Long time readers will know that we plan to reach financial independence via dividend and ETF investing. Our goal is building up our dividend portfolio and dividend income so one day we can live off dividends. When this happens, we can call ourselves financially independent.

Given that dividend investing is one of our core investing strategies, we frequently analyze dividend paying stocks by keeping a divided scorecard so we can keep track of our investment. I also have been updating the best Canadian dividend stocks list regularly to see which stocks we can potentially add more shares to.

Best Canadian Dividend Stocks

Mrs. T and I are certainly not the only dividend growth investors in the world. There’s a big and diverse dividend growth investing community in Canada, the US, and other countries with very supportive people. It’s always nice to talk to other like-minded people, share investing ideas and learn from them.

Recently, I reached out to several dividend growth investing (DGI) bloggers and asked them to pick three of their favourite Canadian dividend stocks based on total growth (i.e. a combination of growth, dividend growth, or both). Let’s see whether their picks mimic my list of best Canadian dividend stocks or not.

If you already own dividend stocks and want to create a spreadsheet to track your portfolio, take a look at my Google Spreadsheet Dividend Portfolio Template.

Dividend Growth Investing Bloggers

Before we go through each pick and the analysis, I’d like to introduce the DGI bloggers that were gracious enough to provide their three favourite Canadian dividend stocks.

I really appreciate their picks, because without them, this Best Canadian dividend stocks round up post wouldn’t have been possible.

Freedom Thirty Five

Liquid from Freedom Thirty Five Blog reached financial independence last year and has been utilizing a similar investment strategy as me. I had the pleasure of meeting Liquid in 2019 when I organized a local personal finance bloggers meet up.

The Dividend Guy

Mike blogs at The Dividend Guy Blog and is the founder of Dividend Stocks Rock. Given Mike’s long investing history and experience, I thought it would be interesting to see what he picked as the top Canadian dividend stocks.

Another Loonie

Another Loonie is a fellow Vancouverite, although I haven’t had the chance to meet him in person yet. Loonie is 28 years old and has $350k in net worth. Very impressive stuff!

Simply Investing

I met Kanwal in person a couple of times. A seasoned dividend investor, Kanwal runs Simply Investing where he demonstrates ways to have your money work for you, so you don’t have to. I was very curious about Kanwal’s picks for the top Canadian dividend stocks.

Passive Canadian Income

Rob is the brain behind Passive Canadian Income, one of the blogs that I have included in my ultimate Canadian dividend blogs directory.

All About The Dividends

Matthew from All About The Dividends has been an active member of the Canadian DGI community. I had the pleasure of talking with Matthew a number of times during the Canadian blogger virtual video calls throughout 2020.

Dividend Earner

Dividend Earner hails from the metro Vancouver area and has been a long time dividend growth investor. Before making his top three Canadian dividend stocks, Dividend Earner has the following statement to make:

“First, I am not so much as to invest for short term annual gain but I believe these companies can benefit from a recovering economy as they have not yet bounced to new highs like many others. The holdings are primarily dividend growth for overall total return and not for income in retirement. The idea is that once you near retirement, you can swap to higher income investments.”

My Own Advisor

I had the pleasure to meet Mark from My Own Advisor a few times. We both utilize the hybrid investing strategy and share similar investing philosophies. We shared a hotel room at FinCon 2019 and spent a lot of time talking about investing and blogging.

Mr. Tako

Since the DGI community is a small one, I decided to reach out to some non-Canadians to see which Canadian dividend stocks they might like. I asked Mr. Tako from Mr. Tako Escapes to pick out three of his favourites. I had the pleasure to meet Mr. Tako and Mrs. Tako in person when we went down to Washington State a few years ago.

Gen Y Money

GYM from Gen Y Money is another blogger from Metro Vancouver. She has been in the personal finance community for a long time as she was formerly known as Young at Young and Thrifty.

FI Garage

Money Mechanic, The Accountant, and The Economist from FI Garage were kind enough to submit their three picks for the best Canadian dividend stocks. I think The Economist may have had a few too many beers with his initial pick though….

Dividend Growth Investor

Dividend Growth Investor has been blogging since 2008 and has provided great insight and analysis on dividend stocks. For his picks for the best Canadian dividend stocks, Dividend Growth Investor decided to ask his readers about their favorite Canadian companies. He compiled a list of the companies mentioned more than once, and ended up with the three most popular Canadian companies.

Dividend Investor

Dividend Investor is a fellow Canadian that has produced some really awesome investment videos on Youtube. Make sure to check out his videos.

Get Rich Brothers

Rick and Ryan from Get Rich Brothers focused their picks on high-quality companies with reliable dividends that can be trusted to increase. The three top Canadain dividend stocks that they picked provide vital services that our society can’t operate without.

Cheesy Finance

Although Cheesy Finance is in the Netherlands, they have close ties with Canada. So I gave them a challenge and asked them to pick three Canadian dividend stocks that they like.

Settling Nomad

Mr. R and Mrs. M from Settling Nomad are originally from India and immigrated to Canada in 2013. They are using the blog to write about their pursuit of financial freedom.

Cut The Crap Investing

Dale from Cut the Crap Investing has been on a mission to help Canadians to discover low fee index investing. Although an index investor at heart, Dale has also been investing and analyzing in dividend stocks and cryptocurrencies.

Best Canadian Dividend Stocks – A round up from the DGI community

Please note, these picks are from fellow bloggers in the DGI community. None of us are professionals and the picks are simply opinions. Please use this list merely a suggestion.

Please always purchase dividend paying stocks based on your own research.

Alimentation Couche-Tard (ATD)

Alimentation Couche-Tard (ATD.B) was picked by six DGI bloggers and came out ahead as the best Canadian dividend stock. This shouldn’t come as a surprise given the large store presence, a low payout ratio, and a solid dividend growth history. Here are the analysis and reasonings for picking ATD.B.

- Sector: Consumer Defensive

- Dividend Yield: 0.92%

- Dividend Payout: 10.8%

- PE Ratio: 11.78

- 5 Year Dividend Growth Rate: 25.1%

- Dividend Increase Streak: 10 years

Freedom Thirty Five:

This is a fast growing company that can deliver both dividend growth and capital appreciation over time. Alimentation Couche-Tard focuses on the convenience store industry across North America and Europe. Its latest 5 year revenue growth was 10% a year, and earnings growth was 13%. The dividend yield is fairly low at just 0.9%. However the payout ratio is only 10%, meaning the company is re-investing most of its profits back into the business.

This is probably the best way to add long term value for investors because the company is still expanding quickly. What makes ATD.B a great stock to buy in 2011 is its low valuation. Its current P/E ratio is only 14x. This has come down from 17x last year. Relative to other growing companies ATB.B appears to be undervalued right now. With strong earnings growth, and a 10 year history of annual dividend increases, it’s easy to see why this is a great long term hold.

The Dividend Guy:

If there is one company showing strong results but being ignored this year, it is Alimentation Couche-Tard. After posting an EPS surge of 32% and a dividend increase of 25%, the stock price has stagnated for the past 3 months. What’s the reason? Everybody wonders about how the company will fare in a world without gasoline.

With almost half of its profit coming from fuel sales, investors are worried about the electric car (EV) trend. This is greatly exaggerated. In Norway, EV jumped from 0% to 14% of all cars between 2011 and 2019. Fuel sales volume dropped by only 4% during that time.

One factor to consider is Couche-Tard’s wide network. The company is adding many of its supercharger stations across this network to help the transition. ATD can also count on its experience acquired in Norway to manage the shift in other countries. After what we saw in 2020, I think we have a very good idea of how ATD can do in a world where gasoline sales decline.

ATD will continue to make smart acquisitions at reasonable prices going forward. The company is on track with its plan to double its earnings by 2023. That’s not a small milestone.

