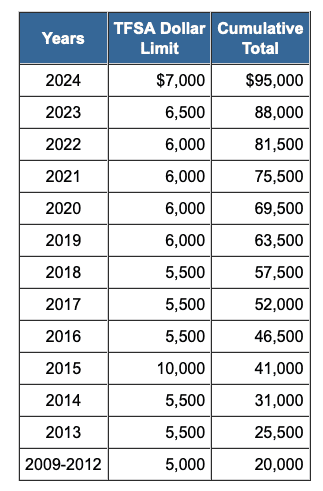

With 2024 just around the corner, I’m sure many Canadian investors, ourselves included, are getting excited about the new TFSA contribution room. Recently it became official that the 2024 TFSA contribution limit will be $7,000. This means that between Mrs. T and I, we’ll have a $14,000 TFSA contribution room.

For those Canadians who are eligible to contribute to TFSA since 2009, the new 2024 TFSA contribution room means you have an accumulative TFSA total of $95,000 available.

At a 4% dividend yield, that means your $95,000 TFSA can generate $3,800 tax free income for you each year.

If you’re not familiar with the TFSA, you may want to take a look at the millennial’s ultimate TFSA guide that I wrote.

Although the math shows that it makes sense to invest in US dividend stocks in your TFSA, we plan to use all of the $14,000 to buy Canadian dividend paying stocks. Why? Because this is the simplest approach. That way we’d avoid the 15% withholding taxes on US dividend paying stocks and as well as having to convert currency back and forth. Furthermore, Canadian dividend stocks typically have higher yields than their US counterparts, making TFSA a good investment vehicle to invest in these higher yield dividend stocks.

Which Canadian dividend stock are we considering buying in early 2024 for our TFSAs?

Let’s find out, shall we?

Consideration #1: Alimentation Couche-Tard (ATD.TO)

The first Canadian dividend stock we’re considering is Alimentation Couche-Tard.

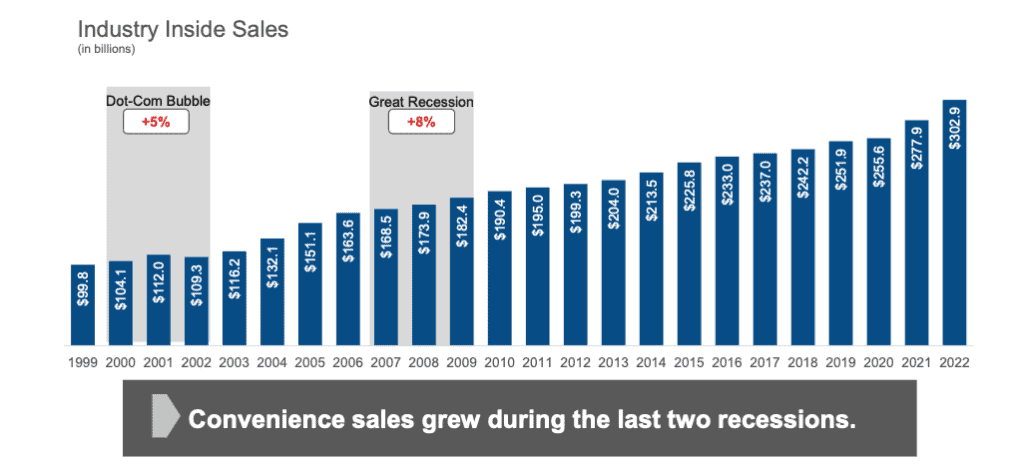

Alimentation Couche-Tard operates convenience stores in 25 different countries. ATD’s stock price performance has shown that the company is very recession resilient.

Recently ATD’s management announced it aims to achieve US $10 billion in EBITA by FY2028, up from US $5.8 billion in FY2023.

It was interesting to note that back in 2018, ATD’s management launched the “Double Again” 5-year strategy where they set various doubling goals, including doubling EBITA. As FY2023 closed, ATD revealed that the company has achieved the Double Again strategic goal.

With a solid historical track record, I have confidence in ATD’s management that they can achieve the $10 billion US in EBITA goal in five years.

