Back in December, I shared Canadian dividend stocks we’d like to purchase for 2024 TFSA. Since then, we have made our purchases and added more dividends toward our forward annual dividend income (more information in the January 2024 dividend income update).

As we have now maxed out our TFSAs and purchased different dividend stocks, the next step is to contribute money and purchase dividend stocks in our RRSP, and then finally do the same thing in our taxable accounts.

Max out TFSA first, then RRSP, and finally taxable – this is something we’ve been doing since we started our financial epiphany. This “keeping it simple, Stupid” strategy has worked quite well for us over the years.

At the time of writing, our dividend portfolio consists of 46 individual dividend stocks and 1 index ETF (XAW). The individual stocks we own consist of a mix of US and Canadian stocks:

- 17 US dividend stocks including mega international names like Apple, Costco, Pepsi, Coca-Cola, and Starbucks. We own a handful of US dividend paying stocks in our RRSPs to avoid the 15% withholding tax on foreign dividends.

- 29 Canadian dividend stocks. We own 12 out of my 13 Canadian best dividend stocks and other well known Canadian names like Manulife Financial, Emera, Metro, and Canadian Tire.

Since we are working to reduce the number of holdings to about 40, we don’t plan to introduce any new positions to our portfolio.

In other words, we plan to add more shares to dividend stocks that we already own. With that in mind, here are 5 dividend paying stocks we plan to buy in 2024 for our RRSPs and taxable accounts.

Stock #1: Visa (V)

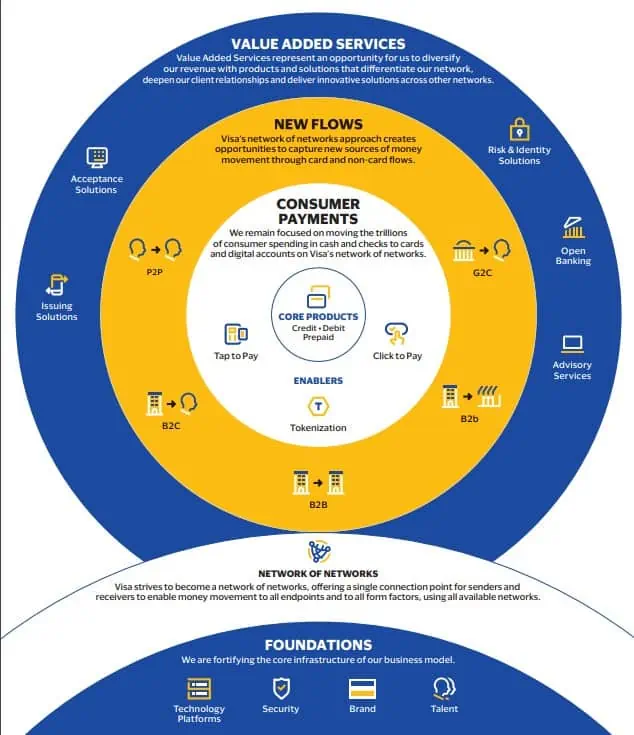

Visa is a well known multinational brand that facilitates electronic fund transfers throughout the world, most commonly through Visa-branded credit cards, debit cards, and prepaid cards.

Visa’s payments technology connects consumers, businesses, banks, and governments in more than 200 countries and territories, enabling them to use digital currency instead of cash and checks. Visa has completely transformed how we purchase merchandise.

Some of you might ask, why even bother adding more Visa shares when the initial dividend yield is less than 1%?

Yes, Visa has a very low initial dividend yield so if you’re filtering stocks by dividend yield of 1.5% or higher, Visa won’t be on your watch list. What makes Visa quite impressive is the total return over the years.

