With the first half of 2023 in the books, I thought it’d be an interesting exercise to review our dividend portfolio. The key focus will be determining what to do with each position – should we continue to hold, should we add more shares, should we trim some shares, or should we close out the position altogether?

At the time of writing, we hold 48 individual dividend stocks and 1 index ETF. We went from a total of 50 individual dividend stocks down to 48 with the closing of Verizon and Omega Healthcare in May.

Our dividend portfolio generated $24,685.91 in the first half of 2023. Based on my current dividend income projection, we are on track to receive over $49,000 in dividend income. If companies continue to raise dividend payouts and we continue to reinvest dividends via DRIP, there is a very small chance we may even get close to $50,000 in dividend income for this year.

Fingers crossed!

Our holdings in alphabetical order are:

- Apple (AAPL)

- AbbVie (ABBV)

- Algonquin Power & Utilities (AQN.TO)

- Brookfield Asset Management (BAM.TO)

- BCE (BCE.TO)

- Brookfield Renewable Corp (BEPC.TO)

- BlackRock (BLK)

- Bank of Montreal (BMO.TO)

- Brookfield Corporation (BN.TO)

- CIBC (CM.TO)

- Canadian Natural Resources (CNQ.TO)

- Canadian National Railway (CNR.TO)

- Costco (COST)

- Capital Power Corp (CPX.TO)

- Canadian Tire (CTC.A)

- Dream Industrial REIT (DIR.UN)

- Emera (EMA.TO)

- Enbridge (ENB.TO)

- Fortis (FTS.TO)

- Granite REIT (GRT.UN)

- Hydro One (H.TO)

- Intact Financial (IFC.TO)

- Johnson & Johnson (JNJ)

- Coca-Cola (KO)

- McDonald’s (MCD)

- Manulife Financial (MFC.TO)

- Magna International (MG.TO)

- Metro (MRU.TO)

- National Bank (NA.TO)

- PepsiCo (PEP)

- Procter & Gamble (PG)

- Power Corp (POW.TO)

- Qualcomm (QCOM)

- RioCan REIT (REI.UN)

- Royal Bank (RY.TO)

- Starbucks (SBUX)

- SmartCentres REIT (SRU.UN)

- Suncor (SU.TO)

- Telus (T.TO)

- TD (TD.TO)

- Target (TGT)

- TC Energy (TRP.TO)

- Visa (V)

- VICI Properties (VICI)

- Waste Connections (WCN.TO)

- Waste Management (WM)

- Walmart (WMT)

- iShares international ex-Canada index ETF (XAW.TO)

As you can see, we hold some dividend stocks like Enbridge, TC Energy, and BCE with very high yields. Some of these higher-yield dividend stocks have low dividend growth. On the other hand, we also hold some dividend stocks like Apple, Waste Connections, Visa, and Costco that have very low dividend yields but have raised dividend payout at high rates over the years.

The idea is to have a mix of high yield low dividend growth and low yield high dividend growth stocks to generate sufficient dividend income for us to eventually live off dividends. We want our dividends to continue to grow organically when we slow down with new capital contribution.

With that in mind, here’s our 1H 2023 dividend portfolio review.

1H 2023 dividend portfolio review – Part 1

Because of the number of stocks and the length of the article, I decided to break up the review into 3 parts. This is the first part of the review.

For the dividend portfolio review, my plan is not to sugarcoat anything and provide readers with my thoughts and what I’m thinking about each holding.

1. Apple (AAPL)

It’s not a surprise that we like Apple a lot. Over the years, Apple has transformed itself from a hardware-centric company to a company that generates revenues from both hardware and software. Furthermore, Apple is slowly turning itself into a consumer discretionary company (some may argue it’s almost like a consumer staples company) rather than a high-tech company.

The Apple silicon is a game changer for Macs. iPhone continues to be dominant in the smartphone sector (a side note, Mrs. T and I recently watched BlackBerry and it reinforces my belief that Apple doesn’t enter a product segment early. Instead, they spend time researching and perfecting a new product that works better than other existing products. Essentially, they are changing the product environment. One only has to look at the iPod, the iPhone, and the Apple Watch to see the truth of “the Apple approach”).

