Warren Buffett is one of the best investors of all time and has offered many excellent quotes over the years. The quotes below are my all-time-favourites and our investment strategy revolves around them.

“If you aren’t willing to own a stock for 10 years, don’t even think about owning it for 10 minutes.”

“Only buy something that you’d be perfectly happy to hold if the market shut down for 10 years.”

“Our favourite holding period is forever.”

“It is wise for investors to be greedy when other investors are fearful and to be fearful when other investors are greedy.”

“Price is what you pay; value is what you get.”

“It is far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

As much as active trading gets a lot of attention, especially in today’s social media driven investing gurus & influencers world, there’s a lot of value in doing your due diligence in researching a stock, buying quality companies that are profitable and that you understand, and then holding them forever – be an owner!

As Buffett wisely noted, if you don’t plan to hold a stock for at least 10 years, you shouldn’t hold it for 10 minutes.

There is considerable debate about whether you should only invest in a stock if the share price hits a specific price. The belief is that you only want to invest in a stock when the stock price is below its intrinsic value. But the problem is if the stock never falls below this set price target, you may end up quibbling over eighths and quarters and never own the stock

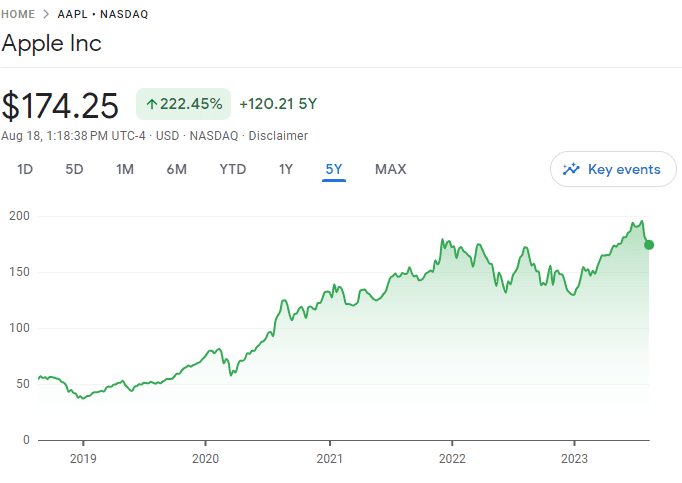

For example, imagine back in 2019 you missed the chance of buying Apple shares at around $50. For some reason, you decided that you won’t invest any money until Apple’s share price got below $55. The share price fell to about $57 due to global pandemic concerns in 2020. But because you have your mind set on this $55 price target, you decided that you’d wait longer.

Unfortunately, the price never went below $55 and Apple stock price has soared since then. You missed a chance to own a high quality profitable company…

Despite wanting to get a “great deal” on stocks, I have learned over the years to not lose sleep over a few cents on the purchasing price when I’m convinced that the company will continue to grow and increase revenues for years to come.

The key here is time in the market rather than timing the market!

With that in mind, some readers have asked me about my top five Canadian stocks to buy and hold, perhaps forever. I thought it’d make an interesting blog post.

Please note, I’m offering my list of five forever Canadian stocks because I believe they truly are the very best available. As well, I offer the list as a springboard for further discussions and debates. You might – amazingly – agree unanimously with my five forever stocks.

But that’s probably highly unlikely. Far more probable is you agree with some of them but you will argue about a favourite stock of your own has been left off the list.

Top five Canadian dividend stocks to hold forever

For the five Canadian stocks to hold forever, I decided to pick Canadian dividend stocks because of three key reasons – dividends provide a steady income to investors, companies tend to raise dividend payout over time to reward shareholders, and great companies will reward investors not only with increasing dividends but with share price appreciation over time as well.

Since it was nearly impossible to come up with just five Canadian dividend stocks to hold forever, I came up with five different options.