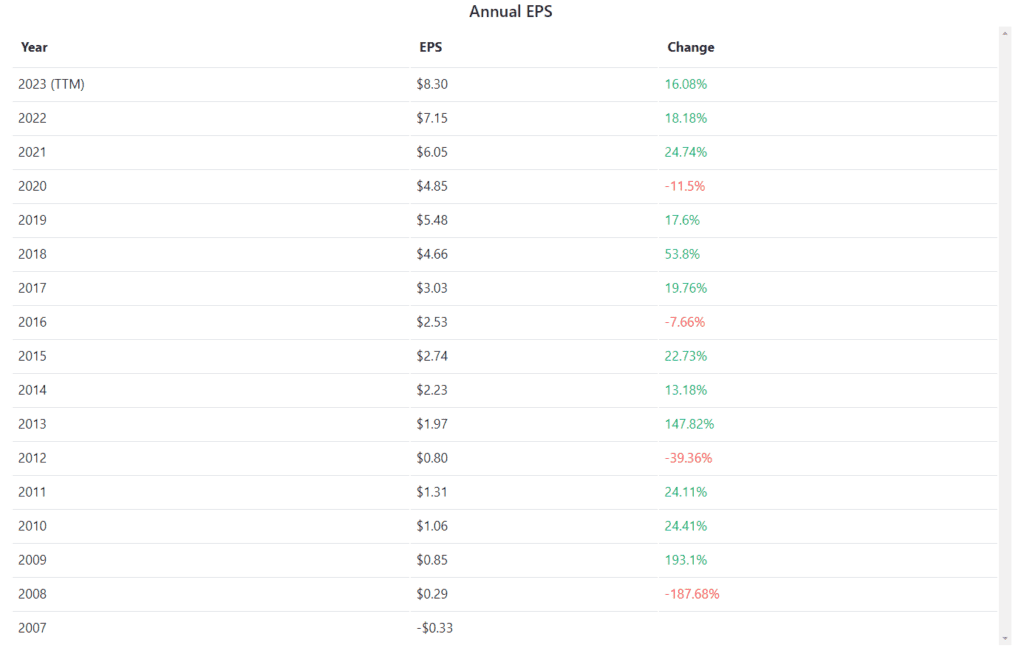

Visa has a 5 year return of +87.08% and a 15 year return of over 1,400%!

In addition to the impressive total return, Visa has a 15 year dividend increase streak with a 15 year dividend growth rate of 26.3%. Recently, Visa announced a 15.6% dividend increase from $0.45 per share to $0.52 per share. Visa is one of those low yield high dividend growth stocks that reward shareholders in the long run.

As one of the largest payment processors in the world, Visa has a nearly impenetrable moat. (as well as a runway for further growth in developing countries) Visa also has built a very strong and well recognized brand.

Visa’s Q4 2023 earnings beat expectations and the company has so much free cash flow that the management decided to return $5 billion of capital to shareholders in the form of share repurchases and dividends. According to the management, Visa is expecting another strong year ahead and I would not doubt this is going to be the case.

Adding more Visa shares should help us on the total return front. Since we purchased Visa shares a number of years ago, we have more than doubled our initial investment. We’d like to add more shares to continue the impressive returns.

Potential Risks for Visa

Visa has had very impressive earnings per share growth since 2007. Can Visa keep such an impressive growth rate of around 15% annual EPS growth? My guess is that it will be extremely difficult to maintain but it is definitely possible to continue the EPS growth at a minimum of 10%, still not too shabby.

If the annual EPS growth goes from 15% to 10%, this will likely slow down share price appreciation and dividend growth.

The other potential risks are an increase in competition from the likes of MasterCard and American Express. Furthermore, new FinTech companies could potentially impact Visa’s revenues. But these risks should be relatively low.