In addition, ATD has increased its dividend payout at an impressive rate of 21.2% over the last five years, showing that the management is very shareholder friendly.

Adding more ATD shares should help us on the total return front. Due to the low initial dividend yield, ATD wouldn’t be considered as a dividend income play initially, more as a growth stock with a slight dividend.

Potential Risks for ATD.TO

ATD has been expanding by acquiring other companies. Recently ATD announced it would acquire certain European assets from TotalEnergies. Since acquisitions are often costly and it takes additional time, money, and effort to integrate these acquired companies. This is just one of the potential risks for ATD.

Having said that, since ATD has done many acquisitions over the years and has shown that they can smoothly integrate the acquired companies under the ATD umbrella, so this potential risk is low.

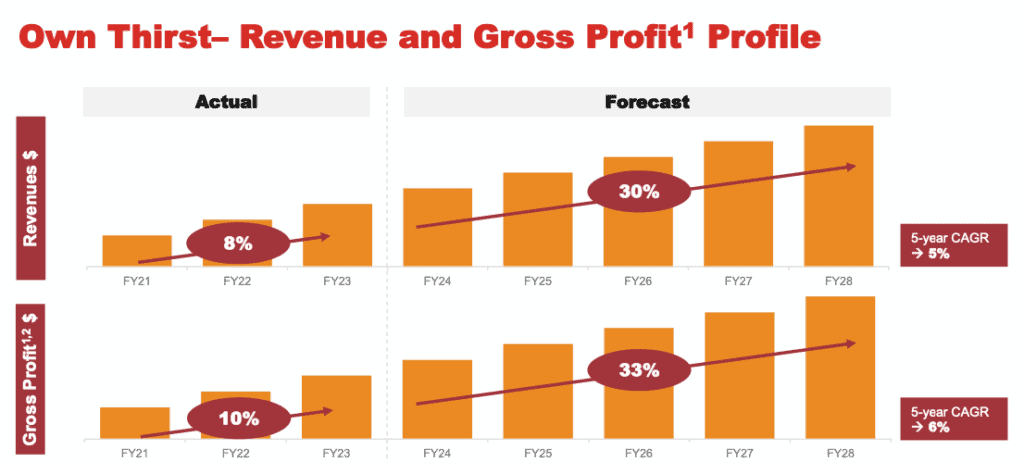

ATD has a goal of expanding fresh food offerings in their convenience stores. The company also believes the #1 reason why customers visit their convenience stores is for cool drinks. As a result, ATD plans to invest money in their stores to enhance the customer experience in food and drink items. This can be a costly exercise if this move doesn’t improve revenue and gross profit to the levels that ATD anticipates.

Consideration #2: Canadian Natural Resources (CNQ.TO)

Next up on our consideration list is Canadian Natural Resources, a Canadian oil and natural gas company that operates primarily in Western Canada.

During the latest quarterly results, CNQ announced an 11% dividend hike, making the 24th consecutive year of dividend increases with a Compound Annual Growth Rate (CAGR) of 21% over the same time period.

Furthermore, the company has set a debt target of $10 billion which they believe will be achieved in Q1 2024. When this debt target is hit, the company has specifically stated it plans to funnel 100% of its free cash flow to shareholders through either share buyback or special dividends.

In the past Canadian Natural Resources paid a $1.50 per share special dividend in August 2022, so the general consensus among investors is that CNQ will declare a special dividend sometime in 2024.

Overall, CNQ is firing on all cylinders and the stock is at an attractive price considering the strong performance and significant free cash flow. It may make sense for us to buy more CNQ shares, dollar cost average up, and have more shares in anticipation of the special dividend in 2024.

Potential Risks for CNQ.TO

Canadian Natural Resources is an energy company, so its profitability is directly tied to the price of crude oil and natural gas. Therefore, the biggest risk would be if oil and natural gas prices unexpectedly tank in 2024 and stay low for a sustained period of time. This would hurt CNQ’s profitability and cause the share price to drop. Let’s not forget that both crude oil and natural gas prices are cyclical in nature, so CNQ performance can be cyclical as well.

