites such as Morningstar, Yahoo Finance, Marketbeat, Digrin, Seeking Alpha, Simply Wall St, etc.

In case you’re wondering, Liquor Store eventually was de-listed. It is now part of Alcanna (CLIQ.TO).

Mistake #2: Being greedy, not following my own rules

When I graduated in 2006 and entered the workforce, my company’s stock was trading around $15 per share. After my three-month probation period, I enrolled myself in the share purchase program and purchased company stocks with a portion of my pay-cheque every two weeks (the company matched 15% of my contribution).

The stock price went up to $22 in 2007 but I decided to keep my shares instead of selling them.

Then the financial crisis happened and the company stock went down the drain. My company stopped the share purchase program and I owned a few hundred shares at a cost basis in the low teens.

Early in 2009, the company stock went all the way down to just below $4 a share. It sat around that price for a few months. Being young and with some money saved up, I decided to purchase 300 shares at $3.93. I then purchased a few hundred shares more as the stock price climbed its way up to around $10.

Altogether, I owned less than 2,000 of my company shares. Knowing that the company was not profitable at the time and that I could be easily replaced in a blink of an eye, I decided that it was not a good idea to put all my money in one basket, so I invested my money elsewhere (i.e. high fee mutual funds).

My company turned itself around in 2012 and the stock price started climbing. At one point, I told myself that I’d sell everything when the stock hit $20.

Throughout 2013, the stock price kept climbing, reaching a high of $25. The company was firing on all cylinders – we had won many multi-million deals with key customers and we were gaining market shares. I sold a few hundred shares to take in some profit. But I was not satisfied. I believed that the stock price would keep climbing.

I was being greedy and wanted to make more money.

So I kept most of my shares.

The stock price continued to climb. First, it was $30 per share. I told myself I’d wait for a little bit longer and sell when the price hit $35.

The stock price hit $35. Once again, I told myself I’d wait for $40.

Then the stock price hit $40 and I told myself I’d wait for $45 before selling everything.

The stock price went higher and higher. It was exhilarating. Everyone in the company was excited and happy about the stock price.

In early 2015, the stock price hit a high of just below $55. I thought about selling all my shares at the time but decided to reset my selling target to $60.

I was crunching numbers and imagining how much money I’d profit if I sold all my shares at $60.

But the stock price never got anywhere close to $60. In about three months’ time, the share price quickly tumbled from a high of around $55 to just below $20.

I was kicking myself for not selling my shares at higher prices. A year later the stock price eventually climbed back up. Seeing that I missed the boat the first time and didn’t want to miss my chance again, I sold a few hundred shares at a time as the stock price climbed its way up to $35.

What lesson did I learn? First of all, I was being too greedy and wanted to sell things at a high point. But I couldn’t have predicted where the top was so I completely missed it. Although it’s fine to increase my selling target incrementally, what I should have done was to sell some shares along the way and take in profits while the stock price was going up, instead of just holding onto all the shares and keeping increasing my selling target price.

Investing has a lot to do with being patient, setting and executing strategies as flawlessly as possible, and not letting your ego get in the way. In this instance, I totally got my ego in the way. I needed to learn to have an exit plan and execute this exit plan according to it, rather than continuously deviating from it.

Mistake #3: Not thinking long term

I purchased a number of Google shares in October 2012, a few days after Google announced a terrible quarterly result and the stock price went for a slide. At around $340 a share, I thought the per-share price was high but when I looked at the PE ratio and how much cash Google had, I thought I purchased Google shares at a discount (remember, you can’t just look at the stock price alone and claim it’s expensive).

I’ve always wanted to own Google shares, ever since I started using Google for internet searches in the late 1990s. I was amazed at how good and efficient Google was compared to other search engines like Yahoo, Altavista, and Excite (remember them?). As a teenager, I was convinced that Google would be extremely profitable. In the early 2000s, on several occasions, I told my dad to invest in Google if the company was to go public.

Neither of us ever followed up on that idea until over a decade later. But that’s a story for another time…

I was really happy to finally own a few Google shares, although looking back, I wished I purchased more shares (don’t we all?).

In late 2014, Google announced a 2 for 1 split. Two classes of shares were created – the voting class GOOGL shares and the non-voting class shares GOOG.

After receiving my new shares of GOOG, I decided that I would sell them and only hold onto my GOOGL shares. In my mind, I thought it wasn’t worth holding onto no-voting shares. More importantly, for some unknown reason, I had the impression Google had stopped growing and stopped innovating.