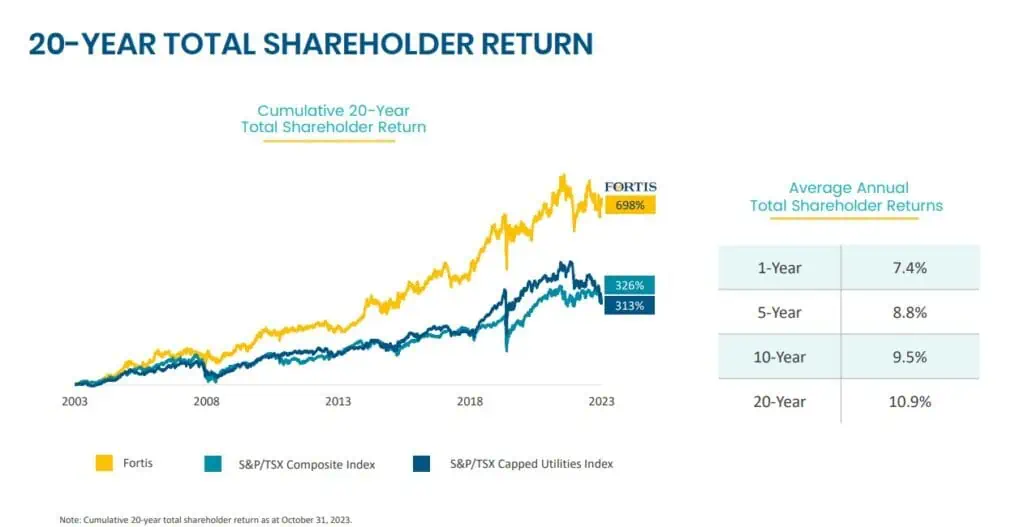

Stock #2: Fortis (FTS.TO)

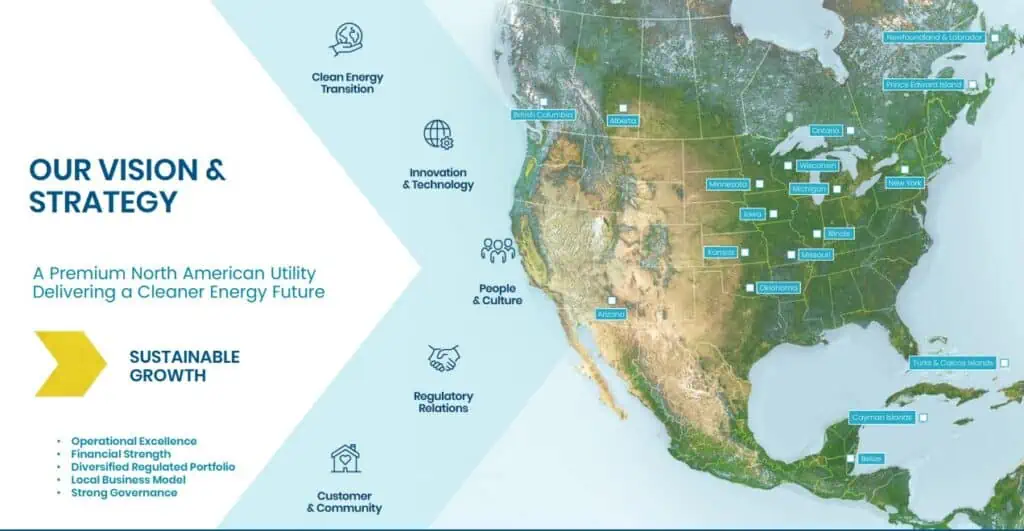

Fortis is a Canada-based electric and gas utility holding company that operates in many different regions including Arizona, BC, Alberta, New York, Newfoundland, Ontario, PEI, and the Caribbean, serving about 3.4 million utility customers.

Why purchase more Fortis shares?

One word – Boring!

Yup, investing in Fortis is as boring as it gets. But boring is a very good thing when it comes to investing.

