I’ve always thought it’s super cool to be born on Feb 29th. How cool would it be to tell people that you’re 5 years old but in reality you’re 20? (Yes I’m weird this way. :p) I didn’t tell Mrs. T but I was secretly hoping that Baby T2.0 would be born yesterday. That didn’t happen so Mrs. T and I were able to spend quality time together after Baby T1.0 went to bed. Since Baby T2.0 is full term already, we’re just playing the waiting game. Mrs. T and I are certainly trying to enjoy the last few days of quiet times. We don’t know what having two kids would be like but we’re both very excited. Given that we have some experience with having a little baby already, we believe things will be easier this time around. 🙂

Anyway, let’s get back to the topic of the post shall we? For those of you that are new to this site, each month I provide an update on our dividend income and our dividend growth. We love dividend income because it’s money that we receive for doing absolutely nothing as all. We can be running around after Baby T1.0 and changing diapers for Baby T2.0 while our money is working hard for us, generating more money. Who doesn’t like that?

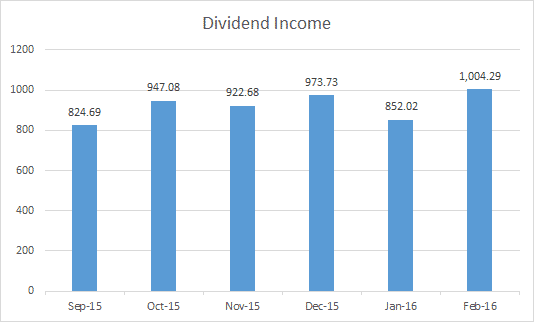

Dividend Income

In February, we received dividend from the following companies:

Apple (AAPL)

Pure Industrial REIT (AAR.UN)

Bank of Montreal (BMO.TO)

Corus Entertainment (CJR.B)

Dream Office REIT (D.UN)

Dream Global REIT (DRG.UN)

EnergyPlus Corp (ERF.TO)

General Mills (GIS)

H&R REIT (HR.UN)

Inter Pipeline (IPL.TO)

KEG Income Trust (KEG.UN)

Kinder Morgan (KMI)

Liquor Store (LIQ.TO)

National Bank (NA.TO)

Omega Healthcare (OHI)

Procter & Gamble (PG)

Potash (POT.TO)

RioCan REIT (REI.UN)

Royal Bank (RY.TO)

AT&T (T)

Vodafone (VOD)

Verizon (VZ)

We received a total of $1,004.29 in dividend income from 22 companies. Of the $1,004.29 received, $294.05 was in US dollar and $710.24 was in Canadian dollar. Please note, we use a 1 to 1 currency rate approach, so we do not convert the dividends received in US dollar into Canadian currency. Reason for doing this is to keep the math simple and avoid fluctuations in dividend income over time due to changes in the exchange rate.

OH MY GOD!!! This is the first time ever that we crossed the $1,000 dividend income in a month milestone! (I don’t consider March 2014 because we received special dividends) I’m thrilled to see that we finally crossed this special & key dividend milestone. Considering the recent dividend cuts in stocks like Kinder Morgan and Potash, I was worried that our February monthly dividend income would take a big hit. Fortunately the combination of new purchases and organic dividend growth in other stocks helped pushing our February dividend income over the $1,000 mark by just a few dollars. Phew!

Dividend Growth

Compared to February 2015, we saw a YOY growth of 15.75%. Pretty solid but we’d love to see that number to be closer to 20. For those of you that are new, our dividend growth is contributed by three things – investing fresh capital, purchasing of additional shares through dividend reinvesting plan (DRIP), and increasing of individual stock’s organic dividend payout each year. We see DRIP as a very effective way to utilize the power of compound interest. I’m extremely pleased to see that enrolling in DRIP has allowed us to purchase additional 12 shares of dividend paying stocks this month. The 12 new shares will increase our annual dividend income by $30.31.

$30.31 more in annual dividend income? What’s the big deal? That’s such a small amount, you may have thought.

Think again! Given a conservative 3% dividend yield, it would take $1,010.33 to generate this amount. What does this mean? It means we didn’t have to save $1,000 and invest it in dividend stocks because we took advantage of DRIP. It also means that the $1,000 that we set aside in the future can be used to buy more dividend stocks and generate more dividend income. Essentially we can generate double in dividend income for half the dollar amount invested. That’s the type of leverage I would use any given day.

Although we have seen some dividend cuts and freezes in some of our holdings, a number of stocks have increased their dividend payouts in February as well. This include BCE Inc, Manulife Financial, TransCanada Corp, Coca-Cola, Wal-Mart, Enbridge, Royal Bank, TD, CIBC, Magna International, and Waste Management. That’s 11 companies that have increased dividend payout in month of February! Wow! That’s fantastic! The largest 3 increases are Enbridge at 13.98%, Magna International at 13.64%, and Manulife at 8.82%. As owner of these dividend stocks, I’m ecstatic to see these increases.

