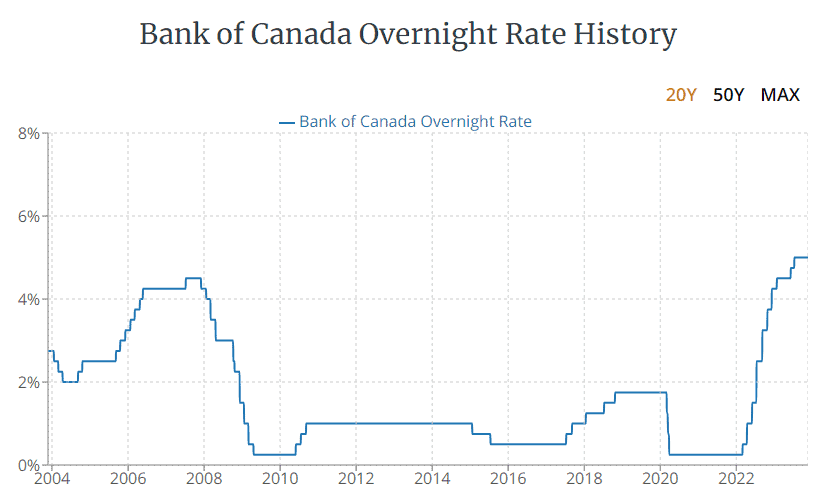

In the last year or so, I have received many emails from readers asking if we are investing in GICs. With the interest rates at the highest level in the last 20 years, banks offer some very juicy GIC rates. Why do we continue to invest in dividend stocks when GICs have guaranteed returns?

Source: Nerdwallet

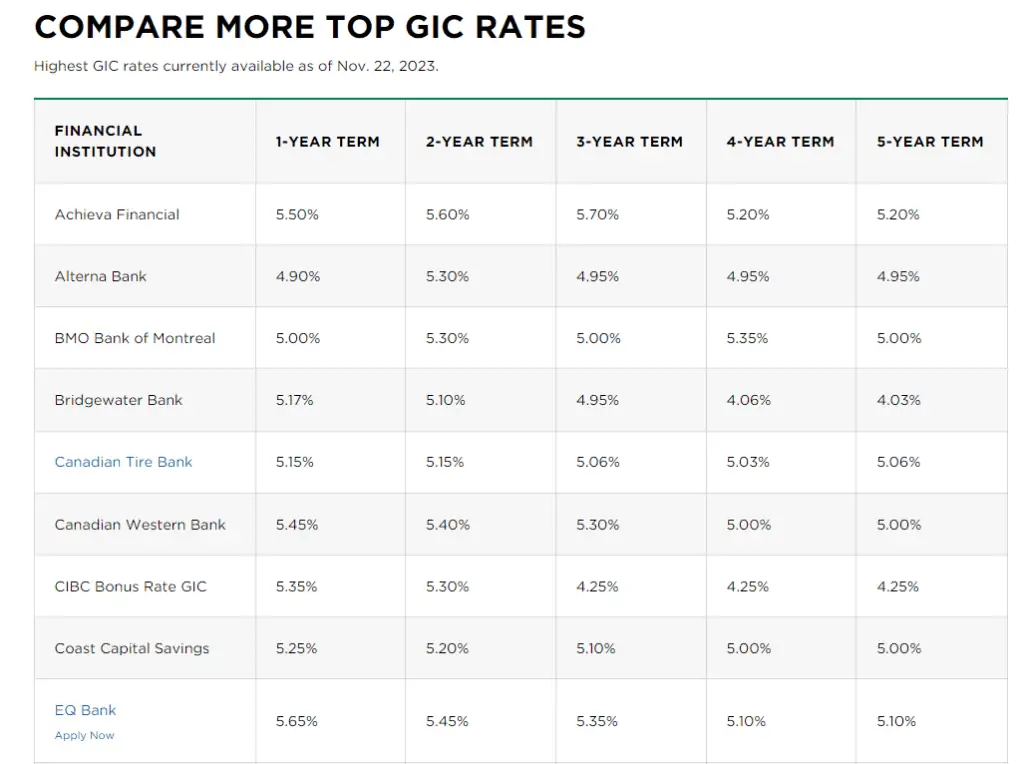

Given it’s relatively easy to find GIC rates north of 5%, it’s not difficult to see why so many Canadian investors are enticed by them – because your capital is guaranteed. You don’t have to worry about the ups and downs of the stock market. You can sleep easy knowing that you won’t lose any money.