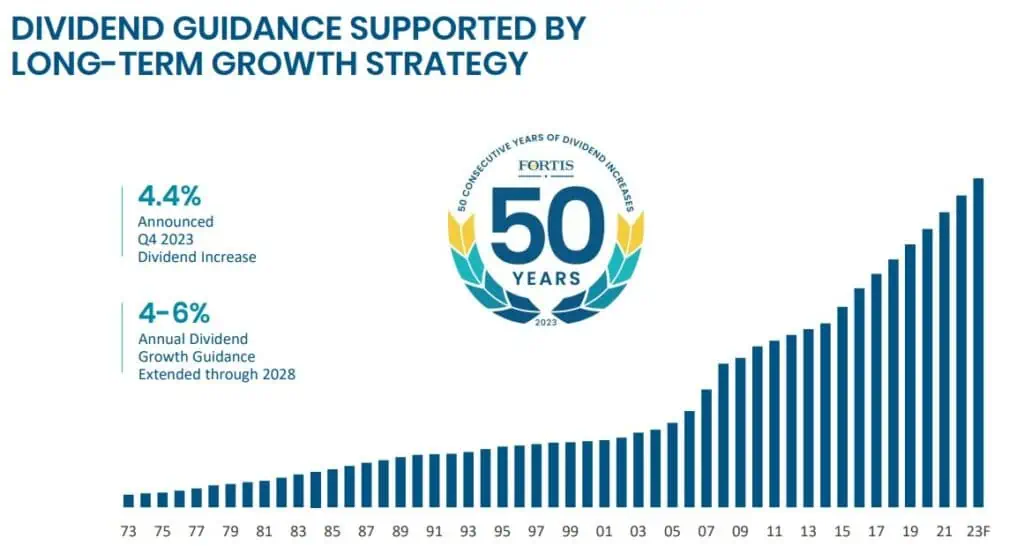

Fortis is one of the only two Canadian dividend stocks with more than 50 years of dividend growth streak and thus can be labelled as a dividend king stock (50 consecutive years of dividend growth). Fortis management has provided a 4 – 6% dividend growth guidance through 2028. As a shareholder, we are assured that we will continue to see dividend growth for many years.

In addition to the consistent dividend growth, Fortis’ share price has steadily appreciated over the years, demonstrating that it is very shareholder friendly.

I also like that Fortis is very forward looking and working to meet de-carbon goals. Fortis is working to exit from coal and move toward renewable energy like wind and solar generation and reduce overall carbon emissions with a 50% emissions reduction by 2030 and a near-zero target by 2050.

Potential Risks for Fortis

Like any other utility company, Fortis’ potential risks and challenges are:

- Changes in regulations and the geopolitical landscape

- Natural disasters

- Public pressure to reduce emissions earlier than planned

- High capital expenses

- Rising interest rates and if interest rates continue to be high for a long period of time

Knowing Fortis’ stellar performance over the last 20+ years, I’m not too concerned with these potential risks and challenges. I am confident in the Fortis management team and believe it will continue to steer the ship in the right direction.

Stock #3: Costco (COST)

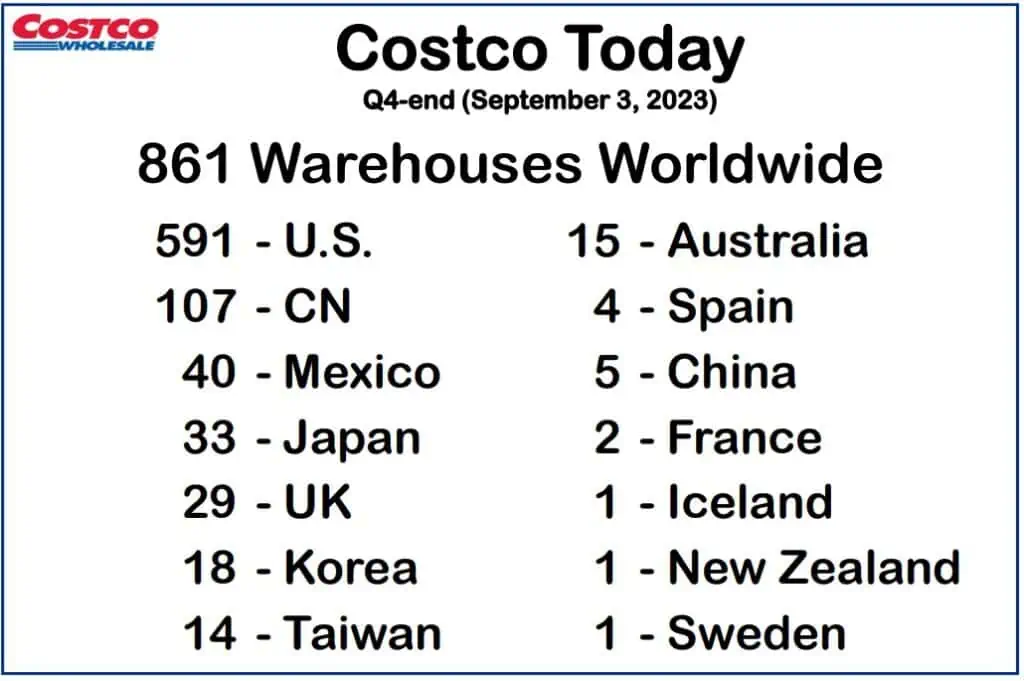

Costco is the third largest retailer in the world and operates a chain of membership-only big box warehouse club retail stores with 861 warehouses worldwide. Unlike other grocery retail stores, Costco doesn’t make a lot of margin from the merchandise it sells. Instead, Costco makes money from their membership fees, like the Costco Executive Membership.

