When I interviewed Reader B a few years ago about his $360,000 dividend income and how he and his wife are living off dividends, he pointed out that they only invest in Canadian dividend stocks to avoid the $100,000 CAD foreign investment property rule.

Since then, some concerned readers have asked me about this $100,000 CAD foreign investment rule. To be more specific, who needs to fill out the T1135 form for their foreign property investment properties? Do all foreign investments like real estate, stocks. and ETFs count? Is it only foreign investments inside non-registered accounts that count? Or is it investments across all the different accounts?

Like many readers, I was confused myself, so I started doing more reading and research. I was able to clarify many questions I had about Form T1135 and how the form works.

Therefore, I thought a blog post with more details about T1135 is warranted.

Let’s get into it, shall we?

What is Form T1135?

So what is Form T1135 from the Canadian Revenue Agency?

According to the CRA, Form T1135 or Foreign Income Verification Investment was implemented to make sure Canadian tax residents report income from non-Canadian foreign accounts.

Form T1135 must be filled by:

- Canadian resident individuals, corporations, and certain trusts that, at any time during the year, own specified foreign property costing more than $100,000

- certain partnerships that hold more than $100,000 of specified foreign property

One important thing to know is the $100,000 CAD amount is not the market value, it’s the adjusted cost basis (i.e. ACB). So if your total cost of your foreign investment property does not exceed $100,000 CAD, you do not need to fill out Form T1135.

What is considered as T1135 Foreign Property?

You’re probably wondering, what foreign property has to be reported per the T1135 rules. Per the CRA, the following specific foreign properties count toward the $100,000 CAD limit:

- funds or intangible property (patents, copyrights, etc.) situated, deposited or held outside Canada

- tangible property situated outside of Canada

- a share of the capital stock of a non-resident corporation, even held in a Canadian brokerage

- shares of corporations resident in Canada held outside Canada

- an interest in a non-resident trust that was acquired for consideration

- an interest in a partnership that holds a specified foreign property unless the partnership is required to file Form T1135

- a property that is convertible into, exchangeable for, or confers a right to acquire a property that is specified foreign property

- a debt owed by a non-resident, including government and corporate bonds, debentures, mortgages, and notes receivable

- an interest in a foreign insurance policy

- precious metals, gold certificates, and futures contracts held outside Canada

The following specific foreign property does not count toward the $100,000 CAD limit:

- a property used or held exclusively in carrying on an active business

- a share of the capital stock or indebtedness of a foreign affiliate

- a personal-use property

- an interest in, or a right to acquire, any of the above-noted excluded foreign property

Some more details on T1135 Foreign Property

According to these rules, if you own a property outside of Canada for personal use only, it does not count toward the $100,000 CAD limit. For example, if you’re a snowbird and own a vacation home in Florida and you do not use it as a rental property then you do not have to file a T1135..

Some readers may wonder, do you need to care where the non-Canadian investments are held (i.e. non-registered, TFSA, and RRSP)?

More clarification…

- Only foreign securities outside your RRSP, TFSA, or other registered accounts count toward the $100,000 limit. In other words, if you hold Apple, Microsoft, Alibaba, or other non-Canadian stocks inside your RRSP, TFSA, RRIF, or other registered accounts, they don’t count.

- If you hold these securities in a non-registered account, they’d count toward the limit. For example, if you hold Apple, Microsoft, or Alibaba in your non-registered account. This is the part that Reader B pointed out.

- Any US-based ETFs or funds in a non-registered account would also count toward the $100,000 limit. For example popular US index funds like VTI and VXUS.

- Rental properties outside of Canada count toward the $100,000 limit. One important thing to note is that if any capital improvements are done to the property (i.e. renovation) and the amount increases the cost basis to above the $100,000 limit, you will need to fill out a T1135 form.

- Cryptocurrency is in a bit of a grey area but it’d be wise to include your cryptocurrency as part of your foreign property calculation.

What about Canadian companies that are listed on both the Canadian market and US market? For example, what happens if you were to hold US listed shares of Nutrien (NTR), Royal Bank (RY), and Brookfield Asset Management (BAM)?

Well, since these are Canadian companies, these shares are excluded from the $100,000 limit, even if you were to hold them in non-registered accounts.

Given that there are many Canadian ETFs that invest in non-Canadian stocks like XAW or VXC, what happens to these ETFs? Also, what about these popular all-in-one ETFs like VGRO, XBAL, or the all-equity ETFs like VEQT?

Fortunately, because these ETFs are Canadian-listed, they don’t count toward the $100,000 limit regardless of which account you hold them in. Readers can breathe a sigh of relief knowing these Canadian ETFs investing in foreign stocks do not count toward the $100,000 limit.

Please note that the same applies to Canadian mutual funds.

