Welcome back to Part 3, and the final part of our 1H 2023 dividend portfolio review. I analyzed 31 out of 49 holdings earlier this month.

In case you missed the previous analysis, please take a look:

This week I will wrap up the review. In addition to the review, I will review the top 10 holdings of our dividend portfolio.

1H 2023 dividend portfolio review – Part 3

Like the previous two parts, I am being completely honest with my analysis and not sugarcoating anything. Here are my thoughts on the rest of the holdings in our dividend portfolio.

32. Procter & Gamble (PG)

Procter & Gamble is another juggernaut in the consumer staples sector. We originally started a position to increase our diversification in the consumer staples sector. Remember, there aren’t too many consumer staple companies in Canada.

We have added more PG shares throughout the years but we don’t have quite enough to enroll in DRIP yet. It would certainly be nice to add enough shares in the near future to allow us to drip one share each quarter.

Therefore, we plan to add more PG shares as buying opportunities surface.

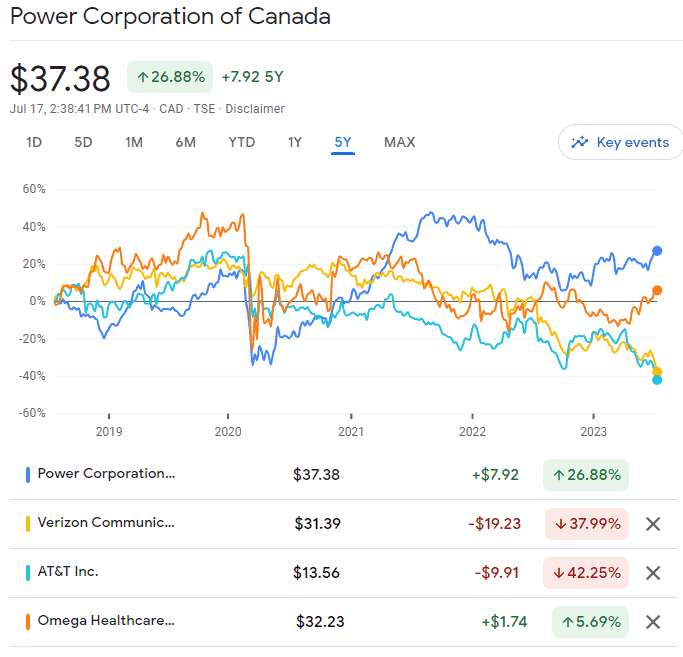

33. Power Corp of Canada (POW.TO)

Power Corp has a solid 5%+ dividend yield but has offered very little in terms of share price appreciation.

Does this mean POW falls into the dividend yield track category?

Well, not exactly. When compared to some yield trap stocks like Verizon, AT&T, and Omega Healthcare, POW actually performed quite well.

For a large management and holding company that focuses on financial services globally with core holdings in insurance, retirement, wealth management, and investment management, I’d have thought POW would have had a better performance in the last five years. But I guess I have been disappointed.

Despite the slight disappointment, I think POW is one of those stocks that we can continue to hold, collect dividends, and wait for the stock price to appreciate. Yup, that’s the beauty of dividend investing – you can wait and collect dividends; not something you can do with non-dividend paying stocks like Shopify and Amazon.

34. Qualcomm (QCOM)

It is well known that there was a significant supply constraint during the global pandemic. Semiconductor and RF parts that Qualcomm makes were very difficult to come by with lead time up to more than 40 weeks.

To secure parts, many Qualcomm customers over-purchased parts to protect themselves from the ridiculous component lead time. As the supply constraint situation improves this year, many Qualcomm customers found themselves overstocked with Qualcomm parts.

This means Qualcomm is facing a bit of short term headwind (i.e. customers aren’t ordering as many parts from Qualcomm), which will negatively impact its 2023 revenues.

But I think this will improve by later this year and early next year. Furthermore, let’s not forget that Qualcomm makes A LOT of money from royalties (i.e. Qualcomm Technology Licensing). It is estimated that Qualcomm makes anywhere from 3-5% on top of its device cost. That’s pure profit for Qualcomm!

