Yup, you guessed it, another post called Random Thoughts from Taiwan… because I’m in Taiwan again!

So greetings from Taiwan everyone!

This marks the 4th work trip to Taiwan for me in the past year, once in September 2022 where I had to quarantine for 4 days, a quick 6 day trip in February this year, and then another work trip to Taiwan and Hong Kong in May.

This time around, I’m spending 7 days in Taiwan and 2 days in Hong Kong. Unfortunately, due to company travel policy changes, I’m back to flying in economy class. No more wine and dine in business class or premium economy!

Unless something drastic happens, this will be my last work trip for 2023. Although work trips are usually very interesting and I enjoy them, it’d be nice to stay on the ground for a few months…

A very long first day

My flight departure was 2 AM in the morning, the day before I had an early meeting at 7:30 AM in the morning and didn’t wrap up my work day until 5:30 PM. Knowing I would have a long day, I planned ahead and sneaked in a 1 hour nap in the afternoon so I could get some rest.

I slept for about 4.5 hours on the flight. Changing into pajama pants, wearing a comfortable hoodie, wearing noise cancellation headphones, and wearing a sleep mask all definitely helped. But getting a decent sleep sitting mostly upright was obviously challenging.

It was definitely a treat to be able to lie completely flat in business class… I was better rested on the flight.

Anyway, I arrived in Taiwan just after 5 AM on a weekday. I made the hotel reservation starting from the night before so I could check in, get a little bit of sleep, and take a quick shower before starting my work day.

The first day was pretty rough, I had a couple of customer meetings in Taipei, sat through a business review, dinner with co-workers, then a program review at 10 PM that I had to present for half an hour (the program review is a weekly meeting that happens at 7 AM Pacific).

Needless to say, a lot of coffee was consumed on that first day.

Randon thoughts from Taiwan

Here are some random thoughts about my fourth trip to Taiwan in the past year…

1. The travel industry

My EVA Air flight was completely packed. Clearly, a lot of people have been heading to Taiwan from Vancouver.

It’s odd that Air Canada hasn’t started its Vancouver to Taiwan direct flight yet. Hopefully, they will soon as I prefer the AC flight’s arrival time (around dinner time which makes the arrival day a bit easier as you can have dinner, try to stay up for a bit, then go to bed).

It seems that air travel has picked up because all the flights I have been in the last year have all been completely packed.

The hotel night rate has also gone up quite a bit in Taiwan. The Courtyard Marriott I stayed in Taipei was about $260 a night. In 2020, I paid just under $200 CAD per night at the same hotel. The Marriott hotel I stayed at back in May was about $40-50 more expensive in comparison.

Some of the other Marriott properties in Taiwan were charging over $400 per night when I was making hotel reservations. The same type of inflated hotel night rates can be observed in North America as well.

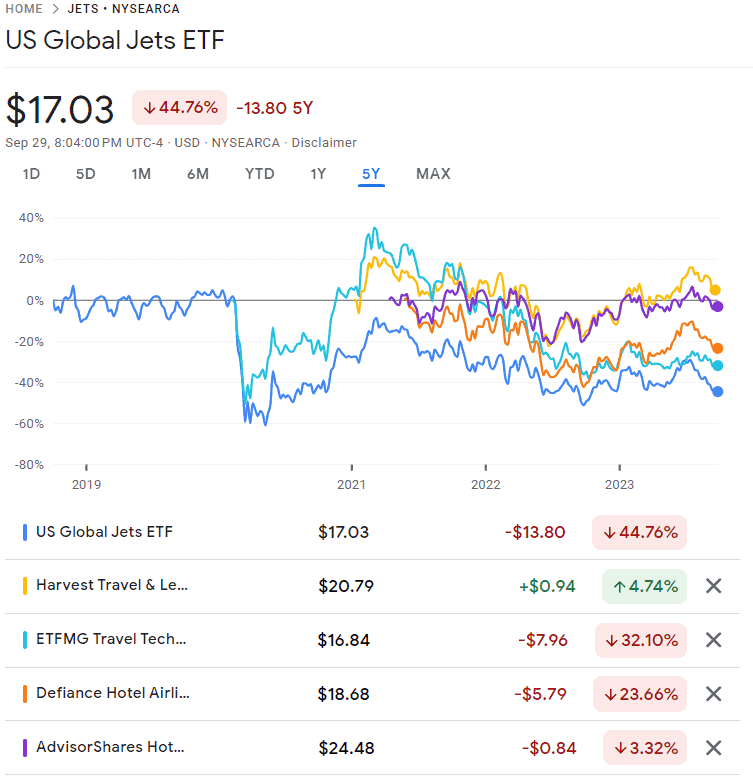

Given that travelling has picked up (and probably recovered?) since the pandemic, you’d think that these travel related ETFs would be doing well. Oddly enough, they aren’t…

Perhaps the travel industry is still recovering from the two years of pandemic lockdown and restrictions? I guess high inflation and higher costs (oil, employee salary, food) are negatively affecting these companies’ profitability.

