Long-time readers know we are deploying a hybrid investing strategy – we invest in both dividend growth stocks and index ETFs in our dividend portfolio. For our kids’ RESPs, we have switched from multi-ETFs to a one-fund solution ETF to keep things straightforward. A one-fund solution ETF such as the Vanguard All-Equity ETF portfolio (VEQT) means there’s no need to re-balance regularly. Whenever you have new cash and want to buy more funds, all you have to do is to buy the one ETF. Life is much simpler that way.

Why are the all-in-one or the all-equity portfolio ETFs so great? There are some significant benefits they offer:

- Instant diversification – both geographically and asset class

- Low management fees in the fractions of a percent

- Easy to purchase via online discount brokers

- No need to re-balance regularly

- Hands-free portfolio management

For the most part, whenever I have coaching clients new to investing, I typically would recommend one of the one-fund solution ETFs to them. But the one-fund solution ETFs, like the VEQT, aren’t just for beginner investors, they can be great for seasoned investors too.

While I have written a comprehensive showdown between three all-equity ETFs – VEQT, XEQT, and HGRO, I wanted to write a VEQT review and do a deeper analysis of this Vanguard all-equity portfolio ETF.

Vanguard All-Equity ETF Portfolio – VEQT

The Vanguard All-Equity ETF Portfolio, VEQT, holds 100% in equity. This means that the ETF holds no bonds. This is the most aggressive portfolio ETF in Vanguard’s selections of all-in-one ETFs. Since VEQT holds 100% in stocks, some people may consider it as one of the riskier ETFs.

The objective of the Vanguard All-Equity ETF is to seek to provide long-term capital growth by investing primarily in equity securities. The ETF is traded on the Toronto Stock Exchange under the ticker symbol “VEQT” and is traded in Canadian dollars.

Compared to some other popular index ETFs traded on the TSX, VEQT is a relatively new ETF. It was created early in 2019. Some key facts of VEQT:

- Inception Date: Jan 29, 2019

- Eligibility: RRSP, RRIF, RESP, TFSA, DPSP, RDSP, taxable

- Dividend Schedule: Annually

- Management Fee: 0.22%

- MER: 0.25%

- Listing Currency: CAD

- Exchange: Toronto Stock Exchange

- Net Asset: $654.5M

- Number of holdings: 4

- The number of stocks: 12,607

- Median Market Cap: $131.6B

- Price/Earnings Ratio: 19.4

- Price/Book Ratio: 1.7

- Return on Equity: 11.4%

- Earnings Growth Rate: 9.4%

VEQT Fees

VEQT has a management expense ratio (MER) of 0.25% which is quite low compared to the average mutual funds available to Canadians. In fact, I remember paying around 4% MER for some actively managed mutual funds in the early days of my investment career (never again!)

In comparison, Robo-advisors like Wealthsimple and Questwealth Portfolios, charge anywhere from 0.2% to 0.5% of management fees. These management fees are on top of the ETF fund management fees that you pay, so fees can add up quickly.

The beauty of ETFs, like the VEQT, is that you can easily manage on your own by utilizing a discount broker like Questrade. Questrade also offers commission-free ETF trading, so you don’t have to pay any commissions when you purchase an ETF like VEQT.

Of course, Wealthsimple Trade also offers commission free tradings. For Canadian investors, it’s great we have more discount brokers options available in recent years. Check out my Questrade vs. Wealthsimple Trade review.

VEQT Underlying Holdings

VEQT holds a vast amount of stocks, over 12,000 in fact. To hold these stocks and manage them all, VEQT holds four underlying Vanguard funds. They are:

- Vanguard US Total Market Index ETF (VUN) – 41.00%

- Vanguard FTSE Canada All Cap Index ETF (VCN) – 29.8%

- Vanguard FTSE Developed All Cap ex North America Index ETF (VIU) – 20.9%

- Vanguard FTSE Emerging Markets All Cap Index ETF (VEE) – 8.30%

Although VEQT is supposed to be an all-equity ETF, it holds a small percentage (0.04%) of its assets in short-term reserves and cash.