Option 1 – The Big Five Banks

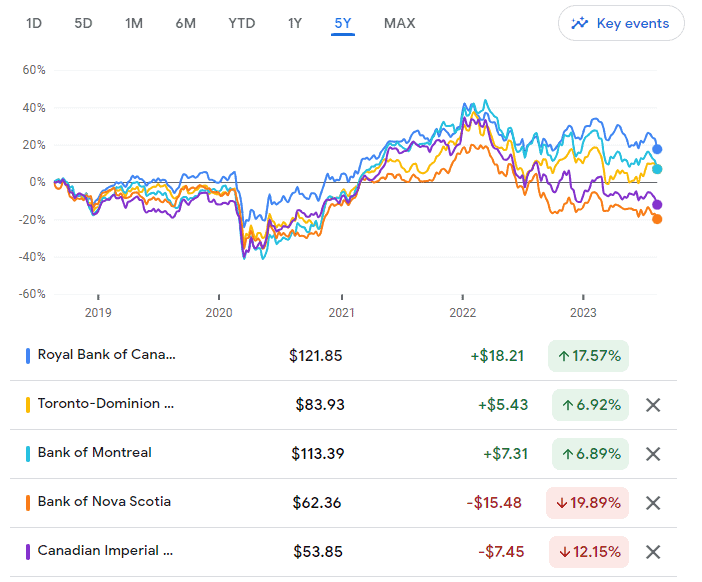

The first option is pretty obvious. The Big Fives – Royal Bank, TD, Bank of Nova Scotia, Bank of Montreal, CIBC all have been paying dividends since the late 1800s. They don’t always raise dividends every single year but these banks have been paying uninterrupted dividends since the late 1800s.

- Royal Bank – dividends since 1870

- TD – dividends since 1857

- Bank of Nova Scotia – dividends since 1833

- Bank of Montreal – dividends since 1829

- CIBC – dividends since 1868

If you ask me, that’s an extremely impressive feat!

These Canadian banks make up a large portion of the Canadian economy. I have no doubt that if any of these banks were to go bankrupt, the Canadian government would have to come and rescue the bank. There is simply too much money tied to the Canadian banks! So the likelihood of that happening is virtually zero.

As you can see, the share price performance has not been stellar over the last five years, mostly due to concerns with the Canadian housing market and mortgages. Last week during the earnings reports, all of the Canadian banks increased their PCLs, an indication that we may see a choppy performance in 2024.

At the time of the writing, the Canadian banks have historical low P/E’s. So if you’re wondering where you might invest your money, especially for the long term, you would be very wise, to look no further than the Big Five Canadian Banks. I firmly believe that a year or two from now, the share price will be significantly higher.

Essentially, I have no issue holding all five stocks forever. In fact, it is a no brainer to have at least a few of these Big Fives in your dividend portfolio.

Option 2 – TD, RY, FTS, ENB, CNR

For option 2, I decided to branch out and pick other than just five banks.

The picks are TD, Royal Bank, Fortis, Enbridge and Canadian National Railway. The reasons are below:

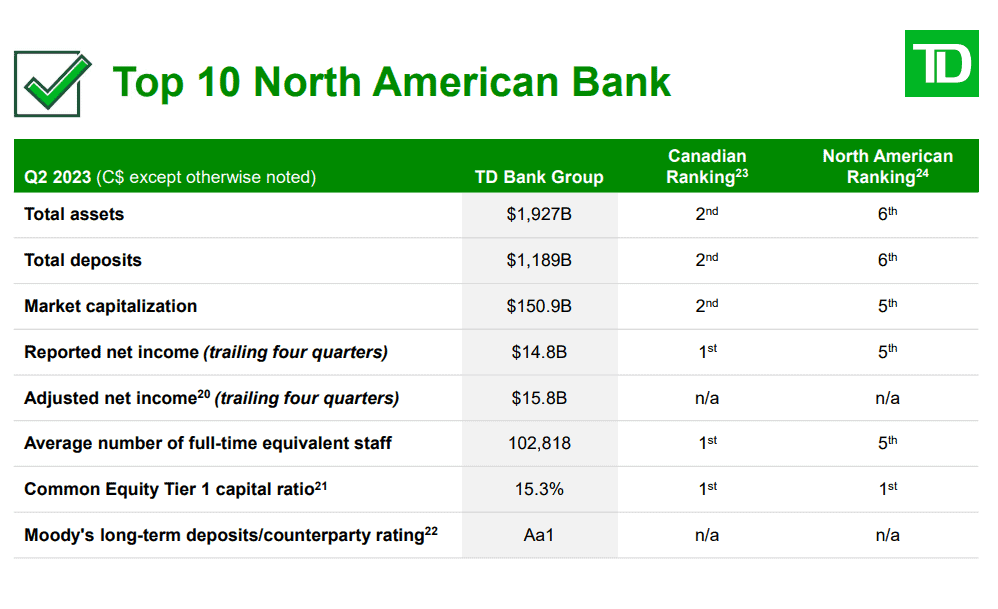

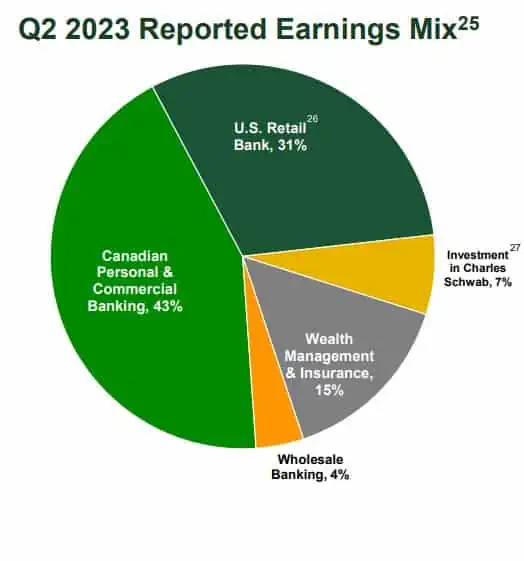

TD – As mentioned, TD has been paying uninterrupted dividends since 1857. TD is not only prominent in Canada, it is also one of the largest banks in the US. There’s absolutely no concern for me to hold TD shares for a very long time while collecting dividends and seeing the share price go up over time.

In fact, this is why we purchased a large quantity of TD shares during the global pandemic (381 shares between 2020 and 2022 for an average price of $64.53 CAD per share).

In addition to the impressive dividend history, TD has raised dividends for 12 straight years and has a 10 year annualized dividend growth rate of 9.4%.

Royal Bank – just like TD, Royal Bank has been paying uninterrupted dividends since the late 1800s. It is the largest bank in Canada with a presence in the US and internationally. In fact, Royal Bank is the 9th largest global investment bank.

RY has been a pillar in many investors’ portfolios and that shouldn’t come as a surprise.

Despite being the largest bank in Canada, Royal Bank has been growing new banking clients consistently over the years. Royal Bank recently announced it had agreed to acquire HSBC Canada which should further increase Royal Bank’s customer base in Canada.

Fortis – While Fortis is considered a very boring stock, it should be in every dividend investor’s portfolio because it is so stable – people in North America will continue to rely on Fortis to provide natural gas and electricity for their homes and businesses for many years – indeed, decades – to come.

Fortis has been paying dividends since 1972 and has a dividend growth streak of 49 years, the second longest for a Canadian dividend paying stock.

Needless to say, this is a very impressive streak. A regulated utility company like Fortis is nice because it continues to generate dependable growing dividends with an appreciating share price.

Enbridge – Enbridge has been paying dividends since 1953 and has been very friendly to shareholders, raising dividends for the last 27 years. With Canada producing so much natural gas and crude oil, there needs to be a way to transport these natural resources from point A to point B. This is where Enbridge’s vast pipeline network comes in handy.

Since it has become harder and harder to build new pipelines, the existing Enbridge pipelines are more valuable than ever. In addition to including Enbridge as one of the hold forever stocks, I have also included Enbridge as one of my best Canadian stocks.

While some investors are concerned that natural gas and crude oil will be replaced eventually by renewable energy, so they wouldn’t consider Enbridge as a hold forever dividend stock, I don’t agree with that. Enbridge has been investing money in renewable energy space such as wind and solar projects. I have no doubt Enbridge will be around for many decades to come.

