Last week I reviewed 15 dividend growth stocks out of the 48 that we hold in our dividend portfolio.

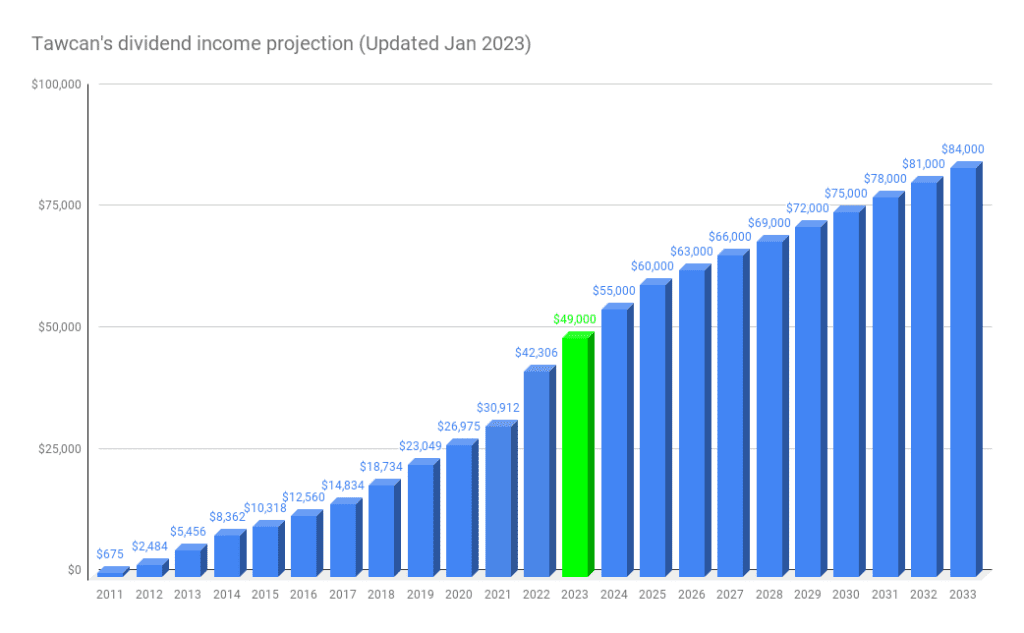

Our dividend portfolio generated $24,685.91 in the first half of 2023. This dividend income growth has been pretty amazing considering ten years ago in 2013 we only received $5,456.20 for the entire year.

Based on my current dividend income projection, we are on track to receive over $49,000 in dividend income for 2023. We are definitely on track with our annual dividend income projection per the chart below.

Let’s continue reviewing the rest of the holdings, shall we?

1H 2023 dividend portfolio review – Part 2

As stated previously, I’m not going to sugarcoat anything with my review. I want to be honest with myself and provide readers with my thoughts and what I’m thinking about each holding.

16. Canadian Tire (CTC.A)

I’ll be the first one to admit that I don’t understand why we Canadians love Canadian Tire (I must be in the minority). Every time I go to a Canadian Tire store, I feel the store is poorly lit and that there is too much merchandise. I often lose my way in the store – and I bet that I’m not the only one!

For whatever reason, Canadians continue to shop at Canadian Tire and the company keeps making money. Canadian Tire does own other brands like SportChek, Mark’s Helly Hansen, Party City, and Atmosphere so the company is well diversified in the retail sector, attracting different types of customers.

Last week, Canadian Tire had very disappointing quarterly results and saw the share price drop by more than 4.5%. How bad were the results? Canadian Tire reported lower than expected profit and revenue and withdrawn a three-year financial forecast. The CEO, Greg Hicks, stated that due to inflation and higher cost of living, Canadians aren’t spending as much on discretionary items.

Is this a turning point in the Canadian economy? Are we going to see other Canadian retailers suffer?

It is highly possible.

At this point, we’re re-evaluating our plan for our Canadian Tire shares. We are sitting at a decent gain so we may close out the position and investing the money elsewhere. We may, however, just keep the shares and continue to collect dividends and wait for the share price to recover.

17. Dream Industrial REIT (DIR.UN)

Although we really like the industrial REIT sector, DIR hasn’t done much in terms of stock price appreciation over the last three years and there has been zero dividend payout growth since March 2013. Therefore, Dream Industrial REIT is definitely one of the stocks we’d consider selling and reinvesting the money elsewhere.

DIR.UN’s share price performance has been decent in recent months. With the higher interest rates, hopefully, the share price will continue to climb for a bit and allow us to sell high – if we were to close this position.