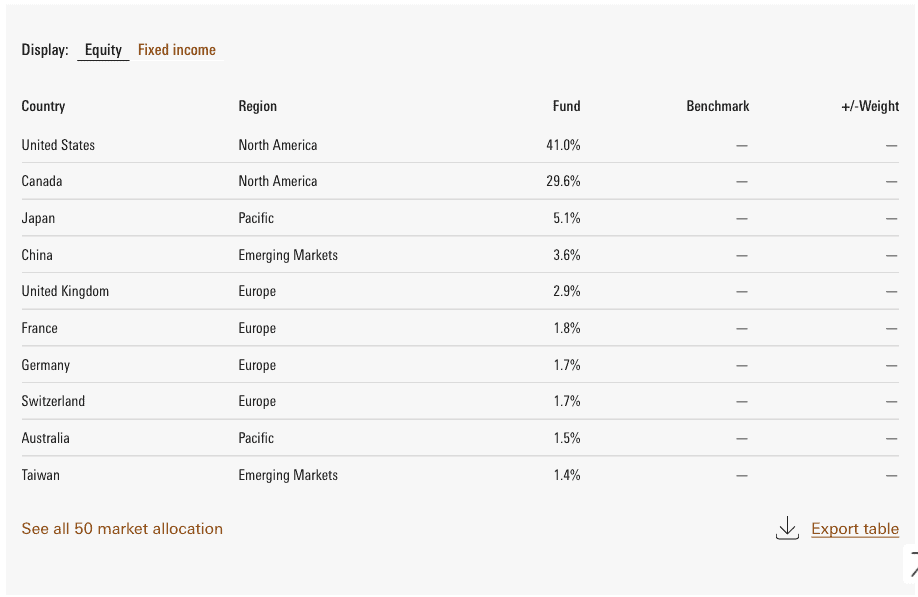

VEQT Top 10 Market Allocation

Here is VEQT’s top 10 market allocation:

- US: 41.0%

- Canada: 29.6%

- Japan: 5.1%

- China: 3.6%

- UK: 2.9%

- France: 1.8%

- Switzerland: 1.7%

- Germany: 1.7%

- Australia: 1.5%

- Taiwan: 1.4%

VEQT has more exposure than just 10 countries. In fact, VEQT holds stocks from 50 different markets.

As we can see, VEQT has a large exposure to the North American market with over 40% of its fund exposed to the US market. But this makes sense given many mega international companies are based in the US, for example, Apple, Microsoft, Amazon, Tesla, Coca-Cola, Procter & Gamble, Johnson & Johnson, etc.

The exposure to each country listed above will vary slightly month over month but generally, the order should stay relatively consistent. For example, I wouldn’t expect VEQT to suddenly have a 10% allocation to Germany.