Another thing that may negatively impact Qualcomm is Apple. Apple still uses Qualcomm chips on iPhones but there are rumours that Apple is working on its own 5G chipsets. If this were to happen, Qualcomm will lose a lot of revenue.

It doesn’t make sense to sell Qualcomm shares or close out our position right now given Qualcomm’s share price is near the 52-week low. For now, we plan to hold onto Qualcomm shares and re-evaluate later this year or early next year.

35. RioCan REIT (REI.UN)

Although RioCan raised its dividend payout recently, the dividend amount is not yet back to the pre-pandemic level.

While I think the shopping mall business is solid and RioCan is well-managed, the lack of dividend increases from RioCan is a bit concerning.

We need to seriously consider reducing the number of RioCan shares or possibly closing out this position altogether and reinvesting the money elsewhere.

36. Royal Bank (RY.TO)

One of the largest banks in Canada with exposure internationally as well, Royal Bank is one of our long term holdings and we are dripping more shares each quarter.

I think Royal Bank is quite attractive at the current price level so we plan to buy more Royal Bank shares. I have absolutely no concern with Royal Bank getting bankrupt and going out of business like what we’ve seen with some US regional banks.

If Royal Bank were to get into financial trouble, Canada as a nation would be in A LOT of trouble. The Canadian government would definitely have to bail out the company. Given Royal Bank’s long history and has paid dividends since the late 1800s, I do not see this ever happening though.

37. Starbucks (SBUX)

A well-recognized global brand and people will go to Starbucks and get their daily dose of caffeine religiously (some call this daily ritual the daily Starbucks sin!).

Starbucks has faced its own challenges over the past few years but the company is slowly turning things around. Although Starbucks isn’t setting profit records like Apple and other high-octane growth companies, it is improving its operational efficiency in order to improve overall profitability.

While Starbucks doesn’t serve the best coffee, what amazes me is people flock to Starbucks stores globally. I was one of those people that would head to a Starbucks in Asia instead of trying the local brands. When I was in Taiwan and Hong Kong in May, I was amazed how packed Starbucks stores were compared to other local coffee shops. This is a demonstration of Starbucks’ brand power!

Starbucks is a relatively small holding for us and has done well for us over the years. We plan to continue to hold it.

38. SmartCentres REIT (SRU.UN)

SmartCentres REIT has 188 properties across Canada with 114 Walmart-anchored centres so the business is quite stable. However, just like Dream Industrial and RioCan, SmartCentres hasn’t raised its dividend for a few years (the last time was in 2019). Unlike RioCan though, SmartCentres did not cut dividends during the pandemic despite lower rent collections.

The share price is near a 52-week low but with the higher interest rates, I’m optimistic the share price will recover.

We’re patiently waiting for a dividend increase from SmartCentres REIT. For now, we’re dripping and adding more shares each month. We may need to consider trimming some SmartCentres shares and reinvesting the money elsewhere for better overall growth.

39. Suncor (SU.TO)

We sold a large number of Suncor shares in 2020 and 2021 right after the dividend cut. Since then Suncor has raised dividends and the payout amount exceeds the pre-pandemic level. We kept the remaining few hundred shares instead of closing out the position altogether.

Suncor share price has struggled the past year mostly due to lower crude oil prices. Unfortunately, that’s the cyclical nature of oil stocks.

The dividend yield is pretty decent and Suncor has grown its dividends since the cut. Since this is a relatively small position, we have no plan to do anything. We’ll leave it alone and collect dividends every quarter.

40. Telus (T.TO)

Canada has one of the highest cell phone rates in the world. Telus benefits from this. Like Bell, Telus’ share price has struggled this year, mostly due to higher interest rates as Telus builds up its 5G network across Canada (i.e. Telus taking on debt).

Telus is very shareholder friendly and has raised dividends consistently (twice a year, between 7-10% combined, although we’ll have to wait and see whether Telus raises dividend payout in the 2H of 2023 given the revenue struggles).

