A few weeks ago, Henry from “Your Every Growing Income” posted a questionnaire for income investors and tagged me and a few other dividend investors on Twitter. Rather than answering the questions via a comment or tweets, I decided to write an extensive post instead.

Let me set the record straight before starting; we are not pure dividend investors and we are not pure index ETF investors either. Long-time readers will know that we hold both dividend-paying stocks and index ETFs in our dividend portfolio. We are unconventional, we are hybrid investors.

Why do I take this somewhat unconventional approach? Well, I like the predictability of dividend-paying stocks when it comes to dividend income. I know exactly how much we will get paid every pay period and can estimate our monthly dividend income accurately. I also like that dividend-paying stocks, in general, are extremely tax-efficient and can keep up with inflation.

On the other hand, I like index ETFs for tax efficiencies, sector diversification and most importantly, geographical diversification. It is simply not possible to own many well-run, highly profitable international stocks because they aren’t listed on the Canadian or US stock exchanges.

In case you’re wondering, I stumbled onto dividend growth investing around 2007, just before the financial crisis and didn’t start getting serious on dividend growth investing and index ETF investing until 2011. Thanks to a shift in focus and increasing savings rate, we have been able to go from less than $100 per year to close to $15,000 so far in 2019.

Having over 10 years of investing experience, I thought Henry’s questions were very interesting. Here’s my attempt to answer them.

1. Which stocks should you buy and why?

For dividend growth investing, I like to buy companies that produce products that I use on a daily basis. The more dependent I am to these products, the better. So companies that provide services like banking, utilities, telecommunication, insurance, food, drugs, waste removal, etc. are great to consider.

When I started with dividend investing, I was focusing a lot on high yield stocks. What I didn’t realize is that while high yields are great, some high yield stocks aren’t sustainable. Furthermore, high yields typically mean a much lower organic dividend growth each year.

Nowadays, I like to focus on companies that have a long history of increasing their dividends. I also focus on a handful of companies that have high dividend growth rates. If you look at our dividend portfolio, you will notice that we hold a mix of high yield, lower dividend growth and low yield, higher dividend growth stocks. As we invest more and more money, I have been focusing more and more on low yield, higher growth stocks because I want our dividend income to grow organically once we stop adding fresh capital each year.

Since I’m a Canadian, I invest in many of the top Canadian dividend-paying companies. The Canadian economy is very financial and energy focused, so our top holdings definitely contain most of these top Canadian financial and energy companies. Having said that, we do hold many US-listed dividend-paying stocks for diversification purposes. Generally speaking, you can find more dividend-paying stocks in the consumer staples and consumer discretionary sectors in the US market than the Canadian market.

For more info, you can check out how I typically short-list the stocks.

2. How should you evaluate the merits of the stocks you are considering?

I have written about how to start investing in dividend-paying stocks. I have also composed two FAQ’s on dividend stocks and index ETFs (FAQ1 and FAQ2). If I am considering a new company that I do not really know, I also like to take a look at their annual and quarter reports.

For the most part, you can evaluate the merits of the stocks you are considering by doing a quick research on Google Finance, Yahoo Finance, or Morningstar by looking at the following criteria:

- Dividend growth history: The longer the dividend growth history a stock has, the better.

- Dividend Yield: I like to select stocks with higher than 2.5% dividend yields, but high yields may be a warning, depending on the company. The key is to make sure the yield is sustainable, which is why we look at the next parameter, payout ratio.

- Payout ratio: Payout ratio is a good way to determine whether the dividend payments are sustainable. Payout ratio is calculated by taking the dividend distribution amount divided by earnings per share. If the payout ratio is close to 100%, that’s usually a warning sign. A word of caution, since REITs typically distribute 70-90% of their earnings, you cannot use DPS/EPS to calculate payout ratio. You need to examine the funds from operation (FFO) or adjusted funds from operation (AFFO) to calculate the payout ratio, rather than EPS.

- Annual dividend growth rate: How much did the company raise its dividend payout for the past year, the past 3 years, the past 5 years, and the past 10 years? If a company has an above 15% dividend growth rate for the last 10 years and has continued this high growth rate, I may ignore the initial 2.5% yield requirement I have.