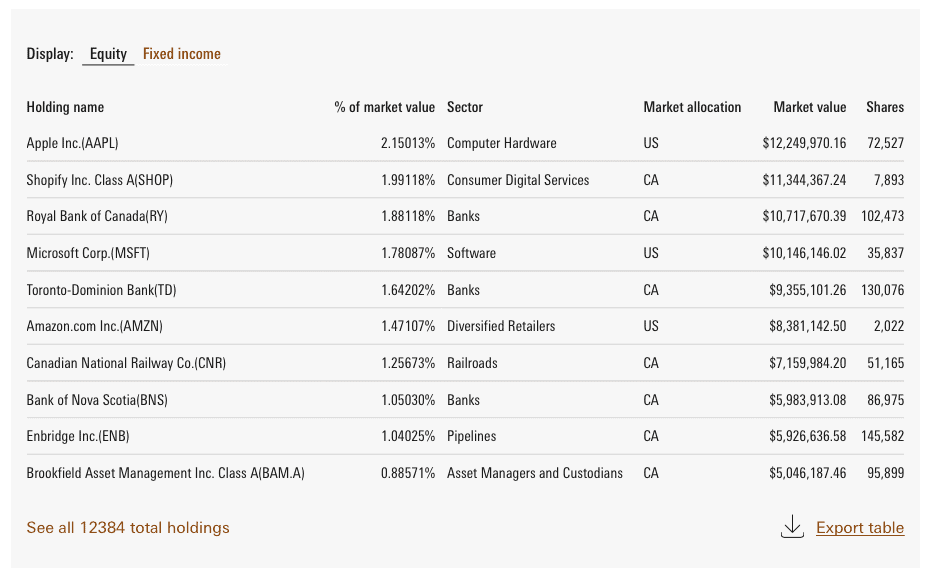

VEQT Top 10 Holdings

Because of the high North American exposure and high exposure in Financial Services and Technology, I was curious to find out about VEQT’s top 10 holdings.

- Apple: 2.15%

- Shopify Inc: 1.99%

- Royal Bank: 1.88%

- Microsoft: 1.78%

- TD: 1.64%

- Amazon: 1.47%

- Candian National Railway: 1.26%

- Bank of Nova Scotia: 1.05%

- Enbridge: 1.05%

- Brookfield Asset Management Inc: 0.89%

I was a little surprised that Alphabet, Facebook and Tesla aren’t on VEQT’s top 10 holding list. But I guess that makes sense given the underlying holdings use a market cap approach for stock selection and exposure. In case you’re curious, Facebook is #11, Alphabet is #18, and Tesla is #39.

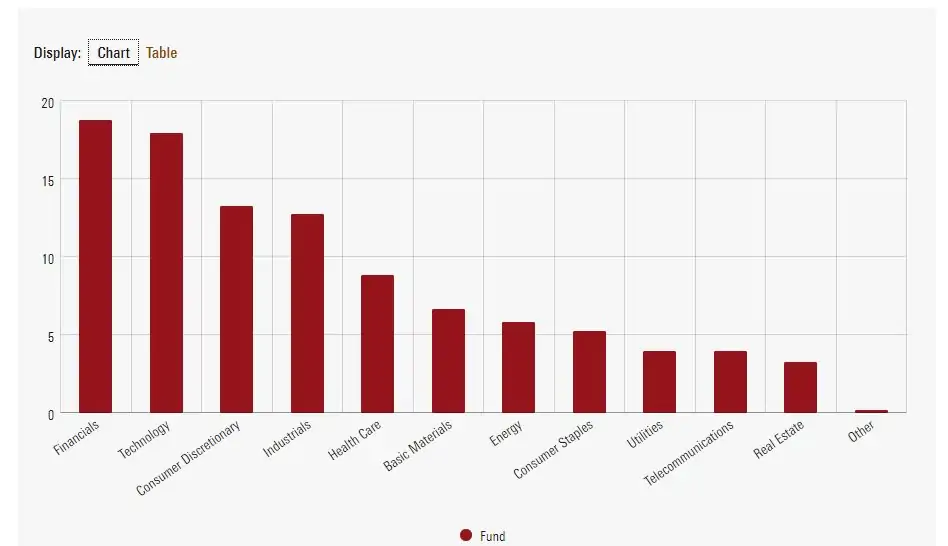

VEQT Sector Exposure

In terms of sector exposure, VEQT has somewhat a balanced exposure with Financial Services and Technology taking the lead.

