Becoming financial independence is simple but it is not an easy task. It takes years of planning and hard work to hit this simple yet challenging goal. We have always set a target of becoming financially independent sometime in our 40’s. On the About page, I provided a more specific timeline:

Through frugality, dividend stock investing, and other passive income streams, I am targeting to reach financial independence in 2025 or earlier (in my early 40’s). My wife and I want to become financially independent to gain more freedom and choices in life. When financially independent, I plan to continue working. My ultimate dream is to one day travel around the world and live in different countries for extended periods of time to learn about the local culture and explore the surrounding area.

In reality, we don’t have our hearts set to a specific year. Becoming financially independent sometime in our 40’s would be fantastic.

What if we were to aim to reach financial independence by 2025? Are we on track?

Let’s take a closer look at the two key elements on becoming financially independent – Expenses and Passive Income.

Controlling our expenses

Below are our historical expenses and our 2017 expenses so far.

| Total Core Spending | Core Spending per Month | Total Annual Spending | Total Spending per Month | |

|---|---|---|---|---|

| 2012 | $26,210.52 | $2,184.21 | $44,603.76 | $3,716.98 |

| 2013 | $26,343.00 | $2,195.25 | $45,260.88 | $3,771.74 |

| 2014 | $29,058.96 | $2,421.58 | $47,391.96 | $3,949.33 |

| 2015 | $31,256.88 | $2,604.74 | $47,270.16 | $3,939.18 |

| 2016 | $29,831.40 | $2,485.95 | $4,7566.96 | $3,963.91 |

| 2017 (after 5 months) | $15,267.47 | $3,053.49 | $19,224.14 | $3,844.83 |

| 2017 (after 5 months, minus unexpected expenses) | $12,984.96 | $2,596.99 | $16,941.63 | $3,388.33 |

As you can see, our 2017 core monthly average has gone up quite a bit compared to the previous years. An extra of $600 per month in expenses is a bit concerning. However the $600 per month increase is due to a couple of unexpected major expenses and the purchase of a small green house. If we take out these expenses, our core monthly spending drops down from $3,053.49 to $2,596.99. At $2,596.99 per month core spending, this roughly aligns with the other years. Considering there are 7 more months in 2017, we are hopeful that we can lower our monthly core expenses.

When we are financially independent and not working, we expect our expenses to be lower. In our financial independence assumptions, we estimated our total expenses to be $38,640 per year, or $3,220 per month.

For conservative estimate, we will assume that $40,000 to $50,000 per year of passive income is needed to be financially independent. It is hard to estimate the exact amount since many things will change over the next 6- 16 years.

Controlling our expenses is critical. The lower the expenses, the easier and faster it is to achieve financial independence. This is why we track our expenses and review & analyze them on a regular basis.

Using dividend income to cover expenses

For this particular simulation, we will assume are we financial independent when dividend income can cover 100% of our annual expenses.

Below is our historical dividend income and the respective YOY growth rate.

| Dividend Income | % YOY Growth | |

|---|---|---|

| 2011 | $675.21 | N/A |

| 2012 | $2,484.37 | 267.94% |

| 2013 | $5,456.20 | 119.62% |

| 2014 | $8,362.30 | 53.26% |

| 2015 | $10,318.02 | 23.39% |

| 2016 | $12,559.74 | 21.73% |

One thing that jumped out right away is that our YOY growth rate is decreasing. This, however, is an expected behaviour.

As dividend income amount gets larger, it becomes more difficult to have a high YOY growth rate.

For example, going from $100 dividend income to $200 dividend income (a 100% YOY growth) requires $3,334 of fresh capital. This is assuming there is no organic dividend growth and a 3% dividend yield. Adding over $3,000 to an investment portfolio is a relatively easy task for most people.

Now consider going from $20,000 to $22,000 in dividend income (a 10% YOY growth). This requires $66,667 of fresh capital assuming there is no organic dividend growth and a 3% dividend yield. This is a much harder task because $66,667 is not a small lose change for most people.