Why risk your capital when you can lock in a five-year GIC at more than 5%? At the end of the five-year term, you’ll get your full capital at the end of the term, plus the interest. So if you invest $25,000 in a five-year GIC at 5% from Coast Capital Savings, you’ll end up with $25,000 and $6,250 interest when the GIC matures.

A win-win situation right?

To make matters worse, many of the top Canadian dividend ETFs have underperformed compared to all equity index ETFs like XEQT. Many of the solid Canadian dividend payers like Canadian banks, Canadian pipelines, and Canadian telecoms are all near their 52-week low. Some of them are well below their 2021 highs.

So it’s not a surprise that many Canadian investors have been looking elsewhere than the stock market for their investment.

Investors are always looking for higher returns. And when the returns are guaranteed, people’s eyes tend to light up. In some ways, the shift in money from dividend stocks to GICs further drives the share price down. Some investors that made the shift then use this to validate that their change from dividend stocks to GICs is the right decision (aka a self-fulfilling prophecy).

As a long time DIY investor, I have seen this behaviour many times. Dot-com stocks, cannabis stocks, ARK funds, cryptocurrency, NTFs, etc. Investors will leave a certain asset that underperforms and look for higher returns elsewhere, typically the “hottest asset of the moment” type. The usual fear of missing out (FOMO) behaviour as I’d like to call it.

“To be fearful when others are greedy and to be greedy only when others are fearful.” – Warren Buffett

To me, it is odd that when stock prices go down, people run away from them. People treat these price-depressed stocks like TD, Royal Bank, Telus, and Enbridge like trash. But in reality, when the prices are down, that’s the best time to buy!

Anyway, back to the point of the article… So why don’t we invest in GICs despite the attractive rate? Are we dumb for not locking in our money for guaranteed returns? Why are we continuing to invest new capital into our dividend portfolio and buying dividend stocks that are near their 52-week lows?

Allow me to explain.

GIC return is too low

On the surface, it’s excellent that GIC rates are above 5%. A guaranteed 5% return works very well for retirees and people who are looking for income. A fixed guaranteed income is very popular when the market is volatile or bearish.

But let’s not forget that over the long term, the stock market tends to return between 8 to 10%. If you invest $25,000 over 20 years at a rate of return of 10%, you’ll end up with $168,178.50. On the other hand, if you invest $25,000 in a five-year 5% GIC and keep locking in at 5% for 20 years, you’ll end up with $66,332.44. A significant difference of $101,846.06!

Yes, the stock market will be volatile and can provide negative returns for many years, but history has consistently validated the stock market’s long term return of 8 to 10%.

In other words, the GIC guaranteed principle is a significant downside risk for investors. When the market goes up, you will completely miss the upside by locking your money in long term GICs. Even if you only lock in your money in one-year or two-year GICs, you can still easily miss the run-up.

Imagine in early 2023, instead of investing in VFV (Vanguard S&P 500 Index ETF) or XQQ (iShares NASDAQ index ETF), you locked yourself in a one-year GIC at 5% because you were concerned with a potential bear market.

Needless to say, you’d have missed a significant return during this one year by locking your money in a one-year GIC.

If you need the money in the next two or three years, by all means, invest in a GIC. You may kick yourself for missing out on higher stock market returns, but you’re protecting yourself from the potential downsides. It’s the worst feeling when you need the money and you’re forced to sell stocks or ETFs at 52-week lows.

But if you don’t need the money for the next five years or longer, you’re far better off investing in the stock market for the potential upside.

I came across this Reddit thread a couple of months ago. The thread starter is 22 years old and decided to lock in $15k for a 15-month GIC at a 5.5% interest rate.

Assuming this person doesn’t need the money for the next five years and knowing they are still very young and have a very long investment timeline, I believe they are far better off investing that money in either XEQT or VEQT. Or if they are interested in dividend stocks, split the $15k three ways and buy Royal Bank, Alimentation Couche-Tard, and Canadian National Railway. Over 20 years, I’m 99% sure that they will end up with more money than investing the money in a GIC.

It’s fine if you can’t stomach the potential downside and can’t sleep at night because your portfolio is down 20%. It’s not worth losing sleep over your investment, hence knowing what kind of investor you are is vital.