All About The Dividends:

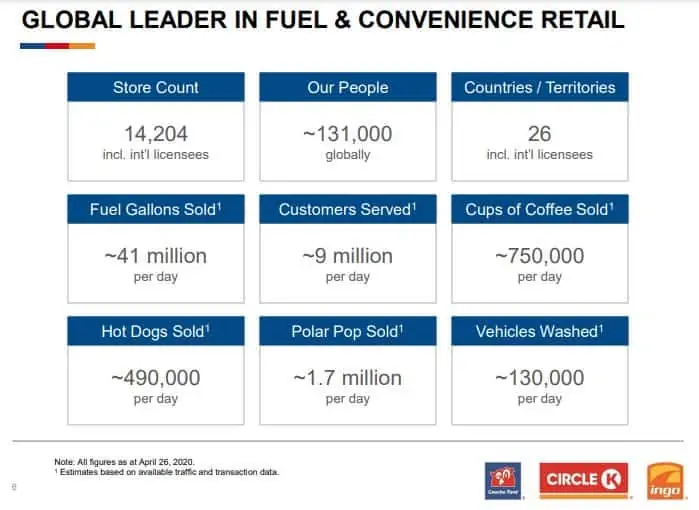

Alimentation Couche-Tard is one of the world’s largest convenience store operators, they currently have around 14,000 stores in 30 countries worldwide. The company currently operates under the following banners Circle K, Mac’s, Couche-Tard and Ingo. Fun fact I used to work for the company and managed a store.

So why is this a top pick you ask? Well the company is very ambitious with the founder Alain Bouchard saying they would like to double their revenue in the next five years or so. Couche-Tard is a company that has fuelled it’s growth through acquisitions and being able to successfully find synergies within their business with every acquisition. The last big purchase the company made was back in 2017 when they purchased 1,300 stores in the US and Canada from CST Brands for $4.5 billion which was their largest purchase ever.

Year to date the stock is down 12% the majority of the decline came in the second week of January when the company announced they were in talks to acquire Carrefour, France’s largest private employer. The rumoured cost of this merger if it happened would have been $20 billion dollars. The merger was called off due to the French government voicing opposition to the deal.

Couche-Tard currently pays a quarterly dividend of $0.087 and has a yield of 0.91%, it’s not a great yield but don’t let that fool you. The company has been raising their dividend for the last several years and the payout ratio is quite low. The last raise was in November and it was for 25%. With Couche-tard you get dividend raises and share appreciation for a total return.

Dividend Earner:

A solid business impacted by Covid-19 with reduced car movement. The management team is smart and they are already ahead of the curve on EV charging in some European countries. Between the reduced revenue from petrol consumption and the transition to EV, there is a potential for winning with both and not losing. As much as EV is different from petrol, the vehicles will still need charging points and someone will collect its dues.

My Own Advisor

I’ve owned ATD.B for only a few years now but I like what I see and own.

Remember, total return matters, not just yield.

In the last 4-5 years as a shareholder, I’ve seen the price rise split-adjusted (most recently January 2020) and some consistent dividend increases as well.

I own this stock to have some proxy-exposure to our Canadian consumer market sector but to also have some built-in diversification beyond Canadian borders.

Couche-Tard is a multinational convenience store owner-operator with tens of thousands of stores across Canada, the U.S., Mexico, Ireland, Norway, Sweden and more international countries.

Couche-Tard has deep pockets and I have little doubt they will grow more via acquisitions over time.

Canadian National Railway (CNR.TO)

Next up is another high dividend growth Canadian dividend stock that many dividend growth investors have come to like. Although Canadian National Railway doesn’t provide very high yield, it is a stable business with a very wide moat. Best of all, CNR has been consistently raising dividends every year.

- Sector: Industrials

- Dividend Yield: 1.77%

- Dividend Payout Ratio: 50.2%

- PE Ratio: 28.95

- 5 Year Dividend Growth Rate: 16.5%

- Dividend Increase Streak: 25 years

All About the Dividends:

One of only two railroads in Canada Canadian National Railway transports more than $250 billion worth of goods annually, it has a rail network that spans 20,000 route miles and connects ports on three coasts. Canadian National has a big moat in it’s business and as investors we should love these companies because the barrier to entry is huge for anyone thinking about competing with them.

2021 is looking like it might be a good year for CNR on Jan 26th when they announced it’s 4th quarter earnings they reinstated it’s full year financial outlook. Also announced they are planning on spending $3 billion on capital investments throughout the year.

On January 26th the company also announced that they were going to raise the dividend 7%, this marks the 25th consecutive year of dividend growth for Canadian National. The yield is under 2% but when it comes to this stock I don’t even look at that, you get a good return on your investment through dividends and share appreciation and I expect this to continue.

As Canada goes, Canadian National goes, I expect once more people are vaccinated in Canada economic activity will pick up and that will mean more business for the railroad. With that being said I expect CNR to have a good second half of 2021.

Dividend Earner:

Solid mover of products from coast to coast and into the US. In fact, it’s the backbone of raw material movement and without new pipelines (Keystone XL is not happening in the US), they benefit the most. With the pandemic, adjustments were made and consumption of goods has changed, and we should see a higher recovery as we come out of lock downs.

My Own Advisor:

I had CNR on my “buy” list last year in 2020, and I picked up more shares last summer after the markets and CNR started to recover from March 2020 lows.

CNR makes my list again this year as one of my top Canadian dividend stocks to buy and hold because like the game Monopoly, as in real life, there are only a few railroads to own. In the game, in many cases, you win by owning railroads and other major board properties. For those of you that enjoy playing that game, you might recall one strategy is to own all the railroads.

The rent for your Monopoly railroads goes something like this: if you own one, the rent on it is $25. If you own two, you get $50 rent from anyone landing on either, if you own three then you get $100, and if you own all four railroads then the rent is tidy $200.

Well, I would argue it’s the same in real life!

With very few players involved at this scale in North America, to transport goods around the continent, I figure CN rail is a key stock to own for mostly growth sprinkled-in with some dividend income.

CNR’s has a rather impressive dividend payout history and I’ve been a part of it for about a decade now as a shareholder.

In fact, CNR recently reported their year-end 2020 results. While there was a slight drop in overall revenue in 2020 (a reminder we are in a pandemic still), there remains billions in free cash flow. The Board rewarded shareholders with a 7% dividend increase this month (January) despite this drop in revenue, a sign in my opinion they are very optimistic long-term about growth and revenue prospects in 2021 and beyond.

According to Yahoo Finance, CNR has returned nearly 80% over the last 5-years (at the time of writing January 27, 2021) when compared to the broad S&P/TSX Composite Index which has delivered about 40% over the same period.

Unless our economy can find a way over the coming decades to ship goods, cheaper and better than rail, coast-to-coast-to-coast, I will continue to buy and own this company pretty much every single year.

Mr. Tako:

On top of having a large moat and being one of the most energy efficient ways to move goods from the US to Canada (or vice versa), CNR is one of the best run railroads in North America. Period. They frequently achieve Returns on Equity exceeding 20%. Yes, the price of shares is a bit expensive, but in this case you’re paying up for quality. Solid dividend growth and modest financial leverage make this a very safe investment earning very good returns.

Fortis Inc (FTS.TO)

Fortis has a 46 year dividend increase streak. The stable dividends and constant and stable yearly dividend increase makes me think that Fortis should be a core stock in any dividend growth investor’s portfolio. It’s no wonder why so many of my fellow DGI bloggers have picked Fortis as one of the best Canadian dividend stocks. It also shouldn’t come as a surprise that I included Fortis as one of the best Canadian utility stocks.

- Sector: Utilities

- Dividend Yield: 4.12%

- Dividend Payout Ratio: 75.9%

- PE Ratio: 18.86

- 5 Year Dividend Growth Rate: 7.4%

- Dividend Increase Streak: 46 years

Freedom Thirty Five:

This is a solid dividend growth stock. Electric and gas utilities will always be in demand, making this industry recession resistant. Fortis has grown its revenue by 7% a year on average over the last 5 years. But its earnings over the same period have grown by 10% a year, signifying higher margins and efficiency.

2021 is a great time to buy this stock and hold it. The company has laid out its long term plan for the future, financing most of its capital expenditures via cash from operations instead of debt. So its balance sheet should remain strong. Fortis has increased its dividends for over 40 years in a row. With a dividend yield of just under 4%, and a 5 year dividend growth rate of 20% a year, Fortis is a reliable name to hold for any dividend investor.

