We got serious with dividend growth investing after our financial epiphany in 2011. Since then, we have maxed out our TFSAs and RRSPs, and invested in our non-registered accounts with extra new cash every year.

In the last few years, we were very fortunate to be able to invest a lot more new cash into our dividend portfolio than in the earlier years. For that, we have to say thanks to our relatively high savings rate and increasing our household income.

After building our dividend portfolio for 12 years, I thought it’d be an interesting exercise to reflect on the past 12 years and run some projections on what it might look like in the next 10 years.

In case you’re curious, this post was inspired by Lanny’s post over at Dividend Diplomats.

Looking back on 12 years of dividend income

It’s hard to believe that we’ve been building our dividend income for 12 years. Time sure flies when you’re having fun.

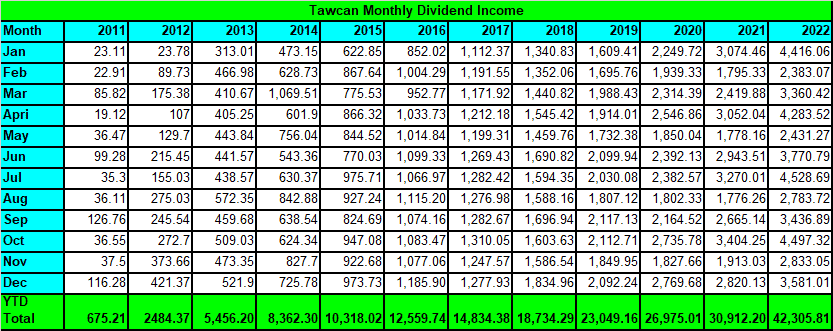

Despite the chart below, we actually started investing in dividend-paying stocks in 2007 but didn’t get serious with dividend growth investing until 2011. The dividend income between 2007 and 2010 was quite dismal.

- 2007: $54

- 2008: $155

- 2009: $154

- 2010: $329.79

When we start moving available cash from mutual funds, GICs, and other savings, our dividend income really started to take off. This was evidently from the jumps in 2011, 2012, and 2013.

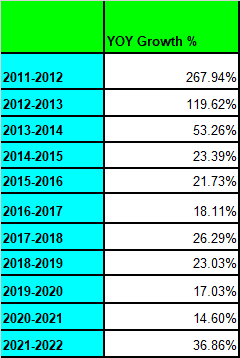

But we hit a dividend income growth snag in 2017 – we started to encounter the law of the big numbers.

What does that mean exactly?

Imagine that you received $200 in dividend income last year. To double your dividend income from $200 to $400 this year, or a 100% year-over-year (YoY) growth, at a 4% dividend yield, that means you have to invest at least $5,000. For many people, saving and investing $5,000 a year or $416.67 a month is a doable task.

Imagine that you received $2,000 in dividend income last year. Doubling your dividend income this year, at a 4% dividend yield, means you have to invest at least $50,000 in a year. This is a large sum of money and may not be possible for some people.

Now imagine that you received $30,000 in dividend income last year. To double your dividend income this year, at a 4% dividend yield means you need to invest at least $750,000 this year ($30k divided by 4%). Unless you make millions of dollars each year, this is simply not possible for the overwhelming majority of the population. Even if you aim to increase the dividend income by 10% YoY (an increase of $3,000), it would require saving and investing at least $75,000. Again, not an easy task.

Therefore, unless you earn millions of dollars each year, building up a sizable dividend income will take both time and patience. You can’t just eat ramen noodles all year and put 99% of your income toward buying dividend stocks. That’s not how the world works.

As you can see, we grew our dividend income relatively quickly in the first few years of our financial independence journey. We then kind of hit a snag in 2017, mostly because my working salary was flat that year. In 2018 and 2019 we grew our dividend income above 20% thanks to salary raises and our ability to put most of that toward investing.