18. Emera (EMA.TO)

In terms of share price performance, Emera has done poorly in the last year. But the high dividend yield allows shareholders like us to wait for the price to recover.

Like most utility stocks, I don’t expect Emera’s share price to explode. What I’m expecting is a stable dividend income and slow share price growth. Emera is meeting both of those expectations.

19. Enbridge (ENB.TO)

Enbridge is one of the top ten positions in our dividend portfolio. In June we dripped 36 Enbridge shares and increased our forward dividend income by $127.80.

Given that Canadians still rely on oil and natural gas daily – and are likely to do so for at least the next couple of decades – and it’s harder and harder to build new pipelines due to environmental concerns, Enbridge’s existing 192,000 miles of pipelines are now more valuable than ever. In short, Enbridge satisfies one of Warren Buffett’s chief requirements of a “good” stock – a wide moat.

Enbridge is a high-yield dividend stock and the company has rewarded its shareholders with a solid dividend growth rate (11.6% annualized dividend growth for the past 20 years).

Many people are concerned that Enbridge won’t be able to continue paying its dividends. But from what I can calculate, Enbridge has sufficient cash to both continue paying dividends and raising them. We plan to continue to hold Enbridge for the long term.

20. Fortis (FTS.TO)

With a 49 year dividend growth streak and a 7.8% 20-year dividend growth rate, Fortis is as steady as you can get when it comes to dividend growth stocks.

I have absolutely no concern with Forits. It’s a boring stock and it should remain boring.

21. Granite REIT (GRT.UN)

As mentioned, I like the industrial REIT sector a lot. If we look at Granite REIT’s share price performance over the last five years, we’ll see that it’s relatively flat.

But unlike many REITs, Granite REIT is one of the few REITs that has raised its dividend payout consistently. With a 12-year dividend growth streak and a 4.5% annualized dividend growth rate over the last 10 years, I consider Granite REIT a stable dividend payer.

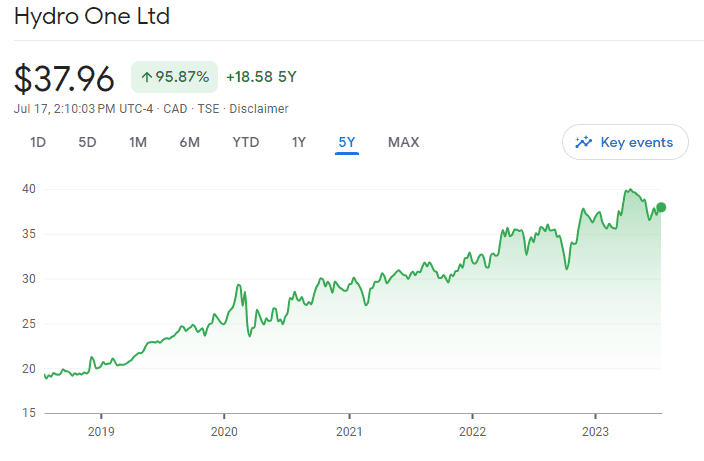

22. Hydro One (H.TO)

No concerns with Hydro One. The position makes up less than 0.5% of our portfolio so it’s a very small position. The stock has seen solid performance in the last five years.

Just like other utility stocks, Hydro One is one of those boring stocks with a stable dividend income. The only concern would be with potential government regulations that may impact how Hydro One operates. This is something to keep an eye on for any utility company.

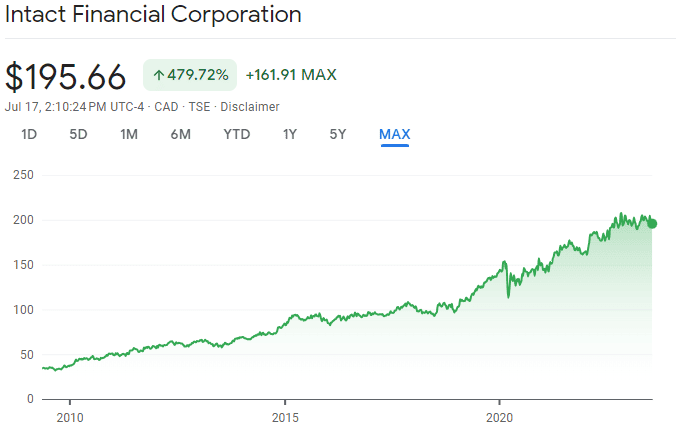

23. Intact Financial (IFC.TO)

Intact Financial is the first dividend stock that I ever purchased. Despite the stock dropping significantly during the financial crisis, I didn’t sell.