We plan to add more Telus shares in the future. The recent share price drop has created a good potential buying opportunity for long term Telus shareholders.

41. TD (TD.TO)

TD is one of our top ten holdings and one of our long term holdings. No concerns or issues holding TD at all.

TD pulled out the planned Memphis-based First Horizon acquisition on May 4 and stated that it will probably find itself shut out of any US retail banking acquisitions for the next five years due to regulatory problems. But given the banking concerns in the US, this may be a blessing for TD.

TD is a solid stock to buy and hold. At the current share price, I believe TD is discounted and we’d like to add more shares and take advantage of the buying opportunity.

42. Target (TGT)

A relatively small position in our portfolio, so not really concerned with how Target is doing recently. We hold Target so we have exposure to the consumer staples sector.

Target is facing a bit of headwind when it comes to profitability. The company certainly isn’t doing as well compared to during the global pandemic. However, I believe Target has laid a strong foundation for long-term growth. It continues strengthening its same-day services to make it convenient for its customers.

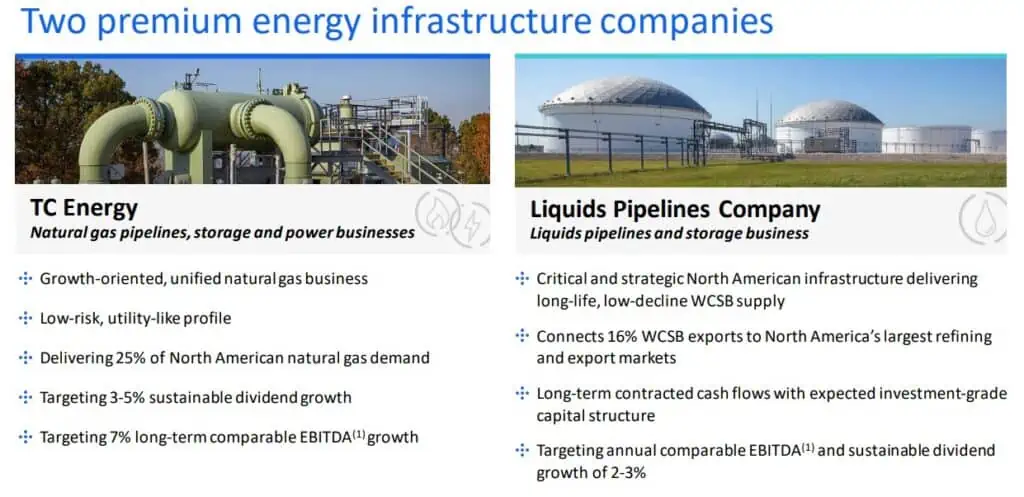

43. TC Energy (TRP.TO)

We hold TC Energy for pipeline/energy exposure specifically. North America will continue to rely on TC Energy’s network of pipelines to transport natural gas/crude oil from point A to point B.

The share price has done poorly this year largely due to the combination of massive cost overruns on the Coastal pipeline and higher interest rates.

However, I believe that TC Energy is investing money in renewable natural gas production by turning biowaste into natural gas and agricultural fertilizer while reducing carbon emissions each year.