Just don’t kick yourself when the market recovers and you completely miss out on the ride!

Another important thing I haven’t mentioned is inflation which is running at about 3% or so in the last little while. If your GIC rate is 5%, you’re actually getting 2% real growth. If you lock your money in a five-year GIC at 5% and the inflation rate keeps going up, you are in fact losing your purchasing power!

GIC Interests are taxed poorly

Another important factor to consider is taxes.

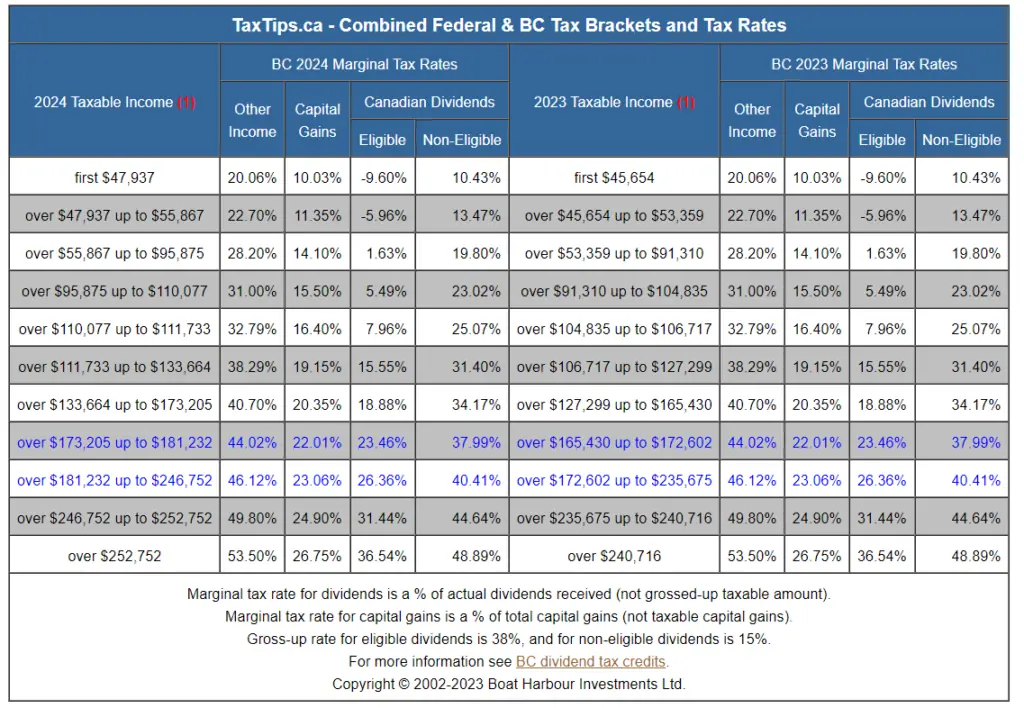

The interests you receive from GICs are taxed at your marginal tax rate. Meanwhile, dividends are treated very favourably in Canada.

ased on the chart above, if you don’t have any working income, you do not have to pay taxes on dividends up to $55,867. This is very powerful when you split your dividend income between you and your spouse.

Since we typically have working income, assuming you’re bringing in $80,000 from your 9-5 job and you received $6,250 in interest from your five-year GIC, the $6,250 is taxed at a 28.20% marginal tax rate. Meanwhile, if you receive $6,250 in eligible dividends from a Canadian dividend stock, it is taxed at 1.63%.

The favourable tax treatment is true across all Canadian provinces and territories.

Remember, taxes matter!

Organic dividend growth

Investors can be short-sighted, ourselves included. Right now, a 5% guaranteed GIC looks a lot more attractive compared to a dividend stock, say Canadian Tire, despite Canadian Tire having about the same dividend yield.

Why? Because investors focus on the word “guaranteed.” Canadian Tire’s share price will be volatile. Investors can lose their principal while you are guaranteed to get your principal back with a GIC.

What if we ignore the principal aspect and only focus on comparing GIC interests and dividends? Are they the same?