2. Eating out in Taiwan

Generally, it’s pretty cheap to eat out in Taipei if you’re OK with local cuisine and eating at somewhat sketchy looking shops.

You can get a local Taiwanese cuisine meal for less than $5 CAD. Finding a place that has nicer ambience may increase the meal cost to about $10 to $15 CAD, still quite reasonable.

However, there’s a huge disparity in restaurant prices once you step into the higher end places. You can certainly find restaurants that cost more than $100 CAD per person in Taipei.

Having said that, if you do an apples-to-apples comparison, eating out is cheaper in Taiwan than in Vancouver. For example, you can get a really nice Japanese omakase (chef’s choice menu) starting at around $50 CAD in Taipei. Similar omakase would start around $100 CAD here in Vancouver. I found a nice Japanese BBQ place with tons of wagyu beef for around $45 CAD per person. A similar meal in Vancouver would cost more than $80 per person.

No wonder there’s a large expat population in Taiwan.

3. Reflecting on the FIRE future

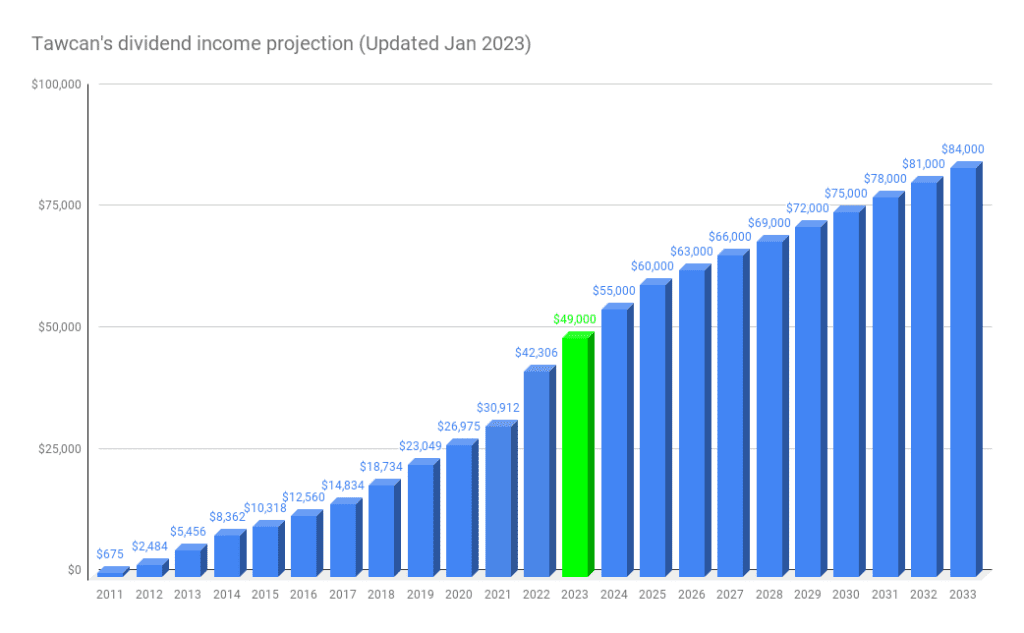

Based on my dividend income projection, we are about $100 or so away from receiving $50,000 dividend income this year. In other words, we are slightly ahead of our dividend income projection and we’re basically at our original dividend income target of $50,000 per year.

At $50,000 dividend income per year and with some level of part-time work, say generating $20,000 a year, we should have more than enough to sustain our current lifestyle. Getting $60,000 in dividend income per year would provide a bit more margin of safety. So this will be something we are working towards in the next few years.

At this point, I can certainly step back from my full time high tech job if I really wanted to. Since I am enjoying what I’m doing and enjoying the challenges, there’s no plan to send in my two-week notice any time soon. But it’s comforting to know we have options.

Lately, I’ve been thinking about questions like…

- When I talk about working part time, what does that mean exactly?

