Back in late 2017, I reviewed our top 5 long term holdings. Looking back, I was shocked that we used to hold a total of 72 dividend stocks and 2 index ETFs. I will be the first one to admit we owned way too many individual stocks. Since then, we have trimmed our total holdings down to 49 individual dividend stocks and 1 index ETF.

Ideally, we’d like to trim our holdings down to a more manageable number of around 40. If we can enroll in a DRIP for all of these stocks, or as many as we possibly can, that would make our investment life a lot simpler. But this is definitely a work in progress…

In case you’re wondering, we are currently dripping 27 out of 49 dividend stocks (~55%) and also the index ETF, XAW.

Diversification is always a concern when one holds individual stocks. To ensure we have good geographical and asset diversification, we use an ex-Canada international market index ETF, like XAW, to diversify our dividend portfolio.

Over five years ago, I determined that Royal Bank, TD, Vanguard Global All-Cap Ex Canada ETF (VXC), Visa, and Johnson & Johnson were our top 5 long term holdings. Since it has been over five years, I thought it’d be interesting to re-examine which stocks and ETF in our dividend portfolio are considered our top 5 long term holdings. Most importantly, has our list changed since 2017?

Note: By top, it means we don’t ever plan to sell and plan to buy more shares in the future. It has nothing to do with market value/number of shares.

Re-examine our top 5 long term holdings

As I’ve mentioned many times on this blog, we deploy a buy and hold strategy. We identify products that we use on a daily basis and become owners of the companies that make these products. The more people that are reliant on these products or finding it hard to switch from using them, the better. We also like to be curious about the companies we own and regularly examine how they are doing.

Here are the 5 stocks that we believe we can hold for a very long time… like forever!

1. Royal Bank (RY.TO)

First up is Royal Bank, which is the same pick as five years ago. Royal Bank is one of the biggest banks in Canada and has paid uninterrupted dividends since 1870. That’s over 150 years of dividend history!

I like Royal Bank as a long term holding because of the following reasons:

Ask yourself, how many people do you know who switch banks regularly? If you’re like me, you can probably count them on the fingers of one hand. Most people start banking at a financial institution because their parents bank at the same financial institution. Once they are set up, usually it’s very unlikely for them to abandon this financial institution and switch to another financial institution completely. Even if one uses a new financial institution, they’re likely to keep the existing one.

So having 17 million clients means these clients most likely will open a Royal Bank account for their kids when the time comes, increasing Royal Bank’s client base.

Let’s also not forget the simple business model for banks – they take people’s money and safeguard it (and pay a low interest rate), then loan that money to people (at a significantly higher interest rate) to make more money. Royal Bank’s ability to offer a large number of financial services, such as wealth management, and having over 1,200 branches in Canada will enable it to continue growing its customer base.

2. TD Bank (TD.TO)

TD is another pick that was the same as five years ago. It shouldn’t come as a surprise that I really like Canadian banks. I think it’s better to hold Canadian banks individually than rely on a Canadian bank ETF.

Like Royal Bank, TD is one of the largest banks in Canada and has paid uninterrupted dividends since 1857. That’s an even longer track record than Royal Bank! At the current dividend yield of over 4% and the stable dividends, I believe TD’s dividends can almost be considered as bond-like income.

TD has been expanding in the US market and it’s now the 7th largest US bank by deposits and the 11th largest bank in the US by total assets, operating in 15 US states and Washington DC (and after the First Horizon purchase goes through, it will be the sixth largest bank in the US). Basically, TD just keeps getting bigger and bigger. That’s music to any investor’s ears.