This impression was something I created completely on my own. Looking back, it was probably because Google’s stock price was bouncing around $600 throughout 2014 and I was losing my patience. I failed to do much research into Google’s businesses and didn’t realize that Google was getting into the Cloud, artificial intelligence and home automation with their acquisition of DeepMind and Nest. I also failed to value the huge revenue potentials from Android and Android apps.

Essentially, I failed to look at the long term potentials of Google. I was being narrow-minded and only looked at Google as an internet search engine and generating money from advertising. I failed to realize that Google was bigger than just the internet search engine. I was only thinking about the short term.

In fact, Google CEO Larry Page and his teams were acquiring and building other segments of business and broadening the Google empire.

In 2015, Google restructured itself as Alphabet, a multinational technology conglomerate holding company that owns several companies, including Google. Some of its products include artificial intelligence, automation, autonomous cars, biotechnology, cloud computer, computer hardware, healthcare, robotics, and software.

Nowadays, Alphabet is even bigger than ever. We are even more dependent on Alphabet products than ever. Just recently, Alphabet announced a 20 to 1 split, the second split in company history since 2014.

I can’t help but kick myself for being shortsighted and selling my GOOG shares back in 2014. On the bright side, I did keep my GOOGL shares and do not plan to sell any time soon.

Therefore, when analyzing a company, always look at the big picture (i.e. macro environment). Always consider the company’s long term profitability and growth potential.

Mistake #4: Only look at dividend growth rate

Enter Laurentian Bank (LB.TO) for mistake #4.

A few years ago, I was looking at dividend stocks that were growing dividends at a high rate. After looking at the Canadian Dividend All Star list and the respective historical dividend growth rate, I narrowed it down to Laurentian Bank as one of the dividend growth stocks to add to our dividend portfolio. Per my 2018 dividend consideration:

“Laurentian Bank has seen its share price retreating the last little while. At a PE ratio of 9.9, it is one of the cheapest Canadian banks available from a PE ratio evaluation point of view. With a 10-year dividend payout increase streak and a 10-year dividend growth rate of 7.8%, LB has a solid dividend track record.

LB certainly isn’t as big as the big 5 Canadian banks, with most of its branches in eastern Canada. So from a future growth point of view, LB may not grow as quickly compared to its Canadian peers.

One of the concerns with Laurentian Bank is that it has high exposure to residential mortgages. In the fourth-quarter earnings, LB disclosed that an internal audit found some documentation issues on some mortgages it had sold to a third-party company. As a result, the bank has decided to buy back $392 million of problematic mortgages from the third-party.

Having said all that, I think at the current share price, it may make sense to purchase some shares of LB, collect dividend income, and see what the future holds.

Furthermore, it also makes sense to expand our banking exposure to outside of the Canadian big 6. Laurentian Bank of Canada is relatively small compared to the Canadian Big 6. If LB manages to grow outside of eastern Canada and possibly internationally in the future, the earnings will up.”

We started purchasing LB shares in January 2018 and nibbled on more shares throughout 2018. By the end of our purchases, we owned just under 150 shares at around a $46 cost basis.

After we purchased LB shares, the stock price began to slide. Since it paid dividends at a good yield, I wasn’t too worried. I figured we could collect dividends and wait for the share price to recover.

Unfortunately, the stock price never went back up to $46 again. To make matters worse, when the COVID-19 global pandemic started, Laurentian Bank reduced its dividends by 40% from $0.67 to $0.40 per share and the stock fell dramatically.

We ended up exiting this position in late 2020, taking quite a bit of a loss as a result. In case you’re wondering, we switched from LB.TO to one of the big six so overall we did pretty well.

Looking back, I can’t help but return to my original statements like “Laurentian Bank isn’t as big as the big 5 Canadian banks,” “LB may not grow as quickly compared to its Canadian peers,” and “LB has a high exposure to residential mortgages.”

Most importantly, I failed to look at the big picture and the macroeconomics of Canadian banks. Being a smaller bank and having high exposure to residential mortgages, Laurentian Bank was already a riskier bet to begin with. It didn’t take much to set the entire business upside down.

While the uncertainties of the global pandemic had sent the global stock market on a free fall, many stocks have recovered since. However, Laurentian Bank has yet to recover. If we had held onto our LB shares, we would still be in the red!

I learned that I shouldn’t just pay attention to the historical dividend growth rate. It is far more important to understand the macro environment and how the company fits in that big picture.

