This is the first time I am doing a year end financial review to show some numbers. Why? Because I have always enjoyed looking at other bloggers’ year end numbers and see how we are in comparison. The numbers also give us a good idea on where we are on our financial independence journey.

Overview of Our Budget System

We started using our current budget system in mid-2011 after our financial epiphany. Each month we break down our after-tax income into 6 different accounts and allocate a certain percentage for each account.

- Necessities/Core Expenses (55%)

- Education (10%)

- Play (10%)

- Financial Freedom Account (10%)

- Long Term Savings for Spending (10%)

- Give (5%)

The percentages listed above are the default suggest values. Over the years we have adjusted all of these numbers to suite our needs. Our necessities percentage is now significantly lower than 55%.

The Number: $47,566.96

In 2016 we spent a total of $47,566.96. This number excludes any business related expenses. As you may recall, Mrs. T and I have a few side businesses; I have a photography business, this blog costs some money to operate, Mrs. T and I have our cookbook business, and Mrs. T has a few other business projects as well.

If we only look at the necessities/core spending, we spent $29.831.40 in 2016.

Here’s an overview of all the numbers since 2012.

| Total Core Spending | Core Spending per Month | Total Annual Spending | Total Spending per Month | |

|---|---|---|---|---|

| 2012 | $26,210.52 | $2,184.21 | $44,603.76 | $3,716.98 |

| 2013 | $26,343.00 | $2,195.25 | $45,260.88 | $3,771.74 |

| 2014 | $29,058.96 | $2,421.58 | $47,391.96 | $3,949.33 |

| 2015 | $31,268.88 | $2,605.74 | $47,270.16 | $3,939.18 |

| 2016 | $29,831.40 | $2,485.95 | $47,566.96 | $3,963.91 |

Note: These numbers do not include money that went into our FFA and LTSS accounts. The numbers only represent money that we actually spent.

Some Thoughts on 2016 Numbers

- We successfully reduced our annual spending and core spending in 2016. Our core spending per month decreased by almost $120 compared to 2015. This was mostly contributed by less money spent on things like gasoline, house heating, household items, and baby related items.

- Food spending stayed relatively flat compared to 2015.

- Education spending went up slightly due to Baby T1.0 starting pre-school.

- Give spending was relatively flat compared to 2015. We spent about $200 per month on gifts and charity donations

- Overall we dined out less but still spent a bit of money on dining out. This is mostly due to taking families visiting from oversea out for meals.

- We saved more money in LTSS and FFA in 2016! Woohoo!

- Our annual spending is roughly $2,000 more than Prince’s ex-wife Manuela Testolini’s extravagant $42,500 per month budget. (Can you imagine actually spending $42.5k per month? Wow!!!)

Areas where we can keep a close eye on or improve

While our expenses look pretty good, there are a few areas we an probably keep a close eye on or do better.

- We eat quite well and love eating great food. With Baby T2.0 now eating solids, we’ll continue keeping a close eye on our food budget.

- For work commute I have been trying to drive at a steady speed of 100 km/hr instead aggressively. Our car mileage has improved by roughly 5%. I nee to continue paying attention on how I drive.

- We have been driving more for grocery shopping because we usually bring the kids along and driving is just easier. What we really need to do is to walk to grocery stores more and reduce our gasoline consumption.

- We shop often at Costco and Save-On. Need to improve on getting produce at the local grocery store because things cost significantly less.

Net Worth: +34.4%

When it comes to net worth, I’m not comfortable sharing actual numbers. Hence I’m only sharing percentages.

In 2016 our net worth grew by a jaw-dropping 34.4%!!!

Holy cow!

Much of the net worth growth came from our house. Vancouver housing price is absolutely insane right now. Given that the federal government and provincial government have both introduced some laws to try to dampen the hot housing market, maybe the 2017 house assessment will drop slightly. We will have to wait and see.

Note: We track our house value by using the yearly assessment value.

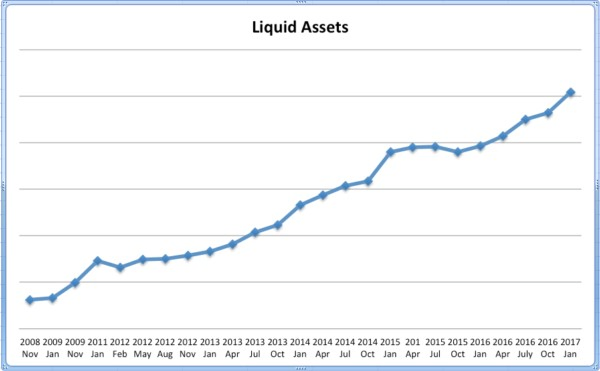

If we only look at our liquid assets, it grew by 29.4% YOY. It is a pretty significant amount of growth. Like everyone else that invests in the stock market, our portfolio value jumped quite a bit after the US presidential election.

The 29.4% increase puts us over a pretty significant milestone. Overall we are very pleased with our net worth increase in 2016.

In case you’re wondering, I have found using Wealthica is a great way to track our net worth and portfolio. If you don’t want to bother with a big Excel spreadsheet, I’d recommend checking out Wealthica.