3. Apple (AAPL)

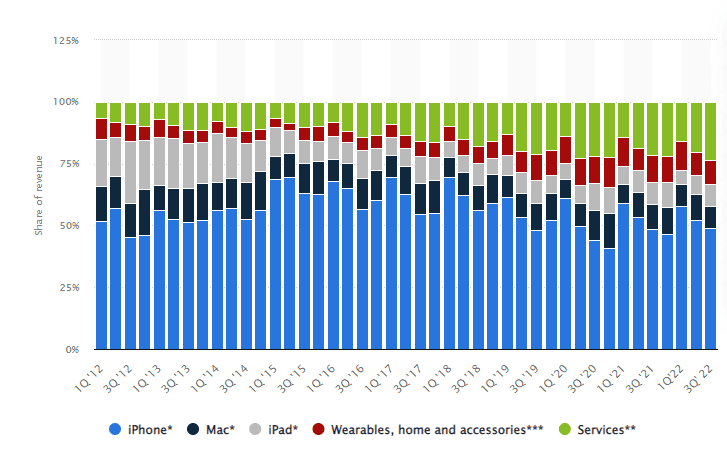

Apple wasn’t on my original list five years ago but I now consider Apple as one of our top 5 long term holdings. Years ago, people used to consider Apple as a one trick pony – generating revenues mostly from iPhones. This was the case over five years ago as iPhone sales were over 50% of Apple’s quarterly revenues.

However, in the last five years, Apple has been generating revenues from other segments of the business, like wearable, home and accessories, and most importantly, subscription services.

In Q3 2022, 23.63% of Apple’s revenue came from services and 9.74% came from wearable, home and accessories.

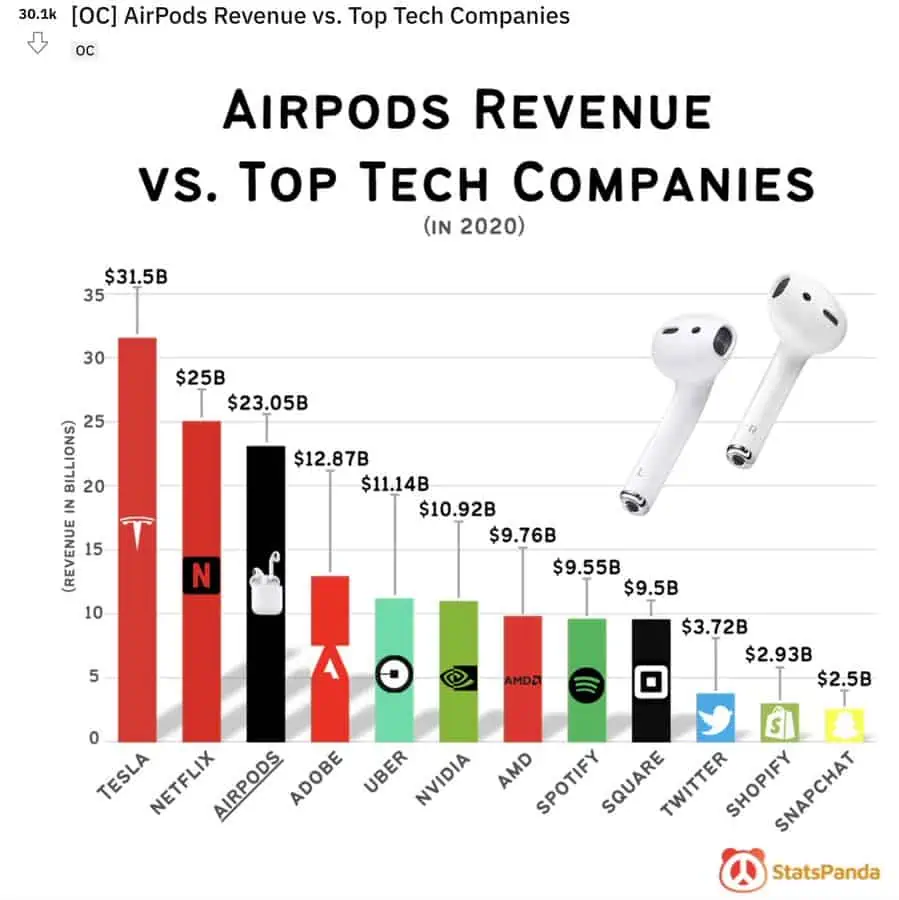

To give you some perspective, in 2020, revenue from AirPods was $23.05 billion, more than companies like Nvidia, AMD, or Shopify!