Mistake #5: Not believing my investment thesis

This is the last mistake I’ll write for this post but it’s certainly not the last mistake I’ve made or will make…

When I started investing in Potash Corp in mid-2014 and Agrium in mid-2015 I came up with a simple investment thesis on why I’d invest in these companies – People need food. With an increasing world population, more food is needed and therefore, the demands for fertilizer will only increase over time.

The fertilizer business seems like an easy to understand business. Start a mine, dig out fertilizer from the mine, sell it, and rack in the profits.

For some reason, both Potash and Agrium struggled with their share prices. Since the fertilizer sector was very cyclical, we also encountered a dividend payout reduction of 60% by Potash a few years ago.

Through all the turmoils, we continued to hold both Potash and Agrium shares because I believed in my investment thesis. I continued to believe that the demand for fertilizer will only increase over time and the need for more food to supply the global population will be extremely important.

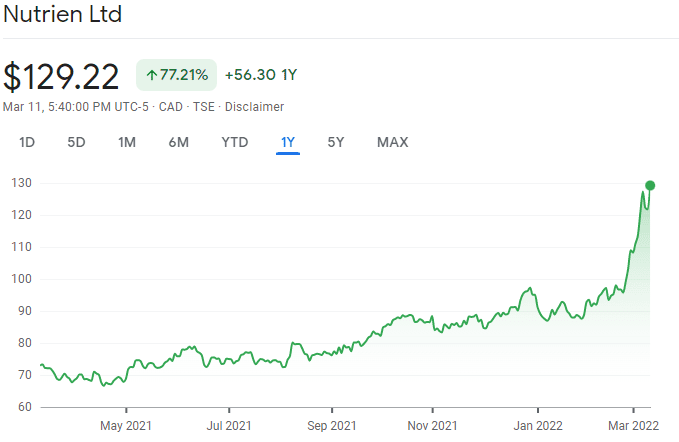

Eventually, Potash and Agrium merged together into Nutrien. The merger created one of the largest producers of potash and nitrogen. We decided to continue to hold Nutrien shares.

That all changed when the global pandemic started in March 2020. With the idea of reducing the number of stocks in mind, we closed out several positions throughout 2020, and we decided to sell all of our Nutrien shares in 2021.

My reason? Nutrien’s stock price had done very little over the last few years. I thought we’d do better by investing our money elsewhere. I stopped believing in my investment thesis completely.

Well, as our luck would have it, Nutrien stock price went for a run shortly after we sold everything. The climb in share price was mostly caused by strong demand and higher prices for fertilizers, supported by the strengthening of global agriculture markets.

Nutrien’s stock price really went for a ride when Russia invaded Ukraine with aid from Belarus. Since Russia and Belarus are the world’s second and third largest potash producers after Canada, the economic sanctions placed upon Russia and Belarus have caused a major and long-lasting disruption to the fertilizer market.

Given all the major global supply constraints, I expect Nutrien’s stock price to continue to soar.

Did we make a major mistake in selling Nutrien and not believing in our investment thesis?

Most definitely!

But when it comes to investing in individual stocks, you win some and you lose some. The important part is to have more winners than losers. This is very different from investing in a low cost index fund where you’re tracking the market performance minus fees.

Summary – Learn from my own investment mistakes

As you can see, I have made many investment mistakes and I will most likely continue to make these mistakes. While mistakes are usually painful and lead to leaving money on the table – or losing it – it is far more important to learn from these mistakes, so we don’t keep repeating them.

I hope I can help readers learn a few lessons by sharing my own mistakes.

Dear readers, what lessons have you learned from your investment mistakes?

Hi Guys,

Came across your site by accident & reading of your experiences took me back a lot of years. I became interested in the market back in my early twenties & am now in the mid 80’s. Ironically, my story is a lot like yours as I started in the early 60’s when my salary was about $4,800 per year. I remember buying some oil & mining stocks for pennies in the early years & realizing fantastic profits while at the same time seeing some of my purchases drop to zero. It sure takes awhile to figure out how to determine what makes a company sucessful & what indicates that a future for many others is highly unlikely……I had some huge winners but also some (luckily) fewer duds. It took me awhile to realize that what I was doing was, in effect simply gambling. I figured that I had better get myself educated in the ways of the market if I intended to stay in this game & be sucessful at it. I started reading the G&Mail, read a few books on investments, subscribed to The Money Letter etc. I read & read everything I could get me hands on. These moves proved to be the end of my “gambling”.