Our dividend income then hit another snag in 2020 and 2021. The slower YoY growths in these two years were caused by the dividend cuts that we encountered (the COVID-19 global pandemic had a lot to do with these cuts).

We saw significant dividend income growth last year. This had to do with injecting a lot of new cash from 2020 and companies like the Canadian banks finally raising dividends at higher than usual rates. It is extremely unlikely that we will see another +30% YoY moving forward.

Looking back on 12 years of dividend growth investing we need to contribute our success so far to the following key factors:

- Our relatively high savings rate

- Investing money regularly in TFSAs, RRSPs, and non-registered accounts

- Stay consistent with our investing strategy

- Ignoring noises

- Thinking like an owner – owning appreciating assets

Investing doesn’t have to be complicated. In fact, the more complicated the investing strategy is, the easier for someone to give up on that strategy, instead of continuing with the same investing strategy for decades.

Looking forward 10 years – Financial independence

There’s no doubt in my mind that we will be financially independent sometime in the next 10 years. The question is really when we’d reach this point. Fortunately, we aren’t in a rush to get to that so-called finish line. We want to enjoy our lives and live in the present moment.

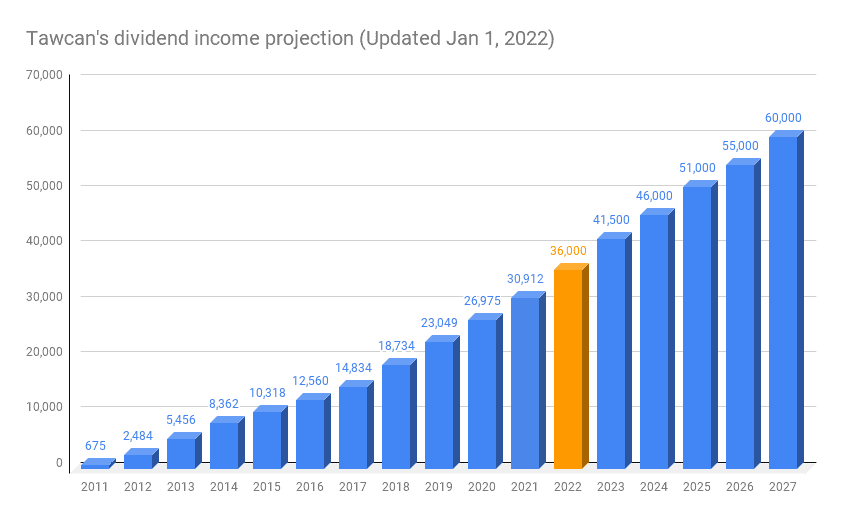

Per my dividend income projection from early January 2022, I estimated that we’d finish the year with around $36,000 in dividends. But I was completely off with this projection.

We ended the year with $42,305.81, $6,305.81 above the projection, or out by 17.5%. It was great to exceed the projected income and receive more dividend income than what I projected for 2023. But it also made me realize that I need to be more pragmatic with our dividend income projection.

But how can I be more realistic and sensible with our dividend income projection?

For those readers that are new, we’ve been growing our dividend income with these key three factors:

- New capital & reinvest of 100% of dividends received

- DRIP’s

- Organic dividend growth

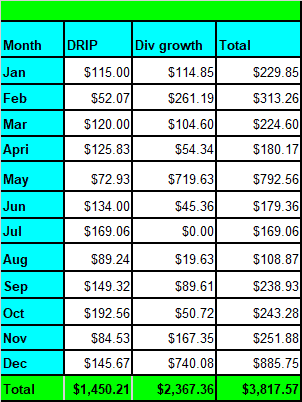

By enrolling in DRIP’s and companies increasing dividends (i.e. organic dividend growth), we have been able to grow our forward annual dividend income by $3,817.57 in 2022. At a 4% dividend yield, we would have to invest $95,439.25 to get the same amount.