[the_ad id=”1878″]

Moving Forward

So far in 2016 we have received a total of $1,856.31 in dividend income. We’ve already added around $19,000 into our dividend portfolio this year but there is a lot more work to do in order to reach the $13,000 annual dividend income goal. We plan to sell a few stocks that have cut their dividends and use the money to purchase other dividend stocks. We also have some money set aside ready to purchase more dividend stocks. Now that the RRSP 2015 contribution deadline is over, we can start contributing money into our RRSP toward the 2016 tax season. We hope the market will continue to be volatile so we can purchase stocks at a discounted price.

Dear readers, how was your Feb dividend income?

Hey Bob, just came across your site and am enjoying your articles. I think we’ve met before sometime as I recognize your picture but I can’t put my finger on it!

Just curious, do you ever share the total value of your portfolio, or the ROI on your dividends? I’d like to learn about that.

Thanks very much.

Hi Chris,

No I don’t think we’ve met before but maybe I am wrong. I don’t share total value of our portfolio and ROI as want to keep that info private. We are sharing a lot of financial numbers on this site already, so want to keep some stuff confidential.

Hello Tawcan,

I ‘ve been following your story from the side lines so I will share my story… My wife and I have been living in Amsterdam almost 4 yrs since leaving Calgary in 2012. I am a non-resident for tax purposes paying my income tax in the Netherlands. I still file taxes in Canada because I am taxed 25% on any net rental income (house is rented at arms length). I also submit my 15% tax on my non-reg dividends to the CRA. Since 2012, I do NOT contribute to my RRSP or TFSA as I am no longer allowed to contribute as a non-resident. In Canada, I only invest my net rental income and dividends back into the market via my TDwaterhouse account (primarily div paying stocks like Banks, T, BCE, TRP, VAB). I have a couch potato RRSP portfolio I re-balance occasionally.

My savings (I get paid in Euros) here in NL stay in Europe and are invested 100% in Vanguard VHYL using my TD Waterhouse account in Luxemburg. That fund is paying about 3.8% divs. I current re-invest those funds too. I have just over 2 yrs to run on this contract. By mid-2018 I should have about $1.4MM Can in reg and non-reg savings split about 1/2 in Canada and 1/2 in Europe (Euros). I paid my house off 2 yrs ago. So I am hoping to switch to part-time work in 2018. Living part time in Canada and part time in Europe. By then I will be 47 yrs old 🙂

Hope that makes sense? Its a bit of a complex story.

Keep up the great saving and inspirational blogging.

Mark.

Hi Mark,

Thank you very much for the kind words. Interesting that you are doing non-resident approach. Considering that we plan to travel around the world in the future, that’s an approach we might have to look into. Did you consult with a tax expert before you moved to Amsterdam? Love that you’re getting paid in Euros and have assets in Canadian. That’s hedging in my books and you’re certainly protecting yourself from currency fluctuation. Living part time in Canada and living part time in Europe sounds like a great idea! Do you have a PR status for EU? Or are you an EU citizen somehow?

Tawcan,

Congrats on the new addition to the family, hope everyone is doing well. To follow up, I have both Canadian and UK (by birth) passports. So I am here on my UK passport. However, as a Canadian you could get a working visa in NL with no issues. I did get some specialist advice before I left, though I got slightly different advice from different sources. But we are tying to be as compliant as possible. I don’t add to my RRSP or TFSA’s to avoid going offside. Also, I have not sold anything in my non-reg accounts since leaving in 2012, only buying. I pay tax on my Can divs each year. I am also very transparent with my rental income to the CRA. So hopefully we have no issues when we return. I sent quite a bit of money to Canada in the first 18 months to pay off the LOC on the Calgary house. Now I dont send anything back as I dont really need the cash there and I just invest the net income from the house into Can div stocks.

Keep up the great work and growing the income!

Any thoughts on the Vancouver housing market? Its going the opposite way from Calgary!

Mark.

Hi Mark,

Thanks, always appreciate you dropping by and leaving a comment. I’ll have to look into getting a working visa in Denmark since Mrs. T and our kids have Danish passport to allow them staying there. Makes sense that you’re not adding to your RRSP And TFSA. Not selling anything in non-reg accounts make sense too. I think the key is to be as transparent as possible to avoid CRA audit.

Vancouver housing market is just nuts. I think it’ll continue climbing for a while.

Hey Tawcan,

Do you consider dividend income both in registered and non-registered (RRSP and TFSA) accounts?

