Although we can technically be financially independent today if we really wanted to, we have decided to prolong our financial independence journey. Mrs. T and I have decided that we can declare ourselves fully financially independent when our dividend income exceeds our annual expenses.

In case you’re wondering, Mrs. T and I are targeting to reach financial independence in 2025 or earlier (in our early 40’s). That gives us about 6 years to go until we hit this target, but we aren’t too focused on the target year. If we become financially independent by 2025 or earlier, great; if not, we aren’t going to lose sleep over it. Since we know that one day our dividend income will exceed our annual expenses, it’s simply a matter of time.

Over the last few months, I have received many emails from fellow readers asking me exactly when we will become financially independent. Being a number/Excel nerd, I began to wonder: when will our dividend income exceed our annual expenses so that we are fully financially independent?

Some background info

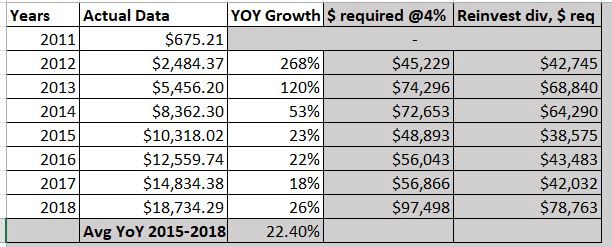

For this simulation, I will first look at our historical annual dividend incomes from 2011 to 2018.

We had a pretty big spike in dividend income in 2012, 2013, and 2014. This is a common occurrence to almost all dividend growth investors in the early years of their investment journey. Usually, many dividend growth investors would move money from other investments to invest in dividend growth stocks, which would trigger the dividend income spikes.

Therefore, I will use data from 2015-2018 to calculate the average dividend income year-over-year growth rate. Based on 4 years of data, we had an average YoY growth rate of 22.4%.

In case you are wondering how much fresh capital is needed (at 4% dividend yield) to generate the respective increase in dividend income each year, I have shown that in the table above. Given that our dividend income growth is powered by 3 key components: the investment of fresh capital, organic dividend growth, and DRIP, we don’t actually need as much fresh capital as indicated. So, I created another column on how much fresh capital is needed if we reinvest all of our dividend income (assuming no organic dividend growth and no DRIP).

Additional Information

Based on our financial independence assumptions, I will assume that we will need different levels of dividend income to be fully financially independent.

- $40,000 CAD/year – This is the leanest annual expenses we anticipate. LeanFI, if you want to label it.

- $50,000 CAD/year – This will allow us to maintain a similar lifestyle as what we have today.

- $60,000 CAD/year – This will allow us to have a few more vacations throughout the year than what we do currently.

Let’s run the simulation and find out when we can reach these levels.

When can we become fully financially independent – the numbers!

I ran 5 different scenarios to see when we can become fully financially independent. The 5 different scenarios are based on different dividend income YoY growth rates:

- Annual dividend income grows at the average YoY growth rate of 22.4% annually.

- Annual dividend income grows at a YoY growth rate of 15% annually.

- Annual dividend income grows at a YoY growth rate of 10% annually.

- Annual dividend income grows at a YoY growth rate of 20% in the first 3 years, then 15% the next 5 years, then 10% after.

- Annual dividend income grows at 20% YoY growth in 2019, then decreases by 1% each year.

And here are the numbers:

Note: Green highlighted entries mean we hit the $40k/year mark. Teal highlighted entries mean we hit the $50k/year mark. Yellow highlighted entries mean we hit the $60/year mark.

Calculation results

Scenario 1: Average 22% YoY Growth

We can reach the $40k mark in 2022 (3 years), the $50k mark in 2023 (4 years), and the $60k mark in 2024 (5 years). This is ahead of our 2025 target.

Scenario 2: 15% YoY Growth

We can reach the $40k mark in 2024 (5 years), the $50k mark in 2026 (7 years), and the $60k mark in 2027 (8 years).

Scenario 3: 10% YoY Growth

We can reach the $40k mark in 2026, the $50k mark in 2029, and the $60k mark in 2031. This is the slowest path to becoming financially independent out of all the 5 scenarios.