Since this dividend growth didn’t come at the beginning of the year, the actual impact on our 2022 dividend income was a lot less than $3,817.57. I’d estimate that we increased our 2022 dividend income by around $2,500 due to DRIP and organic dividend growth.

We started 2022 with a dividend projection of around $34,000. Adding the $2,500 increase from DRIP’s and organic dividend growth, meant about $5,800 worth of dividend income increase from the contribution of new capital. At a 4% dividend yield, that would mean we had to add around $145,000 worth of capital in 2022.

Please note, all these numbers are estimates. We actually didn’t contribute nearly as much as $145k last year; nowhere close, in fact.

So what would our dividend income projection look like for the next 10 years? I decided to run a few different scenarios.

Before starting here are a few parameters I used:

- I will assume DRIP’s and organic dividend growth will add about $2,500 to our 2023 dividend income.

- Assume that the companies that we currently hold will maintain similar dividend growth rates.

- I took AQN’s 40% dividend cut into the calculation. For now, we have no plan to sell any AQN shares. We will drip additional shares each quarter and lower our cost basis. The plan is to reevaluate AQN in two or three months.

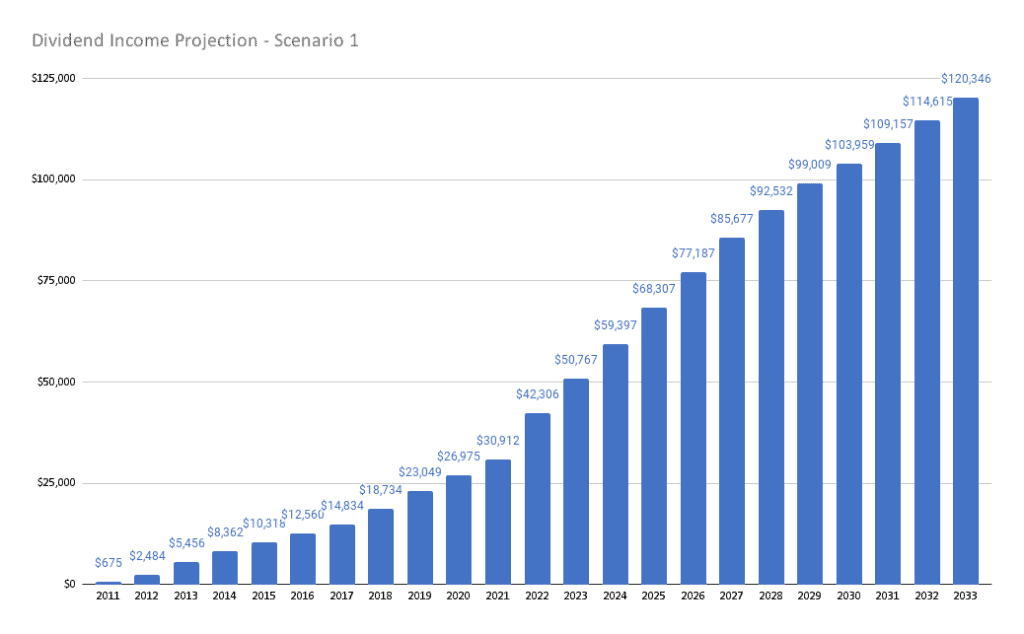

Scenario 1 – aggressive dividend growth

Scenario 1 assumes we can continue with the aggressive dividend growth for the next few years and slow down once we are living off dividends, or Dividend FIRE as Wonderer called it on Millennial Revolution.