- PE ratio Historical PE ratio: I like to invest in stocks with lower than 20 price to earnings ratio. The lower the PE ratio, the better, but PE ratio is going to be different depending on the different sectors. For example, Canadian banks typically have PE ratios of around 10-12 while most US consumer staple companies usually have PE ratios closer to 20. If I’m comparing two stocks in the same sector (say Royal Bank and TD), by looking at the PE ratio, I can quickly tell which stock may be more attractive. In addition, I also like to take a look at the historical PE ratio of a stock and compare it to the historical PE ratio data to see whether the stock price is expensive or cheap. Another way to look at PE ratio is how long it will take for the company’s earnings to add up to your original purchase price.

- PEG ratio: While I care about dividend income, I also care about stock price appreciation. I like to take a look at the PEG ratio of the stock to determine what analysts’ estimates are for the future growth of the company. The lower the PEG ratio, the better.

3. When should you invest more money into new stocks or the ones you already own?

When I was building up our dividend portfolio, I would usually invest money into new stocks to increase our sector diversification. With over 60 stocks and two index ETFs in our dividend portfolio today, I would say we probably can reduce the number of stocks that we own. So lately I have been adding more money into the ones that we already own.

When do we invest more money into new stocks or the ones we already own? When I deploy more cash, I like to wait for a small correction in the market. So I usually buy stock shares when the market is red. A rule of thumb is that I do not let any single position exceed 5% of our overall portfolio.

4. When should you sell your stocks

It’s pretty rare for us to sell our stocks but it can happen and I have outlined this on the blog a few times. If a company cuts or eliminates its dividend, usually that would trigger a sell for me. Another reason for selling the stock would be if the company has changed its core and its losing key competitiveness that made the stock attractive in the first place. For example, if Apple were to stop making new iPhones, Watches and Macs, and start manufacturing toilets, that probably would trigger a sell for me.

Recently we did a dividend portfolio house cleaning and closed out four positions. You can view the various rationales in the post.

5. Should you be worried when the market and prices are going down? Why?

If you are worried and losing sleep over the day to day market drop, you shouldn’t be investing in the first place! Before investing, you should really be asking yourself these three key questions. The money that we use for investing is money that we do not need in the short term. So in some way we are OK if the value of our dividend portfolio decreases by 50% or more. We can live with the potential downside and we can continue adding capital into the dividend portfolio to purchase more shares or add new positions.