Since then, the share price has done quite well and the company has been raising its dividend payout consistently. We are happy to hold IFC and wished we had purchased more shares in the past to allow us to enroll in DRIP.

Intact Financial is definitely a keeper for us!

24. Johnson & Johnson (JNJ)

Johnson & Johnson completed its consumer health division spinoff in May, creating a new company called Kenvue. The “new” Johnson & Johnson will focus on medical devices and technology and pharmaceutical products. Having more focused business segments can be a good thing for the company.

As Johnson & Johnson owns nearly 90% of Kenvue shares, JNJ recently announced its shareholders will be able to swap their shares for stocks of Kenvue. While the information is still limited, we probably will just keep holding JNJ shares rather than swapping for Kenvue shares.

While the share price hasn’t performed well the past year, I have no doubt JNJ will do just fine over the long term. After all, JNJ has a 61-year dividend increase streak with 10-year dividend growth rate of 6.36%. This is a stock that every dividend growth investor should hold.

25. Coca-Cola (KO)

Coca-Cola is one of the largest holdings of Warren Buffett’s Berkshire Hathaway. While our Coca-Cola holding isn’t nearly as large, we are dripping one share each quarter and slowly increasing our position.

The company is facing some short term challenges that many consumer goods companies are facing in the high-inflation market. However, because people are “addicted” and many of them are loyal to Coca-Cola products like Coke, Fanta, Minute Maid, Costa Coffee, and Vitamin Water, they will continue to consume these products.

Therefore, I’m confident that Coca-Cola will continue to be profitable in the long run.

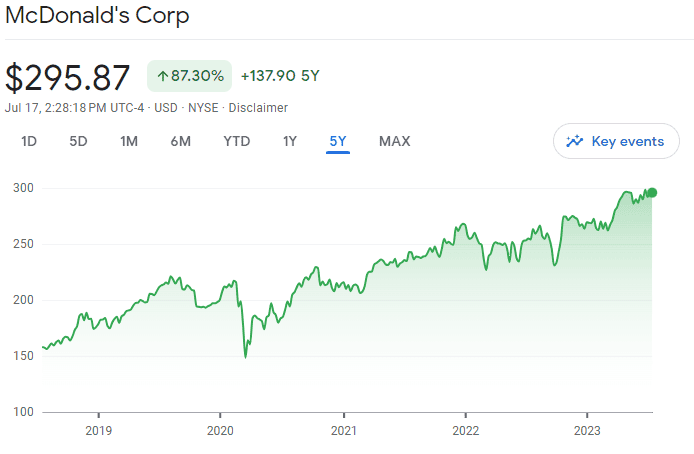

26. McDonald’s (MCD)

A few weeks ago we drove past a McDonald’s and both kids asked why people don’t just demolish all McDonald’s stores because the food is junk (we don’t eat at McDonald’s). I then quickly reminded them that we own McDonald’s shares because people will continue to eat at McDonald’s despite the fact that the food isn’t exactly nutritious (This same rationale is why we also hold Coca-Cola and PepsiCo stocks).

While the food items aren’t great for your body, you can’t argue with the stock performance nor with the dividend history of McDonald’s.

27. Manulife Financial (MFC.TO)

Manulife’s price performance has been pretty poor over the last five years as you can see below. The above 5% dividend yield does make up for the poor price performance a little bit. (in the sense that you’re being ‘paid to wait’ while hopefully the stock price appreciates).

Insurance companies usually do well in a high interest-rate environment, we’ll see if MFC can turn it around. Manulife is facing some headwinds in the Asia Pacific area though.

Since we’re focused on total return rather than purely on dividend income, if Manulife share price continues to stay flat, it may make sense to trim some MFC shares and reinvest the money elsewhere.

28. Magna International (MG.TO)

Magna International has taken quite a bit of a hit since the Russian-Ukraine war started. Magna is the fourth-largest automotive parts supplier globally and supplies many of the components for many new EV models.

Since MG makes up less than 0.1% of our portfolio, we aren’t too concerned with the poor price performance. We plan to continue to hold MG shares, collect dividends, and wait for the stock price to recover. Once the price recovers a bit, we would potentially consider closing out our MG position completely and reinvesting the money elsewhere.