| Year | Dividends | YoY % | Portfolio value (4%) | Contribution (at 4% yield) |

| 2023 | $50,767 | 20% | $1,269,174 | $211,529 |

| 2024 | $59,397 | 17% | $1,484,934 | $215,760 |

| 2025 | $68,307 | 15% | $1,707,674 | $222,740 |

| 2026 | $77,187 | 13% | $1,929,672 | $221,998 |

| 2027 | $85,677 | 11% | $2,141,936 | $212,264 |

| 2028 | $92,532 | 8% | $2,313,290 | $171,355 |

| 2029 | $99,009 | 7% | $2,475,221 | $161,930 |

| 2030 | $103,959 | 5% | $2,598,982 | $123,761 |

| 2031 | $109,157 | 5% | $2,728,931 | $129,949 |

| 2032 | $114,615 | 5% | $2,865,377 | $136,447 |

| 2033 | $120,346 | 5% | $3,008,646 | $143,269 |

A YoY growth of 20% in 2023, 17% in 2024, 15% in 2025, and 13% in 2026 all seem quite aggressive to me, especially when we look at the contribution dollar amount required.

Don’t get me wrong. It would be awesome to have over $68,000 in dividend income by 2025, the year we target to be financially independent. But I think this scenario is simply too aggressive and unrealistic.

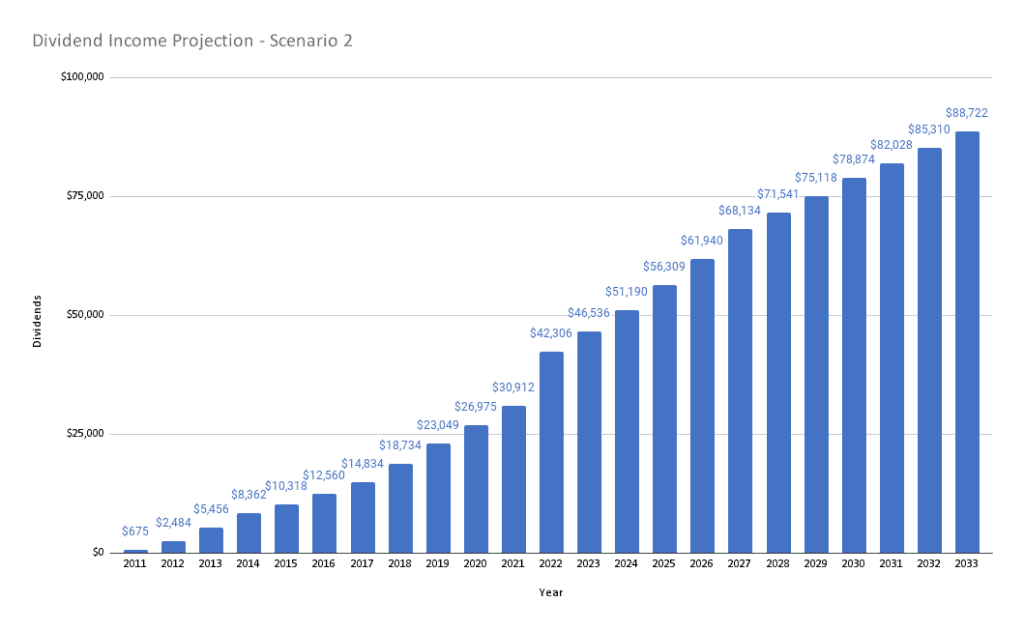

Scenario 2 – foot off the pedal

What if we went the opposite direction from scenario 1 and took our foot off the pedal starting this year?

| Year | Dividends | YoY % | Portfolio value (4%) | Contribution (at 4% yield) |

| 2023 | $46,536 | 10% | $1,163,410 | $105,765 |

| 2024 | $51,190 | 10% | $1,279,751 | $116,341 |

| 2025 | $56,309 | 10% | $1,407,726 | $127,975 |

| 2026 | $61,940 | 10% | $1,548,498 | $140,773 |

| 2027 | $68,134 | 10% | $1,703,348 | $154,850 |

| 2028 | $71,541 | 5% | $1,788,516 | $85,167 |

| 2029 | $75,118 | 5% | $1,877,941 | $89,426 |

| 2030 | $78,874 | 5% | $1,971,839 | $93,897 |

| 2031 | $82,028 | 4% | $2,050,712 | $78,874 |

| 2032 | $85,310 | 4% | $2,132,741 | $82,028 |

| 2033 | $88,722 | 4% | $2,218,050 | $85,310 |

In this scenario, I assumed we’d grow our dividend income by 10% over the next 5 years before slowing down to 5% starting in 2028 and then 4% in 2031. If we look at the contribution amounts required, we are still talking about a sizable amount each year.