This is exactly what happened in the early days of the global COVID-19 pandemic when the demand for crude oil was extremely low due to lockdowns. But CNQ showed its ability to weather the storm amidst all the pandemic uncertainties and didn’t cut its dividends, unlike many of its energy peers. As a shareholder, this gives me a lot of confidence in the CNQ management team.

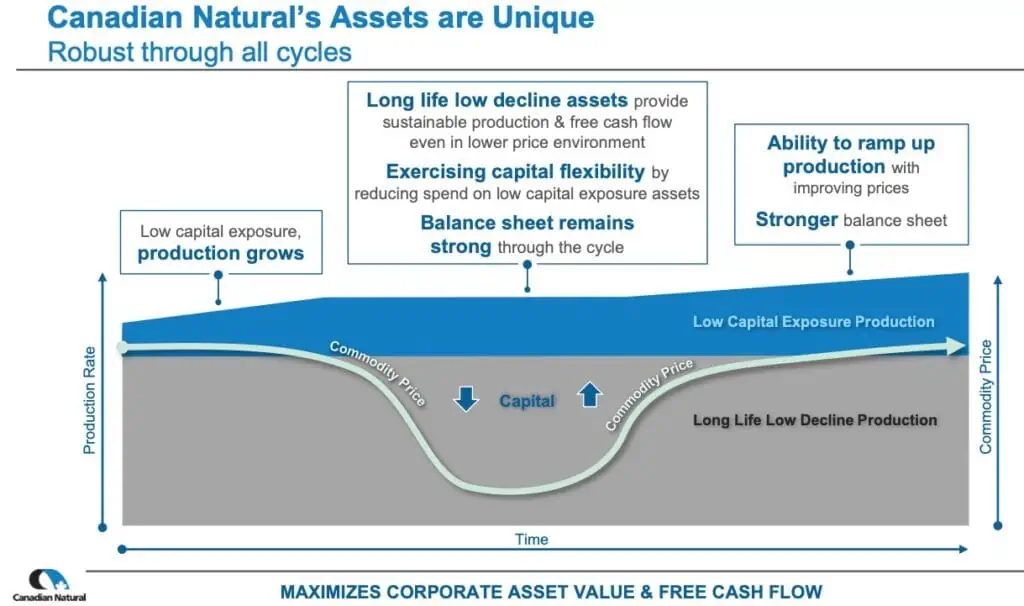

As you can see in the above chart from CNQ, the company provided examples of how to stay robust through different financial cycles.

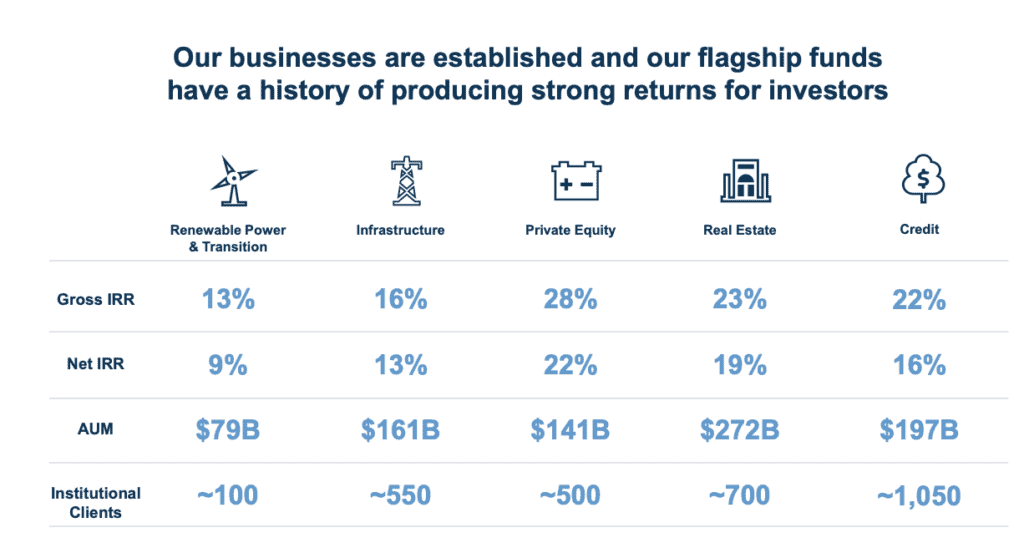

Consideration #3: Brookfield Asset Management (BAM.TO)