- Technology: 18.5%

- Financials: 18.5%

- Consumer Discretionary: 13.2%

- Industrials: 12.4%

- Health Care: 9.0%

- Basic Materials: 6.6%

- Energy: 6.0%

- Consumer Staples: 5.0%

- Utilities: 3.9%

- Telecommunications: 3.8%

- Real Estate: 3.1%

- Others: 0.0%

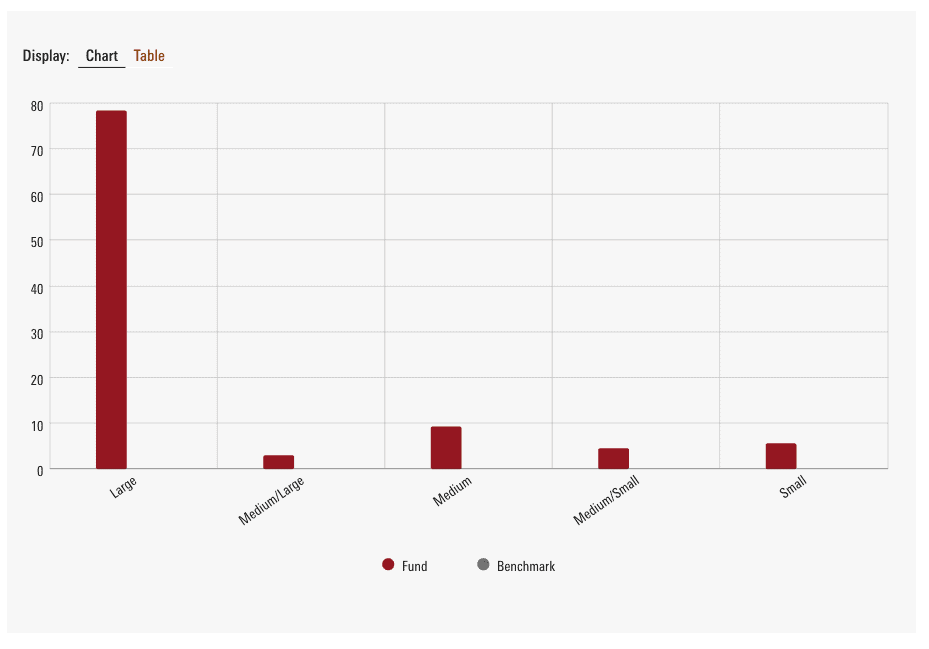

VEQT Market Capitalization

Most of the stocks that VEQT holds are large cap stocks, but VEQT does hold some mdedium and small cap stocks.

- Large: 78.21%

- Medium/Large: 2.89%

- Medium: 9.19%

- Medium/Small: 4.25%

- Small: 5.46%

VEQT Returns

Given that VEQT is a relatively new ETF, there’s no long historical data we can use to gauge the fund return history. As of Jan 31, 2021, VEQT has a 1 year return of +10.91% and a +13.31% return since inception.

In comparison, the S&P 500 has a 1 year return of 17.34%, the Dow Jones Average has a 1 year return of 7.61%, and the TSX has a return of 3.3%.

VEQT Distributions

Unlike the typical dividend stocks and many index ETFs, VEQT pays distributions annually. The dividend in 2020 respectively was $0.403751 per share. At the current VEQT stock price, this is equivalent to around a 1.2% yield.

Foreign Withholding Taxes with VEQT

When it comes to holding an ETF that has exposure to the US market, we definitely have to consider the 15% withholding taxes that the US government charges on any dividends paid to Canadians. The fund would take care of the withholding taxes when it pays out any distributions. If you hold an ETF with US exposure that pays dividends inside TFSA, RRSP, or RESP, you won’t be able to recover any withholding taxes paid. If you hold the ETF in a taxable account, however, you can recover a portion of the withholding taxes by getting foreign tax credits.

The Canadian Portfolio Manager blog has an excellent Foreign Withholding Tax Calculator on determining what the VEQT’s expected foreign withholding tax is when held in the different accounts.

According to the calculator, VEQT has the following tax drag in the different accounts:

- TFSA: 0.22%

- RRSP: 0.22%

- RESP: 0.22%

- Taxable: 0.02%

One thing to remember is that the foreign withholding taxes, or “tax drag”, needs to be calculated on top of the MER. So, considering VEQT’s MER of 0.25% that means the overall tax drag for the different account are:

- TFSA: 0.47%

- RRSP: 0.47%

- RESP: 0.47%

- Taxable: 0.27%

In other words, it may be more beneficial to hold VEQT in a taxable account. But you also have to consider capital gains if you do end up selling VEQT in the future. Please always consult a tax specialist when it comes to tax planning and investment tax efficiency.