Cheesy Finance:

Starting yield around 4% and 47 years of dividend growth, what’s not to like? However, a Chowder rule value of just under 11 is not something to shout about, that I realize. But the 5 year EPS growth is very good. Payout ratio is good considering it’s a utility.

Forward looking PE of around 18 is not too bad either. Prices are somewhat favourable at time of writing ($52 vs. $54 as a fair value). All things considered, it’s a great cornerstone company to have in one’s Canadian dividend portfolio. It’s a stable payer and it is not a very volatile stock either. In short, it’s a safe bet.

Gen Y Money:

Dividend is safe, has been increasing for over 46 years, and the yield is just under 4% right now.

Get Rich Brothers:

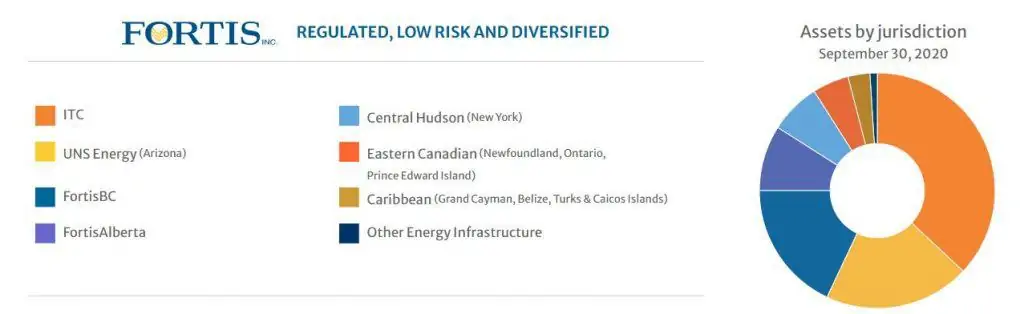

Fortis brings in 99% of its earnings from regulated utilities. Its electric and gas operations serve customers across Canada, the U.S., and the Caribbean.

The company is in a transition phase as it focuses on reducing its carbon footprint. In the years to come, greater emphasis is going to be on renewable energy generation, positioning Fortis to remain a top player in its field.

Fortis provides dividend guidance; they are currently forecasting 6% annual increases through 2025. Given their 47-year track record of annual dividend increases, the durability of their business model can be counted on.

The Toronto-Dominion Bank (TD.TO)

TD is one of the biggest banks in North America. With presence in both Canada and the US and paying dividends since the late 1800’s, TD is another solid dividend paying stock that should reward its shareowners with both share price appreciation and juicy dividends.

- Sector: Financial Services

- Dividend Yield: 4.1%

- Dividend Payout Ratio: 49.2%

- PE Ratio: 11.74

- 5 Year Dividend Growth Rate: 9.5%

- Dividend Increase Streak: 9 years

Cheesy Finance:

A yield of around well over 4% and over 20 years of dividend growth (if you ignore the 2010 hiccup due to the financial crisis). It’s got an acceptable payout ratio of around 50%. It has one of the lowest PE ratios of the Canadian banks and one of the highest 5 year EPS rates.

Another great thing is that it’s reasonably priced at around $73 compared to a fair value of around $80. It has got a broad international spread in terms of business and has been a cornerstone in Canadian banking, which all together makes it one of the better buys if you are interested in Canadian financial institutions.

Gen Y Money:

You can’t go wrong with one of the top Canadian banks. The current forward dividend yield for TD Bank is 4.4%. It is the 5th largest bank in all of North American in total assets. It’s the 2nd largest bank in Canada when you look at market cap. The P/E ratio is 11.27 and the 5 year dividend growth rate is over 9%. I bought some in March but didn’t buy enough. Just recently ‘averaged up’

FI Garage – The Economist:

I was super excited when the Money Mechanic told us Tawcan wanted our Canadian dividend picks for this article. However, my excitement was tempered when I was told (by the Money Mechanic) that I could not pick an ETF as my dividend play for 2021.

I was dismayed because one book that I read in 2018 or ’19 has really stayed with me…Howard Marks’ The Most Important Thing Illuminated which takes Marks’ old text and has three investors add their take to it. The book is split into 21 chapters, each being the “most important thing” and it hit home that I am not willing to invest the time in stock picking that is required to maybe put me on an even playing field with the best in the field.

Marks’ book is on value investing the same lesson on stock picking would seem to hold for dividend investing. That is why if I were allowed to pick an ETF I would pick XEI, iShares S&P/TSX Composite High Dividend Index ETF, with 75 holdings, a MER of 0.22 percent, a 4.87 percent trailing yield, and a P/E of a little under 13.5.

But I am not allowed to pick that, so I will pick TD, they are at the top of the holding list for XEI after all.

Dividend Growth Investor:

TD provides financial and banking services in North America and internationally. The company also has significant operations in the US. The Toronto-Dominion Bank has paid dividends since 1857. Over the past decade, The Toronto-Dominion Bank has increased its quarterly dividends per share at a rate of 9.80%/year. And that’s despite the fact that the annual dividend was left unchanged in 2010.

Earnings per share have increased by 9.60%/year over the same time period. The bank sells for 12.45 times forward earnings and yields 4.36%.

Get Rich Brothers:\

TD is my favourite bank, the world over. It’s a powerhouse with a solid track record of rewarding shareholders with increasing payouts. As we trend to the other side of the pandemic, there will be a huge amount of pent up demand both on the residential and commercial sides of the equation. When life returns to some semblance of normalcy, there will be families looking to purchase new homes and businesses eager to recommence their expansion plans. TD is going to be there to provide the financing.

This company was my first individual stock purchase back in 2009 and it has continued to deliver over the years. I increased my position by 150% during the pandemic.

Telus (T.TO)

Consider that Canadians are consuming more and more data on their phones, telecommunication companies like Telus will benefit from this trend. Rather than expanding into media, Telus has been staying in its core strength by focusing on the wireless business and expanding businesses that can benefit from the wireless business. For example, Telus Health and Telus International will allow Telus to grow once both of these internal businesses are segmented out as separate business entities.

- Sector: Communication Services

- Dividend Yield: 4.8%

- Dividend Payout Ratio: 99.5%

- PE Ratio: 26.98

- 5 Year Dividend Growth Rate: 8.2%

- Dividend Increase Streak: 16 years

No wonder a few DGI bloggers have picked Telus as one of the top Canadian dividend stocks.

Passive Canadian Income:

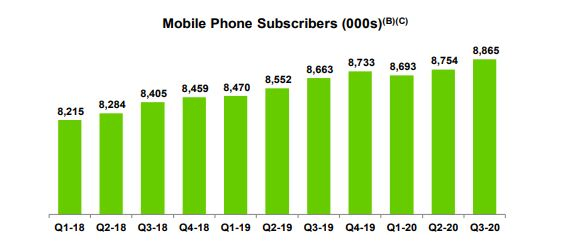

Telus has been a great DGI stock. They continue to add new phone subscribers and grow their telus health business. The recent IPO of Telus International will generate a lot of cash for further growth in that business. While current shareholders won’t get any shares from the IPO, Telus will still be the majority owner and the growth of Telus International should reflect in Telus’s share price as well.

I think people will also be travelling more in the 2nd half of 2021 and Telus will once again be generating more revenue from those roaming fees!

The Dividend Guy:

As opposed to both BCE and Rogers which have built media empires, Telus focused solely on their wireless business. This has paid off well so far and the introduction of the 5G technology should support their continuing growth. In Q3 2020, the wireless segment of their business generated 68% of Telus’ EBIDTA.

What is fascinating about Telus is not just its strong position in the wireless industry. There is more. The company has diversified its business through two interesting divisions. Telus Health is now Canada’s largest healthcare IT provider and TELUS International delivers their innovative business process solutions to some of the world’s most established brands.

By 2019, Babylon by TELUS Health had become Canada’s fastest-growing consumer virtual care service amassing tens of thousands of users while achieving a 4.9 out of 5 satisfaction ratings from their customers. It is almost a sure bet that Telus Health will grow in importance with the pandemic.