However, given that I plan to continue working full time and Mrs. T plans to continue working on her doula services in the next few years, I believe we can continue to save and invest a large amount of capital each year. So the 10% YoY growth may be slightly on the low side.

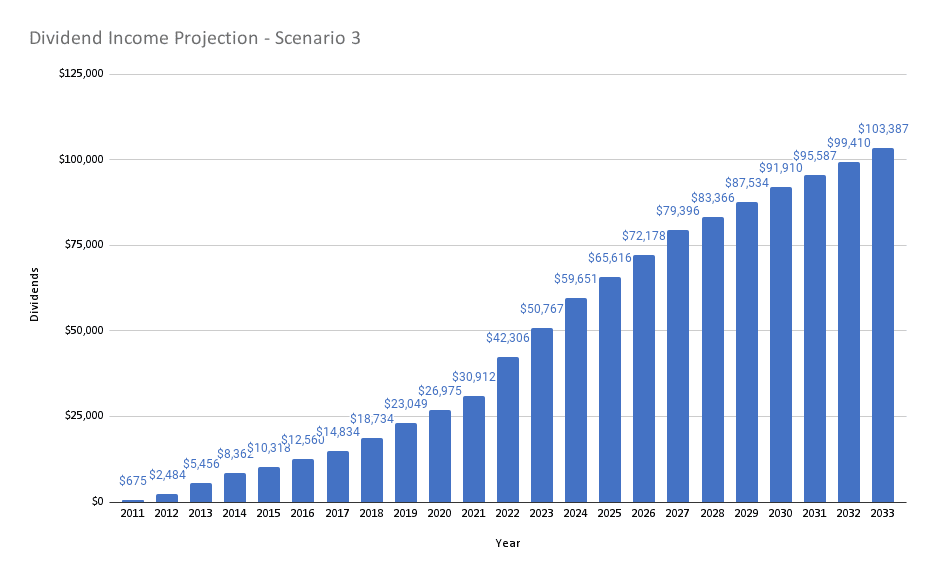

Scenario 3 – more realistic approach

For scenario 3 I took a middle-of-the-road approach and assumed we’d be able to continue to grow our dividend income by a decent percentage in the next couple of years before slowly reducing that growth.

| Year | Dividends | YoY % | Portfolio value (4%) | Contribution (at 4% yield) |

| 2023 | $50,767 | 20% | $1,269,174 | $211,529 |

| 2024 | $59,651 | 18% | $1,491,280 | $222,106 |

| 2025 | $65,616 | 10% | $1,640,408 | $149,128 |

| 2026 | $72,178 | 10% | $1,804,449 | $164,041 |

| 2027 | $79,396 | 10% | $1,984,893 | $180,445 |

| 2028 | $83,366 | 5% | $2,084,138 | $99,245 |

| 2029 | $87,534 | 5% | $2,188,345 | $104,207 |

| 2030 | $91,910 | 5% | $2,297,762 | $109,417 |

| 2031 | $95,587 | 4% | $2,389,673 | $91,910 |

| 2032 | $99,410 | 4% | $2,485,260 | $95,587 |

| 2033 | $103,387 | 4% | $2,584,670 | $99,410 |

This scenario is more realistic than scenario 1. Growing dividend income by 20% this year should be achievable if we continue with our investing strategy outlined above.

One of the questions we need to figure out is whether to continue to hold AQN or if we’d start trimming the position and re-invest the money elsewhere later in 2023. I believe AQN’s management made the right decision with the dividend cut. This will improve the company’s balance sheet. But revising the guidance to a lower level is quite concerning, especially when AQN lowered its guidance not too long ago.