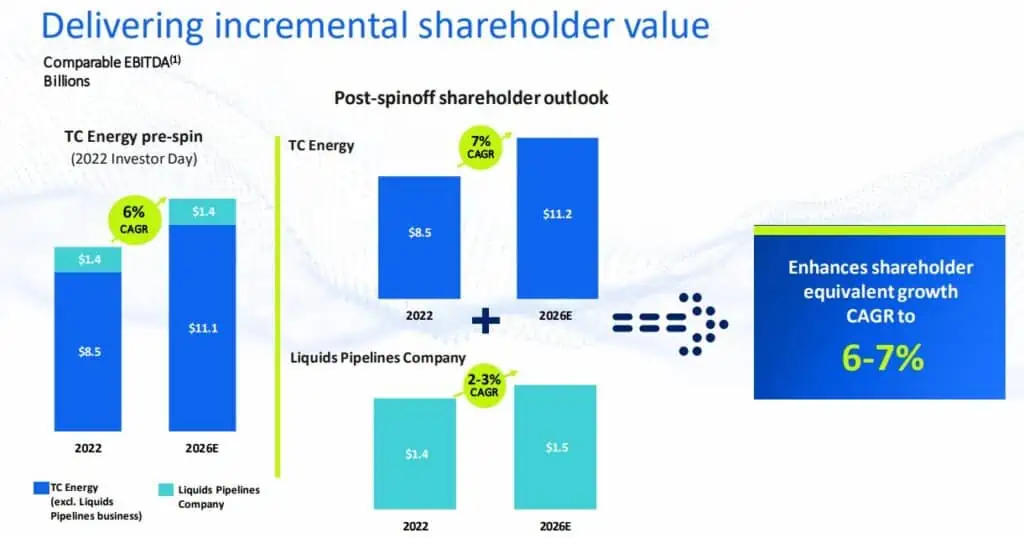

TC Energy recently announced intention to spin off Liquids Pipelines business and separate into two independent, investment-grade, publicly listed companies. Overall I think this is a good move for the company and should unlock values for shareholders.

According to TC Energy, shareholders will be able to retain TC Energy shares and pro-rata allocation of common shares in the new Liquids Pipelines Company. Since the target to close this spin out is in the second half of 2024 so we don’t need to decide what to do yet. For now we’ll continue to hold TC Energy and re-evaluate what with TC Energy and Liquids Pipelines Company shares late next year.

44. Visa (V)

Another one of our top holdings that just chugs along and continues to make money. Whenever we do have some USD sitting around, we plan to add more Visa shares. The low dividend yield isn’t a concern to me since Visa has been raising dividend payout for 15 straight years with a 10-year dividend growth rate of over 19%.

Visa is one of those low dividend yield high dividend growth stocks that offers a lot of capital growth. I think every dividend growth investor should consider owning Visa in their portfolio for growth reasons.

45. VICI Properties (VICI)

VICI Properties is a niche REIT company that invests in real estate assets across leading gaming, hospitality, entertainment, and leisure destinations. It owns a large percentage of the properties on the Las Vegas Strip, including Caesars Palace, MGM Grand, Excalibur, Luxor, and Venetian Resort. With Las Vegas becoming an increasingly popular vacation destination, I really like where VICI is going.

We own enough VICI shares to drip an additional share each quarter. We will drip and let things roll.

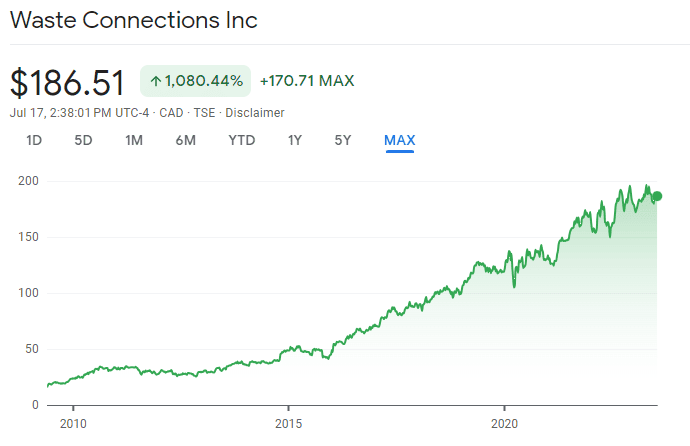

46. Waste Connections (WCN.TO)

We started a position in Waste Connections in recent years because we like the waste disposal business.

Although the yield is very low, Waste Connections has raised dividends for 13 years straight with a 10-year dividend growth rate of 14.4%. We are counting on WCN to continue raising its dividend payout at an impressive rate and the share price to continue to grow.

47. Waste Management (WM)

We’ve done really well over the years with Waste Management. The business model is very simple and straightforward – collect and dispose of garbage from homes and businesses, then produce and sell power using that garbage whenever possible.

We will definitely continue to hold WM shares. The only mistake we made with WM was not buying more shares initially!