Telus International has recently acquired Lionbridge AI for approximately $1.2 billion. They are a market-leading global provider of crowd-based training data and annotation platform solutions used in the development of AI algorithms. These algorithms power machine learning. I like that Telus is looking at expanding its business through AI. Telus’ plan is to partially spin-off Telus International in 2021 but intends to keep 50% of the shares after the IPO.

Get Rich Brothers:

Telus is one of the Big Three Telecoms in Canada. It has consistently shown itself to be a leader in the wireless space, providing services in a sector that is only going to grow in the years to come. If anything, the pandemic has accelerated the digital shift in consumer behaviour which was already underway.

As an added kicker, I love Telus’ footprint in the healthcare field, where it hosts a wide range of electronic medical record offerings.

When it comes to dividends, Telus has a very transparent policy with shareholders—currently forecasting 7-10% dividend growth through the end of 2022. They’ve been providing this sort of guidance since 2011 and it provides great confidence as an investor.

Cut The Crap Investing:

Telus is a solid safety play. It is a solid telco with a tech twist. It is a more pure play on wireless growth but it also has an entrepreneurial bent. Telus recently did a very successful IPO with Telus Health. There is more to come on that front.

Wheaton Precious Metals (WPM.TO)

I’m not a precious metal investor so I have to say that I don’t know anything about Wheaton Precious Metals. Let’s let Dale explain why he picked WPM as one of the best Canadian dividend stocks.

- Sector: Basic Materials

- Dividend Yield: 1.34%

- Dividend Payout Ratio: 48.3%

- PE Ratio: 36.02

- 5 Year Dividend Growth Rate: 28%

- Dividend Increase Streak: 5 years

Cut The Crap Investing:

Wheaton Precious Metals will benefit greatly from the strength in gold and silver and other metals. Gold may continue to respond to the relentless printing of monies by central banks and the debasement of fiat currencies. Silver will benefit greatly from the continued surge in electric vehicles and solar energy. They recently increased their dividend by 20%.

Brookfield Renewable Partners (BEP.UN or BEPC.TO)

Mrs. T and I really like renewable energy and are planning to invest more money into renewable energy companies. One of the renewable companies that we really like is Brookfield Renewable Partners. The company has had solid revenue growth in the last number of years and has consistently grown their renewable portfolio. Not to mention the solid dividends.

- Sector: Utilities

- Dividend Yield: 2.67%

- Dividend Payout Ratio: 63.4%

- PE Ratio: N/A

- 5 Year Dividend Growth Rate: 7.7%

- Dividend Increase Streak: 10 years

All About The Dividends:

BEP operates one of the world’s largest renewable platforms. It has approximately 19,400mw of capacity and 5,318 generating facilities in North America, South America, Europe and Asia. The company’s investment objective is to deliver long term annualized total returns of 12-15%, including annual distribution increases of 5-9% for shareholders.

The stock has gotten more expensive over the last 52 weeks, it has increased 73% but I feel with the world continuing to turn towards renewable energy, and with a new US administration Brookfield is in a good position to develop new generating facilities or just buy facilities from others with their deep pockets.

BEP currently pays a quarterly dividend of US$0.434 and yields 2.47% I expect these to both increase this year and for years to come. I believe BEP stock will continue to shine this year.

Algonquin Power & Utilities (AQN.TO)

Algonquin Power & Utilities is another company that has been focusing on renewable energy. We have been slowly adding AQN shares throughout the past few years to take advantage of AQN’s growing renewable assets. AQN is one of the best Canadian renewable energy stocks in my top 5 list.

- Sector: Utilities

- Dividend Yield: 4.01%

- Dividend Payout Ratio: 74.4%

- PE Ratio: 17.99

- 5 Year Dividend Growth Rate: 9.8%

- Dividend Increase Streak: 9 years

Passive Canadian Income:

Algonquin is a great dividend growth stock. You get a fantastic dividend growth rate and solid capital appreciation as well. Renewables are the future and Algonquin is well positioned in this area and has a couple more solar and wind projects in the works.. While some other green energy companies stock prices have skyrocketed, I feel Algonquin is still trading at a fair value price point.

My Own Advisor:

The future is now, unless we don’t want to have a future at all…

I’ve been a shareholder of this company for more than a decade now and certainly in hindsight, this has been a great Canadian selection in the power and renewable energy space.

I started writing about AQN back in 2013 on my site – I’ve been a shareholder since before that time.

My thesis on AQN and other Canadian renewable energy companies is rather simple – for the sake of our planet, we need to go more green far sooner than later. I’m happy to support that push with my wallet.

Algonquin Power & Utilities Corp. is a growing renewable energy and regulated utility company with assets across North America. This company both acquires and operates green and clean energy assets including hydroelectric, wind, thermal, and solar power facilities, as well as sustainable utility distribution businesses (water, electricity and natural gas).

The renewable energy space has also been good to shareholders and that trend should continue for the foreseeable future. I hope so. We need more of what AQN delivers.

FI Garage – Money Mechanics:

My dividend pick is Algonquin Power & Utilities (AQN). Currently yielding 3.62%, they are not the highest in the sector. But I believe that Algonquin offers a good valuation as a growth pipeline that includes renewable power development activity, potential acquisitions, utility rate base investments, and potential international investments.

AQN has confirmed that it will continue it’s dividend growth wof 10% in 2021. Beyond 2021 it is anticipated that the dividend and increases are sustainable with EPS growth, stable EPS payout ratio, and capital investment opportunities.

AQN also has a good track record of completing renewable power projects, this, along with other acquisitions position AQN as a strong and consistent dividend stock going forward. Disclosure, I am long AQN.

Royal Bank of Canada (RY.TO)

If you take a look at our dividend portfolio, you’ll notice that we own all six Canadian banks. We like Canadian banks for its stable dividends and solid revenues. Royal Bank is one of the biggest banks in Canada and has been paying dividends since the late 1800’s. During the financial crisis, Royal Bank didn’t cut its dividends at all, unlike many of its American counterparts. For that reason alone, I think RY is one of the best Canadian dividend stocks.

- Sector: Financial Services

- Dividend Yield: 3.99%

- Dividend Payout Ratio: 55.2%

- PE Ratio: 13.42

- 5 Year Dividend Growth Rate: 7.5%

- Dividend Increase Streak: 9 years

Simply Investing:

- RY is currently undervalued because its current dividend yield (4%) is higher than its 20-yr average dividend yield (3.64%)

- RY has been paying dividends since 1870

- RY has had 9 years of consecutive dividend increases

- RY is the largest bank in Canada

- In my opinion RY is recession proof

- RY passes all my 12 Rules of Simply Investing

Dividend Growth Investor:

A diversified financial service company, provides personal and commercial banking, wealth management, insurance, investor, and capital markets products and services worldwide. This is another bank that has operations in the US. Royal Bank of Canada has paid dividends since 1870.

Over the past decade, Royal Bank of Canada has increased dividends per share by 7.90%/year. And that’s despite the fact that the annual dividend was left unchanged in 2009 and 2010. Earnings per share have increased by 8.40%/year over the same time period. The bank sells for 11.84 times earnings and yields 4.17%.

Magna International (MG.TO)

If you want to invest into the growing electric vehicle (EV) segment, one way is to invest in EV companies like Tesla, another way is to invest in car parts manufacturing businesses like Magna International. MG has emerged as a key manufacturer of car parts. Many car companies have signed supply agreements with MG.

- Sector: Consumer Discretionary

- Dividend Yield: 2.02%

- Dividend Payout Ratio: 83.94%

- PE Ratio: 33.7

- 5 Year Dividend Growth Rate: 13.9%

- Dividend Increase Streak: 10 years

The Dividend Guy:

Magna is not only a dominant player in the car parts manufacturing business, but it is also the only car part maker able to build an entire car from its own parts. The company has been proactive by shifting part of its business into electric cars and hybrids. Magna has signed a partnership with Fisker to provide the framework for platform sharing and manufacturing cooperation. The company has the resources and expertise to support electric car companies as it still supports “classic” car brands.