- What would my “FIRE” life look like?

- Am I really ready to leave the high tech world? Would I miss the fast work pace and the daily challenges?

So I have been doing some personal reflection on my “FIRE” future.

Like many early retirees, I probably would take 6 months or so to decompress.

Since this blog has been a big part of my life the last 9 years, I plan to continue to post new articles on this blog. Maybe spend more time and publish one or two more articles per month?

Maybe I can focus more time on photography and shoot more weddings and portraits?

But do I want to do a part time job? Do I look for a barista job? A cashier job at the local grocery store? Or something else? For me, I have never heard of “part-time” high tech jobs. Do they exist? Could I negotiate with my current employer to step back from full time to part time somehow?

I have no clue and this is something worthwhile to explore.

This past weekend, I had lunch with my cousin who retired when he was 42. I wanted to pick his brain about his FIRE life and the steps he took before he decided to retire.

It was so great to be able to talk openly about money and FIRE with a family member that I always looked up to. Some key points from our conversation:

- Busy FIRE life – kids, sports, hobbies, exercising, and cooking are some things that have been keeping my cousin busy after retirement. Boredom was not part of his post retirement life.

- Margin of safety – have enough cash reserve the first five years of early retirement so you don’t have to touch the principal. When asked, my cousin said they had about 1 year worth of cash saved up before he retired.

- Consistent income – generate a consistent income from your investments. This can be from either dividends, bonds, interests, or a mix of all three. Again, try to avoid touching the principal the first few years of the retirement to increase your margin of safety. When I ran our dividend income numbers and our living expenses, my cousin agreed that we’re getting pretty close.

- Cost of living – ensure living costs stay consistent. Avoid lifestyle inflation. An increase in living expenses means you need an even bigger retirement portfolio.

- Capital growth – Grow your investment. Although a consistent income is essential, total return is even more important. Withdrawals from the investment portfolio is a good idea, especially from a tax efficiency point of view. The key is being able to strategically time the withdrawals rather than being forced to withdraw when the market is down.

- Have backup plans – one backup plan is not sufficient, having multiple ones is the best. For example, keep up your resume if you need to go back to work.

For the most part, all these points are well known in the FIRE community but it was nice to hear directly from someone over a decade of us on the FIRE journey.

4. Holy mother ugly market!

Ok, not exactly about Taiwan but the North American stock market sure has been a mother ugly one! The value of our dividend portfolio has been stuck at the same range in the past year despite adding new capital. It can be tough to look at the portfolio value and not see the number getting bigger.

Our portfolio’s performance has been dragged down by Canadian banks, Canadian telecom, Enbridge, and TC Energy (well everything else too but these stocks in particular). I’m not concerned at all though. I think both Canadian banks and the telecoms are very solid. We plan to load up on more TD, National Bank, Royal Bank, Telus, and BCE early next year with the new TFSA contribution.

Enbridge and TC Energy are down quite a bit due to the recent acquisition and split news. Long term, I think both companies are positioned very well so I would not hesitate to add more shares.

REITs also have been taking a beating due to higher interest rates and worries with REITs not able to collect rents. Years ago, we used to own a higher percentage of REITs but we have slowly reduced our exposure to the REIT sector. Today, the REIT sector is less than 3.5% of our overall dividend portfolio. Granite REIT, VICI Properties, and SmartCentre REITs are the only REITs that we hold and I think all three should perform well long term.

Some investors might be concerned that their portfolio is down quite a bit. But that’s just the reality of investing in equities – the market goes up and the market goes down. The market can go up for a long time and the market can also go down for an extended time period.

As investors, it’s vital to remember to only invest with money that we don’t need in the short term. Think long term. Reducing your exposure to the stock market when you’re close to retirement or in retirement is a good idea. Utilizing safer investments like bonds, GICs, and term deposits is a good idea.

The nice thing with dividend investing is that even though the market is down, you can continue to collect dividends and not be forced to sell. Seeing dividends getting deposited in your account regularly can provide a big mental boost. I believe it also helps investors to think twice before selling any dividend stocks.

I feel that I’m repeating myself again and again but remember, time in the market is far more important than timing the market.

Let me repeat this again – one cannot possibly time the market effectively with 100% accuracy.

If someone tells you that they know when the market is bottoming or when the market is peaking and wants you to invest with them. RUN AWAY!!!