Although Brookfield Asset Management has a very different business model as Berkshire Hathaway, the two companies have many similarities. It may be a bit of a stretch but you can probably say that Brookfield Asset Management is the Canadian equivalent of Berkshire Hathaway. (And Brookfield CEO Bruce Flatt has often been referred to as “the Canadian Warren Buffett.”)

BAM is one of the world’s leading asset managers with $850 billion of assets under management (AUM) across renewable power and transition, infrastructure, real estate, private equity, and credit. The company also generated $4.3B annual fee revenue, achieving significant scale as a company.

What’s impressive is that Brookfield Asset Management grew its AUM significantly from $3 billion in 2022 to $850 billion in 2023.

Brookfield Asset Management is set up to distribute ~90% of its free cash flow and grow the dividend payout each year. Hence for making BAM quite attractive for dividend investors like us.

Before the split of Brookfield Asset Management and Brookfield Corporation, the parent company Brookfield Asset Management provided an annualized return of 19% for its shareholders from 2002 to 2022. This is very impressive.

As a shareholder, I have a lot of trust and confidence in Brookfield’s CEO Bruce Flatt and his team. I believe the team will continue to deliver remarkable performance for years to come.

Currently, Brookfield Asset Management and Brookfield Corporation make up less than

1.5% of our dividend portfolio. We’d like to add more shares and hopefully bump up the overall exposure to between 3 – 4% in the near future.

Potential Risks for BAM.TO

Due to how Brookfield Asset Management is structured, it will only pay out dividends if it is profitable and has free cash flow. So, if the AUM and free cash flow were to decrease, this would cause the dividend payout to drop. Having said that, since Brookfield is a well-managed company, the chance of this happening should be quite low.

Brookfield has a very complex structure and the splitting of the original Brookfield Asset Management into two companies makes things arguably even more complicated. For the average investor like you and me, it can get very confusing to go over the quarterly results and comb through all the financial statements.

In other words, if Brookfield decides to do some funny accounting (I highly doubt they will), the company might be able to do it through the various sub-companies.

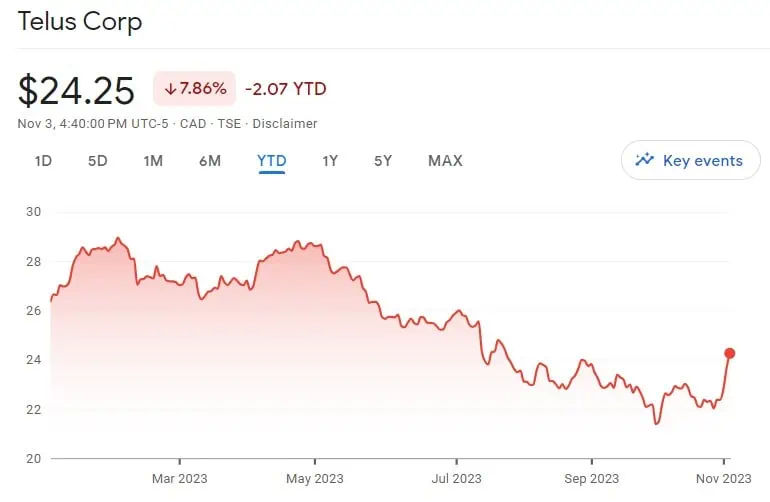

Consideration #4: Telus (T.TO)

Telus is one of the big three telecommunication companies in Canada with 18.9 million subscribers as of Q3 2023.

2023 hasn’t been kind to Telus with the stock down almost 8% year to date. During the recent Q3 results, Telus announced that its Q3 profit was down 75% from a year ago. The company blamed the lower profit on high interest rates, high restructuring costs, and the high network buildout cost.

Interestingly Telus reconfirmed the 2023 consolidated financial targets and increased the dividend payout by 3.4% from $0.3636 per share to $0.3761 per share.