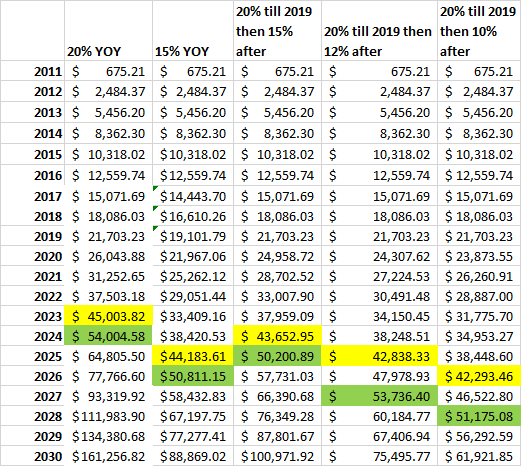

With a decreasing YOY growth in mind, I ran a few different dividend income simulations.

Based on these simulations, we can hit ~$50,000 in dividend income somewhere between 2024 and 2028 (highlighted in green above). This roughly aligns with my 2025 estimate.

If $40,000 is needed to reach FI, then we can achieve FI somewhere between 2023 and 2025 (highlighted in yellow above). Again this roughly aligns with the 2025 FI estimate.

Overall, it’s comforting to know that we are on track with our goal of achieving FI in our 40’s. But we are using a lot of assumptions and estimates. Is it valid to use these YOY growth rates? Or should we use lower YOY growth rates?

Expediting our financial independence journey

Are there ways to expedite our financial independence journey? Absolutely! Here are a few ways we might be able to expedite our FI journey.

- Increase family income. Right now we are a single income family. Once both kids go to school, Mrs. T can spend more time on her businesses and bring in more income each month. This will allow us to add more money in our dividend portfolio each month.

- Reduce our expenses. This may mean cutting back on a few luxuries. Is this the right call? Hard to say. Looking at our past 5 year expenses, I think we have gotten our expenses mostly in control. Currently I am more on the side of finding the right personal balance between spending today and saving for the future rather than extreme saving.

- Move to a lower cost of living city or country. For example a smaller Canadian city, Taiwan, or South East Asia.

- Sell our house and use part of the proceeds to add dividend stocks to our dividend portfolio. We would then either relocate to a lower cost of living area or get a smaller house.

- Right now we plan to live off dividend income only. We do not plan to sell any stocks. We can expedite our FI journey if we were to sell a small portion of our portfolio each year and use the money in conjunction with dividend income.

- Create other passive income streams so we don’t have to rely 100% on dividend income to cover our expenses.

Final thoughts

A closer look at our financial independence journey reveals that we are roughly on track with our timeline of becoming financially independent sometime in our 40’s. One key thing to keep in mind is that we are not set on our post-financial-independence plans.

Mrs. T and I continue to remind ourselves to be flexible. We need to be flexible and fluid with our future plans and goals. Things, plans, and people can all change. We need to be adoptable for these changes.

We may do a partial FI by relying on dividend income and work part time. Or we may prolong our FI journey by shifting our timeline to sometime in our early 50’s.

Whether we decide to expedite our financial independence journey or not that remains to be seen. For now we are thankful and grateful to be where we are financially, especially considering that our net worth grew by 34.4% in 2016.

For the most part, we have been setting our finances on auto pilot. We will continue doing all the things that we have been doing since our financial epiphany. We will practice being patient and enjoy our financial independence journey. 🙂

Bob, how do go about picking the selection of ‘dividend’ investments, stocks, funds or ETF’s in your huge portfolio?

Do you use something such as the flavour of the day/month, what is being promoted to the list of companies with the largest profit or largest market cap or what others are doing or a tip?

https://en.wikipedia.org/wiki/List_of_largest_public_companies_in_Canada_by_profit

https://en.wikipedia.org/wiki/List_of_public_corporations_by_market_capitalization

Be interest to know

thanks

Here’s a piece I did on selecting dividend stocks:

https://www.tawcan.com/start-investing-dividend-paying-stocks/

thanks, that was a decent general informative basic information based on what it is that you do to inform those who are considering getting into stock trading investing.