So unless you specifically own foreign stocks and ETFs in your non-registered account, have a rental property outside of Canada, or have some sort of large foreign investment, the $100,000 limit shouldn’t apply to most Canadian investors.

How to complete Form T1135?

Form T1135 has two main parts and you only need to fill out one part.

Part A – Simplified Reporting Method

This section is if you have foreign properties that exceed the $100,000 limit but below $250,000.

Part A is considered as the simplified reporting method because you need to check off checkboxes and provide additional info like where the funds are held, gross income, and gain or loss from the sale of all foreign property.

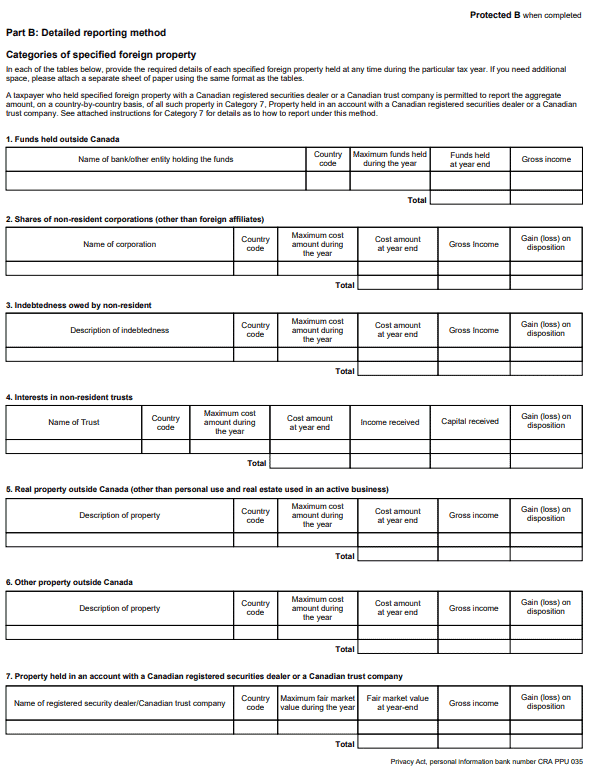

Part B – Detailed Reporting Method

If you own foreign property that cost more than $250,000, you must use the detailed reporting method.

As the name suggests, Part B requires way more information, is more complex, and you need to provide a more accurate description of the foreign property.

When is T1135 due?

Like your personal taxes, the T1135 must be submitted by April 30th each year. If you’re self-employed, then you can file the T1135 by June 15. If you don’t submit the T1135 then you will get hit by late penalties (more on that later).

If you have a corporation or a trust, then the filing date is a bit different. Per the CRA website:

| Taxpayer category | Filling due date |

| Self-employed persons: | On or before June 15 |

| All other individuals: | On or before April 30 |

| All corporations | No later than six months after the end of the corporation’s fiscal period |

| Trusts | December 31 + 90 days |

| Trusts that are estates | If the date of death is between January 1 and October 31, file the tax return by April 30 of the following year If the death occurs between November 1 and December 31, you have six months after the date of death to file the tax return |

| Partnerships: all partners that are individuals | No later than March 31 after the calendar year in which the fiscal period of the partnership ended |

| Partnerships: all partners that are corporations | No later than five months after the end of the partnership’s fiscal period |

| Any other partnerships | No later than the earlier of: March 31 after the calendar year in which the fiscal period of the partnership ended Or The day that is five months after the end of the partnership’s fiscal period |

What’s the penalty if I file the T1135 late?

If you fail to file Form T1135 on time, watch out, the penalty can add up pretty quickly.

The penalty for filing the T1135 is $25 a day to a maximum of 100 days or $2,500, plus interest for that period (note: minimum is $100).

But if you fail to file T1135 knowingly the penalty is higher at $500 per month for up to $12,000 maximum (i.e. 24 months).

Even worse, if the CRA asks you to file T1135 and you fail to do so, the penalty increases to $1,000 per month for up to $24,000 maximum (i.e. 24 months).

If you fail to file after 24 months and pay the penalty, the CRA can access an additional penalty.

In other words, don’t mess with the CRA. The same applies to over contributing TFSA.

What if I have US registered accounts?

For those Canadians who happen to have accounts like IRA, ROTH IRA, and 401K in the US. Do you need to include these in the $100,000 CAD limit calculator?

Fortunately, The T1135 has some exceptions so IRA, ROTH IRA, and 401K accounts do not need to be reported on the T1135.

Some thoughts on T1135

When I first heard about Form T1135 and the $100,000 foreign property limit, I was worried. Do I need to watch what we hold in our dividend portfolio in terms of foreign stocks and ETFs?

The fact that any foreign stocks and ETFs held inside of registered accounts like RRSP, RRIF, and TFSA are exempt is a big relief. It is also comforting to know that Canadian-listed ETFs investing in foreign assets are exempt from this rule.