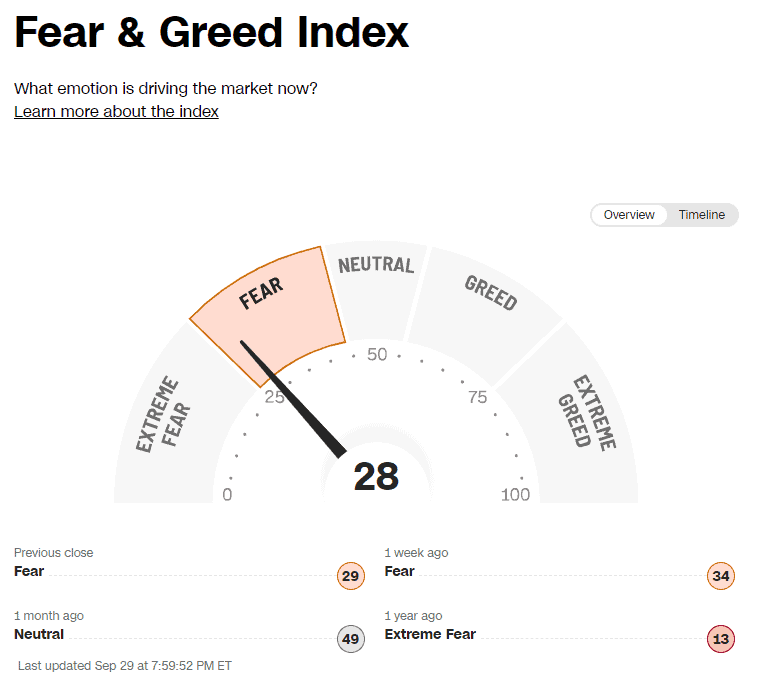

The fear and greed index has been trending down the last few weeks.

As Warren Buffett once said: “be fearful when others are greedy and greedy when others are fearful.”

Is it too soon to back up the truck and buy a massive amount of stocks for potential multi-bagger gains in the future?

I have no idea but what I know is that investors that continue to buy when the market is down and things are looking dire are usually rewarded in the long term.

5. Forget timing the market

Speaking of the market, I get a lot of questions about whether it makes sense to buy stocks now. When everything was firing on all cylinders, people were worried about buying at the peak of the market; now the market is in the red, people are worried that buying now means a further drop in the market.

Interestingly I came across a study by Charles Schwab the other day that helped answer a question on many investors’ minds – does market timing work?

Charles Schwab did research on the performance of five hypothetical long-term investors with very different investment strategies. In this research, each investor received $2,000 at the beginning of every year for the 20 years ending in 2022 investing in the S&P 500 Index and left the money in the stock market for the entire 20 year duration.

The 5 hypothetical investors took the following strategies:

- Peter Perfect: a perfect market timer and invests $2,000 every year at S&P 500’s lowest closing point.

- Ashley Action: invest the $2,000 on the first trading day of the year.

- Matthew Monthly: Divided the $2,000 equally and invested at the beginning of each month. This is known as the dollar cost average approach.

- Rosie Rotten: had extremely poor timing and always invested her $2,000 each year at the S&P 500’s peak.

- Larry Linger: an ultra conservative investor so Larry left his money in cash investments and never invested in the stock market.

As expected, Peter Perfect came out ahead. What’s most interesting is that Ashley came out in second with a difference of only $10,538 after 20 years, or 7.6% in total.

Rosie who has extremely poor timing came out $25,752 or 18.6% less than Peter but still way ahead of Larry by $68,344 or more than 50%.

When different time periods were considered, the rankings were very similar. Charles Schwab analyzed 78 rolling 20-year periods dating back to 1926. The rankings were identical 68 out of the 78 periods!

Interestingly, in the 10 periods where the rankings changed, investing immediately (Ashley) never came in last. According to the study, Ashley would finish second place four times, third place five times, and fourth place once. To repeat and reinforce, Ashley never came in last!

Since it is nearly impossible to time the market, the next best approach appears to be a lump sum approach and invest the money immediately.

This has been our approach for many years – I know I sleep better when we invest in a lump sum. But if you sleep better at night, spreading it out and dollar cost average works just as well.

Therefore, it is important to know yourself and invest according to what you’re comfortable with. It’s not worth it if you lose sleep over your investments.

Happy investing everyone!