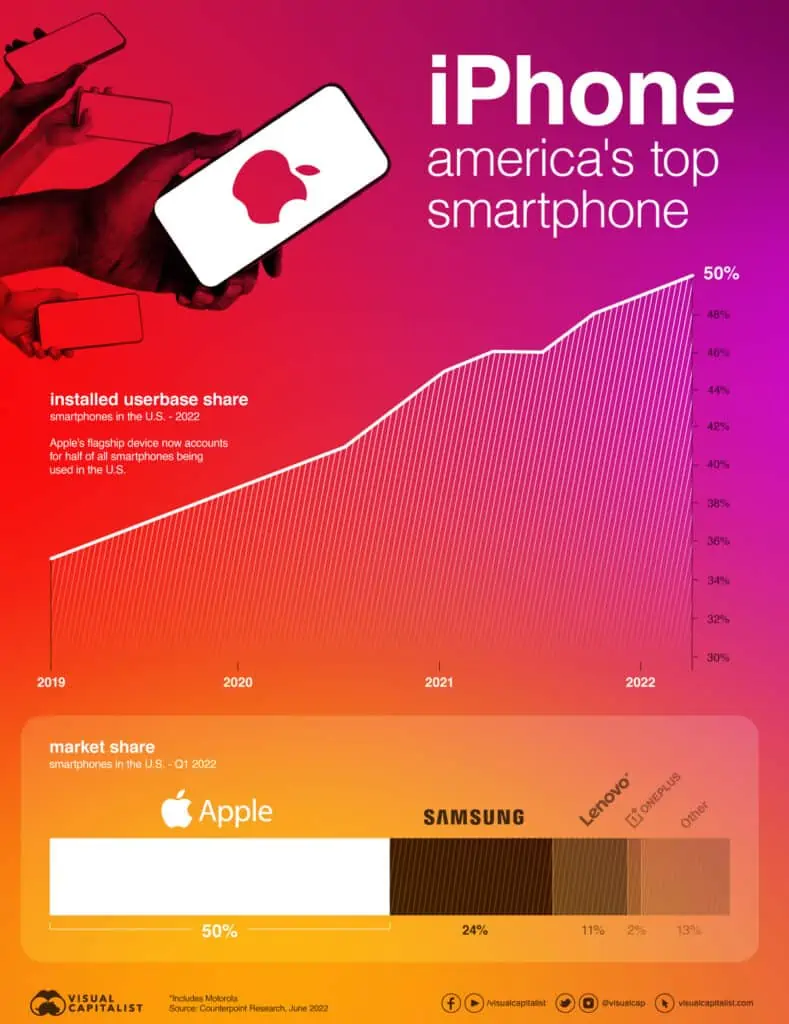

Despite the crazy revenues from AirPods, iPhones are still very important for Apple. In fact, iPhones now make up 50% of the overall installed user base in the US. While riding MRT in Taipei on my recent trip, I noticed most of the Taiwanese transit riders had an iPhone. I was one of the minorities that was browsing on an Android phone. (Shame on me for loving Apple but not owning an iPhone).

What’s amazing about Apple is that they’re able to continue selling their products at a premium. In the third quarter of 2022, Apple’s gross profit margin was 43.26%. Since 2010, Apple’s gross profit margin has never gone below 35%. In comparison, other tech companies like Amazon, Lenovo and Samsung had Q3 2022 gross profit margins of 13.5%, 16.9%, and 14.2% respectively.

Rather than focus on newer and faster technologies on the new iPhone, I noticed Apple is now focusing on safety features like emergency SOS via satellite, and crash detection calls, and marketing them as must-have daily features. Essentially Apple is making the iPhone even more essential in everyday life. Once people are relying for the safety and security of their lives on a product, it becomes nearly impossible to switch to another product. It’s a really smart and excellent marketing strategy!

Like any tech company, one would wonder if Apple will be around in the next 10, 20, or 30 years from now. My best guess is that Apple will continue to be dominant for at least the next 20 years and possibly more as it continues to evolve as a company.