Do you still follow this principle yourself or have other sources that help you pick your selections?

I’m still curious how you picked the current 75 or so positions that you are currently have as well as when you turn the inventory, if ever?

Do you ever sell any positions, do you have a stop loss criteria?

A few random thoughts questions

Hat tip to Garth Turner for this one but what about using an RRSP to defer taxes. You’d be getting a big deduction now and then withdrawing the money when you’re earning less? Or as an alternative to use a spousal RRSP to transfer income to the wife.

Along the same lines have you calculated the tax numbers once you stop working?

Speaking of working don’t forget to calculate you true hourly wage,

http://www.wikihow.com/Calculate-Your-Real-Hourly-Wage

Which brings me to my next point, you mentioned about your wife having a business, which is a good idea as it allows you to deduct normal household expense. But how would that compare to her simply taking a good paying job for a few years. After you deduct the extra costs associated with a two income family it should leave with a decent chunk of change for investments. Say 5 years of full time work and volia you’re both retired.

I seem to remember that you once interviewed a fellow CDN who hit FI and stopped working. Any idea was his FI income was and or how it compares to your number.

Yup the plan is to withdraw RRSP once we have very little or no active income to minimize tax impact. We are now focusing on getting spousal RRSP to have the similar portfolio value as mine so we can income split for RRSP withdrawals.

Here’s a piece I did on tax assumptions:

https://www.tawcan.com/our-financial-independence-assumptions-what-about-taxes/

If she takes a good paying job for a few years, we’d be paying for child care. At this point we think the two would negate each other. We figure it’s better for my wife to look after the kids and build the mom-kids relationship rather than having someone else looking after the kids. I’ll have to ask J a bit on what his FI numbers and compare to ours. 🙂

Thanks for letting us follow along on your journey. Awesome stuff and I have very little doubt you’ll meet your goal. What other passive income streams are you considering?

Thanks, I have very little doubt that we’ll hit the goal, it’s a matter of when.

Doing great on the spending side! We are trying to lower our spending to save even more (currently at 60%) but the further you go, the harder it gets 🙂

Thanks, I think we can improve on our expenses but we’d be sacrificing a few things and it’d become a bit unbalanced to our preference.

Finding the balance between spend now and saving is key. I have a post coming on that. To me, it is a top priority to decide on that. This balance will decide on your timeline and your overall happiness now and later.

Glad to hear that we think alike! Looking forward to reading the post.

Yep there is a balance. I cant ask my family to live like peasants (I could). However I explain to them there is a balance and stuff doesn’t buy you happiness.

Later,

DFG

I used to live like peasants when I was living by myself before I met Mrs. T. It’s definitely harder to do with a family.

It’s great you’ve got such clear goals and good tracking, something inspiring for sure. I might calculate growth in portfolio yield based my savings rate, dividend yield and (geometric) growth in dividend yield (on cost?). It might be too tricky with the assumptions such that is meaningless but I’d have a crack at it and see. One thing I would love to do is semi retire to europe or japan and work in the local community a couple days a week, socialise, blog, write and see the world on the other days (the local world that is).

Good suggestions, I suppose we can definitely do a bit more complex analysis. One key thing I have left out is inflation which will definitely come into play to determine FI timeline. Semi retire to Europe or Japan, and other countries sound like a fantastic idea.

When I first looked at your annual dividend income table, I immediately thought that it was growing around $2000-$3000 a year. I didn’t focus on YoY growth because the numbers on the left seemed to show a better pattern.

If you average those out, maybe they come to around $2400 increase in dividend income a year? By my basic napkin-math, you need around $27,000 more in dividend income to reach $40K. From your $12,500 level today, I would add another 11 years (27,000/ $2400) and put a 2028 estimate for $40,000.

If you start seeing that left column showing exponential rather linear growth, maybe adjust the timeline?

Also, as you say, there are things you can do to change the timeline.

Yes the calculations weren’t all that complicated, I could have used a more complicated projection and using fancy math. But things will change so there’s no point to hang up on the minute details. It’s definitely a lot of fresh cash needed each year but since we reinvest all of our dividends, as it grows, we get to invest more back into the portfolio and let it compound.