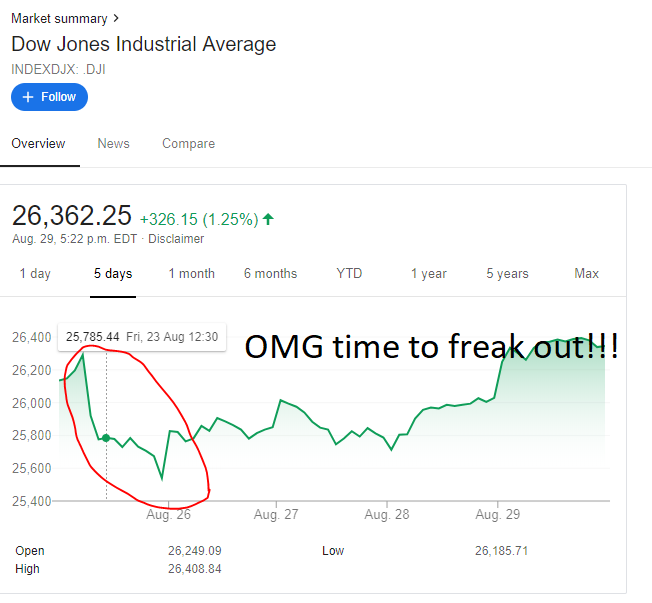

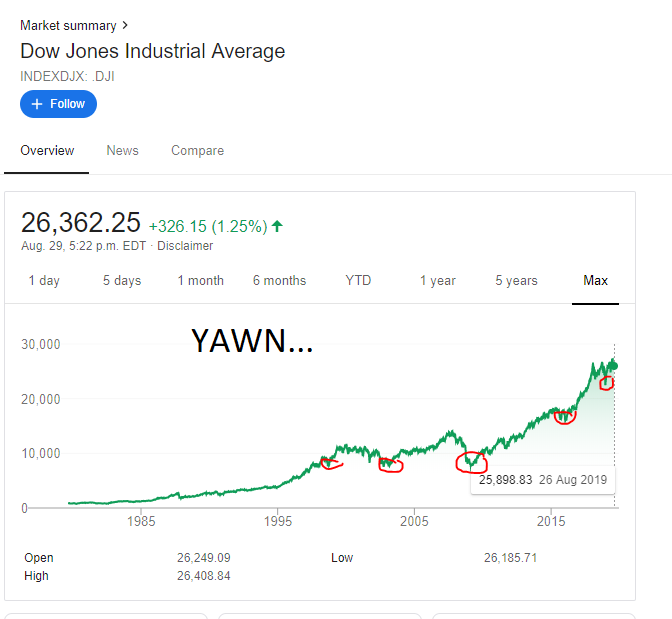

The reality is, the market and stock prices will go up and down every day. That’s how the stock market works and it’s not something you or I can control. Rather than freaking out over the day to day market performance, remember to step back and look at the bigger picture. Remember that over the long term, the stock market has an annual historical return of 7%. And when you zoom out the chart, that 10% market drop will be a small blip in the chart as you can see from below.

6. Should you diversify into other stocks, sectors, and markets?

In general, I think diversification is a good thing, that’s why we use index ETFs to provide us with some geographical diversification. Sector diversification is also a good idea. Putting all your eggs in one basket can typically lead to very bad results when things go bad. Can you imagine investing only in US banking stocks just before the financial crisis? Ouch!

Having said that, I would be careful diversifying into a brand new sector or untested market like cryptocurrency for example.

7. Should you worry about Asset allocation and rebalancing? Why?

For the most part, we are fully invested in stocks. We do own a small percentage of bonds through my work’s RRSP. Given the current low interest rate environment, I don’t believe investing in bonds makes sense given that we are in our mid 30’s. Don’t get me wrong, I do believe that bonds can help smooth out the bumps during market volatility, but I think bonds are more helpful when we are older.

We don’t rebalance our dividend portfolio in the traditional sense that one would rebalance their portfolio which consists of index ETFs. As mentioned, we try not to let any single position exceed 5% of our overall portfolio. If a stock is performing well and exceeds the 5% composition, then we usually reduce the percentage by adding shares of other stocks in our portfolio.

8. Should you worry if your stocks don’t perform as well as the market? Why?

If you want to keep it simple, index ETFs are the way to go. You are essentially tracking the market, minus the fees.

Unlike some dividend growth investors, I monitor both the dividend income and portfolio value. My key focus is the dividend income, as we want to eventually live off our dividend income. Having said that, I do want our portfolio to at least keep up with the market performance because we may eventually tap into our principal in the long term.

The way our portfolio is structured, we own the top 10-20 dividend-paying stocks that the different index ETFs hold, so we really should be able to track to the market. Fortunately, our dividend portfolio has outperformed the TSX for the most part.

9. When should you invest in ETFs, mutual funds, Bonds, and GICs?

We definitely invest in index ETFs for diversification reasons. I own low MER mutual funds and bonds via my work’s RRSP because index ETFs aren’t available. We used to own GICs but no longer own them.

Whether you invest in ETFs, low MER mutual funds, bonds, or GICs is an individual decision. If you need the money in the short term but don’t want to hide it under your mattress, GICs and/or money market may be good investment options to park your short term cash.

10. How do you determine how well your stocks are performing?

I had outlined this in this post. Basically we track our net worth every quarter and how much new capital we have added. I can easily calculate the total return in an Excel sheet and compare the portfolio performance with the market performance.

Final Thoughts

I had a lot of fun answering these questions and I hope you have found them useful. Thank you Henry for the invite to the questionnaire. It has been interesting reading the answers of other dividend growth investors to learn a few things. If you have any questions, feel free to ask in the comment section or contact me.

hello, where is your newsletter feed gone?

Would be good to see how your portfolio performing during covid-19

No the newsletter feed is still available. You’re currently not signed up on the Newsletter.

Hey, Bob! Thanks for sharing it.

A question: which are the three or five best books on dividend investing in your opinion?

Thanks!

You can take a look here:

https://tawcan.com/resources/

Good article Bob. I agree with your take on Bonds. I did an article showing that many investors have way more diversification than they realize, especially if they have pensions. For example: CCPIB invests approximately 85% of their $400 Billion outside of Canada. They also have more fixed income assets then they realize. My personal investments are all stock and Equity ETF for this reason. Currently my equity portion of my income is 23% and my fixed income is 77% and I don’t hold ANY bonds or GIC’s.

Thank you Gruff403. In the low interest rates environment, I see better ways to invest my money than bonds and GICs. 🙂