Lately, I have received many emails and questions on Twitter asking me about split-shares, or split-share corporations (split corp for short). Specifically, are split-shares safe for building a dividend portfolio? Some readers also asked why I haven’t included split-shares like DFN.TO and LBS.TO in the best Canadian dividend stocks list or the best Canadian dividend ETF list.

With an initial look, these split-shares are extremely enticing and attractive due to the very high yields. Are there risks associated with these split-share corporations? Should one build an investment portfolio with them to generate dividend income?

Before we dive deeper into the details, here is a list of available Canadian split shares I can find, the share price, and the yield percentage. CanadianPreferredShares.ca keeps an updated list of all Canadian split-share corporations issued in the Canadian market.

As you can see from the table, most of these split-shares provide a 10% or higher distribution yield. This is extremely attractive if you’re seeking regular investment income.

You will also notice that some split-shares have suspended their distribution. This is because due to how split-shares are structured, distributions will only get paid out if the Unit Net Asset Value (NAV) is over a certain threshold. More on that later…

So what are split-shares or split corps? Unfortunately, not many investors are familiar with them due to how they are set up. I certainly had to do a bit of research to understand the details.

First, a split-share corporation is set up by investing in a selection of stocks, like banks, utilities, pharmaceuticals, pipelines, etc. For example, Dividend 15 Split Corp. (DFN.TO) invests in 15 stocks – Bank of Montreal, Bank of Nova Scotia, BCE, CI Financial, CIBC, Enbridge, Manulife, National Bank, Royal Bank, Sun Life Financial, Telus, Thomson Reuters, TD, TransAlta, and TC Energy.

Within the split-share corporations, two classes of shares are available – Preferred Shares and Class A or capital shares. Investors can choose to hold both types of shares or just one. These two different kinds of shares are traded on the stock exchanges and can be purchased from online brokers like Questrade or National Bank Discount Brokerage.

Preferred Shares are designed for the more conservative investors who seek regular monthly distributions. Preferred shares typically have a finite term (e.g. 5 years but usually get renewed) and have a claim on fund distributions first. No capital gains or losses from the underlying holdings will impact preferred shares. In other words, the preferred shares are structured like a fixed income vehicle.

Similar to how other preferred share stocks work, while distributions are quite safe, there’s usually a limited capital appreciation potential. There’s no management expense ratio (MER) associated with these split share preferred shares as fees are paid by the Class A shares.

Class A shares are created to provide high yields. The Class A shareholders receive all the gains (and losses) on the entire portfolio and any additional dividends or income generated from the underlying holdings (i.e. leftover dividends/income after preferred shares distributions are paid). Since preferred shares do not pay MER, all MER associated with the split-share structure is paid by Class A Share.

In DFN.TO’s case, the fund has a yield of 17.94%. If you look at the underlying holdings, collectively, none of the individual stocks can produce this kind of high yield. So how do DFN.TO and other Class A split shares generate such high yields?

Remember, one can’t arbitrarily manufacture additional yields unless one takes on additional risks. So to generate the additional yields, split-share funds use leverage and covered calls. As many readers would know, leveraging and covered calls increase the overall risk. In other words, there’s no free lunch. Holding Class A shares is certainly not for the faint of heart.

As mentioned, preferred shares will get the split-share distributions first, followed by Class A shares. What’s important to keep in mind is that Class A shares will only get distributions if the Unit NAV is over a specific threshold, determined and set by the individual fund.

The Unit NAV is determined by the performance of the underlying holdings and the performance of leveraging and covered calls. Class A shareholders need to pay close attention to the Unit NAV.

For example, if the market is doing well and the underlying holdings see a price appreciation, there’s no worry regarding the safety of split-share preferred shares. However, if the market is not doing well, this will cause the Unit NAV to fall below the distribution threshold, causing distributions to potentially get suspended. The Financial Post has a really good illustration of how market performance affects split-share funds.

A suspension in the monthly distributions is something many split-share funds experienced during the early days of the global pandemic.

As you can see, split-share corporations aren’t like traditional dividend growth stocks or ETFs. Hence I have excluded them from any of my best of lists.

Here are some important characteristics you should be aware of if you’re considering investing in split-shares.

- Income, income, income. Split-share funds are designed from the ground up to provide investors with income.