48. Walmart (WMT)

Another consumer staple in our portfolio for diversification purposes.

Walmart makes a very small percentage of our portfolio so generally we don’t pay too much attention to it and just leave it on auto-pilot.

Since it’s difficult to own non-US company stocks, we use XAW to increase our international exposure. Holding XAW also helps with asset diversification as well.

XAW is one of our long term holdings and we plan to add more shares regularly by taking advantage of Questrade’s no-commission ETF trading.

Dividend Portfolio – Holdings to close or trim

After reviewing each holding, here are some of the holdings we may close out or trim in the future.

- Algonquin Power & Utilities (AQN.TO)

- Bank of Nova Scotia (BNS.TO)

- CIBC (CM.TO)

- Dream Industrial REIT (DIR.UN)

- Manulife Financial (MFC.TO)

- Magna International (MG.TO)

- Qualcomm (QCOM)

- RioCan REIT (REI.UN)

- SmartCentre REIT (SRU.UN)

As you can see, many of them are REITs. While REITs have a high initial yield, they don’t typically raise dividend payout regularly. This is fine if you’re aiming for a consistent income but it won’t protect you from inflation.

As we get closer to FI, our new cash investment will most likely slow down. Therefore, we need to rely more and more on organic dividend growth. So it makes sense to focus more on the higher dividend growth stocks instead of REITs.

Here are some of the holdings we may consider to add more shares.

- Apple (AAPL)

- AbbVie (ABBV)

- Brookfield Asset Management (BAM.TO)

- Brookfield Renewable Corp (BEPC.TO)

- BlackRock (BLK)

- Bank of Montreal (BMO.TO)

- Brookfield Corporation (BN.TO)

- Canadian National Railway (CNR.TO)

- Costco (COST)

- National Bank (NA.TO)

- PepsiCo (PEP)

- Procter & Gamble (PG)

- Royal Bank (RY.TO)

- Telus (T.TO)

- TD (TD.TO)

- iShares international ex-Canada index ETF (XAW.TO)

Phew, that’s a long list! We’ll be busy saving money and investing for sure!

Dividend Portfolio – Top 10 holdings

At the time of writing, the top 10 holdings in our dividend portfolio are (not in order)

- Apple

- BCE

- Canadian National Railway

- Costco

- CIBC

- Enbridge

- National Bank

- Royal Bank

- TD

- XAW

These holdings make up anywhere from 3 to 7% of our dividend portfolio with most of them around 5%. As you can see, we are a bit heavy with Canadian banks so it’s probably a good idea to trim some Bank of Nova Scotia and CM shares to reduce our overall exposure to the Canadian banks. We plan to continue to add Apple, CNR, Costco, and XAW to further reduce our exposure to the financial sector.

Summary – 1H 2023 dividend portfolio review

Wow, this dividend portfolio review turned out to be much longer than I originally envisioned. Because it’s so long, I broke it up into three parts.

I’m a true believer that we can learn something new every day. By doing a review of every single holding of our portfolio, I certainly have learned a couple of new things. Furthermore, it helps me rationalize which holdings we should consider trimming or closing and which holdings we should consider adding more.

As we move closer and closer to our goal of living off dividends, I think we need to continue to hold a mix of high yield low dividend growth stocks and low yield high dividend growth stocks. We plan to focus more on higher dividend growth stocks so we can continue to grow dividend income organically.

As much as dividend income is great and helps with an investor’s psychology, total return matters more in the long run. We want to collect dividends and have our capital grow as well.

Total return for the win!

I hope readers have found this review useful. I’d love to hear your thoughts, please leave them in the comments below.

Happy investing everyone!

Historically BNS and CM have underperformed when comparing to the other banks, particularly RY, TD and even NA. I have all of them LOL. I have been buying many of the BTSX stocks because they are priced low right now, but I don’t want to be too overweight in BNS and CM. RY and TD have typically had a better business model. I’m more confident in BMO than BNS and CM. CM has a habit of making the wrong decisions or being caught poking their eyes out routinely. 🙂

AQN is one I might trim because of the dividend cut, I already sold half and was on the fence about what to do…not sure their senior management can right the ship.