“Unfortunately, due to company travel policy changes, I’m back to flying in economy class.”. IIRC, your employer was bought by a US corporation 1-2 years ago, so that kind of penny pinching was to be expected…

Regarding part-time work with a high tech job, if your boss appreciates you and has the power to do so, I can confirm that it is possible to negotiate something. I (software developper) worked 3 days a week for the last 3 months before retirement. A collegue did it for a whole year before he retired. With the learning curve required from your eventual successor and recruitment difficulties, a wise company would prefer having 60% of you than 0%.

Being FI or very close to it also gives you a negotiating advange for a potential part-time arrangment.

Good to know Alex that it’s indeed possible to work part time in high tech.

Part time tech work exists depending on the tech. I’ve been thinking of doing “brochureware” websites for small, local companies. I did a free one for a group that I volunteer for and they were blown away. I have no design skills, but I was able to make the functionality they wanted.

However, if your tech expertise is designing microchips… that may be difficult to find part-time.

It’s not surprising that Action Ashley never finished last, when one of the people doesn’t invest at all. That’s basically just testing if there’s a 20-year bear market. You’d have to look at Japan (and maybe some other countries) to find markets that have tanked for decades.

Hi Bob,

Where do you stand on AQN these days? At ~7.50 it’s taking a beating. Do you think it’ll come back in the long term? Or is this a symptom of a bigger underlying issue?

Take your money and invest it elsewhere. We all make mistakes sometimes.

Hi Bob . The two Air Canada YVR-Sydney, Australia flights I did this year are the same story : packed , all seats taken and just not comfortable for a 16 hour flight. Economy of course because I’m too cheap and too scared of flying business as I’d never go back to economy after.

Letting my cash collect 5% in money markets and waiting for better deals in RY, TD, BIPC in C$ and BRK.B in US$ corporate account. Hope not to buy too early as I usually do!!

YVR-Sydney 16 hour flight doesn’t sound very pleasant in economy. That’s probably when it’s worth it to splurge for premium economy or business. 🙂

When we did the Vancouver-Sydney flight in 2015 with Air Canada, we booked early (bought tickets in june 2014 for february 2015) and were able to select seats in the first row of the economy class, which were two seats wide on each side and had more leg space. That was a $120 dollar per seat per trip (total $480) supplement, but was entirely worth it, and less expensive than business class.

Great insights as usual Bob. Canadian markets might be in for a rough ride next year with mortgage renewal worries and untamed inflation but not trying to time the market so looking at it as a potential “sale on everything on the stock market”.

Do enjoy your time – and the local food – in Taiwan!

Thanks Olivier. Agree with you, there will be lots of buying opportunities.

My investing style is more like Mathew monthly I’m adding small amounts to a lot of my positions with each pay cheque. I would hate to double my position in Royal or any other blue chip stock because it looks like a good deal right now and lose 10% or more the following week. Also, the technicals of a lot of TSX stocks look brutal right now and no where near the bottom; not that I know where that is going to be. Do not plan on selling much equity in retirement as I have an employer pension with mortgage paid off… plan to keep most of dividend and ETF portfolio and pass onto kids. I might add some more cash or GICs and dilute it slightly when I get closer to retirement.

Do you plan on reducing your own equity exposure when you retire ?

Monthly investment makes sense. For us we do lump sum regularly so it’s kind of like DCA.

In terms of whether to reduce equity exposure when retired… probably to in some way but not too conservative like 60-40.

We got back from Taiwan after a 2+ week trip and miss the food terribly. Half the price for better tasting meals. As good as your business class meals look, I rather have the cheap meals in country.

I’m hovering closer to your 5 years of cash on hand for living expenses (maybe I’ll settle on 3 years) vs your cousin’s one year. Piece of mind is worth the trade off of lost opportunity cost for me.

Wow that’s a lot of cash saved up. But how much cash reserve needed will depend on your situation.

I would like to understand better how you invest in a lump sum?

For instance, do you invest your entire tfsa’s contribution room on January 1st for example? Do you also invest into your rrsps and taxable accounts at the beginning of each year? Or, do you accumulate a certain amount of money and then invest that lump sum at some point throughout the year? Thanks in advance!

Hi Angie,

For us we invest the entire TFSA’s contribution room on Jan 1st then try to buy stocks on the 1st or 2nd day of the year when the market opens. For RRSP, yes try to max out as early as possible and do lump sum contributions. Invest in lump sum in taxable accounts only when RRSP & TFSA are maxed out.

A few thoughts, in no particular order:

btw, i retired this year, after four years of part time work (in hi tech) and I am past 65 years old.