I think the first stock I bought after becoming more clued in was Kresge on the U.S. market. They were just coming into Canada & were getting set to open their K-Mart stores. I remember buying about 25 shares from a company called Pitfield Securities & the guy I dealt with had never even heard of Kresge/K-mart. Anyway, the stock really started to move & he told me that his manager had called his H.O. & asked them to look into the company & after their research came back, they decided to put a # of their clients into stock. Well, the stock rocketed after their K-mart program took off & they made a lot of the clients pretty happy. I, like you sold a few shares to get my $$ back but held that stock for many years until they began to falter & did not keep up with the new kids on the block….Walmart etc. I sold all my shares & never looked at the co. again.

After lot’s more reading I, (again like you), moved into the dividend stocks full tilt……I now had a few $$$$ free money & was hell bent on not losing it. I bought some Cnd. & U.S. banks & some ENB & TRP & have watched them grow & split over the years…..my next one was FTS again in the teens.

These were bought because I looked into the future & thought I could see the best way to get our oil around was by pipelines & that FTS, a small electic utility in Nf’land had a mg’ment team that were really astute money folks. All of these stocks paid dividends & kept on raising them & went on to split their shares. All this gave me the $$$ to make a few bets on the new oil & gas Cos. that were springing up out west, however, now I was making sure to find out all I could about the mg’ment team…their backgrounds etc & reading, reading & listening to financial news etc.

To-day, I am lucky enough to be able to get into some stocks that I see a real future for down the road…I am able to hold onto these for a couple of years ’til they reall get their acts to-gether because some small .cos Like an ERD doing work in Mongolia are really unique in that they support local school & health programs, give the locals a chance to buy their shares etc. etc. But will not have any cash flow for a year or 2 but have drilling results that are superb. They seem to undrstand that rather than waving the flag they want to be sure that when they start pouring gold that all of their ducks are in order & there won’t be any surprises. These are the kinds of things I leave to my kids & g’kids with instructions to give as much of these $$ as possible to hospital research & less fortunate people, food banks etc. I have discovered that by far the biggest satisfaction I derive from the markets these days is being able to give back!!

I wish all of your new investors all the luck in the world, however, never forget that luck is a tiny part of the investing world reading everthing you can get your hands on & knowing where your $$$ are going is so very important. You are never smarter than the market!! Be well read!!

Thanks for this long and insightful comment Gerry. As investors we need to continue to learn. Most importantly, don’t assume things just because they have gone one way previously. The market can change depending on the environment, nothing is static.

Hi Bob!

it is by far the most interesting article you wrote this year so far I think! Thank you for your willingness to share your own investment mistakes so that others can learn from 🙂

I too 1wish I had bought Nutrien before it took off.. it will be many years before their price drop down to what I think is good PE.. sighs

another regret of mine is that I sold my Costco shares too soon! Yesterday they hit over $600 at some points and I wish I didn’t sell so early when they were only $572.

I hope to learn from my mistakes and hold on stocks that I had certain principles behind original purchase…

Sarah – you make some really good points . I bought Nutrien many years back and just held it in my “bull pen” truly it was dead -money for a while , but I keep it adding in May of 2020 . It is technically one of those companies that people “need”, not want. I like to buy “Need” as opposed to “want” companies(Tesla- although love the concept and technology’ best in class’) .BIPC is a NEED company and so on . Technically Nutrien is a valuable food crop. Potash is an essential ingredient to any sort of farm growing operation these days. Cant grow a bean or rice kernel without it . There isn’t an unlimited supply either . About four sites in the world that produce a lot and are economically feasible. Saskatchewan is one of them. As for Costco – I was lucky on this one , I bought 1100 shares in October of 1990 . I drove down to Kirkland Washington and viewed a couple of their stores etc … I saw alot of promise in the concept, the the ‘need’ concept . So I bought 1100 shares at 10.25 USD and thought I paid way too much- I thought I got hosed !!!! . It recovered quickly over a couple of years and grew its cash flow like crazy ! I kept it . I was going to buy a second car with the money 12 K roughly I spent on the shares ….SO glad I did not . It split around 1998 (?) at a rate or 2:1 ….and I suspect it will split again if it goes over 700USD or our economy tanks . More luck than research I think . But my lesson was . Hang on to those conviction companies that have good metrics ! Growing good key metrics is key though I think ( unlike GE – although ‘best in class on medical machines and Aerospace / GE-90 engine etc …) … the SP looks after itself down the road , so long as its a “need” company , and key metrics are excellent . Happy investing guys ! . Great information here Bob! James V