Tawcan –

Great article and a deeper perspective and review of where you’re and REALLY peeling back the expense layer and overall dividend growth layer, I love it. Pumped that you are on pace, as well, to hit that adjustable target. What’s interesting is that to really set in on an age/time – you almost need to have an idea/plan of what you really want to dive into with your passions and heart, then – the day that you want to retire, will be that much clearer. Very interesting…

-Lanny

Hi Lanny,

Yes expenses and dividend growth go hand in hand when it comes to achieving FI. 🙂

Bob, since it appears your target date to FI and/or retire is before the age of collecting any government old age pension, my only input to you is that dividend/passive income should be twice your annual expenses. If you can achieve this, then you are totally FI.

If you can build into that any inflation increases, then all the better.

Since you are in Canada, your passive income should always be at the lowest tax payable.

You’ve pointed out in your blog that your primary ‘passive investments/income’ goal will come from registered accounts TFSA & RRSP’s, non-registered accounts/investments & a sideline business.

So to get to FI you are stating you would need in the range of $4000 – $5000/mth income. That done would give you ‘time on your side’ without punching a clock or having a boss/paycheque to be chase or be dependant on.

Key for most is ‘mortgage free’, some folks don’t do this & will continue to pull equity from their home/property/investments to leverage further investments. That’s OK too, providing one knows what they’re doing, most don’t (use Donald Trump as an example).

Do you stop contributing to RRSP’s just to save some income tax?

Do you keep loading up the tax free TFSA’s to max the return that gives you DGI returns at not less than 5%/yr compounded?

Plow as much as possible into non-registered investments that earn dividends only, so that you reach $50,000/yr in dividend income which will be basically tax free in Canada due to ‘dividend tax credits’?

Continue to work part-time, at your own pace, at your own leisure?

What ever you do…. family & health first. Investing so that it isn’t complicated & that one can sleep at night while the investments grow.

Having passive income twice than annual expenses would create a nice safety net, it’s something to think about. The plan is definitely to load up on dividend stocks in non-registered accounts. 🙂

I sometimes have a hard time deciding between saving for the future and enjoying life. Our food expenses just exploded last month (~$800). It was definitely higher than usual, and we will try to cut down our food expenses this month. But eating is such a big joy in our lives. I guess we just need to keep a better balance.

Our food expenses have been a bit high this year but we did end up having one more mouth to feed (Baby T2.0) compared to last year. We are also trying to eat more organic food so that increases the food cost. Eating healthy is important for us and it’s good for the long term well-being.

As a beginning dividend investor myself, it’s inspiring to see someone like you who has grown their dividend growth so significantly in such a short period of time. It’s awesome to see your dividend snowball growing at such a consistent pace, keep up the great work Tawcan!

Thanks Zach. It does take years to build up a dividend portfolio. 🙂

These days I can only manage about a 10% dividend growth rate. At some point, organic growth becomes more important; finding that much new capital gets hard when you break $50k+ per year (166k in new capital at a 3% yield).

Such is the life of financial independence.

I think it’s smart you guys aren’t setting your post-FI goals yet. Your life is going to really change between then and now. You’ll be amazed how much the journey changes a person.

Yeah your dividend portfolio is WAY larger than ours and when it comes to that point organic dividend growth becomes more important. You can compound the organic dividend growth by DRIPing shares.

But yes, that’s the life of financial independence. It’s a good problem to have let’s just put it that way.

Hi Tawan!

20% YOY growth is ambitious, but sustainable if you’re purchasing a lot of dividends each year.

Can you do calculation with 18% growth for 2018, 16% for 2019, 14% for 2020, 12% for 2021, and then 10% each from 2020 onwards?

How does that change the #s? That growth might be more conservative and would give you a more accurate idea on when you’ll reach your FI target.

Yes 20% YOY growth is pretty ambitious but I think we can do it for another few years.

If we do the calculation based on the parameters that you provided we’ll cover $40k in 2026 and $50k in 2028. Both are more or less align with our FI estimate. 🙂