I only got into the Dividend plan in the last ten years, wish i had started that sooner. Fluctuations in price will always be there, but a steady income stream from solid boring companies lasts.

-Bob, what about Matthew Monthly? I put a part of every pay cheque into my investments every two weeks for 40 years. Now how to withdraw from rsp’s, tfsa’s, GICs etc and cash that I and my wife own? I am sure thats fodder for many blogs. So, as I saved, so will I draw down; i will take my (average) monthly dividends every month. Over time as the markets go up and down, it will all even out (i think/hope).

-When retiring; I found that we (and many of my retired co-workers) spend a LOT on travel the first year or two after retiring. Coming out of COVID exaggerated this a well. Six weeks in Europe comes with a price tag. Consider this when you are thinking of giving notice at your work/career.

-same for kids education. if you stop work while young, you will need to fund education as the family gets older. You get the idea. I burned through almost $100k the first 18 months (but had a bit of cash sitting for that, so not too much harm done i hope)

-investing losses early in my career, i got into the markets (before ETFs were invented) and on black friday in 1987 i lost 40% of what was supposed to be my house downpayment. Similarly the dot com in early 2000’s hit me; BUT, adding funds every pay day, and Fed lowering interest rates and printing money, markets gained it all back, usually in 24-36 months. 2007 was very bad, but came out of that in good shape as well. I saw all the inflation of the late 70s and early ’80s. I have no good feeling our current situation will get better anytime soon.

-We know Dividends are taxable. So plan your withdrawals with after tax net income in mind. $60k is a fairly low tax bracket, but every time I take money out of my RSP Ottaws gets 20%. That hurts. (but i cannot complain, i got the write down every year for rrsp contribution).

-Finally totally agree on timing markets. Do we live to work , or work to live? Not everyone enjoys watching markets and dividends as a hobby. Use the “Wealthy Barber” rules, work hard, and enjoy your successes (big and small) along the way

Hi Gordon,

Great points! Yes, we most likely will need more in the first few years if we do travel. However, travelling doesn’t always mean more expenses as some countries can be cheaper than Vancouver (for example, South East Asian).

In terms of withdrawals… I wouldn’t necessarily withdrawal every month. The plan is to withdrawal a large amount semi-regularly to minimize any transactional cost.

As the second year anniversary approaches for my entrance into the stock market, I agree it has been very challenging. The hit I took with split stocks (Ponzi stocks in my mind) cost me -3.6% on my total portfolio at the time. Reinvestment’s have recovered much of that with dividends. However, this mornings market (TSX) is now down 9.4% from mid-April. I am down -3.7% from my original investment. Learning curve has been expensive! Still, I would do it all over again as I am making better judgements(hopefully) and stricter criteria. Thanks Bob for your contribution. Going forward, at least $5000/month of dividends and sale of stocks will go into 5.6% 1 year GICs providing monthly returns. This allows the option of cashing in the GIC if needed, or reinvesting. As I have always been the “chief financial officer” for my husband and I, this will make it easier for him to manage should I be unable to. The future stock market does not look particularly good, IMHO.

Hi Dianne,

Therefore it’s important to make sure to have a mix of stocks and “safer” investments like bonds and GICs.

The stock market is the only market in the world where people run away from specials.

Haha so true.

Hi Bob

Super article. Although your focus is on investing and all things financial, reading about your travel experience is interesting.

Thank you, Kevin.

Hi Bob,

Thank you for the excellent article. Your mention of continuing to write even after retirement that is truly valued. Your perspective is invaluable to the community, both now and especially in the future when you retire

Quick question, (you might have the answer in another article), your goal of $60K/year in dividends, is that after of before tax? Say, you are already generating $60K/year in dividends from an RRSP account ONLY, (actually that is is my case) would that be sufficient ? I mean, I wish I had that in my TFSA account, but I only have money in my RRSP account.

Thank you again!

Thank you Lanny, I appreciate it.

$60k is before tax. Per our calculation, our taxes should be minimum as we use RRSPs, TFSAs, and taxable accounts.

See calculation here – https://tawcan.com/do-we-have-enough-to-live-off-dividends-a-case-study/

Lenny, depending on your current TFSA room, it makes sense to open a TFSA account and transfer some of the RRSP investments over -gradually- bearing in mind there will be a tax cost on RRSP withdrawal. In the long term, future tax savings most likely would be worth the short term pain. Or consider stopping some of the RRSP contributions and place the money into your TFSA. A lot will depend on your projected tax rate in retirement and how much pension income you will receive.