Hi James, wow $10.25 per share on costco?!? Congrats on your good investment acumen. Man gone are those good days… I could not take advantage of those due to my infancy haha your anecdote is another reminder that time in the market is the best tool for investment growth. Millenials like me must now a days take the risk and invest in the US big tech and or green growth companies (E.g. Tesla, Google, Amazon, Invesco Solar ETF, etc) with the hopes that these riskier stocks we choose will one day mature into “need” companies. One thing I do thanks to Tawcan is that I balanced my growth oriented portfolio with more mature and dividend paying Canadian companies. With the market downturn these past 2 months, I am glad that I mixed my portfolio! Given that I still have 30-40 more years left till retirement, I am always on the look out for some cyclical price dips for the mature dividend companies (e.g. COST, RCI.B, TD, Fortis etc) to increase dividend stocks over time. I wish prosperous AND prudent investing to you all 🙂

Congrats on buying Costco at such amazing price. Definitely hold onto those conviction companies that have good metrics.

Hi Bob,

You’re one of the few people that’s still around from my early days of blogging and going super strong! I’m really amazed at both your financial results, the life you’ve been able to build for your family and yourself, and the large community you’ve managed to gather here.

Even with all those investing mistakes you’ve done wonderful. I think that shows how good our baseline strategy is and how focussed we are on what we want. The issue that hit home to me the most definitely was greed… It’s so difficult not to be greedy sometimes: the rational part of my brain competing with the emotional part, haha.

I’m glad to have read up on your progress, keep it up!

Kind regards,

NMW

Hi NMW,

Great to hear from you again. I see you’re writing again, that’s fantastic! Hopefully you’re not eating as many waffles nowadays?

Truth be told, I really do like waffles… But my saving and investing game is still strong, no worries! 😉

I’m really enjoying writing again, and the feedback from our community so far has been great.

Thank you for taking the time to reply!

HI Bob and Mrs T,

I have had the same epiphany with regards to mutuals funds. I have been so wrong! I feel embarrassed and have some major FOMO. But the next best time to plant a tree is today.

I will never be FIRE, as we have a farm with a large debt. My goal is to give my kids a generous RESP and be ready for retirement without leaning on the family farm too much, in order to give that next generation a head start. Thank you for your well written posts and willingness to share.

Rule #1 is hugely important. Often times, very attractive dividends are sort of ponzi in a way: they are debt-heavy and/or not in a very good cash flowing position. As a result, QoQ dividends are just return OF capital, creating the illusion that you’re getting a return ON capital. And it’s the last people that get out that ends up paying the most.

Agree. It’s important to do your own research and your due diligence when it comes to investing individual stocks.

Thank you for your honesty Bob! I love reading all your articles, but particularly why you recommend certain stocks. One of those stocks was Nutrien! I am also grateful for the link to Mr. Tako’s dividend scorecard. Wonderful article! I’m going to revise my tracking spreadsheet with his suggestions. Thank you again 🙂

You’re very welcome, Laura.

Thanks for sharing your mistakes and lessons learned, Bob. It is always great to see how we learn and move on.

I remember when I wanted to get rich overnight and started doing day trading many years ago! It went very well the first couple months making 100s then 1000s but eventually the greed and emotions took over and I ended the game with a bit over $20K of loss. I then switched to GICs until last year when I started over with a new mindset.

Day trading is easy to lose big and win big. 🙂

Day trading to GIC’s ? Man! Talk about polar opposites . Day trading is very risky even for the most seasoned Did the GIC’s even keep pace with real inflation? Why not” real return bonds “ or the like ? I view GIC’s a temporary parking spot , as it looses money generally against real inflation and is taxed adversely. Banks love GIC deposits. They take the money in at – and lend it out at an ace of 8.5%. Over double the arbitrage

Yep, I also sold Nutrien too soon. Oops

Great post!

Thank you.

Super interesting read. Investing in individual stocks is definitely a crash course in learning to live with hypotheticals.

My question would be, how do you separate the true lessons learned (I.e., you could do better next time) vs. hindsight bias. Your company could have shot to the moon, and google could have struggled post-2015. Impossible to know in the moment. Thanks!

That’s a very good question Marc. Hindsight is 20/20. Having said that, there were obvious signs that Google would continue to do well that I completely ignored. 🙂

My mistake centres around listening to the hype on CNBC or BNN and buying on stocks historical reputation.

TEVA, GE, DB, KMI are big mistakes I’ve made. Buffet bought TEVA so I thought it would be good .