We already own quite a bit of Costco shares but it’d be nice to add more so it becomes one of the top three positions in our dividend portfolio.

Every time I go to a Costco warehouse, it’s always full of people. It is also very easy to spend more than $300 at the warehouse each visit. Recently we went to Costco for our regular monthly visit and spent almost $700!

Unlike retailers like Target and Walmart which face quite a bit of theft that is hurting their bottom line, Costco checks your receipts and carts whenever you exit the warehouse. This practice has significantly reduced theft issues at Costco warehouses.

Costco has 861 warehouses globally as of the end of Q4 2023. Most of the warehouses are in the US (591) and Canada (107).

In 2019 Costco opened its first warehouse in China in 2019 and it was so popular the store was shut down on the very first day. At the end of Q4 2023, Costco has 5 warehouses in China and it plans to continue the expansion.

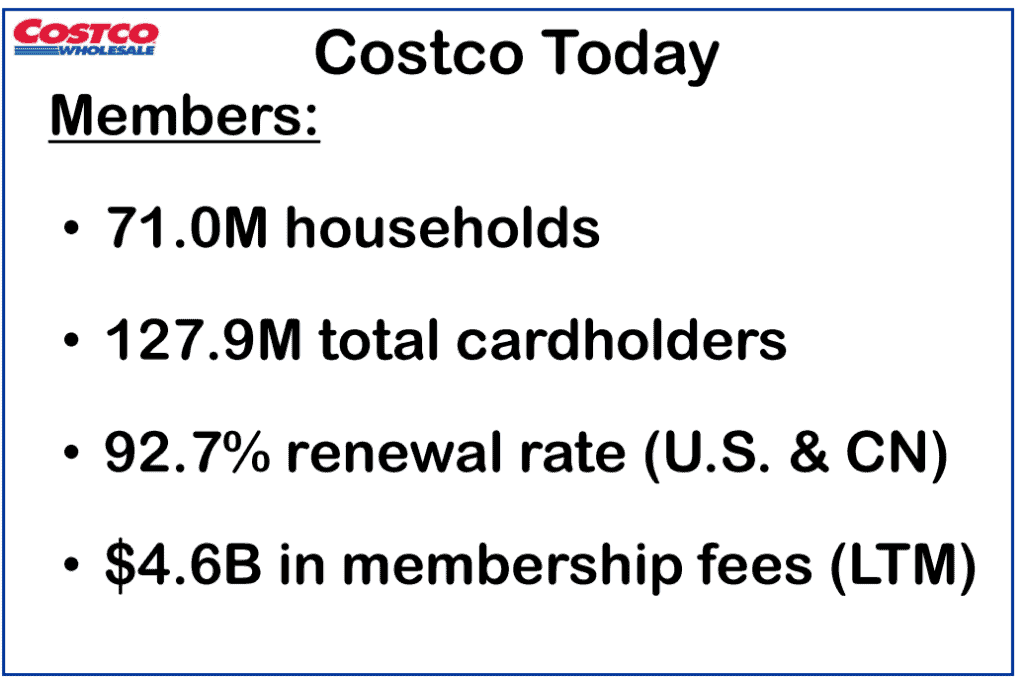

I believe by focusing on expanding non-North-America warehouses, Costco can continue to grow. Costco has a 92.7% membership renewal rate in the US and Canada and a 90.5% renewal rate globally. Both are very impressive.

Like Visa, Costco has a very low initial dividend yield. But Costco has increased its dividend payout for 19 straight years with a 10 year dividend growth rate of 12.62%. Costco also has issued four special dividends in the past with the last one in December 2020 at $10 per share. It is widely believed that Costco may pay out a similar special dividend sometime in 2024.