I am about $1000/Mo in non-reg, but I receive about ~$5000/yr of income in my RRSP account. I dont really think about this as “income” because it is auto invested to buy more of the same (low cost) e-series funds. My non-reg divs build up, when they get to about $1000 I just manually buy more of what seems “on sale” Great work on the income! Mark (Canadian in Amsterdam)

Hi Mark,

Right now we consider dividend income from RRSP, TFSA, and no-reg. All the dividends are reinvested fully. We’re working to build up our non-reg dividend income. Are you permanently in Amsterdam? How does that work when it comes to taxes and such? Would love to get more info from you.

TAWCAN!!!!

YOU DID IT!!! YES! YES! YES! YES! 4 digit figures WOW!!! In February too, YES! Congratulations, well deserved, hard working, much research and passion went into this. You are killing it! this is awesome, HUGE HUGE HUGE! Keep it up and congrats on the newborn!!!!

-Lanny

Hi Lanny,

Thanks, you are just excited as me with this major milestone. 😀

Congrats on hitting $1,000 in dividends! That’s awesome. That would cover my expenses a lot of months! Also congrats on the new baby!

Wow Tawcan! That is really a great dividend income! I hope you reach the $13,000 annual dividend income goal. I know you can! Good luck Tawcan.

Congrats on passing the 1k$ milestone, thats an awesome job. Looks like the market panic has subsided so hopefully things return back to normal for the next little while. Best T

Hi talefromthetape,

Thanks. Hoping the market will drop a bit more so we can continue buying things on a slight discount!

Hey Tawcan, that’s great! $1,000 in a month is HUGE, you could retire in lots of countries for that amount. Your growth is very inspiring to us just starting out. Lots of diverse dividends as well. Good luck for the rest of your year, should be a great one.

Tristan

Hi Tristan,

You’re so right, that amount of money is sufficient in many countries that have lower cost of living. 🙂

18K is HUGE, congrats!

Did baby T1.0 have big brother class? heheh… going from the center of the world to having to share your attention can be hard.

Hi Vivianne,

We hope to continue adding more cash to purchase more dividend stocks.

Nope Baby T1.0 has not taken big brother class but we’ve been reading a lot of books about being a big brother.

Killer job there Tawcan, 1k in divi income in a month is fantastic! That’s more than my current annual dividend income 😛

Keep it up, you’re a great inspiration my man.

Cheers

Thanks Zero to Zeros. It takes time to build up this kind of dividend income. You’ll get there in the very near future too.

Congrats on hitting a cool grand in monthly income. It’s a great milestone to say the least. I’m hoping to be just a few years behind you in that regard. Onward and upward.

Hi Chris,

Thank you, onward and upward for sure. 🙂

Hi Tawcan, just FYI, you could have started making your 2016 RSP contributions on January 1. You would need to declare the contributions made in the first 60 days of 2016 on your 2015 taxes and carry over the deduction to 2016 (or later). Every bit of compounding helps! 🙂

Hi jd,

Good point, I knew about that but have always used the first 60 days of RRSP contribution toward previous year’s taxes. Perhaps I need to complete my contribution in the given year and use the first 60 days toward the next year moving forward.

Tawcan,

Almost 16% YOY growth, great job there thumbs up! But once you hit FIRE, the DRIP aspect will be turned off and fresh capital will decrease and maybe off too, what is your expected organic growth once you guys reach FIRE?

Congratulations on a record breaking solid month!

FFF

Hi FFF,

Thanks! Very true that we’ll probably turn DRIP off once we hit FIRE and the fresh capital will probably decrease. Given we have a mix of high yield and high growth dividend stocks, an organic growth of 5% is in line with my expectation.

Congrats Tawcan. $1,000 in a single month is an amazing milestone. February is traditionally a slower dividend month. Do you anticipate crushing $1,000 again in March?

Hi Investment Hunting,

Thanks. I think we should be close to $1,000 again in March but I guess we’ll have to wait and see.

I’m hoping for $800 + in March. I really hope you hit $1,000

Tawcan

WWWOOOwww, way to go, great milestone – 4 digit of dividend income – hope that I will get there one day – maybe after India I will make it 🙂

Sharon – Divorcedff

Wow! This is so inspiring, especially for someone who is just getting started with investing. Congrats on the milestone. Thanks for sharing the dividend income report.

Amazing!! Congrats, Tawcan. Thats a fantastic milestone to reach. Must feel special to get there … ive been dreaming about getting there for a while now and hope to reach it in the next couple of years.

Up, up and away….keep on compounding that income.

Best wishes

R2R

First, congrats on the 2nd child (any day now) we have a girl (4) and a boy (1) and my day is not complete without sitting in the floor and playing with those rascals…I absolutely love being a dad!

Secondly, a big congrats for crossing over the $1,000 mark in one month, that is awesome…who wouldn’t want to receive that kind of cash for doing nothing!

Third, thanks for stopping by and commenting on my last post. I only received $29.78 in dividends this month…but you know what? It’s $29.78 more than last February.

Keep up the good work!