Over the next while I believe many Apple users will be looking at upgrading their existing Intel-based Macs and moving to Apple silicon based Macs. This will drive Apple revenues. Given that the 15 inch laptop segment is the most popular segment for laptops, Apple coming out with a 15 inch MacBook Air will also help the company become a dominant force in this particular segment.

Furthermore, I have no doubt that Apple will continue to execute well in the existing product segments and come out with complementary accessories that would generate more revenues for the company.

The new Vision Pro looks like yet another revolutionary product from Apple that has the potential to disrupt and change the AR & VR space. Knowing Apple’s new product history, I would guess that the Vision Pro won’t get widely adopted until the third or fourth generation. But things can change pretty quickly…

Not to mention that Apple has been generating more and more revenues from subscription services like Apple Music, the Cloud, etc. These are recurring revenues with high margins, the type that investors love.

I’m convinced that Apple will continue to do well and that is why we bought more Apple shares recently.

2. AbbVie (ABBV)

AbbVie has had a tough year with the share price near a 52-week low. This was mostly caused by the impending decline in revenue from Humira, as there are at least 8 similar versions that will be launched by AbbVie competitors this year.

However, I’m not concerned. The company continues to invest in R&D for new drugs which should provide future revenue growth.

If the stock price stays low we may consider adding more ABBV shares.

3. Algonquin Power & Utilities (AQN.TO)

Ugh, AQN, what a freaking mess! Despite cutting its dividends and pulling out of the Kentucky Power acquisition deal, the share price continues to struggle to recover.

We’re down quite a bit on our AQN holding but don’t plan to sell shares at a loss. If we see some price recovery, we may consider selling some portions over time.

For now, we plan to DRIP and dollar cost average over time. AQN has definitely dragged our overall portfolio performance this year.

4. Brookfield Asset Management (BAM.TO)

Brookfield is a big name in North America and I have a lot of confidence and trust in its executive team.

I believe the company made the right move and split the company into BAM and BN to unlock potential values. The stock price has been relatively flat since the split but I believe over the long term, the stock price should increase, and probably, substantially..

We plan to add more BAM shares whenever we can.

5. BCE (BCE.TO)

BCE is a high dividend yield stock with a good history of dividend growth. The share price has trended down in the past year.

I believe this is caused by the higher interest rates and concerns over Starlink. The media segment business for BCE has not done all that well lately and BCE has been working to cut costs in that segment.

I’m not too concerned with these three things as I think BCE is experiencing some short term headwinds but long term it should be OK.

6. Brookfield Renewable Corp (BEPC.TO)

Recently BEPC announced that they’d buy the commercial renewable business from Duke Energy. This should solidify Brookfield Renewable’s position as one of the largest renewable energy businesses in North America. Furthermore, this purchase should generate strong cash flow for Brookfield.

We like the renewable sector. BEPC is a long term holding so we plan to add more shares.

7. BlackRock (BLK)

BlackRock has seen better days but the company is poised to do well long term. With the popularity of ETFs, it makes a lot of sense to invest in the parent company of iShares. Not to mention that BlackRock has been growing dividend payout consistently.

We plan to add more shares whenever we have some USD available.

8. Bank of Montreal (BMO.TO)

We have been BMO shareholders for a long time now. At the time of writing, I think BMO has an attractive entry point so we plan to add more shares whenever we can. BMO has been paying dividends since the late 1800s so I have no concerns with its dividend payment record.

BMO is definitely a long term holding for us.

9. Brookfield Corporation (BN.TO)

Brookfield Corporation is a newly formed company from Brookfield Asset Management. While the yield is quite low, it should provide some long term capital growth. Brookfield invests in high quality assets and businesses around the world that form the backbone of the global economy. At time of writing Brookfield Corporation owns $825+ billion assets across 30+ countries across segments like newable power & transition, infrastructure, private equity, real estate, insurance, and credit.

I’m quite confident with the Brookfield management & board so we’ll aim to add more BN shares over time.

10. Bank of Nova Scotia (BNS.TO)

BNS has performed quite poorly in comparison to other Canadian banks. This is mostly caused by the company’s presence in Latin America. Over the last few years, BNS has been slowly reducing its exposures in Latin America, but perhaps not fast enough.

While BNS has the highest yield out of the Big Five, I am slightly concerned that the total return performance has been poor over the past few years.

