As a DIY investor, the last two and half years have been extremely interesting. Back in February 2020, equities were firing on all cylinders and we saw all-time highs. Then the uncertainties of the global pandemic, aka COVID-19, caused the global stock market to tank. By mid-March 2020, the equity markets saw significant declines with the S&P 500 and the TSX of over 30%.

Back then, investors were freaking out and had no idea where and when the bottom would be.

To many people’s surprise, the global stock market started climbing after the mid-March 2020 low and kept climbing throughout 2021 and the first few months of 2022.

Since April of this year, the global stock market has been on a downward slide due to concerns about the high inflation rates, rising interest rates, continuing supply chain concerns, the ongoing war between Russia and Ukraine and a potentially prolonged recession

As I’ve mentioned many times on this blog, since we’re still in the accumulation phase, we have been busy saving and buying dividend paying stocks whenever we can. We are hoping the market will stay volatile and potentially bearish so we can purchase stocks at discounted prices.

I had previously reviewed our 2020 dividend stock transactions in early 2021. For me, it was an interesting exercise. It also allowed me to be transparent to readers and demonstrate how we build up our dividend portfolio.

So with that in mind, I thought it would be interesting as well as instructive to review every dividend stock transaction we’ve made between 2020 and 2022 and go over the lessons we’ve learned in the process.

Dividend Stock Sales

Since 2020, we have sold off many dividend stocks. Most of these were us simply closing our positions but we have also trimmed some of our holdings.

Please note that we prefer to hold onto our shares once we make a purchase. But from time to time, the following reasons may cause us to sell stocks:

- The stock price has stayed flat for the last few years

- No dividend increase or minimum payout increase

- Dividend cuts or suspensions

- Dividend cuts or suspensions are anticipated because of deteriorating revenues

- Fundamental change in the business and/or in its leadership.

The stocks that we sold between 2020 and 2022 were:

2020

- Dream Office REIT (D.UN)

- Evertz Technologies (ET.TO)

- Chevron (CVX)

- General Mills (GIS)

- Domtar Corp (UFS.TO)

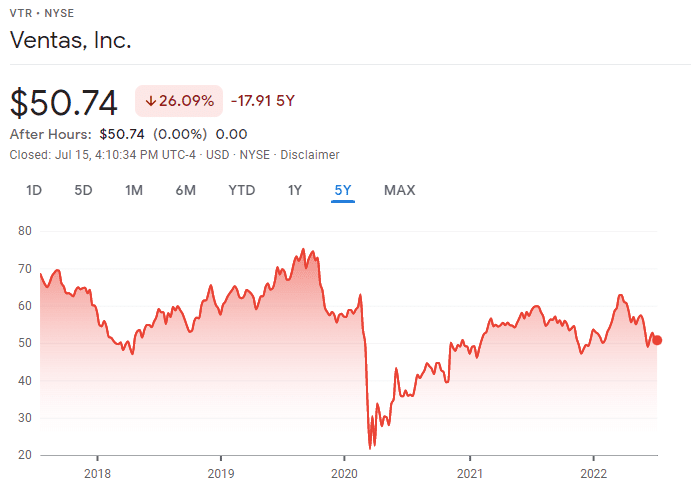

- Ventas (VTS)

- Magellan Aerospace Corp (MAL.TO)

- Laurentian Bank (LB.TO)

- Exco Technologies (XTC.TO)

- PrairieSky Royalty Ltd (PSK.TO)

We sold 110 shares of Dream Office REIT back in February when the stock was around its 52-week high. The other ten stocks we got out of the positions completely. In total, we got about $28,000 in cash from these sales.

2021

- Brookfield Property Partners (BPY.UN & BPY)

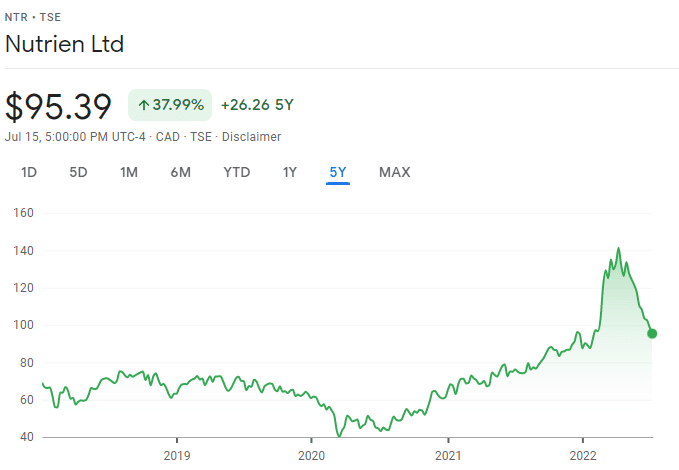

- Nutrien (NTR.TO)

- Vanguard Canada All Cap Index ETF (VCN)

- AT&T (T)

- Inter Pipeline (IPL.TO)

- Suncor (SU.TO)

- KEG Income Trust (KEG.UN)

- H&R REIT (HR.UN)

- Saputo (SAP.TO)

- Dream Office REIT (D.UN)

- Unilever (UL)

We trimmed our Suncor holding slightly and got completely out for the other stocks. We got about $78,000 from all these sales.