29. Metro (MRU.TO)

The Canadian stock market is financial and energy-heavy. Metro is one of the few Canadian consumer staples and consumer discretionary dividend paying stocks available.

Metro makes up a very small percentage of our portfolio. The stock has done relatively well over the last five years, returning over 60%. People will continue to shop at Metro stores for groceries and day to day items. Metro can easily raise prices to combat the high inflation rate. Despite the high inflation, Canadian grocery store brands like Metro have been seeing historical profitability.

We will continue to hold Metro shares for diversification purposes.

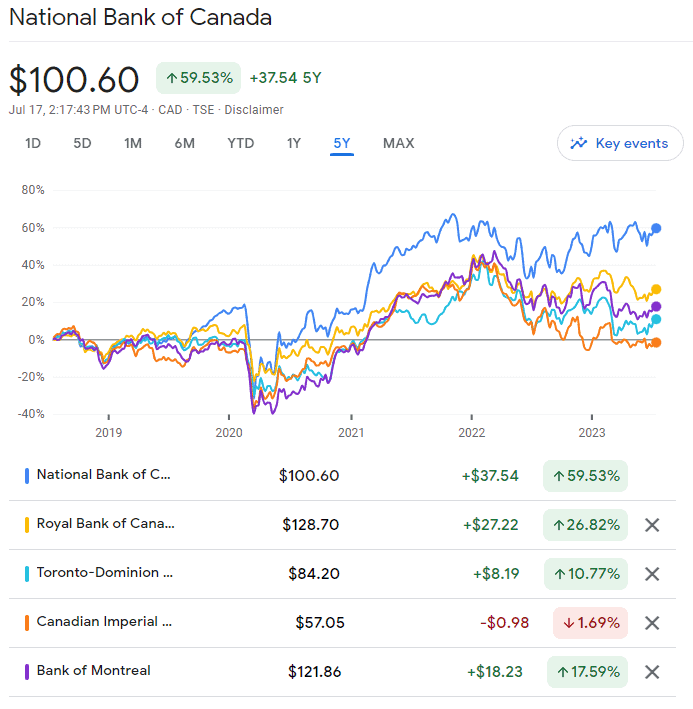

30. National Bank of Canada (NA.TO)

National Bank has performed quite well compared to its peers over the last five years, despite a much lower dividend yield.

Remember, total return matters. I prefer both our capital and dividends to grow over the long term.

NA is one of our top ten holdings and we are happy about the solid performance in the last five years, in addition to consistently raising dividend payout.

Being a smaller bank compared to the other Big Five Banks, NA may potentially have more growth in the next few years. If NA decides to bid on Laurentian Bank, this will give them more customer base, especially in Quebec.

We definitely plan to add more NA shares.

31. PepsiCo (PEP)

We added PepsiCo a few years ago to increase our exposure to the consumer staples sector. Since then, Pepsi has done relatively well and it’s one of those stocks we can just leave on auto-pilot knowing the company will continue to generate billions of revenues each quarter.

Recently PepsiCo posted an earnings beat. Its earnings per share came in at $2.09 vs. $1.96 predicted and the revenues came in at $22.32 billion vs. 21.73 predicted.

What caught my eyes was the fact that despite the decrease in beverage sales volumes, PepsiCo was able to offset that drop in revenues by raising prices. For 2023, PepsiCo expects a 10% organic revenue growth, up from its previous forecast of 8%. This all very good news to shareholders like us.

Compared to Coca-Cola, PepsiCo is a smaller position in our portfolio. We don’t have enough shares to enroll in a DRIP yet but it is a goal we have.

Wrapping Up – 1H 2023 dividend portfolio review Part 2

This is the second part of my three-part 1H 2023 dividend portfolio review. In this Part 2 of the portfolio review, I analyzed 16 more dividend paying stocks.

Some of the stocks that I believe we can either close out or trim are:

- Dream Industrial REIT

- Manulife Financial

- Magna International

We will have to closely monitor these stocks for potential opportunities to unload or trim them.

On the other hand, we would love to add more shares of Coca-Cola, PepsiCo, and National Bank. All three of these stocks, I believe, will continue to generate revenues and be very shareholder friendly by raising dividend payout each year.

What do you think about part 2 of our dividend portfolio review so far? Please leave your thoughts in the comments, I’d love to hear them.

Stay tuned for Part 3 of the portfolio review in two weeks (gotta post the monthly dividend income report first).

Good commentary on your thought process. I’ve been adding to MFC – but I’m more on the income phase nowadays. On part 1 – I’ve been considering sales of CM and BNS which are now more likely. (I did add to my PEP holdings last week).