One interesting that I came across the other day is that 87% of teenagers in the US own an iPhone and 88% of teens expect an iPhone to be their next phone. In comparison, back in 2012, only 40% of US teens owned an iPhone. So the younger generations in the US are loving Apple and should continue to help Apple to generate future revenues.

The danger here is that Apple loses its dominance and becomes an old dinosaur like IBM. I don’t see that happening but we’ll have to wait and see.

Five years ago we had Vanguard Global All-Cap Ex Canada ETF, VXC, listed as one of our five long term holdings. Since then we have switched from VXC to XAW, mostly because XAW used to have a lower management fee than VXC.

Vanguard has changed the VXC structure a bit in the last five years, resulting in a lower MER. Despite VXC being 0.02% cheaper than XAW in MER, we do not plan to switch back. If we had $500,000 invested in XAW, the 0.02% MER difference would mean a difference of $100 each year. For us, that’s not worth the time and effort to switch back and forth.

Therefore, we believe XAW and VXC are both excellent ex-Canada international index ETFs to hold for geographical diversification.

Although XAW is already one of the top 5 holdings in our portfolio, percentage-wise, we plan to buy more XAW shares for many years to come.

5. Visa (V)

Thanks to the global pandemic, we’re quickly becoming a cashless society. More and more transactions are done via electronic payments and Visa, being one of the world’s most valuable companies, is front and centre of this payment revolution.

Most people will have at least a credit card in their wallet, and that credit card is most likely to be either a Visa, a MasterCard, or an American Express. In our case, we hold a few Visa cards and definitely prefer Visa and MasterCard over American Express, simply due to more Canadian merchants taking the two former brands.

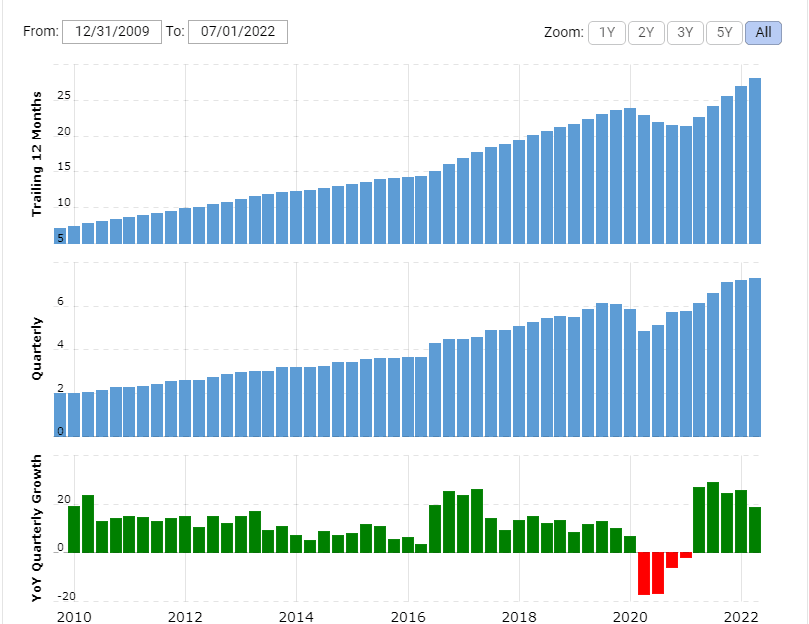

From the charts below, you can see that Visa has continued to grow since 2010. Considering that we will use more electronic payments moving forward, not less, I believe Visa will continue to grow and generate more revenues for many years to come.

Summary – Our Top 5 long term holdings

Although our top 5 holdings have changed slightly compared to five years ago, it doesn’t mean we will be selling the likes of Johnson & Johnson. We still like JNJ, just that Apple has overtaken it from our top 5 long term holdings. We plan to add more shares of these top 5 long term holdings and take advantage of the bear market condition. And the fact that our top five holdings have remained consistent over half a decade only proves we are most definitely boy and hold investors.

Dear readers, what do you think about our updated 5 long term holdings? What are your top 5 long term holdings?