2022

At the time of writing, we have closed out the following position.

- Canadian Utilities (CU.TO)

We received a little shy of $9,800 from the sale.

A quick summary for spreadsheet nerds.

| Year | Ticker | Shares | Sell Price | G/L on Sale | G/L today |

| 2020 | CVX | 63 | $121.03 | Gain | Gain |

| 2020 | PSK.TO | 2 | $4.96 | Loss | Gain |

| 2020 | VTR | 16 | $27.84 | Loss | Gain |

| 2020 | D.DU | 110 | $32.89 | Gain | Loss |

| 2020 | UFS.TO | 32 | $43.72 | Loss | N/A |

| 2020 | GIS | 44 | $52.87 | Gain | Gain |

| 2020 | XTC.TO | 218 | $6.99 | Loss | Gain |

| 2020 | LB.TO | 148 | $29.52 | Loss | Gain |

| 2020 | SU.TO | 274 | $16.07 | Loss | Gain |

| 2020 | MAL.TO | 100 | $7.78 | Loss | Loss |

| 2020 | ET.TO | 103 | $17.84 | Gain | Loss |

| 2021 | BPY.UN | 52 | $22.23 | Gain | N/A |

| 2021 | BPY | 341 | $17.95 | Loss | N/A |

| 2021 | NTR.TO | 66 | $63.26 | Gain | Gain |

| 2021 | VCN | 205 | $37.70 | Gain | Gain |

| 2021 | T | 133 | $31.69 | Gain | Loss |

| 2021 | IPL.TO | 1610 | $14.65 | Loss | N/A |

| 2021 | NTR.TO | 35 | $54.89 | Gain | Gain |

| 2021 | SU.TO | 31 | $22.64 | Loss | Gain |

| 2021 | KEG.UN | 146 | $13.63 | Loss | Gain |

| 2021 | HR.UN | 425 | $22.58 | Loss | Loss |

| 2021 | SAP.TO | 96 | $36.20 | Gain | Loss |

| 2021 | D.UN | 260 | $22.39 | Loss | Loss |

| 2021 | UL | 36 | $53.15 | Gain | Loss |

| 2022 | CU.TO | 270 | $36.29 | Gain | Gain |

Notes:

1. G/L on sale indicates whether we made money or lost money in the transaction.

2. G/L today indicates if we hadn’t sold when we did but rather sold these stocks today at the writing if the transaction would have resulted in gain or loss.

As you can see from above, if we had kept some of these stocks and sold them today, we would be seeing profits rather than losses. But when it comes to investing in individual stocks, you win some and you lose some. Not to mention that we invested the money elsewhere and some of the stocks we purchased instead have returned better than if we were to keep these stocks.

Thoughts & Analyses on Dividend Stock Sales

Here are some quick thoughts and analyses on the sales we made over the last two and half years.

2020

- Dream Office REIT: We lucked out and sold 110 shares around the all-time high price.

- Evertz Technologies: We sold ET shares because the company announced a dividend cut in mid 2020 and the company didn’t increase dividend payouts for a few years. My investment thesis was incorrect with ET and it was best to get out and reinvest the money elsewhere. Looking back, we made the right choice. The lesson learned here is that before we invest in a new company, we should look at the macro environment. Furthermore, it’s important to do more research about the company and the products it sells. I’ll admit that I didn’t fully understand the broadcasting equipment and solutions business segment and how Evertz Technologies’ products & solutions play in this business segment.

- Chevron: We were trying to get out of oil producers and sold Chevron shares in early 2020, just before the market drop. Consider us lucked out on this one. I suppose we could have kept Chevron but at the time of sale, Chevron’s financials had been deteriorating for many years… crude price is very cyclical so it was probably better to get out of cyclical stocks. (although the world price for oil has zoomed up over $100/barrel, with a retreat recently)

- General Mills: Some readers were very surprised when we closed out our position in General Mills. The stock price has gone up quite a bit since we sold it. GIS was one stock that saw a steady price increase since 2020. Truth be told, we probably should have kept GIS.

- Domtar Corp: Domtar’s stock price went on a run after the March 2020 market drop. Domtar merged with another company and as a result, its stock was delisted. Shareholders received $55 USD for each share held. If we had held onto the shares for a few months longer, we would have seen a gain. But the paper industry is another industry I don’t fully understand. It was probably a good decision to sell Domtar shares because not many investors could have predicted the price run-up and the merger.

- Ventas: We sold Ventas basically at the bottom of the market. That was clearly a mistake on our part. Given that many health care facilities were under tremendous pressure early on during the pandemic, we thought our money could have been better off invested elsewhere. I’m not sure if we would have made a different decision today.

- Magellan Aerospace Corp: It was clearly a mistake to invest in Magellan Aerospace Corp in the first place. We were too focused on the dividend growth history when we purchased the stock. The current stock price hasn’t recovered from the February 2020 price.