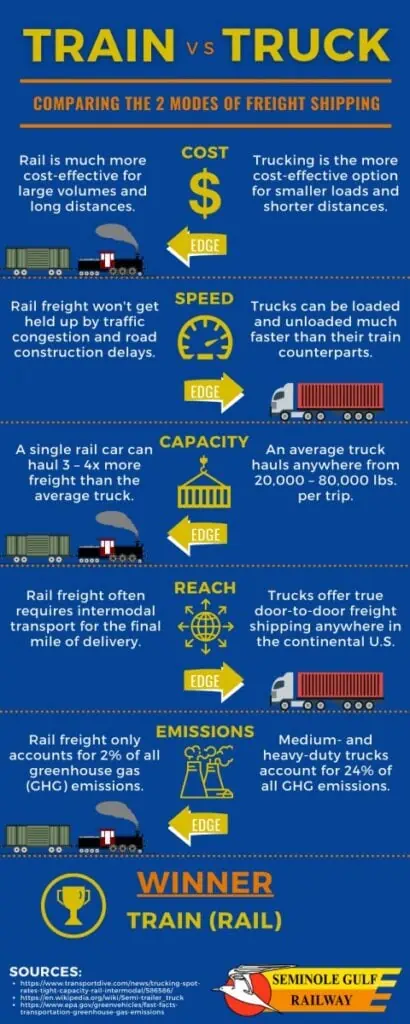

Canadian National Railway – Railways have been the backbone of North American expansions. BC only joined Canada when the federal government promised a railway linking BC to the rest of the country.

Despite the popularity of airplanes, rails still play a major role in the transportation of goods across North America. It is far more cost efficient to ship goods across North America via rail than any other method.

Side note: a quick research on the internet showed that rail shipping costs $70.27 per net ton while over-thee-road truck shipping cost is $214.96 per net ton. That’s a HUGE difference!

Canadian National Railway has been raising dividends for 27 straight years and it doesn’t look like the company will change this streak anytime soon. I am very comfortable holding CNR forever in our dividend portfolio.

Option 3 – TD, RY, FTS, CNR, BN

Option 3 is very similar to the previous option except I swapped out Enbridge for Brookfield Corporation.

For me, I see Brookfield Corporation as the Canadian version of Berkshire Hathaway. Brookfield has approximately $850 billion in assets under management spanning across different sectors – renewable, infrastructure, private equity, real estate, credit, and insurance solutions.

The Brookfield Corporation management team, and especially CEO Bruce Flatt (often referred to as ‘the Canadian Warren Buffett” – is focused on compounding capital over the long term and generating shareholders an annualized return of 15% or more. Since BN holds assets across different sectors and I am very confident in the management team, I have no concerns with holding BN for a very long time.

Note, BN isn’t your typical dividend stock because of the very low yield. However, the overall return (+15%) should make up for it.

Option 4 – TD, RY, FTS, ATD, WCN

For Option 4, TD, Royal Bank, and Fortis remain on the list. I added Alimentation Couche-Tard Inc and Waste Connections instead. Reasons being:

Alimentation Couche-Tard Inc – convenience stores aren’t going away anytime soon and Alimentation Couche-Tard is one of the global leaders in this particular sector with over 14,000 convenience stores across the globe.

Over the years, ATD has demonstrated an exemplary record of growth, both organically and through acquisition. Despite primarily being present in close proximity to a gas station, I was quite impressed that the management was front and centre with the EV transition and started offering EV chargers at some of the locations in Scandinavia. One of the key learnings is that the longer times in relation to chargers have led to an increase in traffic in ATD’s stores and a positive lift in sales. This is good news for Alimentation Couche-Tard.

Like Brookfield Corporation, ATD doesn’t have the highest dividend yield but its total return has been quite impressive. ATD has also been growing its dividend payout at an impressive rate with a 13 year dividend increase streak and a 10 year annualized dividend growth rate of 25.1%.