VEQT Review – Pros and Cons of VEQT

There are always pros and cons of any investment and VEQT is no different. As part of the VEQT review and a deep analysis of the ETF, I believe it’s important to go over the pros and cons.

Pros of VEQT

There are lots of pros of VEQT.

- 100% in stocks targeting long term growth

- Instant diversification by holding over 12,000 international stocks

- International exposure over 50 international markets

- Asset class diversification

- Low Management fees

- No need to re-balance regularly

- Hands-free portfolio management

- Commission-free purchase when a broker like Questrade

Cons of VEQT

It’s hard for me to come up with cons of VEQT but when I really think about it, I did find some.

- 100% in stocks can mean more volatility

- Slightly more fees in the long run compared to the multi-ETFs approach. For example, holding VCN and XAW.

- There might be a slightly cheaper all-equity ETF available

Vanguard VEQT vs. Other Vanguard ETF Funds

With so many Vanguard ETFs available, readers might wonder, how does VEQT compare to these other Vanguard ETF funds?

VEQT vs. VGRO

VEQT holds 100% in equity whereas VGRO holds 80% in equity and 20% in bonds. In other words, VEQT can be seen as the more aggressive of the two ETFs. If you’re not comfortable holding 100% in equity, VGRO is a good ETF to hold. You can check out my All-in-One ETF in Canada comparison here.

VEQT vs. VCN/VCE

VCN, the Vanguard FTSE Canada Index ETF, and VCE, the Vanguard FTSE Canada Index ETF, both only track the Canadian market. While VCN and VCE provide great exposure to the Canadian equity market, both are lacking in international exposure. If you’re looking for international exposure while holding 100% in equity, look no further than VEQT.

VEQT vs. VFV

VFV is the Vanguard S&P 500 Index ETF that tracks one of the US stock market indices. VFV has an extremely low management fee of 0.08%. However, since VFV only invests in US stocks, it is a lot less diversified than VEQT.

VEQT vs. VXC

The Vanguard FTSE Global All Cap ex Canada Index ETF, VCX, holds stocks outside of Canada. VXC is a great fund to hold if you already hold Canadian individual stocks or a Canadian index fund like VCN or VCE. Check out here for my comparison between VXC and XAW. However, if you want a one fund solution that covers the globe and are willing to pay a little more in management fees, VEQT is a great option.

Given that many of the multi-billion international companies are based in the US, holding VFV provides a decent amount of international exposure. However, you are definitely missing out on additional international exposure compared to VEQT.

Who should buy VEQT?

Who should buy VEQT?

- If you want an all-in-one portfolio that invests 100% in equity

- If you want exposure to all the major global markets

- If you don’t want to tinker and re-balance your portfolio regularly

- If you are comfortable with higher risk and volatility because of the 100% equity exposure

I believe VEQT is a great index ETF to hold for most Canadian investors.

Summary – VEQT Review

Although VEQT is a relatively new ETF, the fund has performed relatively well since its inception. If you can tolerate risk and volatility, I think VEQT is a great all-equity ETF for both beginner and experienced investors. VEQT isn’t the only all-equity ETF available to Canadians, iShares and Horizons both offer similar all-equity ETFs. You definitely want to compare all three before picking an all-equity ETF to purchase. You may want to take a look at my in-depth XEQT review.

What I really like about VEQT is its simplicity. By holding one ETF, you get instant asset class diversification and geographical diversification. There’s no simpler way to hold over 12,000 individual stocks.

My review of VEQT is very positive. For many investors, I think VEQT definitely belongs to their investment portfolios.

Hello. Thanks for this article.