Scenario 4: 20% for 3 years, 15% for 4 years, then 10%

For Scenario 4, I decided to use a sliding YoY growth rate to reflect a slow downing dividend income in the future. Based on these YoY growth numbers, we see that we can reach the $40k mark in 2023, the $50k mark in 2025, and the $60k mark in 2026.

Scenario 5: 20% then 1% less each year

For Scenario 5, I decided to use the sliding YoY growth rate again with the growth rate slowing down by 1% each year. Based on these YoY growth numbers, we see that we can reach the $40k mark in 2023, the $50k mark in 2025, and the $60k in 2026.

Some thoughts on the financial independence calculations

Here are some thoughts on the simulation I’ve just shown:

- If $40k per year dividend income is the goal, we can become financially independent as early as 2022 and as late as 2026, or between 3 to 7 years.

- If $60k per year dividend income is the goal, we can become financially independent as early as 2024 and as late as 2031, or between 5 to 12 years.

- Looking at the results from the different scenarios, we really aren’t too far off from our 2025 target. This is nice to see and assuring.

- I think a 10% YoY growth rate is a bit unrealistic – we definitely can grow more than 10% YoY for the next number of years.

- For the same reason as above, I think a 15% YoY growth is a bit unrealistic in the next 3-5 years. I strongly believe we can continue to grow our dividend at above 15% YoY.

- This raises the question about what’s a realistic YoY number? Are Scenario 4 and 5 a more accurate reflection of what may happen to our dividend income?

It’s great that we can become financially independent as early as 2022 and as late as 2031. One major thing, however, is that we are forgetting is something called the law of large numbers.

The law of large numbers

If you’re a long time reader, you’ll probably remember me mentioning about the law of large numbers in some of our monthly dividend income updates. What is the law of large numbers?

The law of large numbers is an inevitable event that will happen to every single dividend growth investor. According to the law of large numbers, your annual dividend income YoY growth rate will slow down at some point.

Why is that?

Well, imagine receiving $240 in annual dividend income. A 100% YoY increase means a future annual dividend income of $480. At a 4% dividend yield, only $6,000 additional capital is needed to see a 100% YoY increase.

Now imagine an annual dividend income of $12,000.

A 5% YoY increase in annual dividend income means an additional $15,000 is needed at a 4% dividend yield.

A 10% YoY increase in annual dividend income means an additional $30,000 is needed at a 4% dividend yield.

A 20% YoY increase in annual dividend income means an additional $60,000 is needed at a 4% dividend yield.

Finally, a 50% YoY increase in annual dividend income means an additional $150,000 is needed at a 4% dividend yield.

This is a simplified example as we are ignoring any dividend income increases from organic dividend growth and dividend reinvestment plan (DRIP), but the message is clear – it takes a significantly large sum of fresh capital to sustain a high dividend growth rate once your dividend income reaches a significant level. Unless you are making millions of dollars at your job, I believe it is extremely challenging to save and invest $150,000 or higher each year. The more dividend income you receive, the more fresh capital is needed to grow future dividend income.

So, if we look at the “$ required @ 4%” columns for each scenario, we’ll see that significant fresh capital is needed for Scenario 1, 4, and 5 to generate the respective YoY growth. Even if we reinvest all the dividend each year, these scenarios still require a significant amount of fresh capital each year, and these numbers are simply not sustainable for us. In comparison, based on our 2018 dividend income growth, we needed over $97k of fresh capital, or over $78k with dividends fully invested. If we use ~$97k of fresh capital as the guidance, that means Scenario 2, 3, and possibly 5 are the most realistic scenarios for us. That means we’d become fully financially independent as early as 2023 or as late as 2026 based on a $40k per year requirement. Again, this is somewhat close to our FI target of 2025. If we aim for $60k per year, that means we will become FI as early as 2026 (in 7 years, my early 40’s) or as late as 2031 (in 12 years, my late 40’s).