I have BCE and T too. T has been so discounted and I’m optimistic things will improve when interest rates fall taking pressure off the cost of funds. Canadians can’t live without cell phones, and we love to hate Rogers and even Bell. I have a hard time equating these companies to the US, because of our population distribution and the difficulty to enter this business (wide moat, a little like railroads).

Thanks for sharing your analysis. Much appreciated.

p.s. not a big fan of REITs particularly since much of my net worth is already caught up in our house in TO.

Thanks Sandra. We’ve been slowly trimming REITs the last few years.

Great blog….thanks for your opinions and sharing your strategy. I’m 67 and just getting into investing. I often come to your site for your insights.

Thank you Mitch.

I have been dividend investing since 1999 and I have found that I would have done much better if I had not sold any shares of stocks that I had bought over the years. Nevertheless there were some losers but overall I would still come out with much bigger gain if I hold all my original position. The point is there is no need to overanalyze any stocks by all means. John Bogle had once said the long term return is sum of the dividend yield and growth of earning. This is nothing but truth. Earning growth simply means dividend growth as company would increase dividend payout with rising earnings year over year. You don’t need to worry about the price of any stocks and over analyzing its business model. If business has been able to raise the dividend year over year for very long time, it is in very durable and stable business. There is absolutely no points of selling BNS or CM unless they start cutting their dividend. In the case of AGN, I would cut it or close out because they cut the dividend. When it happens, we would revisit the balance sheet of AQN and its business model. If you look at the example of MO (tobacco business), the share price has been in down trend for years but I would love to own it. The reason being high dividend yield and steady dividend growth (4-6%). Scientific study had found you would come out way ahead of the game if you continue to buy shares of business at lower share price with steady dividend growth than stocks at higher share price and zero dividend growth. Money flow where cash grow. If the investors don’t appreciate the stock price now, they would at one point as long as the cash flow is growing.

Thank you for the great tips. It’s always good to hear from someone ahead of us on the DGI journey.

Your exercise provided food for thought! Interestingly, of 25 issues held in common we only have a difference of opinion on three. I’m more bullish on MFC and TRP and more bearish on T. Thanks for sharing.

Thanks for your input Charlie.why are you bearish on T?

Management execution. They appear to be following in the footsteps of AT&T circa 1980 where they prefer to monetize operations today (International, possibly Health) rather than using corporate synergies for a longer-term view. One example could be a rollout of full Apple Watch integration into their healthcare providers. Last count by Apple, only 12 Canadian practices were integrated.

Telus is like any other telecom or utility business and the only concern we are looking at right now is the high debts that is usually associated with utility company. High debt tag along with high interest rate is bringing the whole industry(telecom/utility/pipeline) down for this year. Again we don’t need to second guess how their business model works. Mike the dividend guy, said Telus is a technology company rather than utility like business. Whatever the case it is or will be, we would not know and we would not be able to time it or predict it. All I’m concerned is its cash flow to us as an investor. For as long as they are paying out dividend and grow it year over year. I would not worry about holding onto it.

So many choices . I’ve been buying RY, BMO, TD over last 2 weeks.

It’s hard to stop buying with the prices going low.

It needs discipline to not use up all my dry powder.

Next month likely brokerage gic up over 6% so I’ll stop buying for the moment and wait.

It’s hard not to go on a shopping spree right now ha.

HI Bob,

Considering CM and BNS dividend yield is more than 6% is there any possibility of a dividend cut. Alternative if the stock continue to tumble further the div yield could touch 7%+? Is this sustainable to both CM and BNS.

Good question, I don’t see BMS and CM cutting dividends at this point.

Thank you for this really interested review!!! Odd fact: few stocks you want to trim are in the BTSX selection (AQN, BNS, MFC, CM). What do you think of that? Do you review the BTSX strategy and mix with yours sometimes?

Yes we review the BTSX from time to time. It’s a great & simple strategy.