Given the poor historical performance, we may consider reducing our exposure to BNS and investing the money in other banks like TD, NA, or RY.

11. CIBC (CM.TO)

Like BNS, CIBC has a relatively high dividend yield and has performed poorly over the last five years. CM’s poor performance is mainly driven by its heavy exposure to the Canadian mortgage market.

For now, we plan to continue holding CM and dollar cost average via DRIP. We will have to monitor and see whether it makes sense to reduce our exposure to CM or not.

12. Canadian Natural Resources (CNQ.TO)

I’m glad we didn’t get rid of CNQ during the pandemic lows. As demands for oil rebounded, CNQ’s share price recovered and CNQ even paid out a special dividend.

However, due to the cyclical business nature, CNQ’s share price will bounce up and down, heavily dependent on oil prices. Since we are enrolled in DRIP, we can dollar cost average over time.

CNQ continues to be a solid stock for us, earning its inclusion as one of the best Canadian dividend stocks.

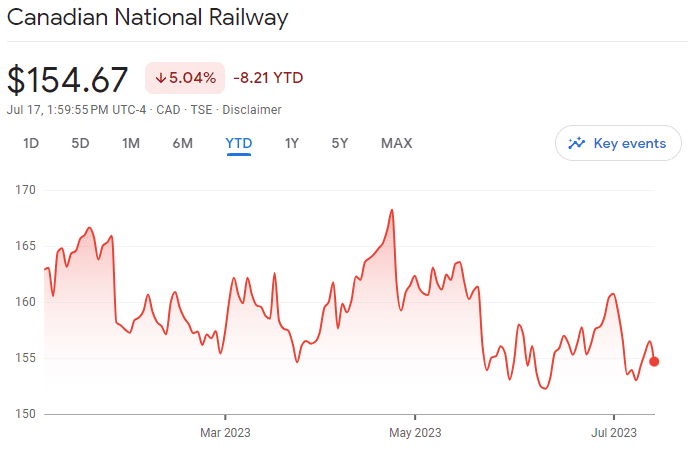

13. Canadian National Railway (CNR.TO)

Although Canadian National Railway’s share price has struggled year-to-date, I’m not too concerned. I believe CNR’s share price will continue to appreciate over the long term.

While most people travel across North America by car or plane, rail is still the key method for transporting goods across North America. CNR’s vast network of railways will help to drive and grow revenues.

Given that CNR has been raising dividends at over 10% annual growth rate, we plan to add more shares of CNR and take advantage of the depressed share price.

14. Costco (COST)

It shouldn’t be a surprise that I like Costco a lot. We shop regularly at Costco and I have done a number of price comparisons over the years to show that Costco is the cheapest grocery store in Canada compared to the likes of Superstore, Walmart, Safeway, and Save-On-Foods.

Costco makes most of its revenue from membership fees and the membership renewal rate is around 92% in the US and Canada and around 90% globally. While Costco has decided to delay its membership fee hike, a small increase of $5 or so will definitely generate Costco a great amount of revenue.

Why invest in Costco? Well, first of all, the business is stable and easy to understand. Like McDonald’s, Costco opens up its warehouses at strategic locations, attracting shoppers from different cities. Also, Costco has been a reliable income generator with a 10-year annualized dividend growth rate of 12.6%.

We plan to add more Costco shares over time. It would be nice to be able to DRIP Costco eventually but that will take A LOT of shares given the low yield.

15. Capital Power Corp (CPX.TO)

Like most utility companies, Capital Power Corp just continues to chug along and generate stable dividend income every quarter. With an initial yield of over 6%, a dividend growth streak of 9 years, and a 10-year dividend growth rate of 6%, there’s a lot to like about CPX.

The only concern I have is the dividend yield is a bit high compared to the rest of Canadian utility companies. It’s probably a good idea to keep an eye on its payout ratio and free cash flow to make sure the dividends are safe.

Having said that, CPX makes up less than 1% of our overall portfolio so if there’s a dividend cut or dividend freeze, we’re not too concerned.

Wrapping Up – 1H 2023 dividend portfolio review Part 1

This is Part 1 of my 1H 2023 dividend portfolio review. I think these portfolio reviews are very worthwhile because they force me to examine our portfolio and write down my thoughts about individual holdings.