Finally, the company is also active in car autonomy and connected devices. Therefore, Magna is creating a variety of cameras, radars, sensors and controllers for the next generation of vehicles. No matter which car brands win the battle for the best electric and autonomous cars, you can bet that Magna will sell them parts or whole systems.

Nutrien Ltd. (NTR.TO)

We all need to eat. To meet the ever increasing food demands, farmers need to grow crops. And what do crops need to grow? Fertilizers. If you want to find a stable company that everyone needs its product, look no further than Nutrien.

- Sector: Basic Materials

- Dividend Yield: 3.4%

- Dividend Payout Ratio: +100%

- PE Ratio: 66.99

- 5 Year Dividend Growth Rate: 2.5%

- Dividend Increase Streak: 4 years

Another Loonie:

Nutrien was formed after the merger of PotashCorp and Agrium in 2018. Anyone familiar with the potash sector knows that Nutrien is an absolute monster; with a $38 billion market cap, Nutrien is the world’s largest potash producer and the third-largest nitrogen fertilizer producer. Nutrien’s focus is to “feed the world” and do so sustainably and profitably.

The investment case for Nutrien is simple: with global warming impacting the world’s agriculture now and in the future, companies like Nutrien will be relied upon to provide the crop inputs and services needed to keep the world fed.

Nutrien also offers historically-stable earnings and a dividend that has grown considerably over the years – currently yielding 3.4%. In 2019 alone, Nutrien returned nearly $3.0 billion to shareholders through dividends and share repurchases.

Enghouse (ENGH.TO)

Enghouse is a Canadian based company that provides enterprise software solutions focusing on remote work, visual computing, and communications for next generation software defined networks. The company has two business segments, Interactive Management Group and Asset Management Group. ENGH has an impressive 13 years dividend increase with a 10 year annualized dividend growth rate of 22%. Although the initial dividend yield is very low, ENGH is considered as a high growth dividend stock.

- Sector: Technology

- Dividend Yield: 0.98%

- Dividend Payout Ratio: 30.4%

- PE Ratio: 31.17

- 5 Year Dividend Growth Rate: 17.2%

- Dividend Increase Streak: 13 years

Cut The Crap Investing:

Canadian tech is more than Shopify. Take your pick, there are many great candidates in this burgeoning sector. I’ll go with Enghouse. It’s a good dividend grower. In fact you’ll find it in Horizons HAL, Canada’s best performing dividend ETF. Enghouse Systems Ltd is a Canada-based provider of software and services to a variety of end markets.

Boralex (BLX.TO)

Boralex is a major player in renewable energy specializing in wind, solar, hydroelectricity, and thermal. Boralex started in Quebec and over the last 30 years, the company has expanded into the US and France.

- Sector: Utilities

- Dividend Yield: 1.49%

- Dividend Payout Ratio: +100%

- PE Ratio: 65.94

- 5 Year Dividend Growth Rate: 4.9%

- Dividend Increase Streak: 4 years

Dividend Investor:

A green energy play. I think this is a sector no one should ignore as its relevance increases over the years. They have a strong management with good international relations. Price has tripled in the last 5 years and will continue to reflect an ever expanding company.

Dividend is low at 1.4% (recent significant run up in stock price) and dividend increases are sporadic with an increase every 1-2 years. 5yDGR sits at 5.2%.

National Bank (NA.TO)

By now, are you really surprised to see yet Canadian bank on the best Canadian dividend stocks list? Well you shouldn’t. Although NA isn’t as big as the Big Five, it has been expanding outside of its key market, Quecbec. Given NA hasn’t captured the rest of the Canadian market, there are a lot of growth potentials for NA.

- Sector: Financial Services

- Dividend Yield: 3.54%

- Dividend Payout Ratio: 49.8%

- PE Ratio: 14.07

- 5 Year Dividend Growth Rate: 7.2%

- Dividend Increase Streak: 10 years

Freedom Thirty Five:

This is one of the best performing banks in the country. National Bank has grown its revenue by 10% annually over the last 5 years. Its 5 year dividend growth rate is 7% a year. It also has a relatively attractive P/E ratio of just 12x. The dividend yield is about 3.9%, and it has increased dividends annually for over 10 years.

This dividend grower has one of the best management teams in the financial industry, and the stock has outperformed all of the Big 5 banks over the last decade. Due to its smaller size and increasing exposure to emerging markets, National Bank may be more volatile than the larger Canadian banks. But that risk is already priced into the stock, and there’s a lot more room for growth potential.

Manulife Corporation (MFC.TO)

Manulife is a juggernaut in the insurance sector. Manulife happens to be one of the first dividend paying stocks that I purchased and it has done quite well over the years.

- Sector: Financial Services

- Dividend Yield: 4.42%

- Dividend Payout Ratio: 38.2%

- PE Ratio: 8.65

- 5 Year Dividend Growth Rate: 11.9%

- Dividend Increase Streak: 6 years

Simply Investing:

- MFC is currently undervalued because its current dividend yield (4.57%) is higher than its 20-yr average dividend yield (2.85%)

- MFC has been paying dividends since 2000

- MFC has had 6 years of consecutive dividend increases

- MFC is the largest insurance company in Canada and the 28th largest fund manager in the world based on worldwide institutional assets under management (AUM).

- In my opinion MFC is recession proof

- MFC passes all my 12 Rules of Simply Investing

Savaria (SIS.TO)

I can’t say I know too much about Savaria so it was interesting to see a fellow DGI blogger picking Savaria as one of the best Canadian dividend stocks.

- Sector: Industrials

- Dividend Yield: 2.97%

- Dividend Payout Ratio: 86.6%

- PE Ratio: 29.21

- 5 Year Dividend Growth Rate: 27.2%

- Dividend Increase Streak: 7 years

Dividend Investor:

A great play on the mobility sector. Basically, they modify homes/cars/commerce to include escalators/elevator/ramps/lifts etc. The population is aging significantly (see stats.) and the number of people in the target demographic have increased to the tune of 30-100% in the last 10 years. This will continue.

With this pandemic, I think more money might be put towards home adaptation as people could become fearful of senior homes. Overall, it’s also a very financially responsible company with great management. They acquire strategically internationally (in the US a few years ago and this year in Sweden). Monthly Dividend sits at 2.8%, well covered, and 3 yr Growth rate is a generous 14.5%. (5yr is 22.45).

GoEasy Financials (GSY.TO)

GoEasy is a Canadian public alternative financial company. Although GoEasy may not be a well known name, the company has had a five year dividend increase streak with a very high dividend growth rate.

- Sector: Financial Services

- Dividend Yield: 1.53%

- Dividend Payout Ratio: 29.6%

- PE Ratio: 19.36

- 5 Year Dividend Growth Rate: 29.5%

- Dividend Increase Streak: 5 years

Setting Nomand:

While their core business is lending and occasionally at pretty high interest, many investor’s see it as opportunistic and predatory business, but the bottomline is GoEasy’s EPS has grown average 30% in last 3 years and have healthy insiders holding of 25%.

Their 3 years dividend growth is nearly 36% with the last raise of 45% and could be a great source of growing dividend in coming years. I own them in my TFSA and would be happy to add them at any dip, various analysts peg their price upside 6% to 14%.

Enbridge (ENB.TO)

Enbridge probably has the highest dividend yield on this list of best Canadian dividend stocks. Since we all need natural gas to heat our home, I believe Enbridge has a very stable business. With the stoppage of Keystone XL, Enbridge’s existing pipelines suddenly have become more valuable.

- Sector: Energy

- Dividend Yield: 7.53%

- Dividend Payout Ratio: +100%

- PE Ratio: 30.05

- 5 Year Dividend Growth Rate: 16.1%

- Dividend Increase Streak: 24 years

Passive Canadian Income:

Enbridge is one of my favourite stocks. Right now they are cheap and you get a massive starting yield off the bat. We saw the cancellation of the keystone pipeline. This should continue to benefit enbridge and also shows just how valuable those existing pipelines are.

I’d say by the fall we won’t be talking about covid 24/7 and the demand for oil will go up and money may start flowing into the oil and gas stocks again. Enbridge is also starting to get more and more renewable energy in their portfolio, which could draw even more investors.