In other words, unless you are an investor that invests money (that is, more than $100,000 CAD) in foreign stocks or ETFs inside of your non-registered account, you shouldn’t need to worry about the $100,000 foreign property limit.

More importantly, the CRA doesn’t care about the current market value. The CRA only cares about the adjusted cost basis. So if you were fortunate to invest $50,000 CAD equivalent in Google when it first went IPO in your non-registered account and you don’t own other foreign properties, you are completely free from the T1135 rules.

In summary, if you follow the typical tax efficient investing approach below, you should be able to ignore T1135.

Tax efficient investing approach 100

Non-registered accounts: Best for Canadian dividend stocks or ETFs

TFSA: Best for Canadian REITs and income trusts. Canadian dividend stocks or ETFs can also work.

RRSP: Best for US listed stocks or ETFs, including REITs and income trusts.

Happy investing everyone!

If crypto currency is received as a barter for an active business in a self custody wallet, how much capital surplus can accumulate before T1135 is required? 1 year? 2 ? more? Assume the business has little working capital needs. Also in general self custody requires reporting at all if over 100k since crypto on your cold wallet or hot wallet on the phone goes with you, so the seed keys are actually in your home in Canada, or possibly no need to report if you are a Canadian resident ?

Hmm I’m not 100% sure when it comes to crypto currency. Best to check with a professional.

lol most professionals know less than unprofessionals!

Dos this apply to mutual fund investments held outside of North America?

Mutual funds held outside of Canada would count toward the $100k limit.

If I have over $ 150,000 US dollars invested in non registered trading account in one of Canadian brokerage account, and aside from regular taxes on capital gain & on dividends. Do I need to fill up the T1135 form?

It depends on what you hold with the US dollars. I think I have listed all the investments that will require you to fill out the form…

How is the CRA ever going to find out about foreign property if you don’t inform them?

You’ll be surprised how much info CRA can obtain. 🙂

I’ve had to file T1135 for years . I’m not sure why anyone should be worried about filing the form unless you’re filing late.

It’s because the CRA is too lazy to do it itself , it gets the taxpayer to file it. This allows the CRA to easily raise more revenue through future taxes and fines .

The thing to worry about though is the US IRS and estate taxes especially if your portfolio of US stocks gets large.

Good old Joe Biden is trying to reduce exemption to estate taxes down to 2009 levels of $3.5M. So if your estate has $3.5M in US stocks it will be taxed at 50% or some high level like that .

Obviously it’s easy to avoid this tax with planning but $3.5 M is within the realm of achievement over a life time and it’s hard to avoid a sudden accident

Generally speaking, I think the worrying is due to the lack of understanding of what triggers the need to file T1135. I certainly was a bit confused myself (stocks vs ETFs, cost basis vs. market value) until I did own research.

” the CRA doesn’t care about the current market value. The CRA only cares about the adjusted cost basis.”

Is T1135 required to report market value? Why not cost?

thank-you for posting this, Bob. Very helpful.

To recap, I have one US growth dividend stock in my TFSA. It’s not going to hit 100k for awhile, but to confirm – since it’s in my TFSA, i don’t need to worry about the T1135?

Much appreciated.

Correct. Now, even if stocks inside the TFSA were to count toward the $100k limit, it’s the cost basis value, not the current market value.

Hi Bob,

Does USD cash held in saving account with Canadian bank also count towards the limit?

Regards,

Thao

Hi Thao,

No, it doesn’t.

I owned foreign property (in USA) and filed T1135 for many years. It is a declaration of ownership and nothing more.

Any income from any source must be declared when you file your personal taxes so I am not sure where the trepidation about T1135 comes from. Like Bob says, inside RRSP doesn’t matter, also the USA recognizes it’s a retirement plan and there is no witholding back on interest, dividends or gains if sold). In a TFSA any USA based dividends have 15% withholding. Your brokerage statements should show this or call your investors help line. It’s messy and confusing but not enough reason to avoid USA markets that tend to outpace the TSX imho

Thanks for the further clarification Gordon.

Agree, this is very confusing and messy but you shouldn’t avoid investing in the US market because of that.

Thank you Bob. I have been wondering about this for some time. At one point I was worried enough that I sold my US stocks and switched to a Canadian listed ETF instead. Thanks for all you do.

You’re very welcome Jan.

Thank Bob for the details about T1135. Same question as Sabrina: is the $100,000 limit for household or individual?

Hi Hong,

I believe it’s per individual but best to double check with a tax specialist.

If the foreign stocks are owned jointly by a couple in a non-registered account, then does the T1135 only need to be filed if each person’s portion is over the $100,000 limit amount? TIA

Hmm, to be honest, I’m not 100% sure when it comes to joint accounts. You may need to double check with a tax specialist. If I had to guess, since it’s a jointed account, then it’d be split 50-50, meaning you wouldn’t hit the $100k limit (since it’s per individual).