Potential Risks for Costco

At a PE ratio of ~40, Costco stock is anything but cheap. You are definitely paying a premium when purchasing Costco shares. Having said that, it is not unusual to see consumer staple stocks at a PE ratio of over 20. For example, Procter & Gamble has a PE ratio of around 25, and Walmart has a PE ratio of around 30.

Costco has ramped up their online store presence over the years but they continue to face significant competitive pressures from other online retailers like Amazon. Having said that, Costco usually sells in bulk so perhaps the target consumers are slightly different than those of Amazon.

Costco depends on membership, specifically membership renewal. Over the years, Costco has enjoyed a very high membership renewal rate. But will this continue? Will Costco members stop renewing their memberships and do their shopping at other retailers? Can Costco continue to attract new members and retain membership renewals as the company expands into new regions?

During the company’s Q4 earnings results, Costco’s CFO Richard Galanti stated that membership fees will increase. Although there’s no clear timeline yet, a key question is whether Costco can increase the membership fees without creating protest and backlash thus resulting in a reduction in the renewal rate.

The last time Costco raised its membership fees was in 2017 ($5 increase in basic membership and $10 in executive membership). Will the next increase be in a similar range? Costco definitely needs to tread carefully here.

There are a lot of concerns over the Costco membership business model but Costco has shown over the years this model works very well. Shoppers seem to like Costco and its warehouse bulk purchase model. Therefore, I believe Costco will continue to execute and perform well.

Stock #4: Apple (AAPL)

Long time readers will probably remember that we like Apple a lot.

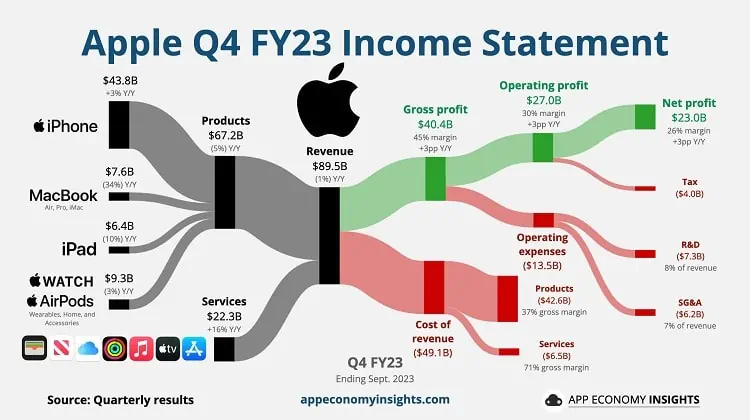

Apple is one of the most recognizable brands in the world, the world’s biggest company by market capitalization, and the company continues to make billions of net profit each quarter.

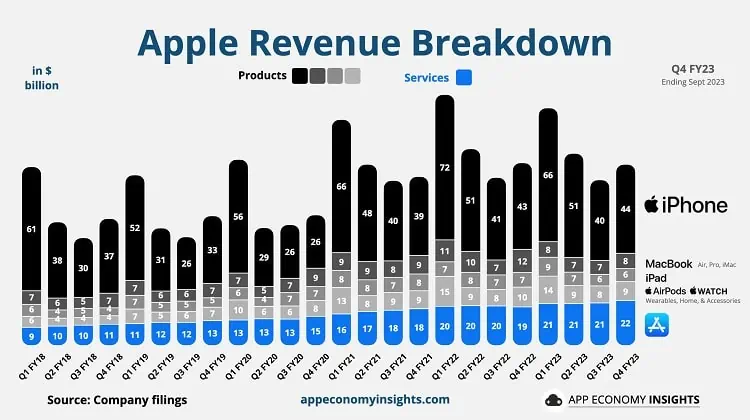

Although most people think Apple is a hardware company, Apple has been growing its Services segment consistently.

In fact, Services revenues now make up over 25% of Apple’s quarterly revenue. Five years ago in 2018, the Services revenues only made up less than 15% of the quarterly revenue.

What caught my attention is that Apple CFO Luca Maestri provided guidance that he expects Services to continue to grow at a double-digit rate in fiscal year 2024.

The powerful thing about Services revenues is that they are typically re-occurring. So Apple no longer relies on customers buying new hardware to generate revenues.