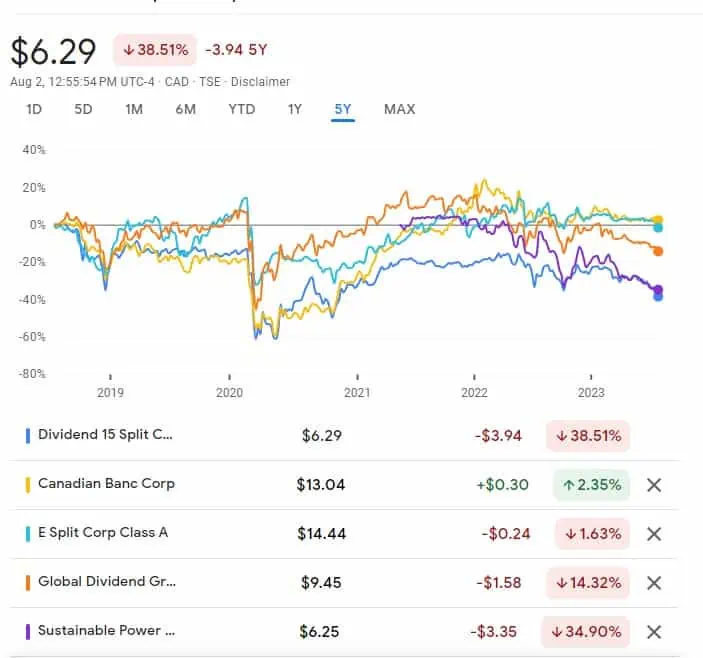

- Limited capital appreciation. Since split-share funds are income-focused, there’s very limited capital appreciation potential, both on preferred shares and Class A shares. You can see the share price performance for DFN.PR.A (Preferred shares) and DFN (Class A shares) below:

- Interest rates. The price of the preferred shares is tied directly to interest rates, just like most fixed-income investments.

- Distributions can get suspended. If Unit NAV falls below the threshold, especially during poor market conditions, you won’t get any distributions. This has happened multiple times in the past with many of these split-shares. Be careful!

- No distribution payout increases. Unlike many dividend growth stocks, split-share fund distributions do not go up and will stay flat forever.

Out of the two different share classes, the preferred shares are definitely the safer and more conservative option. Preferred shares usually mature after 5 years, so you can hold the shares and get your money back at the end of the term.

Please note that like any fixed income investment, the price of the preferred shares is tied to interest rates and has an inverse relationship to interest rates.

Investors looking for stable monthly income may be inclined to invest in preferred shares since it’s moderately low risk. However, while the staple monthly income is nice, you won’t get any capital appreciation.

Given that Class A shares are highly leveraged, you need to ask yourself – Is the yield worth the higher risk? Personally, I would not recommend investing in split-share Class A shares at all.

Just don’t touch them.

Furthermore, if you look at the price performance of many Class A shares, you’ll notice that you end up losing your capital in the long run, despite the high yield. You will encounter a lot of day-to-day, month-to-month volatilities by holding Class A shares.

Personally, I consider these Class A shares a little like annuities (but not as well structured). You’re basically investing money and paying yourself with your own money monthly. Unfortunately, more often than not, you will end up losing your capital with these Class A shares.

Essentially you get a super high yield, but you most likely will be in the red with your investments over the long run.

Since we are focused on total return, not just purely on dividend income, we do not build our dividend portfolio on split-shares. I don’t believe the risks are worth it. I’d rather see our dividend income grow organically and see the value of our investment portfolio grow every year than get monthly distributions that may not be sustainable in the long run.

Having said that, if you are more of a risk taker, you could consider allocating a small percentage of your portfolio to these Class A shares and use them as a way to increase your passive income. But you might be better off utilizing covered call ETFs to increase your yield as covered call ETFs are a little bit lower risk than Class A split-shares.

For us, we would never consider utilizing Class A split-shares. We believe there are other investments that are better suited for our long term goals.

So, are split-shares safe for building a dividend portfolio? Well, if you’re exclusively seeking income, I think the preferred shares may have a place in your portfolio.

It’s a different story with the Class A shares. For Class A shares, I personally wouldn’t touch them with a 100-foot pole. The risks are simply too high and the distributions often aren’t sustainable. Even if the distributions are sustainable, you may end up with a capital loss, so you are not better off in the long run anyway.

Put it this way, if you have a dividend portfolio that yields over 10%, do you believe this income can be sustained in the long run? More likely than not, such a high yield is simply not sustainable. To make matters worse, you probably will experience a drastic capital loss as a result of the high yield. So definitely be cautious whenever people promote these Class A shares as a way to generate dividend income.

Do you invest in split-shares? What’s your view on them?