How We Managed to Grow Our Net Worth

Here are a few things that we have been doing the last few years that have fueled our net worth growth

- We have been maximizing our RRSP contribution room every single year.

- We have been maximizing our TFSA contribution room every single year.

- Once our kids were born, we have been maxing our their RESP every year.

- When all the tax-advantage accounts are maxed out, we then invest in our regular accounts.

- We DRIP our dividend income whenever we can.

- 100% of our dividend income is re-invested.

- We practice frugal living on a daily basis.

- We look at ways to optimize our expenses.

- Focus on increasing our income by side hustle through our businesses.

It’s pretty simple really. We can’t control how the stock market and the housing market will perform, so we only focus on things that we can control.

Financial Independence Progress

In 2016 we received $12,559.74 in dividend income. This amount covered 26.40% of our 2016 annual spending, or 42.10% of our 2016 core spending. Considering that we are aiming to reach financial independence in 2025, we are doing pretty well. Having said all that, about 30% of our dividend income came from the RRSP which is not easily accessible with tax consequences. We will definitely be focusing on our future withdrawal strategy to minimize taxes moving forward.

Our net worth is grew nicely in 2016 and is getting significant. If we were to sell our house, use the proceeds to buy dividend growth stocks, and move to somewhere in Southeast Asia, or a lower cost of living area, we are probably financial independent already. But we choose not to. We are happy living in Vancouver and establishing our roots, I am happy with my work, Mrs. T just recently become a Canadian citizen, and the kids are getting bigger every day. Will our plans change? It might, it might not.

On our recent 1 month stay in Denmark, Mrs. T and I talked about moving to Denmark for a couple of years. We also discussed about moving to Taiwan for a year or so. Having desires to live elsewhere than Vancouver is great but we will need to find a valid way to stay in these countries for an extended period of time.

Mrs. T and I continue to remind ourselves to be flexible. We need to be flexible and fluid with our future plans and goals. Things, plans, and people can all change. We need to be adoptable for these changes.

For now, we are thankful and grateful for an excellent year we had in 2016. We are very much looking forward to what 2017 has in store for our family.

Great breakdown! You have some great growth here! Hope you can continue to progress this way in 2017!

Awesome work Bob. It’s impressive to increase your networth by a third and keep your expenses well grounded! I calculate/update my net worth monthly but am starting to think bi-annually might be better…

Thanks wealthfromthirty.

Yeah that increase is insane! I will have to calculate mine and stick it in my year end review. Also looks like you roughly spend 11k per family member. I will have to also see how I align with you and other FI’ers.

Keep at it,

DFG

Would be interested to see your numbers. 🙂

Wow! nice job on that 34%+ increase also love the EOY dividend. Hoping to see it grow even bigger for 2017. Keep up the good work.

Thanks Jay!

Stellar numbers Bob. Corrected for exhange rates, we spent about the same in 2016. Despite being about 8000km apart in completely different continents and countries ;-).

Unfortunately for us, we were only able to increase our networth by “only” 21%. Deep bow to you sir!

Tahnks Team CF. Good to see what we spent roughly the same amount in 2016.

Great work in 2016! Increasing your net worth by 34% is impressive. Good luck with your Financial Independence goals

Thank you. 🙂

Thanks!

A cool jump! Thanks for sharing and the motivation. What did you spend the education on before baby T1.0 preschool?

Hi Lyn,

We spent on self-improvement and parenting courses.

Great work on keeping your spending down and making regular investments to drive that big net worth increase! Out of curiosity, does your spending number include housing?

Thanks, yes the spending number includes housing.

Wow…thats a nice jump in net worth! Congrats Bob. Looks like things are nice and stable on the spending front. Keep up the great work and thanks for sharing.

R2R

Thanks R2R. We were a bit taken back by the net worth jump that’s for sure.

Great progress on the net worth! Even if it’s from the real estate market you were smart enough to purchase so the credit is yours. I also like how your dividend income is covering 42% of your core expenses. That’s a pretty good spot to be in when you approach FI.

Thanks Mrs Groovy. A good year we had. 🙂

Just out of curiosity, how do you “max” your RESP contribution? I believe you can contribute $50K in total per child. Are you contributing just enough (per kid) to reach the max CESG?

Good to see you doing well! I think you’ll reach your FI goal well before 2025, given how you’ve progressed!

Hi R,

Yes by max out RESP I meant contributing enough to reach the max CESG (i.e. $2,500 per kid).

Wow, that’s some great financial progress in only a single year Tawcan!

My own net worth only grew by 18%, but I’m not working anymore either…so that may have some effect.

Congrats!

Thanks Mr. Tako. Gotta thank to the crazy Vancouver real estate market.

Hi Bob,

You seem to be doing pretty way on your way to FI. Your savings, investments, organic dividend gowth and dividend reinvestments will propel your dividend income higher over time. Also, once you pay off the house, your expenses will likely decrease, wouldn’t they?

Good luck in 2017!

DGI

Hi DGI,

Thanks! Just need to keep doing what we’ve been doing and one day we’ll reach FI. 🙂