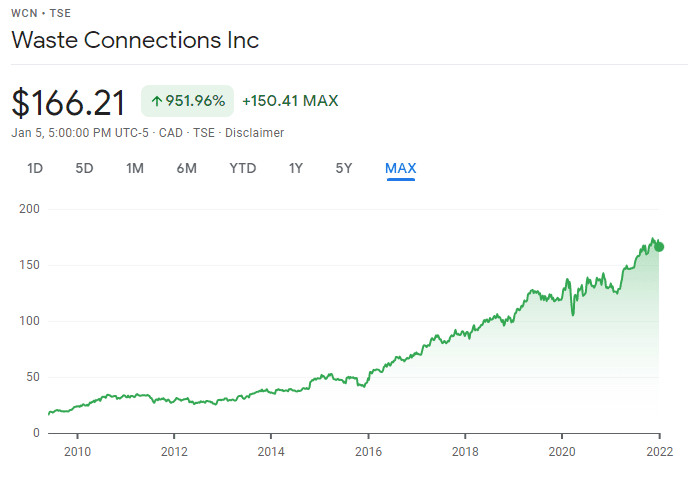

Waste Connections – death and taxes are two certain things in life. But I’d add a third one – garbage. We humans will continue to make garbage no matter what and there needs to be a way to dispose of this massive garbage. This is where Waste Connections come in.

WCN has been paying dividends since 2010 and has managed to raise dividend payout every single year since. Despite a low initial dividend yield, it has an impressive 10 year annualized dividend growth rate of 14.4%. More importantly, the stock has generated an impressive return since 2009.

Option 5 – TD, RY, FTS, T, IFC

I decided to include a couple more names in my top five Canadian dividend stocks to hold forever list. For Option 5, TD, Royal Bank, and Fortis remain on the list and I included Telus and Intact Financial.

Telus – what’s one thing we Canadians complain about a lot? High cell phone bills. So why not invest in one of the Canadian telecommunication companies and collect juicy dividend income?

Telus has been paying dividends since 1999 but the dividend history actually goes back further when it used to be called BC Tel. It also has an impressive record of raising its dividend, usually twice a year to the tune of about 7% combined.

Now due to financial challenges, we probably will see this 7% dividend payout rate to drop, but I have no doubt Telus will continue to raise dividend payouts, albeit at a lower rate.

Canadians will continue to rely on Telus’ services so I am convinced that Telus will do just fine over the long term. One of the major tailwinds that Telus – and the other Canadian telecommunication companies – enjoy is the record high immigration numbers.

When a million people are emigrating to Canada, they need a number of things, among the most notable is internet and phone service. I see Telus becoming like the utilities – stable yet boring.

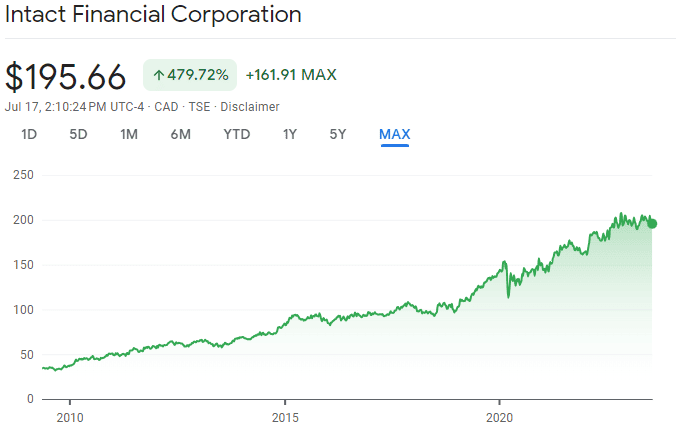

Intact Financial – Intact Financial was the first dividend stock that we purchased and it has done quite well over the years. Intact Financial is the largest provider of property and casualty insurance in Canada with an estimated market share of 20%.

The company has also been strengthening its position in the UK and Ireland over the years. While insurance isn’t the sexiest thing, people will continue to buy insurance products to protect themselves, their families, and their properties.

Intact Financial has a dividend increase streak of 18 years with a 15 year annualized dividend growth rate of 9.1%. Best of all, its stock price has been on a steady upward trend.