These types of investments are better suited for a much more experienced investor with a long range for the NAV. If you purchase these split corps at bargain basement bottoms and hold long term, even if the payouts do not continue, the yields only goes down marginally allowing for explosive capital gains and dividend return in a very short amount of time. I received 100% return in a few short months.

I started with my GIC’s cashed in and jumped in to the stock market knowing very little back in late 2021. I bought a fair amount of Split, many that you had listed, 8 in all. I made great dividends for about 8 months but found it unbelievable not to find more details about the split stocks. Then things started falling apart… big time. I sold several for losses and kept reviewing. I finally figured out how the class A & B’s worked and started monitoring them more closely. By the end of 2022 I was into big time losses for this class of stocks. I sold all of them in early 2023. My Split gain was over $3000 in dividends (2022). My loss was -$22,235. It took real grit to take such a hit but I did and reinvested in stable companies with dividend stocks in the 4% to 9.5% range. Split are definitely black box Ponzi stocks in my mind. I have since recovered my losses with other stocks and am fairly happy going into 2024. The end result for 2023 will only be about 0.75% on total money invested. 50% is now in 5+% GICs and the rest in the market. I will be looking at about $32,000 annually for interest and dividends — a little over 6.4% on investment. If stocks go up, then that would be the icing. I share your opinion on Split stocks Bob. Thanks for doing what you do! The stock market for me is a great learning experience. At 78 it is something I can do and enjoy!

Sorry to hear about your losses with split shares Dianne.

Given that Class A shares are leveraged investments, they tend to amplify the volatility of the underlying portfolio. Canadian banks have been underperformers over the last two years, so the split share corporation BK is extra volatile. The following chart plots the returns of BK (dividends included for all) against the BMO equal weight Canadian banks, ZEB, and you can see that if the banks are up BK is up as well and in the long run its returns are quite respectable. Life insurance companies are generally doing better than banks, but also quite volatile. The Lifecos split share corporation LCS is even more volatile, but if you can stand that, it is doing quite well with a yield of 14-16%. I hold BK and LCS as a retired person for income of around 13-16% and willing to live with the volatility as a buy-and-hold investor. Unlike some other high yielding funds the dividends are not eating into the NAV. (The volatility in the share price is also influenced by the low trading volumes, esp in LCS.)

https://www.barchart.com/etfs-funds/quotes/ZEB.TO/interactive-chart

Scotiabank publishes a daily review of preferred shares that you can find here:

https://www.investorvillage.com/groups.asp?mb=13685&mn=74060&pt=msg&mid=24517612

The last page of this document reviews split share preferreds and gives the DBRS rating for many of them. A useful document if you are interested.

I opened a position on DF.PR.A about 5 years ago and have periodically added more over the years. I am currently down 2.00% which I consider pretty good considering the fall in fixed income prices over the last year or so. I purchased the preferred side to give me a steady income that until 2023, exceeded inflation. I purchased it as an alternative to bonds as the income it gives me is more tax efficient, In 2020 it actually increased the dividend rate from 5.25% to 5.75% which was a nice bonus. Overall I am happy with how it has performed that much as expected.

Good to hear that’s performing for you.

I have always looked at split shares with the lens “If it looks too good to be true….”

The whole class of investments probably works well if the stock market never goes down.

I think the only people getting rich are the ones collecting the MER.

That’s a good way to look at things.

DFN has stopped paying dividends since August will not get a dividend until a NAV reaches $15. I bought in a few hundred shares at approximately $7 now is trading at $4.50. My advice is to stay away. I purchased thinking I could make a quick buck as it was going up. Unless bank stocks rebound, this stock is a dog.

That’s definitely a problem with the split-shares. When NVA drops a threshold you won’t get any dividends.

I feel your pain. I had taken most of the split stocks that weren’t paying through 2019 – 2021 and had moved the money into DFN class A shares thinking this one was fairly safe based on historical payouts. Since my average price was close to $8, I felt confident that I would be able to sell them for a little above that, but watched DFN plunge down to $2.94 this Fall. I knew poor Canadian financial performance was coming, but had no idea that it would affect DFN so much. Now my commitment to sell off my Split Stocks has been solidified as I never want to watch months go by without distributions again.

Hi Bob

Great article!! I had my doubts about split shares but you have clearly laid out the details.

Thanks

You’re welcome Raj.

Yuck! Preferreds have languished as well. Unlike bonds they don’t have to be bought back. I would say no to all of it.

Preferred has a place in the dividend portfolio but the split-shares are way too volatile and risky, best to stay away from them.

Great article but a minor update, it’s now X and not twitter..just sayin’….

Thank you. For me, I’ll probably continue to refer X as Twitter. 🙂