I compared on portfoliovizualiser 3 pf with 100 % veqt, 100. % hgro and 100 %ZGQ (BMO quality worldwide)

Initial. Final CAGR. Maxdrawdown

100VEQT $100,000 $127,562 15.73% -17.91%

100HGRO $100,000 $140,012 22.38% -17.54%

100ZGQ $100,000 $139,431 22.07% -10.08%

Between oct2019-may2021.

Max dd si really better on ZGQ ? Whatdo tou thons about that ?

Did you see this? https://www.tawcan.com/all-equity-etfs-veqt-xeqt-hgro/

Hello,

yes I do. But what tom compare VEQT and ZGQ ? CAGR is really different and max drawdown 10 % instead of 18 from 2019 to 2021.

thanks

francois

Hey Bob,

Great review. I prefer an overall ( after taxes) approach. Corporate class ETF from HGRO or HXS / HXQ combo. All Capital Gains as I choose to withdrawal on demand. I looked to go 100 % equity but thought I would get better returns with higher percentage of Nasdaq and S & P 500 than Cdn TSX. Am I wrong?

The Horizons swap method is interesting for sure. Not sure if the CRA will audit this potential tax loophole or not.

Hi Bob, unrelated to this article, but any thoughts on doing a Bitcoin write up? I realize it’s a pretty polarized topic these days but just wanted to get your thoughts on it. I have 1% of my portfolio invested in it, but that is more what I consider a gamble that I am willing to take than my typical investing strategy. Thanks, and happy new year!

I haven’t paid too much attention on Bitcoin so that’s not in my expertise. You might be able to find better info from another site. 🙂

I love VEQT as a one-fund formula.

Now that my registered accounts are maxed, I’m contemplating going with VEQT vs. doing individual Canadian stock.

VEQT is definitely the easier to go IMO.

Another major con which should not go unspoken. 30% of the holdings are in Canadian companies! Canada’s economy only makes up ~4% of world GDP so it makes no sense to me to have 30% of your holdings in Canadians companies. I do love these all in one funds for their simplicity but I cannot invest in them due to their weightings. 30% may make sense to many others and that’s great, go for it. But that’s screaming home country bias to me.

That’s a fair comment Court. Ideally holding more international stocks would be nice. I guess that’s where XAW comes in handy.

“If you are comfortable with higher risk and volatility because of the 100% equity exposure”

if risk is a worry one shouldn’t be investing .. period

because … investing is long term and as we all know long term good stocks do very well

and the whole idea of this great fund is to buy and forget

thanks Bob

You’re welcome.

When companies create funds of funds, do you actually pay two layers of fees? So in this case, you’d be paying the .25% for the underlying funds and the 0.25% for the umbrella fund?

Nope just one fee set of fees. So 0.25% for the umbrella fund.

When you say “fees”, it’s the MER, right? You don’t actually pay the MER, but the NAV or market price of the ETF is already net after deducting the MER. So in this case, since VEQT tracks 4 ETFs, the NAV or market price of VEQT is net of MER of the 4 ETFs and then net of the MER of VEQT. So yes, indirectly one does “pay” the fees twice, but really doesn’t matter because the MER is not separately charged.

When I say fees it’s the overall fees you pay. The fees are built in as part of the ETF (i.e. overall performance less fees = net ETF performance)

But you never really pay any fees when buying and selling an ETF, other than trading commissions if applicable based on brokerage. Same with any mutual fund (except for front load or sales charges if applicable). All ETFs and DIY (Do-It-Yourself) No Load mutual funds have no fees! They have “MER” (Management Expense Ratio) that is deducted already in the NAV or market price. The performance of an ETF or MF is already net of fees!

And as far as VEQT, the MER gets taken twice, once from the underlying funds, and once from VEQT itself. That’s how Vanguard and Blackrock make money!

The fees are built in as part of the ETF and yes there’s no any extra loads with these ETFs. I updated my previous comment for clarification.