While the drop in profit is concerning, I noted that Telus added 406,000 customers in Q3, an increase of 17% YoY. This included an addition of 160,000 mobile phone subscribers. I am happy to see such strong subscriber growth, especially considering the increased competition in Western Canada given the Rogers-Shaw merger.

Telus currently has about 30% of the Canadian telecommunication market. Knowing that Canada is planning to welcome more than 485,000 new permanent residents in 2024, 500,000 in 2025 and 2026, if Telus continues to hold 30% of the Canadian market, the new immigrants should help continue to drive new subscribers for Telus.

Telus has been very shareholder friendly with a ten-year annualized dividend growth rate of 8.3%, which is roughly aligned with Telus management’s target of a 7 to 10% annual payout increase through 2025 with typically two raises annually.

Yes, Telus is facing some headwinds due to high interest rates and the high cost of rolling out stand-alone 5G networks. But this is not different than when Telus rolled out its LTE network across Canada many years ago.

At the current share price level and an initial dividend yield of 6%, I strongly believe Telus is a bargain and we should consider loading up on Telus shares.

Potential Risks for T.TO

The biggest risk is the level of debt that Telus has. As of Q3 2023, Telus has a substantial total liability of $38.1 billion. This can be a concern given the rising interest rates environment. In the Q3 2023 results, Telus management reported that its balance sheet remains strong with the average cost of the long term debt at 4.33% which is well below the current interest rates. Furthermore, Telus has a strong debt maturity schedule with the average maturity of the long term debt at nearly 12 years. So the rising interest rates shouldn’t be a major concern for Telus.

The Rogers and Shaw merger meant a strong competitor for Telus in its dominant region of Western Canada. It will be interesting to see how Telus deals with the aggressive phone, TV, internet, and cellphone pricing from Rogers and Shaw moving forward. If Telus decides to match Rogers/Shaw’s aggressive prices, this could mean an erosion of its profit margins.

The one benefit that Telus has over Rogers and Bell is that it doesn’t have to deal with media creation. But Telus has been branching out of its core telecommunication services. Telus International was one example where it underperformed, hurting Telus’ overall profitability. Therefore, Telus must be careful with its plan of expanding outside of its core competency moving forward.

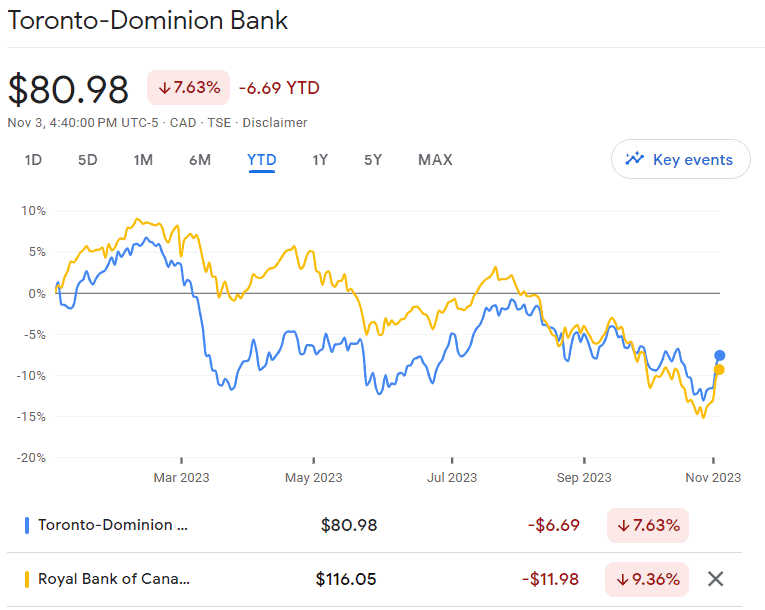

Consideration #5: Royal Bank (RY.TO) and/or TD (TD.TO)

Royal Bank and TD are the top two banks in Canada. I grouped the two together here because they’re both in the financial industry and are very similar.