The North West Company Inc. (NWC.TO)

If you look at any Canadian index ETF, you’ll notice that the top 10-15 holdings consist of banks and oil & gas companies. Although there aren’t too many dividend paying Canadian companies that fall in the consumer staples sector, the North West Company is one of them. For investors looking to expand their exposure in the consumer staples sector, they should seriously consider NWC.TO.

- Sector: Consumer Staples

- Dividend Yield: 4.3%

- Dividend Payout Ratio: 57.3%

- PE Ratio: 13.31

- 5 Year Dividend Growth Rate: 2.6%

- Dividend Increase Streak: 1 years

Another Loonie:

The North West Company is a grocery and retail company unfamiliar to most Canadians. Unlike Loblaws, Sobeys, and Costco, The North West Company primarily focuses on remote markets like those in northern Canada and Alaska. Before becoming a public traded company on its own, The North West Company had a storied history in the fur trade, eventually becoming part of the famous Hudson’s Bay Company in 1821. This long history means that many of The North West Company’s retail stores have been in operation for over 200 years!

Since being acquired and taken public in the 1990s, The North West Company has flown under the radar of the average Canadian investor. With its $1.6 billion market cap, the Company has established itself as a mini-stalwart in the Canadian grocery sector.

Over the last decade, it has grown its dividend by an impressive 50% and plans to continue raising its 4.5% dividend well into the future. Although its outlook has been clouded by COVID-19, its position as an essential service means it will continue to operate as a sustainable, profitable business.

Kirkland Lake Gold (KL.TO)

I will admit I have not considered Kirkland Lake Gold on my list of best Canadian dividend stocks for one simple reason – I don’t know the gold sector well enough. However, if you like the gold sector, Kirkland Lake Gold could be a good stock to hold.

- Sector: Basic Materials

- Dividend Yield: 1.99%

- Dividend Payout Ratio: 24.9%

- PE Ratio: 12.52

- 5 Year Dividend Growth Rate: n/a%

- Dividend Increase Streak: 3 years

Settling Nomad:

With last 3 years of average EPS growth 72% & Dividend raise of astonishing 163%, this is my #1 pick for 2021. Gold is considered safe haven in the time of uncertainty and hence the outlook to me seems positive. KL with their strong balance sheet showing ample cash on-hand and nearly zero debt is an attractive choice. They have a modest but healthy dividend yield and tons of room to increase the dividend growth in coming years. Several analyst predicts the price upside for 2021 from 20% to 60% and while I don’t own it but would, as soon as I have some cash.

ATCO (ACO.X)

I will be perfectly honest that ATCO isn’t on my watch list so it was interesting to see Kanwal picking ATCO as one of the best Canadian dividend stocks. ATCO is a Canadian engineering, logistics, and energy holding company with subsidiaries including electric utilities, natural gas production, and distribution companies, and construction companies.

- Sector: Utilities

- Dividend Yield: 4.68%

- Dividend Payout Ratio: 76.7%

- PE Ratio: 16.4

- 5 Year Dividend Growth Rate: 13.5%

- Dividend Increase Streak: 26 years

Simply Investing:

- ACO.X is currently undervalued because its current dividend yield (4.73%) is higher than its 20-yr average dividend yield (2.39%)

- ACO.X has been paying dividends since 1973

- ACO.X has had 27 years of consecutive dividend increases

- ACO.X is a diversified $22 billion enterprise with thousands of employees worldwide providing solutions in Structures & Logistics, Electricity, Pipelines & Liquids and Retail Energy. It also owns Canadian Utilities (CU).

- In my opinion ACO.X is recession proof

- ACO.X passes all my 12 Rules of Simply Investing except for one, Long-term Debt/Equity Ratio is 240%, however utility and energy companies generally carry more debt due to the nature of their business.

Intact Financials (IFC.TO)

Intact Financials was the first dividend paying stock that I purchased before the financial crisis. The stock price was down quite a bit during the financial crisis. Luck for me, I decided to hold it and the stock has done very well since. IFC has been consistently raising its dividends for the last 15 years. Combined with an appreciating stock price, dividend investors should consider holding IFC in their portfolio.

- Sector: Financial Services

- Dividend Yield: 2.19%

- Dividend Payout Ratio: 52.9%

- PE Ratio: 24.17

- 5 Year Dividend Growth Rate: 9.6%

- Dividend Increase Streak: 15 years

Dividend Earner:

A solid business growing through acquisitions. While we know there is death and taxes, I would like to highlight that insurance is a close 3rd. Damn if you don’t have insurance and something happens. The investment thought here is that the core business being a solid foundation and the company looking for acquisitions for growth will continue to help the company grow and therefore make you money.

Bank of Nova Scotia (BNS.TO)

Another Canadian bank on the best Canadian dividend stocks list. Are you really surprised? For me, I think it’s best to own individual Canadian banks rather than relying on one of the Canadian bank ETFs. Why pay the extra MER when you can simply create your own Canadian bank ETF yourself?

Bank of Nova Scotia is one of the most geographical diversified Canadian banks. Unfortunately, the diversification has caused some pains for BNS and this has been reflected in the stock price the last few years. BNS is working hard to consolidate its Latin America exposure and focus on selective few countries. Hopefully the management will turn things around quickly!

- Sector: Financial Services

- Dividend Yield: 5.05%

- Dividend Payout Ratio: 67.3%

- PE Ratio: 13.35

- 5 Year Dividend Growth Rate: 6.4%

- Dividend Increase Streak: 9 years

Mr. Tako:

Bank of Nova Scotia is another stock that had a difficult year due to the pandemic. Banking, as a whole is a good capital-light business, and I believe BNS could be poised for a comeback over the next couple of years. I like that BNS has gotten more focused in their international operations recently, trimming some bad overseas assets. This should

lower expenses and improve asset returns. The need for large loan loss reserves should also slow in coming quarters, giving earnings a nice boost. Meanwhile a safe and healthy dividend yield will continue to provide for patient shareholders.

TC Energy (TRP.TO)

Given it’s harder and harder to build new pipelines because of the environmental concerns and regulations, I like what TC Energy can provide for dividend investors.

- Sector: Energy

- Dividend Yield: 5.7%

- Dividend Payout Ratio: 68.6%

- PE Ratio: 12.04

- 5 Year Dividend Growth Rate: 9.3%

- Dividend Increase Streak: 19 years

Cheesy Finance:

Albeit the future is uncertain with regards to the move into more renewable energy sources. Currently this stock is pretty interesting. It has a (very) high yield of over 5,5% and 20 years of increasing dividends. That’s a good start.

The fair value is estimated at $65, with current prices at around $55, it might be a good time to buy. Other good news is that it’s PE ratio is one of the best in the business at time of writing. Furthermore, it has an acceptable payout ratio and one of the best EPS percentages compared to its competitors.

However, not all is rainbows and unicorn (depending on how you look at this). The free cash flow has been negative for a few years now. Still, a solid company with a good reputation and the potential to make you a very juicy dividend with an acceptable risk.

Intertape Polymer Group Inc. (ITP.TO)

The packaging sector is an interesting one. While 3M dominates the tape business, ITP has taken hold of the position of the second-largest tape producer in North America. With online shopping become more and more prominent, ITP may benefit from the increasing needs of tapes, films, and woven coated fabrics.

- Sector: Consumer Discretionary

- Dividend Yield: 3.49%

- Dividend Payout Ratio: 53.2%

- PE Ratio:15.24

- 5 Year Dividend Growth Rate: 7.5%

- Dividend Increase Streak: 1 years

Another Loonie:

Intertape Polymer Group Inc. is a Montreal-based packaging supply company with a $1.3 billion market cap. Despite its small size, Intertape is the second-largest tape producer in North America and boasts a market share of 20 to 30 percent for most of its products. You’ve almost certainly heard of Intertape’s much larger competitor, 3M, which has a market cap of nearly $100 billion USD.

With an impressive dividend yield of 3.4%, Intertape Polymer Group Inc. is well-positioned to take advantage of the global transition towards online retail. With its suite of “curb-side friendly” tape, stretch film, paper inserts, shipping labels, and other mailer products, Intertape is doing its part by offering environmentally friendly alternatives to typical wasteful packing and mail products. We can expect that Intertape will continue to grow its revenues going forward as it helps fuel the online-retail revolution.