As mentioned, we plan to re-evaluate AQN next quarter and make a decision.

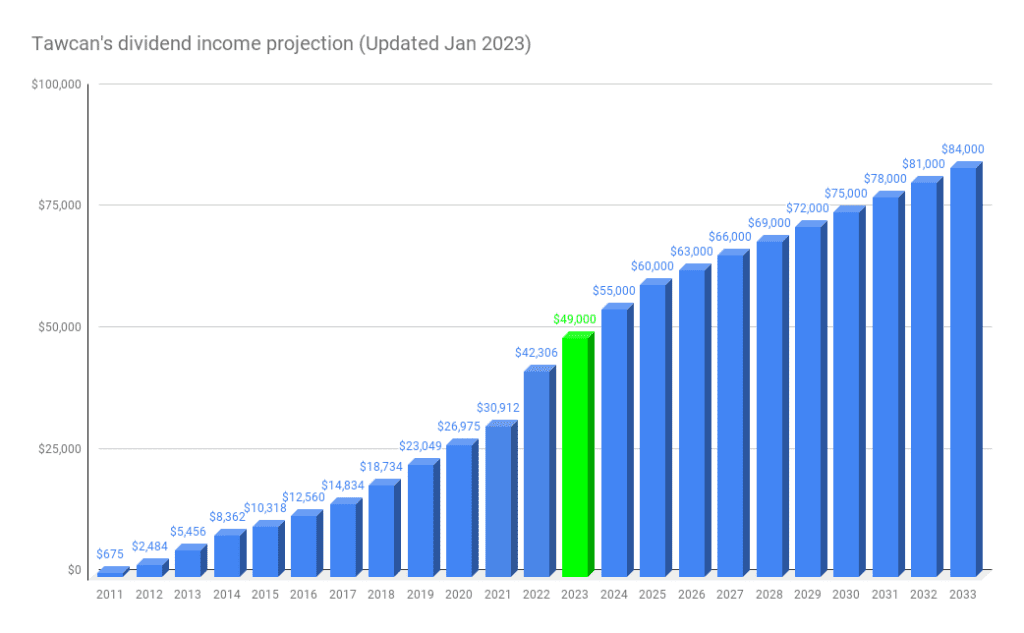

Finalizing our dividend income projection

In addition to the three scenarios above, I ran a few more scenarios and played around with the YoY growth rates for the next 10 years. After a lot of adjustments and refinements and all the information available, below is our finalized dividend income projection:

| Year | Dividends | YoY % | Portfolio value (4%) | Contribution (at 4% yield) |

| 2023 | $49,000 | 15.82% | $1,225,000 | $167,355 |

| 2024 | $55,000 | 12.24% | $1,375,000 | $150,000 |

| 2025 | $60,000 | 9.09% | $1,500,000 | $125,000 |

| 2026 | $63,000 | 5.00% | $1,575,000 | $75,000 |

| 2027 | $66,000 | 4.76% | $1,650,000 | $75,000 |

| 2028 | $69,000 | 4.55% | $1,725,000 | $75,000 |

| 2029 | $72,000 | 4.35% | $1,800,000 | $75,000 |

| 2030 | $75,000 | 4.17% | $1,875,000 | $75,000 |

| 2031 | $78,000 | 4.00% | $1,950,000 | $75,000 |

| 2032 | $81,000 | 3.85% | $2,025,000 | $75,000 |

| 2033 | $84,000 | 3.70% | $2,100,000 | $75,000 |

For 2023 I’m being conservative and used ~15% YoY growth for our dividend income projection. If we can earn more income via side hustles in 2023 and keep our high savings rate, there’s a chance we can end up with more than $49,000 in dividend income by the end of the year.

I slowly stepped down the YoY growth rate starting in 2024, based on the assumption that as we get closer to 2025 we’d be increasing our cash savings reserve instead of adding new capital for our dividend portfolio.