There’s one key reason why the Services revenues have been growing consistently – the tightly integrated Apple ecosystem. Over the years, Apple has done a good job in integrating the MacOS with the iOS so users have a seamless experience across the different products. This is why if you use an Apple computer, there’s a very high chance you also own an iPhone, iPad, and other Apple products. The same logic holds if you start with an iPhone or iPad.

Apple just recently announced the next generation of Apple M3, M3 Po, and Max chips. It is expected that Apple will announce the M3 Ultra chip sometime this year and potentially announce the M4 chips late this year or 2025. These Apple silicon chips are really pushing the performance envelope and helping Apple to tightly control their overall hardware.

There are still many Apple users, ourselves included, that haven’t migrated from Intel to the new Apple silicon based hardware. So I expect a significant growth in Mac sales in 2024 as more and more existing users switch from Intel to Apple silicon based chips.

I’m also very bullish on the wearable and accessories segment. According to Apple, two out of three Apple Watcher buyers were first time buyers. This demonstrates how sticky the Apple ecosystem is.

Finally, Apple is very shareholder friendly. In 2023 Apple returned $93 billion to shareholders – $15 billion in dividends and $78 billion in stock buybacks.

Potential Risks for Apple

The biggest risk for Apple is the Greater China market. This market was around 19% of Apple’s revenue in 2023. What would happen if China were to completely ban iPhones? Apple would for sure see a significant decline in its overall revenues.

As interest rates and inflation rates continue to be high, people are more conscious about what they are spending their money on (aka discretionary spending). It is clear that customers aren’t upgrading their phones as often as they used to. This is causing iPhone sales to slow down. If this trend continues, this is going to hit Apple’s profitability. Hence it is vital for Apple to continue to grow revenues in other non-iPhone segments, especially Services.

Although the Apple Vision Pro has gotten amazing responses from developers, will the general public purchase such an expensive first generation product?

According to insiders, Apple has a target of 400,000 units in 2024 which is a significant drop from the one million units that it originally targeted. We know that it took Apple a few iterations on the Apple Watch before it reached mass appeal. How many iterations and how much money will Apple need to spend on Vision Pro before it is widely adopted?

Finally, while I believe Apple has an extremely strong ecosystem, is it really that strong that it can prevent customers from jumping to the alternative?

Stock #5: Enbridge (ENB.TO)

Enbridge is one of the leading North American infrastructure companies with a vast network of pipelines. Enbridge has the longest pipeline system with a crude oil pipeline network of over 28,000 km and a natural gas pipeline network of over 38,000 km.

For the most part, here in North America, we are still highly dependent on natural gas and crude oil in day-to-day life. Because of that, we need to rely on Enbridge’s vast pipeline network to transport crude oil and natural gas across North America.

Just how much do we rely on Enbridge’s pipeline network?

Well, Enbridge ships over 20% of the US natural gas and 30% of the crude oil used in North America.

Environmental concerns mean it is increasingly difficult (nearly impossible) to build new pipeline networks, so Enbridge’s existing pipeline networks are more valuable than ever.

Does Enbridge enjoy a strong and wide moat due to its large pipeline network? Absolutely!

It’s hard to ignore the high initial yield of over 7%. It is also hard to ignore the 28 year dividend increase streak from Enbridge. Although Enbridge has a payout ratio of over 100%, if we look at its cash flow, the dividend accounts for about 70% of the distributable cash flow, which roughly aligns with Enbridge’s target. Therefore, the dividend payout should be safe and should allow Enbridge to continue to raise dividend payout in the 5 – 7% expected growth rate.

I also like that Enbridge is growing the renewable businesses and it plans to acquire a trio of US companies. Assuming this acquisition gets approved by regulators, it will allow Enbridge to create North America’s largest natural gas utility company. There’s also a good chance for Enbridge to split its current business into two different companies and deliver more value to shareholders (Similar to what TC Energy plans to do later this year).

Overall, I think Enbridge is a dependable dividend payer and its high yield provides a solid dividend income for us. Having the right mix of high yield low dividend growth and low yield high dividend growth dividend stocks is very important as we inch closer toward our goal of living off dividends.