Like Telus, 2023 hasn’t been kind to both Royal Bank and TD, both have been in the red year-to- date. The poor performance has mostly been caused by concerns over high interest rates, potentially causing consumers and businesses to default on mortgage loans.

Personally, I believe the mortgage loan default concern might be a bit overblown. Both Royal Bank and TD have been setting aside money (i.e. loan loss provision) to protect themselves in case loans were to default. This is something that all Canadian banks did during the global pandemic. In the end, the banks didn’t need as much provisioning and the money ended up in the pockets of shareholders as dividends and share buybacks.

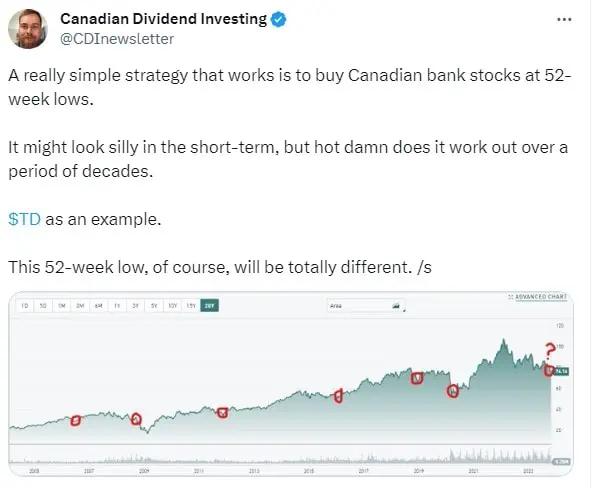

Both Royal Bank and TD are near their 52-week lows. The initial dividend yield of 4.65% and 4.74%, respectively, are considered quite high compared to 10 averages (3.9% for RY and 3.8% for TD). Although these initial yields aren’t anywhere close to the highest yield in the past 10 years (6% for Royal Bank and 6.3% for TD), I believe such high yields won’t stick around for too much longer.

Let’s not forget that both Royal Bank and TD have been paying uninterrupted dividends since the late 1800s. The word uninterrupted should make many dividend investors quite excited.

As Nelson, a fellow Canadian dividend investor & blogger pointed out recently. A really simple strategy that works well is to buy Canadian banks at 52-week lows. While we can’t predict the future with 100% accuracy, it is hard to ignore the historical facts.

Potential Risks for RY.TO and/or TD.TO

The biggest risk that Royal Bank and TD face today is the high interest rates and whether Canadians can continue to pay their mortgage payments. If Canadians start having problems paying their mortgages, this will create a major financial tsunami in Canada.

As an optimist, I don’t believe that’s going to happen. Canada’s inflation rate decelerated to 3.8% in September, down from 4% in August. This is a sign that the rising interest rates are effective and if the inflation rate continues to drop in the future, the Bank of Canada will consider lowering the interest rates.

Furthermore, I believe both Royal Bank and TD are too big to fail. If these two financial institutions were to fail, the Canadian economy would be in a lot of trouble. I strongly believe the Canadian government would have to help and bail them out.

Summary – dividend stocks we’re considering for 2024 TFSA

There you have it, five Canadian dividend stocks we are considering adding inside of our TFSAs in early 2024. I picked a mix of low yield high dividend growth stocks and high yield low dividend growth stocks. More importantly, I picked stocks that should give solid total returns in the long run.

What are some dividend paying stocks you’re considering adding to your TFSA in 2024?

Another great update. I find the reasoning behind ethical dilemmas many seem to have with CNQ (and a host of other energy sector stocks) murky at best. I understand there is legitimate environmental concerns but one has to ask would we better off if these entities ceased to exist? What are the alternatives? At this point other methods would not fulfill our needs. Furthermore I would argue that It would be more ethical to invest in companies in the energy sector that operated in nations with stricter operational regulations in place. The alternative of increasingly relying on nations that exploit workers and have little to no environmental regulations is a far worse proposition in my humble opinion.

Thank you. Yes there are certainly ethical and environmental concerns with CNQ.

Another great blog!

I’m curious to know if you recommend BAM or BN?

I don’t know if I should expand my positions in both or sell one and buy more of the other. Thoughts?