One thing to note, if we look at the last few years in the “$ required @ 4%” columns for all 5 scenarios, we see some crazy amounts of money required (i.e. $141k required in 2024 for the 15% YoY scenario, $121k required in 2029 for the 10% YoY scenario, and $120k required in 2020 for the last scenario). They are simply not realistic.

Wrapping things up

When can we become fully financially independent? Based on the different scenarios, we should be able to hit our target of 2025 or a few years later, but the YoY growth rates used for the 5 different scenarios may not be very accurate. Furthermore, things can change from year to year.

Regardless of the actual year, one thing I have confirmed is that we will be FI one day – it’s simply a matter of time. If we continue with our current level of lifestyle, I am very confident that our dividend income can cover our annual expenses when Mrs. T and I are in our 40’s or 50’s.

Tawcan, I loved this post! I hadn’t considered a retirement plan focused on a dividend portfolio, specifically, before reading this post. Thanks!

Thank you, glad to make you think.

Thank you for this article and the calculations that you’ve provided. I’ve created a similar sheet for myself to crunch my own numbers and I was very excited to see that I can reach my goals in the next few years. I’ve learned more from your site than from so many other books that I’ve read. I’m convinced that you’re one of the people who is genuinely interested in helping others by sharing your knowledge via this awesome blog. I hope that you and your family continue to see great YoY growth in your dividend portfolio. Again, thank you for all that you do in teaching other people how to estimate when their own FI-date might be! Happy Easter to you, Mrs. T, and your baby Ts!

Thank you. I hope to continue to see great YoY growth in the future but as mentioned, we expect the YoY to slow down as we get bigger dividend amount.

Thanks for the nice post Bob.

This is analogous to the 4% rule that many people use in the index fund retirement planning.

So for me the rule is, if I retire at 65, I need expenses*25. If I retire early, it is expenses *40.

I guess for you as a dividend investor, you would need to look at the probability of companies dropping their dividends over the time you are retired, and build it into your modelling. I suspect you will come up with a similar conclusion, which is that you need to have roughly 1.5 times your expenses covered by your dividends. Although I’m curious to see that is the case.

We also hit the law of small numbers, but that is a good problem to have.

The one thing I didn’t include in this simulation is selling of assets. If companies drop their dividends, we can always sell some principals to cover the difference.

Wow, those are some pretty heartening numbers, I bet! Congrats on getting yourself to where you are already — you’re miles (or kilometers, since you’re Canadian) head of me. Thanks to a late start on serious saving, I’ll be financially independent around 65 to 70 and that’s about the best I can hope for. But that beats going into retirement with too few savings, right?

Thank you. These numbers are nice to see but we’re based future outlook on historical numbers. Things can always change. But it’s nice to see where we’re headed to. Nothing wrong with being FI around 65 to 70. It’s all about doing something for your financial future today.

Like always – thanks. And need less to say, you, for one, are a sure shot.

Haha I wouldn’t go as far as saying that I’m a sure shot but thank you.

Love these kind if updates and calculations. Awesome to see how close you are to financial freedom.

You continue to be an inspiration!

Thank you, I love running these simulations too. 🙂

Yep, you’re going to start running into the law of large numbers pretty quick here. Welcome to the club.

For me, big dividend growth numbers are much much harder to create. How much I scrimp and save isn’t nearly as important anymore. Dividend raises have become much more important by comparison.

It’s nice to join the club? Ha!

We definitely have to rely more and more on DRIP and organic dividend growth in the future to increase our dividend income.

You did fantastic over the last 5 years. Congratulations!

I hope you can keep it up. It will be tough, though. As you say, the law of large numbers is against you.

Can you keep adding more and more fresh capital? Also, the spreadsheet looks like the best case scenario which was accurate for the last 10 years. Can the stock market keep this up for 5 more years? The dividend could drop too. I’m just pessimistic about the stock market these days. Sorry!

Good luck and keep us updated.

Thanks Joe. It’s easy to predict the future by looking at the past numbers. But who knows what will happen in the future, nobody can predict that accurately. So yes, the spreadsheet definitely is the best case scenario. 🙂