If we do start living off dividends in 2025, this should further reduce the amount of new cash available for contribution, so I reduced the YoY growth rate to below 5% starting in 2026.

Overall, I think this updated projection is quite sensible and reasonable. Some readers might consider this projection extremely conservative, given our ability to grow dividend income significantly in the past. But being more conservative in income projection is probably better than being overly optimistic.

Summary – looking ahead

We have always estimated that we’d need between $50,000 to $60,000 to be financially independent. Since I enjoy what I do at work, there’s currently no plan to hand in my resignation letter but I can’t say that will be the case forever.

As mentioned many times in various blog posts, we plan to continue earning income through either part time work or side hustles. There’s no plan to stop working and stop making money. This approach is very similar or perhaps identical to Mark’s FIWOOT (Financial Independence Work On Own Terms) approach.

Inflation is on many people’s minds right now. If inflation continues to be above 6%, growing our dividend income organically at less than 5% means inflation will eat into our dividend income. But I expect the inflation rate will start slowing down (as we’ve seen in recent months). I doubt we’ll see near 0% inflation any time soon but I’m convinced that the Bank of Canada will be able to bring down the inflation rate close to its long term target of 2 to 3%.

Another thing to point out is that we focus not only on dividend income but also on capital appreciation. In other words, total returns matter. Having your principal grow from $500,000 to $1,000,000 while getting a 4% dividend yield is better than getting a 10% dividend yield but having the principal shrink from $500,000 to $100,000.

So, if inflation does eat into our dividend income organic growth rate, we can always consider selling some stocks to supplement the shortcoming. Winding down the principal at some point is absolutely necessary for tax efficiency and estate planning. In fact, when we think about selling principal, it would be far more sensible to sell off stocks gradually over several years to minimize taxes and possibly OAS clawbacks.

Dear readers, what do you think about our updated dividend income projection? Have you done something similar? If you’re already financially independent and living off dividends, did your projections pan out? I’d love to hear from you.

Is it really so common for people in Canada to be able to contribute $150K per year?

Makes me feel really bad…

Jokes aside, great content, keeps me focused and hopeful.

Hi Andrei,

No, I don’t think it’s common. 🙂 We certainly don’t contribute $150k per year…

hi Tawcan, thank you for your site, very good work. For DRIP in a non-registered account, can you please have a detail artical how to report tax return for DRIP, it is very complicated which is why I am afraid of doing DRIP in non-registered account.

Thank!

Hi Frank,

Thank you. I don’t have a specific article about DRIP, might publish something in the future. To get more details, try googling. 🙂

Hi – I am not a math major, so can you clarify how this is working? You had projected $41,500 for 2023 dividends, and I understand you’ve done better than your projection lately, but even if you earn $55,500 in 2023, that still leaves over $100,000 to contribute? I am not an accountant but I do try to really pay attention to your posts and learn how different calculations work, and I am not understanding this one. Thanks for your help

Hi Nic,

You can’t just look at the net contribution amount as some of the dividend growth come from the compounding effect of DRIP and organic dividend growth.

Are you saying that “organic dividend growth and DRIP” will make your earned dividends for 2023 over $67,000? This plan is not making sense to me unless you have over $100,000K new money going in for 2023. What am I missing?

Where are you getting the $67,000 number from? To get to our projection of $49,000 we don’t believe we need to contribute $100k. Considering organic dividend growth and DRIP, probably around $80k or so. But that totally depends on when the contributions are made. If most of that contribution is front loaded, then yes, we should be able to hit $49k. If most of the contribution is backloaded, then we probably need more than $100k. Does that make sense?

Perhaps I am misunderstanding – in your last table, under the heading “Finalizing our dividend income projection” you have noted $167,355

The dividend cut is concerning. It would be prudent to have another projection with past dividend cut ratio modeled in.