Potential Risks for Enbridge

Enbridge can be seen as a utility company so it faces similar risks & challenges as Fortis that I outlined above. Due to the vast pipeline network, Enbridge needs to spend a lot of money to maintain the pipelines. New projects require a lot of capital and in the rising interest rate environment, this can increase liability risks for Enbridge.

If Enbridge can continue to grow at its planned rate, things should work out just fine. However, if the company takes on too much debt and growth slows down, this can create havoc on the share price and its dividend growth streak.

However, I believe the risks are limited. Enbridge may face some short term and medium term challenges but Enbridge should do just fine long term given the solid assets that the company owns.

Summary – 5 stocks we plan to buy in 2024

These are the five dividend paying stocks we plan to buy in 2024 in both our RRSPs and taxable accounts. I really hope the market will stay volatile so we can purchase these stocks at a discounted price.

Are there dividend paying stocks that you’re planning to buy this year?

Just mention about Costco’s special dividend – they paid $15 per share mid-January 2024!

I’m enjoying being a shareholder!!

They seem to pay a special dividend every 2 to 3 years. Gotta love that.

Hi Bob

Thanks for sharing your list of stocks you plan to buy. I own 4 out of 5 myself. Do you think it is ok to add more COST even at this price?

Thanks

Personally I’d probably hold off on adding more COST unless there’s a little bit of pull back.

Got TD, ENB, FTS in the kid’s RESP and taxable brokerage last week.

Waiting for the 5.5% Gic from the RSP to mature.

COST climbing everyday to another all time high with a PE over 40, seems like a set up for a great short.

Yes COST continues to climb, we’ll see if shorting it pays off. Short term it’s probably due for a pullback. Long term, I think it’ll just continue to go up.

I already have 4 of the 5 you mentioned here, so overall it must mean we think alike on our assessment of our own portfolio.

The only one that doesn’t interest me on that list is Enbridge. I just don’t have love for that buisness which used to grow their dividend by 10% until 2020, because of the debt, they are now growing at a rate of 3% which is on par with inflation.

If I were retired, I wouldn’t mind that much, but since I have many years left before needing the income, I prefer companies that can grow their dividends above inflation rate and able to have capital appreciation.

Not saying your pick of Enbridge is bad btw, it’s the only stock simply that doesn’t align with my portfolio strategy and I think at the end of the day that’s what matters.

That’s a fair assessment. 🙂

Hi Bob

I always find your insights informative. I know you have written above about each company’s risks; however, with Visa, Costco and Apple, how much consideration do you give to the currency risk (if the CDN dollar were to gain strength against the US dollar)?

Thank you

Years ago CAD was over parity to USD… I don’t see that happen in the next decade or more. There’s always a risk but IMO Costco and Apple’s growth outweighs the currency risk.

Hi Bob,

Visa and Mastercard form one of the most remarkable duopoly of the world! With a dividend growth rate of 15-20%/year, they double it every 4-5 years! I owned both of them since 2009-2010 and although they started with a yield around 1% they pay now both over 6%.

I would not worry to much about competition from Amex, since their main success is their deal with Costco. Even then, Costco Canada replaced them with Mastercard. Amex apex was during the traveler’s check era. Now that you can easily withdraw money at an ATM almost everywhere in the world, they are reinventing themselves.

The ubiquity of intelligent phones in south east Asia, India and Latin america reduced the confidence barrier toward credit cards and is an important growth vector for that duopoly.

Agree with you Alex, I don’t think you can go wrong with either Visa or MasterCard.

Thank you for sharing your thoughts on what you find attractive in 2024. Me and my husband are a bit conservative and tend not to buy stocks at high P/E ratios. One company which pays a low amount of dividend, but is trading at very low multiples is Fairfax financial. We are very interested in this one.

Makes sense to find something low multiples. 🙂

Apple has a lot of lawsuits related to the ecosystem their famous 30% tax on other company’s subscription services may go away. They are trying to build a moat around it, but it’s under a lot of attack.

Warren Buffett has been selling some of his Apple stock. He had so much of it, he might just be rebalancing or taking some profits.

Yea, lots lawsuits but that’s typical for a major international company like Apple.

I think Buffett has been rebalancing due to having so much of it.