Through this exercise, I have identified Bank of Nova Scotia, CIBC, and Algonquin Power & Utilities as ones that we may consider trimming or closing out completely.

On the other hand, I would love to add more shares of Apple, AbbVie, Brookfield Asset Management, Costco, BlackRock, BCE, and BMO as I think these stocks are either at a discounted price or will continue to perform well in the long run.

What do you think about the review so far? Please leave your thoughts in the comments, I’d love to hear them.

Stay tuned for Part 2 of the portfolio review next week.

Curious why you hold both WCN and WM?

Same reason for owning multiple banks and telecoms. Why not own them both if they’re both good companies?

I’ve been using the Beat the TSX (BTSX) as a gauge to assist in the asset accumulation phase. A number of the stocks you’ve considered for divesting are in the BTSX portfolio. While perhaps it’s tempting to sell some of these stocks, and maybe even at a loss, it’s also noteworthy that as of the end of 2022, the 30-year average rate of return using the BTSX method was 12.27%. To put this in context, the benchmark index rate of return was 9.53% over the same time period. I’ve been buying a number of the beat up BTSX stocks to take advantage of their “sale” such as TRP, AQN, T and BCE, but also adding higher dividend growth and industry leader stocks such as TD, CNR, BN, ATD, and IFC.

Btw, I appreciate your posts and find reading them an excellent way to challenge and consider my own investing thesis.

Hi Chris,

Thanks for pointing out BTSX, very aware of this strategy (met Matt in person years ago). It’s definitely a good reminder to think about long term.

Hi!

I have 30k ready to invest – would you suggest putting 10k in an index fund and the rest in dividend stocks?

If you have $30k, I’d suggest purchase one of the all in one EFTs. Build up your portfolio to abut $100k then start investing in dividend stocks if you desire.

Interesting read. I feel in the minority in that I plan to hold AQN for the foreseeable, dripping the dividend, and hoping for better times ahead. Sadly I’m down even further with AP.UN.

(The numbers are seen next to each other when I review my holdings)

My current plan for new investments is to increase my holding of XAW, as it’s done as well as many of my best stocks, and I like the broad exposure that it offers. I rather like having less to track with it,

as it feels very much a buy and hold forever purchase.

That’s our plan with AQN as well but we’ll see how the company does with a new CEO.

XAW is a great choice for diversification.

Excellent report, thanks for sharing your insights as they always help me with my own thinking.

To provide balance to the other comments, I held on to my AQN shares and piled some more on top with the hope that the stock will bounce back somewhat in the coming years. That being said, it’s rather hard to not look at the drop in prices in that sector lately and see an out.

Our Canadian banks have been rather lucklaster in terms of share price growth recently but I’m hopeful about BNS long-term.

As for the number of positions you guys hold, I would say that since you’re still in the accumulation phase, it makes sense to me as it gives you more flexibility to shift things around as needed and reduce exposure.

Looking forward to part 2 of your report 🙂

You’re welcome Oliver. It would be nice for Canadian banks to perform better moving forward. 🙂

I was busy buying last week- FTS, BIP, CM, TRP.

I’m anticipating the taxes on the interest returns of my money market accounts this year will be too high so I’m shifting from cash to tax advantaged stocks .

Thinking of buying telcos like Telus and BCE but I have been scared off by them both having huge debts and both buying a lot of non core businesses like health and vets.

Congrats on your purchases. 🙂

Great review. I haven’t been a DIY investor for too long but have a mix of ETFs and some Canadian dividend stocks for cash flow – plan to retire in year. I took a hit with AQN and sold half, thinking it was a way to hedge my bets. 🙂 It’s been painful waiting for it to recover. Having said that, this year has been tough with Canadian dividend payers, most of them are down across the board. I keep thinking I am buying low so it will be a bonus one day when the stocks recover. I have CIBC and BNS too and they are two of the worst growing stocks, even though they pay a great dividend. I also have RBC, TD, BMO, and NA – so again, it’s a way to capture financials without being wed to one company. It means more stocks to manage, but I decided to buy the top stocks in the Canadian Index funds to avoid paying the MER.

Curious what your thought is on BIP-UN, I also hold some of this Brookfield stock. It’s like many other utilities with a high payout ratio so wondering if this was really the best purchase.