Points International Ltd. (PTS.TO)

This is one stock I haven’t been following so it was interesting to see Mr. Tako, a fellow dividend investor that I admire a lot, picking this stock.

- Sector: Financial Services

- Dividend Yield: N/A

- Dividend Payout Ratio: N/A

- PE Ratio: N/A

- 5 Year Dividend Growth Rate: N/A

- Dividend Increase Streak: N/A

Mr. Tako:

Being in the travel sector, Points International had a rough 2020. This is to be expected, but I was surprised to see Points came very close to breaking even (despite 2020 being one of the worst years for travel ever). Prior to 2020, Points was a profitable and growing company in the travel-loyalty sector with customers around the globe.

Technically this is not a dividend stock, but prior to the pandemic Points generated enough free cash flow to buy back over $10 million in shares every year. They choose to do buybacks instead of dividends. I expect business at Points will return solidly when travel picks up again.

Power Corporation (POW.TO)

I have looked at Power Corporation for a while but haven’t pulled the buy trigger. I like POW as it partially owns Personal Capital and Wealthsimple. Wealthsimple is becoming a big investing platform here in Canada. We have a Wealthsimple Trade account for the kids and I really like the no commission trading Wealthsimple Trade offers.

- Sector: Financial Services

- Dividend Yield: 5.81%

- Dividend Payout Ratio: 71.4%

- PE Ratio: 12.29

- 5 Year Dividend Growth Rate: 6.6%

- Dividend Increase Streak: 5 years

Gen Y Money:

Dividend yield is around 6% right now, they invested in Personal Capital and Wealthsimple, and even though the stock price hasn’t moved much, the dividend is safe and I’m happy with a 6% dividend.

A&W Revenue Royalty Income Fund (AW.UN)

Of all the fast food restaurants, I really like A&W’s burgers, rootbeer, and fries. When we first started investing, I considered buying AW.UN but decided to invest in KEG.UN instead.

- Sector: Consumer Discretionary

- Dividend Yield: 3.76%

- Dividend Payout Ratio: 78.3%

- PE Ratio: 20.85

- 5 Year Dividend Growth Rate: N/A

- Dividend Increase Streak: N/A

A&W.UN has had a tough time due to COVID-19 but the fund should hopefully start to recover as restrictions start to ease. One thing to keep in mind is these restaurant royalty income funds usually have very little dividend growth.

FI Garage – The Accountant:

I’m going a little off the board for this one and taking AW.UN as my dividend pick for 2021. A&W got beat up in 2020 as expected, they had to close many restaurants and had to suspend the distribution as a result. They have since reinstated the distribution and paid out special dividends in order to make up for the missed payments.

In 2019 they saw the distribution start the year at $0.143 per month and end at $0.159 per month. Over an 11% increase for the year. While the distribution is currently back at $0.10 monthly this has a lot of room to grow as we open back up. A&W is well run and has many growth opportunities ahead, once they get back to seeing same store sales growth as they did before COVID along with strong openings of new restaurants added to the royalty pool we should see earnings continue their steady rise.

As of writing this the current yield is 3.81% with EPS of $1.54 and a P/E around 20. Look for all of those to rebound in the coming months as things finally start to get back to normal. I wouldn’t be surprised if we see the distribution back to its former level by early 2021, so if you’re looking for some dividend growth don’t sleep on A&W.

Brookfield Asset Management (BAM.A)

Brookfield Asset Management is a leading global alternative asset manager with over $575 billion of assets under management across real estate, infrastructure, renewable power, private equity and credit. Some of its holdings include Brookfield Renewable Partners, and Brookfield Property Partners.

- Sector: Real Estate

- Dividend Yield: 1.2%

- Dividend Payout Ratio: N/A

- PE Ratio: N/A

- 5 Year Dividend Growth Rate: 7.1

- Dividend Increase Streak: 8

Dividend Growth Investor:

BAM manages and owns long term real estate and infrastructure assets worldwide. They invest in renewable energy and infrastructure projects. They also manage assets, which provides a nice stream of recurring fees, and helps them partner on promising projects.

They have high insider ownership and their CEO Bruce Flatt is a brilliant asset allocator with a strong track record.

The company has expanded through strategic acquisitions as well, and it has the record of integrating them successfully.

Brookfield has managed to increase dividends for 9 years in a row and yields 1.24%. While the company does not yield much, it offers the possibility for stronger dividend growth and total returns.

Agnico Mines (AEM.TO)

It was interesting to see Settling Nomad picking yet another mining company. I can’t say I know Agnico well enough so I’ll leave the analysis to Settling Nomad.

- Sector: Basic Materials

- Dividend Yield: 2.28%

- Dividend Payout Ratio: 69.8%

- PE Ratio: 30.63

- 5 Year Dividend Growth Rate: 11.4%

- Dividend Increase Streak: 4

Settling Nomad:

This is my last pick for 2021, again belongs to Gold mining business. Their last dividend raise was 75% and 3 years average dividend growth rate of 32% and analyst predicts price upside ranging from 8% to 31% for this year. The current dividend yield is 2.1% with payout ratio of 42% and since 1998, they consistently outperformed both gold and gold equities with a compound annual growth rate of approximately 13%.

Park Lawn (PLC.TO)

Park Lawn is the only Canadian publicly listed cemetery, funeral and cremation business. I suppose if you want to bet on the aging Canadian population, PLC.TO might be worthwhile to consider.

- Sector: Consumer Discretionary

- Dividend Yield: 1.52%

- Dividend Payout Ratio: +100%

- PE Ratio: 67.26

- 5 Year Dividend Growth Rate: N/A

- Dividend Increase Streak: N/A

Dividend Investor:

Another play on the aging population. This is the only publicly traded ‘Death Sector’ stock in Canada. Growth is both organic and through acquisitions. Also a monthly dividend, sits at 1.4% and is very well covered. Unfortunately no Dividend growth. Stock Price nearly tripled in the last 5 years to make up for that though.

Summary – Best Canadian dividend stocks from the DGI community

Thank you so much to everyone for submitting their picks for the best Canadian dividend stocks. It was quite interesting to read the analysis and reasoning behind each pick.

Everyone seemed to have different favourites but there is some consensus. It appears the Alimentation Couche-Tard, TD, Fortis, Canadian National Railway are the favourites due to their strong revenues, wide moat, and solid dividend increase history.

While neither ATD.B and CNR.TO have the highest dividend yields, the strong organic dividend growths for the past number of years make these two dividend stocks extremely attractive.

I was not surprised to see people picking TD and Algonquin Power. Both of these companies, again, have strong revenues, wide moat, and solid dividend increase history.

What I found particularly interesting is that TD came out ahead as the Canadian bank to pick. I was a little bit surprised that not as many DGI’s picked Royal Bank and National Bank.

It is also interesting that nobody picked a REIT. I suppose it’s a telltale sign that the Canadian REIT sector is struggling because of COVID-19.

There are a few picks that aren’t on my watch list at all so it was always interesting to learn more about new companies and potentially put them on the watch list.

I hope this round up from the DGI community has shone light on some Canadian dividend stocks that people may have not considered previously. Finally, please remember, it is always important to do your own research, like reading company’s annual and quarter reports, before pulling the buy trigger and always ask the three key questions before you invest.

And if you do not want to invest in individual dividend paying stocks, investing in an all-in-one ETF like XBAL and VGRO is always a great way to stay diversified. If you want a portfolio consists of 100% stocks and do not want to manage your own portfolio, an all-equity ETF like VEQT or XEQT may be a good fit for you. Check out the VEQT review for some in-depth analysis.

If you’re looking to diversification outside of Canada, it may make sense to utilize one of the low cost ex-Canada ETFs like XAW to diversify our portfolio internationally. Or you can choose to hold individual US and international dividend stocks.

Happy investing everyone!

Hello and Thank you for this post.