Top five Canadian dividend stocks to hold forever

It was a fun exercise to pick out the top five Canadian dividend stocks to hold forever. The stocks that I picked out all have a long dividend paying streak with a solid track record. I am pretty confident all of the stocks I have listed will continue to grow revenues and grow dividend payout for many years to come.

When investing in these hold forever Canadian dividend stocks, you can definitely sleep well at night, knowing your money is working hard for you. Again, time in the market is far more important than timing the market.

As you can see, there are many choices and I probably left out a few solid Canadian dividend stocks. Some may argue that you can swap out Intact Financial and insert Manulife or SunLife. That’s certainly up for debate.

Are there other Canadian dividend stocks that you’d buy and hold forever instead of the ones I’ve mentioned?

I’ve always avoided ENB. Some of the numbers scare me.

According to the Can Div All Star List PDF…

TTM payout 190%, Forecast payout 121%, Cash flow payout 87%, P/B 3.7. Debt/Equity 131%

Thanks for much for your site and newsletter, great stuff, I really enjoy it.

Jeff

Thanks Jeff.

Yes, Enbridge does have a lot of debt.

The way how we look at how the utlities companies pay out dividend from their cash flow is different from other companies. First of all, utilties companies including Fortis raises a lot of capital (cahs flow) through stock and debt issuance. If you look at their balance sheets, you would see increasing trend of debts and outstanding shares. However, utilities business are regulated industry where barrier of entry is completedly impossible. They have enjoyed incredible pricing power even though they do required regulatory approval from time to time on rate hike. Unless you want to live out in the woods and wildnerness you have no choice but using them on regular basis. There is complete different way to analyze their cash flow picture. In the case of Endbridge, they pay out their dividend from distributable cash flow and they target 60-70% of their distrbibutable cash flow. Also utilties business require heavy capital investment and a lot of the non-cash itesm are tied to amortizatin/depreciation which would not impact their cash flow. Same can be said for all the telecom which are different type of utilties that provide essential serives to millions of households. If you look at their earning and free cash flow vs the dividend they pay out, it would not make any sense at all. Due to the nature of their business, they can finance throught debt and stocks issuance.

Just adding to my previous replies, we are adding 500,000 new immigrants to Canada year over year. All these people would need utlties service from gas , hydro to internet. This would present them best case senario for getting lower cost of loans when it come to financing. These are over 1% of annual organic growth that all mongoploy and obiligopoly business would enjoy for years to come

A lot people only look at Buffett’s quotes but forget the context. Most answers/quotes were to answer specific questions. Some comments are for retail investors, some for institutional investors. Don’t treat those quotes as universal and one fit all situations

Agree with you William but these quotes provide some perspective for long term investing.

Love the article and reading your blogs only things I would add is I like emera ema.to over fortis and Bce.to bell over Telus however all are good for long term hold.

Thank you frank. Emera is a solid stock too.

I recently learned that my Dad sold Apple at $15 sometime in the 80s.

ARRRRRRRRGH

Well, Apple almost went bankrupt a few times back in the 80s, so don’t fault your dad for doing that.

thanks, i really enjoy articles like this!

Personally, I would swap out BM for MRU. A boring, defensive dividend stock that has increased its dividend for almost 30 consecutive years. I find a lot of us have a high percentage of financial services stocks in Canada, so supplementing in MRU, ATD and WCN makes a lot of sense.

I also like SJ. If you look at it’s earning and revenue growth over the past 10 years its really impressive. It also raised it’s dividend for close to 20 years. The Beta is low because of its focus on utility poles and railway ties.

You’re very welcome Stephen.

MRU is a solid pick too. SJ is an interesting pick, haven’t paid too much attention on SJ.

Interesting that Buffett buys and sells alot more than people think. I don’t pay much attention to his quotes about buy and hold, the punch card with 20 punches, etc… His actions don’t support that. There have only been a few stocks that he has held for 10 plus years and he said it was a mistake not to sell KO when it reached nosebleed levels.

**You spelled “Buffett” wrong in your article.

Oops, thanks for pointing that out.

Buffett buys and sells a lot more but they also have kept some stocks for a very long time. 🙂