BAM is more for income.

BN is more for total return.

BN owns about 50% of BAM.

IMO both are very solid.

I like CNQ for all your reasons and for the fact that it produces the most important product in the world and is working hard to reduce CO2 emissions in a practical manner. Oil and gas will be an important part of our lives for a long time. Very well run company.

I am confused about the risks for TD and RY regarding mortgage default risks. When I looked at this it is CMHC on the hook not the banks. Could you confirm that they have significant exposure?

Thanks for the info

Despite CMHC, there Canadian banks still take on risks on mortgage and other loans. This is why all the Canadian banks have been increasing their provisions.

TD is about incur a big fine (~1B). They seem to have a history of issues with compliance in the USA (aka money laundering). BUT the 5% yield just increased by 6% is hard to ignore. Maybe buy after the fine? I don’t like CNQ for the same reasons given above (tar sands) and as well the inevitable long good bye to oil. BCE at 7% is pretty tasty too, as well EMA at 5.9% with interest rates declining next year. On the growth side I’m with Stephen on DOL and I’ll propose EFN (GARP).

That’s a good point about TD’s big fine but they have had a history of similar issues so I’m not too concerned.

Makes sense that you’re avoiding CNQ for the environmental reasons.

“Although the math shows that it makes sense to invest in US dividend stocks in your TFSA, we plan to use all of the $14,000 to buy Canadian dividend paying stocks”

I don’t know what to make of this quote, I mean naturally there’s no point in owning a stock like VZ (Verizon in a TFSA) when we have many Canadian high dividend yielders…to that you are 100% right.

But I think it’s a case by case situation.

In my case, I am in the lower tax bracket and will most likely be in the lower parts of the tax bracket which means the TFSA has priority over the RRSP.

Therefore, by going all Canadian to avoid the witholding tax, I will have two issues, too much home bias and a lack of diversification. Let’s face it, Canada is mainly known for Financials and Energy. We don’t have any Health Care dividend payers, well not reliable ones as an example.

Also, the US has much more access to dividend growers (just look at the number of Dividend Kings and Dividend Aristocrats they have), so although it’s great to buy good high Canadian dividend yielders, it is equally important not to ignore the US market either.

Now if you’re in the tax bracket where the RRSP has much more importance for you, the option is better to hold US stocks there, but for someone like me who needs to maximize the TFSA and will unlikely max it out, I think having both is a prudent choice.

One thing I will do though is avoid those high yield US stocks that offer little in capital appreciation. Dividends are great, but we shouldn’t totally neglect capital appreciation either.

Not a bad list btw

It was based on my analysis here – https://tawcan.com/does-it-make-sense-to-invest-us-dividend-stocks-in-tfsa/

Hope this helps.

Good selections, Bob. As much as I love CNQ, i have chosen to exclude it from my portfolio for climate reasons.

A couple of options I am bullish on in 2024 that you haven’t mentioned here is WCN, DOL, and STN. I’m still +15 years out from ‘retirement’, so I am focusing more on capital appreciation in my TSFA as opposed to dividend yield. I’ll switch strategies when the time comes.

ps – i also subscribe to purchasing the big 6 (RY,TD,BMO) when they are treading on 52 week lows. It’s a successful strategy.

Hi Stephen,

That’s fair about CNQ. We don’t invest in tobacco companies for ethical reasons.

Very solid pick on WCN, DOL and STN. Yup, total return is important when you have a long retirement timeline.

Hi Bob! Thanks for another great article. You mentioned that for CNQ, you will buy: “more shares in anticipation of the special dividend in 2024”. Where did you get this info because they have not issued a special dividend in 2023?

Thank you Valerie.

It was a speculation on my part. CNQ is sitting on a large pile of cash. Last time they had a lot of cash they distributed it in the form of special dividend.

Divid

Hi Bob Would u consider the recent tax on the Cdn Banks of 3 billion over a period of 5years which will be born mainly by the big 6 to be of any significance in buying or holding any of the big 6 banks which are usually thought of as safe solid quality dividend growth stocks.

Yes it a headwind against the banks but I think they’ll do just fine despite the additional taxes.