Hi Our Dime Our Time,

It’s great being a dad. 🙂

Keep that dividend income coming!

Tawcan,

Congrats on the milestone! The portfolio is looking great and rolling forward. Keep at it and keep investing in great dividend growth stocks!

-Dividend Monster

Hi Dividend Monster,

Thank you!

Congrats on reaching a new milestone! $1,000 per month in dividends is just insane. A minimum wage worker doesn’t earn that in 2 weeks. Keep up the good work!

Hi German,

Thanks! That’s a great way to look at how powerful dividend income is. It saves us 2 weeks of “minimum wage” work.

Great milestone to cross: your first 1k. Keep the snowball rolling!

Going from one baby to two baby’s is a great event. The first few weeks you need to find a new routine. It will be fun!

Hi ambertreeleaves,

Thanks, definitely keeping that snowball rolling and making it bigger and bigger. We’re looking forward to finding a new routine that’s for sure.

Congrats on hitting the $1k/month milestone, this is one of my long-term goals too.

Some parents I recently spoke to were worried about giving birth on February 29th because it’s so weird for children when they’re young.

Hi Dividends Are Coming,

Thanks. I can see that having a Feb 29 birthday is weird for young kids. I just think it’s super cool. 🙂

Baby T2 and baby DivHut might have the same b-day. Well see. I can’t believe it’s almost one year since I became a father. Really, where does the time go? Awesome results and congrats on reaching a new milestone for a monthly divvy income. Reaching the $1k/month mark is my next long term goal. Happy to see some great names in common and of course those Canadian banks continuing to pay and raise their dividends in 2016 despite a crappy economic environment. Thanks for sharing.

Hi Keith,

Time flies eh? It’s hard to believe it’s already March and Baby T2.0 is about to born. It’s not long ago that we found out that Mrs. T is pregnant. I guess the next milestone for us would be 1.5K per month. That will require a bit of work for sure.

Great news that you guys have managed to achieve the $1000 a month dividend milestone. Congrats! May there be many more to come.

Hope that you may welcome baby T2.0 very soon.

Hi Team CF,

Thanks! It’s awesome to receive over $1K for doing no work. Gotta love that.

Congrats on the G note Tawcan. You 2 are doing wonderful. Keep up the great work and never stop. Congrats on baby t2 anyday now. It’s gonna be a new wonderful chapter so take care and have fun.

Hi Tyler,

Thanks. It will be a wonderful chapter of life to have two kids. 🙂

Hi TawCan

Congaats on the 1k milestone. I know you probably posted this in one of your posts but what broker do you use? Questrade or with the big banks?

Hi JT,

Thanks. We use Questrade and TD Waterhouse.

Congrats on receiving over 1000$ in dividend. That is an amazing feat. Wow! And I wish you well with the arrival of your second child. It will be a blast!

Hi Monsieur Dividende,

Thanks! Very happy that we finally crossed this milestone. Having another kid will be another great milestone in life.

Congrats on crossing the $1k threshold. That has to be a great feeling. Looks like you have a very diversified portfolio. Interesting that you stuck with KMI. I did as well, largely because I like why management had to cut the dividend (going out and buying depressed assets). I have found that most dividend investors have a pretty hard and fast rule of removing companies that cut their dividend from their portfolio. Is that something you considered? Sorry if you’ve already discussed.

Good luck with the new one. Our first just turned 6 months, I’m sure 2 will be a handful for the first 6-9 months.

Hi Nick,

Thanks. We decided to stick with KMI because we think it’s still a great company. I don’t like to sell just because a company reduces its dividend payout.

We think the same. It will be nice when they increase their dividends again in a few years AND the price comes back as well 🙂

Just my take!

I think KMI was increasing dividends too aggressively and simply got caught. The same thing happened with Potash to some extend. I think both KMI and POT will increase their dividends again in a few years.

I agree with others. Making > $1,000 per month on average is huge. That’s money you’ll NEVER need to work for again. Well done 🙂

Mark

Thanks Mar. 🙂

Great to see those dividends grow, quarter by quarter. Keep monitoring the income and your YOC which I’m sure is also growing slowly.

Our Feb income was $6,876.63, Jan was double that.

Wow cannew, that’s a crazy amount of dividend income for doing absolutely nothing at all. We hope to get to that point one day. 🙂

Hey Tawcan!

Too bad you didn’t get that leap year baby you wanted, haha. Congrats on receiving over $1, 000 for the first time in one month! I just surpassed $100 for the first time last month. Good use of the DRIP. An extra $30 in annual dividend income by having your portfolio on auto-pilot is really sweet. Compounding at it’s finest over here, keep it up.

DB

Hi Dividend Beginner,

Apparently Leapers miss out on some deals because companies don’t recognize Feb 29 as a “real day.” I’m sure you’ll surpass the $1,000 soon yourself.