Hi Sandra,

Very interesting that you’re another investor that have sold some AQN. I think BIP.UN should be fine in the long term but I’d go with BIPC for better tax structure.

Bummer I wasn’t aware of that difference when investing. I guess that’s what happens when you are a newbie. I see your point about the withholding tax. Thanks for the tip!

I suppose it really only matters if you’re holding in taxable accounts.

Does the thesis for AQN get thrown out the window with their plan to sell off their renewables unit as they are shifting to be a regulated utilities company?

I sold off my AQN position at a pretty steep loss when they axed the dividend and moved to BIPC and BEPC.

For now we’ll continue to hold AQN and see how things work out.

Good review Bob,

I had also sold my AQN taking my loss and moving on. Figure I will recoup my losses on a better stock faster than waiting for AQN to improve. I had 50 stocks but working my way down 30-35. I believe holding a max 2-3 top stocks in a sector is better than holding many.

How do you make a decision on when to move funds to the US? Is it mostly based on the exchange and if so what would be your max rate?

Jeff

Thanks Jeff, makes sense on AQN. Something for us to consider.

A general observation is that 48 positions is still too many! I agree with others here that dumping AQN and BNS would be a start. And I’d use the proceeds to add to your other holdings in the same category, such as Brookfield Renewable and Royal Bank. I’d also have another look at ABBV. There are some other US pharmas, such as Lilly that are doing a lot better. It’s never a bad move to take a profit from time to time too. For example, since the date of your analysis, Apple is down about $15. Taking some profits in the $190’s would have been a good trade.

I’d be the first one to admit that 48 positions is too many, that’s why one of our goals for this year is to get down to about 45 positions.

As a new reader and fan of your site, I’m curious what were the metrics in selling VZ . I just recently purchased a position due to the dividend. Did I make a mistake?

Hi Steve,

We purchased VZ a while ago and the price just kept going down. We figured the high yield wasn’t worth it given the price performance. Having said that, if you purchased at a low price point, VZ might be a good choice. It totally depends on your entry point. Hope this helps.

I did get a pretty good entry point, so I’ll stay with it a bit. Thanks for all the incredible information you put out. I am hoping to get to 15K in dividends this year! Your site definitely helps.

You’re very welcome.

Excellent report Bob. Cant wait to see parts two and three. I recently sold AQN and purchased VICI.

Not a long track record but regardless of the economy I think folks will always enjoy their one armed bandits! Hoping for some capital appreciation but will enjoy the 5% yield in the interim.

Dont be too quick to sell positions, simply to get down to 20-25. You seem to stay on top of your 48 while enjoying some great diversification.

Keep up the good work

Chuck

Thank you Chuck. Sounds like a lot of AQN shareholders have sold AQN and moved on. We’ll probably end up doing the same thing as some point.

VICI is a great choice IMO.

I sold off my AQN stocks recently and took a bit of a hit. I didn’t like the direction the company was considering. I have also sold off most of my Ponzi stocks (split stocks)–bigger hit but lesson learned! As a new investor with only two years experience I find your discussions very helpful.

Looking forward I have shifted more toward 5.5% GICs with about 40% of portfolio there now. TD estimates about $30,000 in dividends + interest, so I am happy. As a senior pushing toward 80 this will help preserve our savings and provide some growth.

Two stocks from your review I will be considering are BEPC and CPX as they fit my criteria. Thank you for those reviews! 🙂

Hi Dianne,

Interesting you sold off your AQN shares. Sounds like many investors did the same as well.

Congrats on $30k in dividends, that’s fantastic.

Hi Bob:

Thanks for sharing your portfolio holdings. I noticed that you still have AQN. in your list while many have dispose of this or switch to something else. How do you decide when to sell off a stock, or would u buy it back at a lower price? I always have this confusion . Appreciate your thought.

David

Hi David,

Right now the plan is to drip AQN, dollar cost average, and wait for the stock price to recover before we trim a bit of shares.

Have you ever considered a higher yield closed end fun for a small portion or your portfolio Ala eit.un as I added it a few years ago for a stable monthly payout, but I am already semi retired.

That’s something we’ve been thinking but since we do care about total return and we’re still in accumulating phase, it doesn’t make sense to us right now.