Historically General Electric, Kinder Morgan and Deutsche Bank have been strong well managed companies. But there was a lot of hidden malfeasance, corruption and fraud going on behind corporate doors .

Good news is I diversify and these were only 1-5% of my portfolio. Also I got capital loss tax wise

We used to own GE and KMI as well and those were certainly investing lessons we’ve learned.

Dont be too hard on yourself with GE . Even today some analysts have a strong buy on it – another reason to do your own research ! I think GE has fooled everyone at one point or another. So many pension funds invested in it in “good-faith” ….not knowing the fraud that was taking place on their books and other , under the previous regime . The Current leaders have done little to improve the street image and the recent “rollback” they did … did nothing to impress the street . Rollbacks to increase trading price is a ‘death spiral move ‘ in most cases . The Health Division and Aerospace Division in the company are world class , and are second to none in technology ( GE 90 Jet engine is probably the best in the world for long range use and durability) …. yet mechanically the company just a flop these days . Maybe …just maybe , the split-up pending into 3-5 divisions will bare fruits !? Happy investing guys !

I bought a few shares of Google stock around 2008. It was probably one of my biggest wins. I sold the non-voting shares this year just to diversify. The major US index all have a lot of tech and it made sense to me to not have so much Google.

There are times when I haven’t been greedy enough. I bought Facebook at $19 when everyone wasn’t sure what they’d do about mobile. I sold at around $35. Now, I have a plan of selling off partial amounts as a stock goes up. I’ll rarely hit a big homerun for a 10x gain, but selling and reinvesting is working for me.

A lot of coulda, shoulda, woulda when it comes to investing. 🙂

When Facebook when IPO I never thought they’d become the empire today. I wasn’t sure about their business model. So little I knew back then.

Wonderful article Bob. Concise, well written, and clear. You have brought up five key points to follow. I can summarise these: stick to one’s goals, and evaluation methods.

Thanks for writing your weekly blog!

Dan

Thank you Daniel, I appreciate it.

Great commentary Bob , as usual . Mistakes are meant to be learned from and you do . We all make them, even the most researched analysts make them. One mistake you didn’t make is getting out of Mutual funds. In Canada our MER’s ( Expense costs eating up your profits win or loose ) are the most expensive in the world ….at least 150% higher than the USA as well… on average. I don’t know why Canadians keep money in these Mutual funds at these VERY high costs compounded , baffling . Canadians in general are clearly are a different lot when it comes to investing costs, and investing in general . The problem is as well, in Canada they don’t teach ANY finance in the primary grades . In Asia, where I grew up as a foreigner kid, we had finance classes from about grade 6 onward . By grade 8 we could all read a fundamental balance sheet. The teachers were very well versed in Finance . Here – not so much .

Thank you James. Many mutual funds have very high MER’s indeed. It’s good that there are more investment choices available nowadays.

We definitely need to refresh our K-12 system. There need to be more personal finance topics in schools.

I absolutely agree! Much more focus needs to be put on money management, financial goals and the whole investing market in general.

When I/we moved back to Canada , after growing up in the Philipines since I was an infant, I was 15 , I was amazed at how far back the “basics” were, and especially economics and finance!… Zero knowledge. We also had ‘National Studies’ that was mandatory – it was about the importance of the Philippine culture and the great history of the Philippines as a nation and Nationalism – Could you imagine in Canada’s schools ? ( mandatory…even though I was a foreigner kid at a private school! HA!!) Sure, I went to a private school but even the public schools in the major cities were up to speed on finance and the basics. …concerns me going forward in Canada. Take Care/ Happy Investing ….. J .

Good morning, Bob

Thanks for writing and posting this article. It is valuable to me since I have also made my share of mistakes, mostly considering my lack of ‘proper research’. I have a question: do you use technical analysis when you research stocks? I use http://www.stockta.com for example, as part of my research. In general, where can I find more info on how to research stocks?

I look forward to your reply.

Cheers

Bill

Hi Bill,

I did take a few technical analysis courses before but I don’t trade using technical analysis anymore. I usually do research on free sites like Yahoo Finance, Morningstar, and company websites. I’ve come to like FAST Graphs but that’s a paid site.

Great stuff Bob, as usual. You are one of the top five blogs I follow. I appreciate your transparency and willingness to share. Plus no hype and no junk! Keep up the good work and I’ll keep reading and learning. Matt

I appreciate your kind words, Matt. Thank you very much.