One thing to remember is that companies that pay dividends tend to increase their dividend payout. Take Canadian Tire for example. The stock has a 12-year dividend increase streak with a 10-year dividend growth rate of 17.2%. Canadian Tire’s dividends since 2003 look like this:

- 2003: $0.40 per share

- 2004: $0.475 per share

- 2005: $0.56 per share

- 2006: $0.64 per share

- 2007: $0.72 per share

- 2008: $0.815 per share

- 2009: $0.84 per share

- 2010: $0.54 per share

- 2011: $1.10 per share

- 2012: $1.20 per share

- 2013: $1.40 per share

- 2014: $1.875 per share

- 2015: $2.10 per share

- 2016: $2.30 per share

- 2017: $2.60 per share

- 2018: $3.60 per share

- 2019: $4.15 per share

- 2020: $4.55 per share

- 2021: $4.70 per share

- 2022: $5.85 per share

- 2023: $6.90 per share

- 2024: $7.00 per share (estimated)

If you were to invest $25,000 in a five-year 5% GIC and another $25,000 in Canadian Tire today, at the end of the five years, I can confidently declare that you will end up earning more from money in the form of dividends than GIC interests. Let’s not forget that dividends are taxed more favourably, so you will end up with even more money in your pocket.

Even if you invest in a dividend paying stock that has an initial yield of lower than 5%, you may still end up with more money in your pocket. For example, Fortis has an initial yield of 4.20% or $2.36 per share. Fortis has been raising dividends for 50 straight years with a five-year dividend growth rate of 6%, a three-year dividend growth rate of 5.9%, and a one-year dividend growth rate of 5.9%.

Assuming that Fortis continues with the 5.9% dividend growth rate each year over the next 5 years and you invest $25,000 in Fortis at $55 per share, resulting in 454 Fortis shares.

Your dividends would look like:

2024: $2.36 per share or $1,071.44 in dividends.

2025: $2.50 per share or $1,135 in dividends.

2026: $2.65 per share or $1,203.01 in dividends

2027: $2.81 per share or $1,275.74 in dividends

2028: $2.98 per share or $1,352.92 in dividends

At the end of the five-year, you’d end up with $6,038.11 in dividends. This is compared to $6,250 in interest from the five-year GIC at 5%. However, if we consider a tax rate of 1.63% on dividends and 28.20% on interests, you’d end up with the following:

Dividends: $5,939.68

Interests: $4,487.50

Not to mention there’s a very high chance that Fortis’ share price would appreciate during the five years.

Summary – Why we don’t invest in GICs

Above are three key reasons why we don’t invest in GICs and have no plan to invest in them any time soon. We plan to continue to invest in dividend paying stocks and broad market index ETFs regularly with money that we saved up.

The GIC rates are looking enticing but let’s remember they are primarily driven by interest rates. When interest rates do eventually come down – as they will – the GIC rates will go down as well.

While GICs may look very attractive right now, because other investments are not as attractive, this can change very quickly. The question is, if you lock yourself in GICs, can you pivot and change your investments quickly without taking penalties?

For me, I doubt anyone can react so quickly and change their investments. Jumping in and out of different investment assets typically will result in lower returns. That’s why it’s far better to get in line and stay in line – time in the market is far more important than timing the market.

Remember between February and March 2020 when the sky was falling and the market took a sharp turn for the worst amidst all the uncertainties from the global pandemic? If you were to have stayed in the market and continued to invest your money regularly, you’d have done quite well. If you had sold all your investments and moved to cash only, you would have done extremely poorly.

Are GICs the right choice? For us, focusing on long term returns, GICs are the wrong investment assets. But for others, GICs might be the right choice.

Make sure you understand the tradeoffs and that you can rest easy at night with your choices.

GICs are not worthwhile due to low post-tax returns. However, some investors may justify this and say its safe to hold it in TFSA and pocket the 5% return. I personally believe an overall market index or index ETF can beat this return despite the volatility. In bear markets one may face temporary capital loss (kind of paper loss) with index ETFs but they do provide dividend yields around 3%. So when dividends are combined with capital growth we can expect to see around 8-10% returns over a longer time frame (say 7-10 years).

I do understand the big concern about volatility and unpredictable nature of stock prices, which I face too. To diversify or smooth out the fluctuations one likes to have stable income (like GIC). For this stable income there are different options – index ETFs, REITs, mortgage investment corporations (MICs), covered call ETFs, enhanced yield ETF (using options strategies), etc. Each of these stable income options have their pros and cons, so IMO one should look at these options and pick a few that works for them. In a way one is also able to spread risk, diversify in to different asset classes and create cash flow for future re-investment or reallocation.