In the POW stock, you mention that you hold a wealthsimple account for your kids. How do you go about doing that?? My kids are 5 and 7 and I would love to start an account for them. Can you explain more? ( or do a post on the subject) Thank you again.

divi 011024 How to invest for minor children

in the last month i dreamt up this for my minor gchildren in their teens:

I issue them the appropriate celebration card eg xmas or birthdate or grad and give them a small portion in cash and at least an equal value amount in stocks which i write on the card with the date and i just before I write up the card, assign them the appropriate number of shares at the current price from an existing stock i own which with the dividends and dividends reinvested with gain/loss (should be gains for sure if over 7 yrs later) will be given to them to put into their own tfsa at Wealthsimple at age 18. eg My eldest just turned 17 and for her birthday she ended up with ~$200 cash and 5.49 stocks of CM (next round i will do that with FTS and prol alternate w Cm) which i have entered onto a spreadsheet. I will round off the # of shares on transfer(as my broker does not allow fractional shares) to gchild when she/he turns 18 and I will sell them on the market and give them with a trust note the resulting entire cash to to be placed in her TFSA – i told her i will demi – blackmail her if necessary (ha ha ) so she does not spend the money = told her that for every $ she does not place in the tfsa i will dock her $3 from her inheritance ( she can get cash and things gifts from other gparents and relatives). (14 yr old sister ended up w 2 shares of CM). They will have to absorb the capital gains tax i incur but i told them i will absorb the div taxes and that the older one will get more shares for 2024 as she only has one year to run this trust type of investment. That set of parents were too busy to set up a NR account in their own name at WS but my son, for his 2 kids, of similar ages to those 2 of my daughter, did set up a NR acct for his kids at WS so i just give him all the money on the occasions and he does as i do. Explaining it sounds complicated but the doing is quite easy.

Thanks.

Hi: Love your analyses.

I took your advice and bought CNR, which promptly went down 8.72%.

Why is this? Isn’t a good old stock like CNR supposed to be able to stay at least what I paid for it?

I’m a beginner investor, so maybe this is a dumb question.

Sincerely, Lula in Toronto

Stocks go up and down. Long term I have no doubt CNR will continue to go up.

Hi Bob,

Impressive list of top Canadian dividend stocks. I am fortunate to own most of them in my portfolio. Not playing favorites but I would say ATD.B and NWC easily among my top 10.

That’s a awesome list, thank you for sharing ! I have most of these stocks into my portfolio but it gives me ideas for maybe a new position either $MG $ENGH or $PLC ✓

Nice work, Bob! A great list of Canadian blue chip dividend stocks that will work in any portfolio. I like Canadian National Railway with 16% dividend growth rate and 25 years of consecutive dividend increases. What’s more, it has appreciated by 417% over the last decade, far beating the S&P 500 and the $TSX.

What do you think about investing in Financials Stocks in the US that are not really banks and do not carry the lending risk? As an example, Intercontinental Exchange that owns the New York Stock Exchange. It has gained over 400% in the last decade, grown dividends at 16% CAGR over the last 5 years and carries operating margins of greater than 60%.

I also like S&P Global that provides the S&P 500 index and investment intelligence to institutional investors. It is a dividend aristocrat having grown dividends for 47 consecutive years and gained about 1047% in the last decade?

Thanks and cheers to all good things!

Hi Bob

Nice compilation. Thanks for putting it all together and share. This kind of list is interesting because there are always some new companies that are, at least for me, out of the radar, such as PLC, POW, PTS and ITP.

All the best.

Cheers!

It’s always interesting to see what stocks other investors are looking at. 🙂

Great list thanks for the information

I have been a dividend investor for years with some growth companies mixed in. So this is excellent information for my investing ideas this year and a few years going forward.

Eventually I want to blog about my journey especially as I close in on retirement (7 years) where I like to help out others. This year I will hopefully pull in 20 k in dividends from all our accounts and keep increasing forward.

Thanks

Very cool that you are aiming to pull in $20k in dividends. 🙂

Thanks Tawcan for putting this together and I apologize in not getting my list in on time. Crazy month. Looking at the list I personally own almost all of these. Keep doing your thing!

Thanks Brian. No worries about not getting your list in on time. 🙂

Thanks for this wonderful summary from a little old lady of 75 who almost exists, but not quite, on her dividends. I am going to take up some positions on the basis of these recommendations, but am so pleased that I have already invested in some –not because I’m an expert, but because I use the products, e.g., a nice meatless burger at A. & W!

Now, how about the same kind of summary of US stocks, of which I hold a few, even though I hate the withholding tax.

You’re welcome Laurie.

Good suggestion on US dividend stocks. Something I plan to work on in the future.

hi, i’m new to this but i’m in my early 50’s. which of these would you recommend for someone just starting out and could use this money in the next 15-20 years? thanks!

Thanks for including me in this little (?) round-up Bob! A few of the companies were new to me, so this was great!

I know I cheated a little and picked a non-dividend payer, but the free cashflow used for buybacks is something interesting to behold there.

Thank you for participating Mr. Tako. There were some interesting picks that’s for sure.

Thanks for including me and lots of work for you compiling all the thoughts and responses.

Interesting list, lots of names that I haven’t heard about.

I think I remember hearing about Park Lawn briefly, but that would be an interesting investment given our aging population.

Thank you for participating, it was much appreciated. 🙂

Park Lawn is definitely an interesting pick and will require more research.

My favorite would be Canadian National Railway. Transportation of goods will never stop and it’s a solid business model with perpetual demand for all of eternity. Even as we move to the digital world, physical goods will never stop being transported.

Good on you for compiling the list of great dividend stocks. Passive income should be on people’s radar to improve for 2021.

CNR is definitely one of my favourites. The dividend yield isn’t high but the growth has been very consistent.

Wow, this is incredible. Thanks for putting this all together. It’s going to give the community so many great investment ideas. I was so happy to participate. Cheers!

You’re welcome. Thank you for participating.

Hey Bob,

Really impressive article. This had to be a monumental task to get it together.

Plenty to chew on and quite a few companies I have to admit I wasn’t even aware of; it’ll be nice to dig into them in some greater detail to see if they merit a spot in the portfolio.

I appreciate you including us. Felt great to contribute to this collaborative piece of work.

Take care,

Ryan

Thanks for participating Ryan. This has been a great list to put together.

That’s a great post and summary. Thanks, Bob.

From all the stocks listed, there are a few we would like to add to our portfolio, including Fortis and CNR.

Last year we started a position with Couche-Tard. 🙂

Stay safe!

Seems like I’m one of the few investor that hasn’t started a position with Couche-Tard…

Awesome list! Thanks Bob for putting it all together! And thanks for including me.

Thank you for participating and submitting your list Kanwal.

The list of quality dividend growth stocks, is probably about 30 or so stocks. My preference is for each investor to review, evaluate, and make up their own list, the ones they feel most comfortable with. The make your buy decisions based on the current status of the companies on the list.

It’s always interesting to see what others like, but always do your own analysis.

Good article.

Thanks HenryM. This list is meant as a suggestion. Each investor should review and make their own buying decision.

Wow, amazing job curating all of this Bob!! Thank’s for including the FI Garage. I see a lot of familiar companies in here, just wish I had enough to deploy more $$$.

Thank you Money Mechanic. It took a long time to curate and organize everything. Thank you for participating.

I like this article because it confirms my biases, haha. Thanks for reaching out and including me. I can only imagine how many long hours it took to put all of this together. Great job. 🙂

As a follow up, it might be interesting to conduct a reader’s poll with a list of all these dividend stocks, and having your visitors pick their favourite. I wonder how the poll results would line up with blogger’s picks.

Haha. It was interesting to see all the picks. Yea a readers’ favourites might be interesting. 🙂

Tawcan,

That’s a great resource of Canadian Dividend Stocks for investors. Compiling it and putting it together must have been a monumental task.

Thank you for sharing and thank you for including me!

Dividend Growth Investor

Thank you DGI. It definitely took a while to put everything together. 🙂

Always interesting to see the wide array of companies and picks in the personal finance community. Some of these I never even heard of.

Thanks for including me, appreciate it. Let’s all have a fantastic 2021.

cheers

You’re very welcome. Thanks for participating!