Its a smart move not to own a Apple device. They are way too expensive and its demonstrated by their profit margins. Yes they have some nice features but they dont provide value due to their high pricing. Plus Phones now have become the new cars. Our obsession with new gadgets is mind boggling especially considering the high prices they have reached in the last few years. Apple is good as an investment but not sensible to own their products.

Although I hold the top 6 banks in my portfolio, I’ve recently left BMO and RBC for an online bank. The big banks need to become more competitive. I don’t see the need for bricks and mortar when I can do everything online. Also I own about 40 stocks. I know it’s not what is recommended but I prefer to minimize the risk by not putting too much money into each stock. I appreciate your blog. Thanks for sharing your journey.

Thanks for sharing your top 5 holding.

Could u tell us what’s your current top 10 holdings, and has there been any change over the past 3 years about these holdings? Appreciate that

Please note, these are top 5 long term holdings, doesn’t mean these made up the highest weighing in our portfolio. Sorry if I didn’t make it clear.

Top 10 (not in order)

XAW

Apple

TD

RY

ENB

BCE

NA

CNR

T

COST

You mentioned that you still like JNJ – any concerns with the talc lawsuits they are facing? I have held back on JNJ for this reason….

IMO short term JNJ will be a bit volatile but over long term I think they’ll be just fine.

Good write up and reasons to hold. I have 4 of your 5 top holdings and agree with what you stated.

My top 5 are as follows:

1) Apple

2) TFII

3) CNQ

4) CNR

5) Visa

TFII and CNQ entered the top positions over the last year or so. I plan on holding these companies for a long time.

Makes sense, thank you Dean for your input.

I had the large Canadian banks in my retirement account for many years. TD, BND and RY. All served well and continued to pay dividends despite all the recent and previous economic turmoils experienced. AAPL is another gem for my long haul. Sales climb, sales drop… AAPL is a serious brand sitting on serious cash.

Glad to hear that we hold similar holdings.

Hi,

Love the analysis and explanations as always!! I wanted to ask what your thoughts are on IFC.TO? I first learned about that company when I read about it a couple years ago when you listed it as one of your top Canadian dividend stocks. Since then it seems to have disappeared from your top lists. Just wondering if there’s a reason for that or just that other stocks climbed up on your lists of favourite dividend stocks? Curious to hear what you have to say!!

Keep up the good work!

Hi Brandon,

We’ve held IFC before the financial crisis, it’s probably on my top 10 long term holding, just didn’t make it to the top 5 list.

Hi Bob,

I read every one of your blogs, thank you for all the great info! Will your mix of holdings shift once you retire? That is, the mix of dividend vs. growth stocks?

As retirees, we are living off dividends and keeping our capital intact, but we also own ETF’s for growth. We have been using your stock/ETF picks as a starting point for our research, and it’s working well 🙂

By the way, we don’t own Apple stock, but I’m an Apple believer now! The integration between devices is amazing. I can’t imagine ever going back, just as I can’t imagine ever changing banks.

Thank you Laura, appreciate your support.

A small percent of our portfolio is on growth, no dividend paying stocks. Don’t plan to mix our holdings once we do retire but plan can change.

I like most of your choices. Do you take into consideration the USD exchange when purchasing US listed stocks.

Yes, have to consider currency exchange. Norbert’s gambit when you try to exchange a large sum of money… what we’ve been doing lately is wait till we have enough USD from dividend payout.

If you are holding these stocks “forever” you shouldn’t be too worried about their stock price and overall performance ass long as they are strong performers, as you are never going to sell them. What becomes important is their yield. Apple, XAW and Visa all have lousy yields and you get could do much better with other higher yielding stocks to hold “forever”. Thoughts?

Hi Don,

That’s a good point but you also need to consider capital appreciation and organic dividend growth. The likes of Apple, XAW, and Visa all have higher capital appreciation rate and organic dividend growth compared to some high dividend yield stocks.

You may want to take a look at this article – https://tawcan.com/should-i-invest-in-high-yield-dividend-stocks/

Royal bank 150 years of dividend history

Oops, thanks for pointing that out.