Sorry forgot to mention I agree with you Bob about the reasoning for not choosing GICs for investment.

Very interesting and timely article Bob. I recently put $50,000 into a 5.25% GIC but I’m turning 60, and with my TFSA maxed out in stocks, I wanted some cash safe at a guaranteed return. My plan now is to invest $25,000 in a non registered account and try and get the same results with 5 to 10 good dividend payers. Are there any ETFs that pay >5% in dividends that you would buy?Thanks for taking the time to write these blogs and putting it into simple terms anyone can understand.

Hi Donna,

I think in your situation putting $50k into a 5.25% GIC makes a lot of sense. Given the market condition, many of the blue chip Canadian dividend stocks are yielding more than 4%.

What’s your opinion of the horizon CASH or HSAV ETF as an alternative to a GIC, especially for emergency funds? Sure it’s not guaranteed and it will be interesting to see how many investors keep their cash there once interest rates drop, but at least it’s more liquid than than a GIC.

I think these ETFs are good as you’re locked into a specific maturity date.

Excellent article, as always, exactly at a time when I was asking myself that question: stocks or GICs?

Thanks Pierre.

love this blog! this article in particular hits home. My husband is always telling me to invest in the market NOT in GIC’s – primarily due to the tax implications. I guess he’s right!

I will still keep some cash in GIC’s for the security (mainly my emergency fund) but i will begin to invest the rest since we have a 15+ year horizon to retirement still.

GICs as an emergency fund don’t make any at all. GICs are generally uncashable until maturity, making them useless for when you need money in an emergency.

You’re better off using HSIA for emergency fund since GICs you’re locked in until maturity.

Thank you Angie, I appreciate your kind words.

Question along a similar line: Do you invest in bonds? Classic 60/40? Or are you 100% equities? If so is the same rationale as above?

We’re investing mostly in equities, very little bonds.

Given the somewhat “low” interest rates (relatively speaking compared to when the percentage bonds to your age idea that came out when interest rates were over 10%), it doesn’t make a lot of sense to be very highly concentrated in bonds.

Agree with everything you’ve laid out here!

Unfortunately the financial advisory industry conditions clients to be happy with 5% CAGR. So when the client sees 5+ yield on GICs, it’s more attractive than it should be.

And interesting you use Cdn Tire as one of your examples. Over the last 10 years, total return is ~6% including dividends and a boatload of volatility. FTS is much better with TR ~9% in that same timeframe.

Thanks. Yes, Canadian Tire was definitely more volatile over the last 10 years.

Agreed! I am always amazed that people get really excited about high interest GICs when it locks your money in when stocks are on sale.

I did choose to invest in a GIC for my kid as a starter investment. I am trying to encourage her to use a GIC ladder with her first job money so that they come up when she isn’t working during the school year – like a little DIY allowance she creates for herself. She’s 15 though, so I am just dipping her toes into the savings and investing pond.

For our Emergency Savings though, I much prefer a HISA over a GIC for the liquidity alone. Sure, the interest will fluctuate with the Prime Rate but at 4.5% (currently) + easily accessible, I’ll take it. There isn’t a lot in there – basically enough for a small-to-medium emergency – but once it goes over a certain amount, I toss it into a dividend payer.

I get GICs are safe investments but IMO they’re a terrible investment for someone who is young and has a lot of time on their hand.

In your case, I’d probably teach your kid more about stocks rather than focusing on GICs.

HISA is a good choice for emergency savings as like you said it’s more liquid.

Thanks for the info! We look forward to reading your blog every week. I think it’s important for people to remember that when Canadian dividend paying stocks (qualified) are in RRSPs, they are taxed as income when withdrawn, just like anything else in an RRSP. Dividend stocks receive the favourable tax treatment in an unregistered account, and of course in a TFSA where nothing is taxed on withdrawal!

Good point that RRSP withdrawals are taxed at your marginal tax rate…. however, long term investments, in theory, should have a higher return than GICs.

Now, if you’re close to retirement age, it may make sense to have a higher percentage of your investment in GICs to avoid volatility.

Brenda, if you’d like a precise list of what Canadian companies pay the Canadian Eligible Dividends in a non-registered account, take a look here (I researched all Canadian dividend payers to see what kind of dividends they pay): https://canadianmoneytalk.ca/list-of-canadian-eligible-dividend-payers/