Thanks for the suggestion Kai, will consider next time I do another projection deep dive.

Great article, Bob. Nice macro view of before, present and projected future through the three different scenarios with careful consideration. This is the second year I have been tracking our dividends (almost religiously) and even decided to start a blog about it! I like your focus on organic growth, something I try to replicate as well. Even early on, OG has been a big part of our YoY growth, further we have been able to capitalize on OG through fractional purchases so we are able to DRIP +80% each month. Perhaps another iteration of this article can look at the expected breakdown of dividend income by account type (TFSA, RRSP, Non-reg). For ex: “in 2027 we expect to receive X in our TFSA”.

Our strategy is to continue to plug up our TFSAs with TSX dividend payers for optimum tax efficiency. Through previous capital gains we withdrew several years ago in our TFSA, we were able to create an additional six figures in contribution room in our TFSAs. In the next 10 years, our plan once we reach FI or FIWOOT would be to live off TFSA dividends primary which in turn would create additional contribution room the following year that we would then have the option to plug up with additional income/savings. Withdraw and Repeat annually. As you said, the challenge (or opportunity) is withdrawing dividend income in the most tax efficient manner once required.

Cheers,

Josh

Thank you Josh. Good suggestion on the expected breakdown of dividend income by account type. I have written something similar in the past but that was a projection (https://tawcan.com/revisit-our-financial-independence-assumptions/).

TFSA is a very powerful account that more Canadians should be taking advantage of. 🙂

At some point the growth is going to have to slow down. It certainly did for us. Once I realized that working hard, saving every penny, and busting my ass all year only amounted to a few extra thousand dollars, I definitely shifted my focus to growing dividend income organically.

The trick is (of course) when letting off the gas is to not accidentally fall into lifestyle inflation. Once you start to believe you deserve that giant house, luxury car, regular trips overseas, and all the latest tech toys, you’re pretty much done for. There’s no way dividend income can keep up with that kind of lifestyle once it becomes “normal”.

Thanks for the tips Mr. Tako. It’s always nice to hear from ppl ahead of us on the journey.

Thanks for the post! One quick question, what’s the impact of income tax on the dividends? Are they mostly in taxable non registered accounts or RRSP and TFSA type accounts? Just wondering because,

Non-reg means you can dividend tax credit but it results in more tax on other sources of income;

RRSP means eventually it will be taxed like normal income, without the dividend credit;

TFSA can grow tax free within limits

Thanks for sharing!

Dividends in taxable account can be quite tax efficient. If you’re not receiving any working income, you can receive up to $55k or so dividends without paying any taxes.

Tax planning will be quite important moving forward.

You can see our dividend income account breakdown here – https://tawcan.com/dividend-income-december-2022-update-2022-summary/

Love your practical and logical articles.

We’re getting about $110K a year in dividends. Non registered are mostly Canadian and US growth stocks . US stocks in RRSP and TFSA.

We always have the expectation of lower but conservative returns.

Life happens with big ticket costs like a new roof, renovations, appliances, schools and now inflation.

With RESP allowing so little to invest, we’re budgeting for larger university costs for the little ones.

My philosophy is “you can’t have too much money”

Amazing stuff Dad MD. 🙂

Thanks for the insight Mr. T!

Oh wow! I am not sure if I am more impressed by the details and all the calculations and charts or the growth from $0 to more than $30k in dividends in 10 years. Very well done and good luck with the next 10 years.

Am I understanding this correctly? You plan to contribute $167,355.00 new money this year to your investments? Even if this number includes your earned dividends, you will be able to plan to put over $100,000.00 new money into your investments this year?

The math doesn’t work that way, the growth from DRIP and organic dividend growth should allow us to get more dividends compared to last year, so we shouldn’t need to put over $100k into our investments this year.

Pretty impressive portfolio! I hope I can get something similar one day. What do you think about dividend generating ETFs?

Please see here – https://tawcan.com/best-etfs-in-canada/