Re: your aversion to GICS, if I understand your tax law correctly, if they’re held in registered accounts, there’s no tax ‘penalty’. Perhaps the deeper reason is to get a decent return requires a 1-2 year commitment as opposed to the 5.3%-5-5% rate available on 3-month CDs here in the States (available in registered accounts as well)?

If you’re on the income phase, makes sense to add more high yield stocks. Interesting that you’re considering selling CM and BNS giving they’re high yield.

You’re correct that there’s no tax penalty when you invest GICs inside a TFSA, but my argument is that you’re losing potential upsides from stocks. But if you need the money short term, GICs make sense.

True they are higher yield, but both hold an ancillary position in the portfolio (< 1%). Over the years I've accumulated 156 positions so paring this number is my first priority. MFC is one I've selected to retain and raise to a 3% position for the same reason you identified – the historical performance in a high interest rate environment. So losing 6.6% and 6.95% positions while increasing a 6.1% position with greater upside potential (assuming Asia doesn't hurt them too bad) isn't a bad trade-off in trying to get to about 80 (fewer but larger) positions.

That’s a lot of positions. 🙂 Makes sense to trim a bit.

HI Bob,

I love reading your analysis with a no nonsense approach. I was evaluating about fixed income instruments for my RRSP investments. A 2 year GIC is paying close to 5.3% and a 5 year GIC is about 5%. Under the current circumstances what’s your take on GIC vs Dividend Growth Stocks.

Hi Swami,

That’s a very good question, I have covered this topic in a previous post – https://tawcan.com/random-thoughts-on-the-market/

I agree with your decision on possibly selling Dream Industrial. I have nothing against the company itself, but I avoid reits for the reason that it’s difficult (not impossible) for them to grow their dividends and they usually tend to be slow growth in capital appreciation (in general). Good if you need the income now, but if you are still long away from FIRE, I find it’s not worth having them or at very least limit them to a small position in a portfolio.

Thanks for the update.

You hit the nail there. While REITs are good with high yield, they typically don’t grow their dividends so that can be a problem if you want to organic dividend growth.

I have avoided REITs because I don’t see the long term value and I’m already overweight with real estate owning a home in Toronto. Given that you have a house in the Vancouver area, I suspect a big chunk of your net worth is already in Real estate so you likely don’t need more. Just a thought

That makes a lot of sense. Definitely something to consider.

I have many of the same stocks, Canadian Tire being one of them. What’s interesting is their mix of retail, real estate and financial services. Their credit card is a going concern in Canada along with their loyalty program. Even if their retail segment struggles, they have property they can rent or sell for future development (housing). I see them as a staple and don’t have a plan to sell even though their down right now.

That’s a good point about Canadian Tire has a good mix of different services.

Hi Bob,

As a dividend growth investor, I like a mix of medium yield (around 4%), medium growth (around 5%) and low yield ( 8%) stocks. Metro (MRU) is one of them. I also have Alimentation Couche-Tard (ATD) and Transforce (TFII) in that latter category.

I know you want to reduce your number of positions, but these two deserve to be on your watch list.

Looks like my comment copy&paste was mangled…

First sentence should end with: “low yield ( 8%) stocks”.

“low yield (less than 2%), high growth (greater than 8%) stocks”

The “less than” and “greater than” symbols seems to have been interpreted as HTML delimiters and every characters in between were deleted/filtered out.

Yes, makes sense to have a mix of different yield/growth dividend stocks in your portfolio. 🙂

I think the pandemic has greatly influenced how we shop and this is having a major influence on companies like Canadian Tire. The creative influence of Amazon shopping has influenced the way we shop. The price of gas has also made a significant hit on the cost of shopping.

During the pandemic we ordered our food via the internet (Quality Foods) and picked it up without going in the store. Very convenient and I found many interesting products I was unaware of. They temporarily stopped this program and recently announced they will be expanding the “shop on line” in 2024. I won’t have to push a cart around 17 isles and take an hour to do it.

Also banking online has changed considerably in the last 3 years. No more writing checks for bills! Many fewer employees will be required.

Connecting all the dots provides the foundation for future decisions in stock choices.

Keep up the good work Bob!

Hi Dianne,

Very good points on how the pandemic has greatly influenced how we shop. I’d argue that some things people prefer shopping in stores rather than online.

Much appreciated summary of the holding and food for thought as I hold many of the reviewed positions

You’re very welcome Denis.