- Laurentian Bank: We sold all LB shares after the company announced a dividend cut. Given LB was highly concentrated in Quebec and a smaller bank, we should have invested money in the Big Five or National Bank in the first place rather than paying too much attention to its dividend raise streak. A lesson learned here.

- Exco Technologies: I’ll admit that Exco Technologies is in a sector that I don’t quite understand and it was probably a mistake to invest in Exco in the first place (see the trend here?). It’s one thing to check the dividend growth streak and growth rate using the Canadian all-star list spreadsheet but it doesn’t mean we should ignore the company fundamentals and understand what the company does and how it fits in the macroenviornement. Despite selling at a loss, I believe it was a good idea to close out this position.

- PrairieSky Royalty Ltd: We received a few shares of PrairieSky Royalty Ltd from owning Canadian Natural Resources. The sale was us trying to trim the number of stocks we own.

2021

- Brookfield Property Partners: Brookfield decided to take Brookfield Property Partners private. So we decided to sell the shares prior to the closing of this transaction.

- Nutrien: Well, who could have predicted that Nurien stock price would go for a ride in the last two years? I certainly didn’t. Selling Nurien was definitely a mistake on our part. Having said that, the stock price has tumbled as of late. If this trend keeps up, the share price could very well get back to a similar price level as when we sold the stock.

- Vanguard Canada All Cap Index ETF: We decided to sell VCN because we own quite a number of the top VCN holdings already thanks to my best Canadian dividend stocks list.

- AT&T: We sold off AT&T shares because we didn’t like the spin-off WarnerMedia and the uncertainties with it. We decided to focus on a pure telecommunication company by investing in Verizon instead.

- Inter Pipeline: This was a classic case where we were chasing dividend yield and bought a whack load of IPL shares. I was very high on IPL’s Heartland project. However, I lost my confidence in the IPLs board when news that other companies were trying to acquire Inter Pipeline and the board rejected a bunch of great offers only to end up taking a not-as-good offer later on. We sold all the shares and reinvested the money elsewhere. Hindsight being 20-20, it probably would have been better if we had kept our IPL shares and waited for the Brookfield Infrastructure (BIPC) shares. That way we’d have gotten shares of another Brookfield company.

- Suncor: Like Chevron, we were trying to get out of oil producer companies. We trimmed our Suncor shares slightly after Suncor announced a surprise dividend cut. Little did we know, the crude oil price went for a run and Suncor share price jumped significantly. Would we have predicted this crude oil price run? Definitely didn’t see that coming.

- KEG Income Trust: Because KEG restaurants were closed for many months due to pandemic restrictions so the share price and dividends suffered as a result. We decided to reinvest the money elsewhere. If we look at KEG’s stock price, it hasn’t really gone anywhere so I believe it was the right move to sell KEG shares.

- H&R REIT: With many people working from home due to pandemic restrictions, we thought it was a good idea to reinvest the money elsewhere. I believe the sale was the correct call.

- Saputo: The dairy business is tougher than I thought. Furthermore, the dividend payout increase rate slowed down significantly in the last couple of years so we decided to reinvest the money elsewhere. The share price hasn’t done much since 2020.

- Dream Office REIT: We decided to sell all our Dream Office shares for the same reason as HR.UN. Looking back, we should have sold everything back in February 2020.

- Unilever: Some readers were surprised that we sold UL shares. We figured it was better to focus on other stocks in the consumer staples sector. UL’s share price hasn’t done much in the past two and half years.

2022

- Canadian Utilities: After lousy 1% dividend increases in the last couple of years, we decided to reinvest the money elsewhere, despite CU being the only dividend king in Canada.

Dividend Stock Purchases

In addition to all the sales, we made A LOT of purchases. Thanks to a relatively high savings rate, we regularly added new capital to our TFSAs, RRSPs, and taxable accounts to purchase more dividend paying stocks.

We typically max out our TFSAs in early January and make purchases in January and February. We also try to max out our RRSPs as early in the year as possible. Once we max out TFSA and RRSP, we then contribute money to taxable accounts.

We believe in time in the market rather than timing the market. Therefore, whenever we have cash, we try to invest the money right away. Another key reason we do that is that we sleep better at night if we invest the money right away rather than spread out the money. It is important to know what kind of investor you are.

We purchased the following stocks between 2020 and 2022:

2020

- Algonquin Power & Utilities Corp (AQN.TO)

- Brookfield Renewable Partners (BEP)

- Bank of Montreal (BMO.TO)

- Bank of Nova Scotia (BNS.TO)

- Brookfield Property Management (BPY)

- CIBC (CM.TO)

- Canadian National Railway (CNR.TO)

- Canadian Utilities (CU.TO)

- Enbridge (ENB.TO)

- European Residential REIT (ERE.UN)

- Granite REIT (GRT.UN)

- Inter Pipeline (IPL.TO)

- National Bank (NA.TO)

- Pepsi Co (PEP)

- Royal Bank (RY.TO)

- SmartCentres REIT (SRU.TO)

- Suncor (SU.TO)

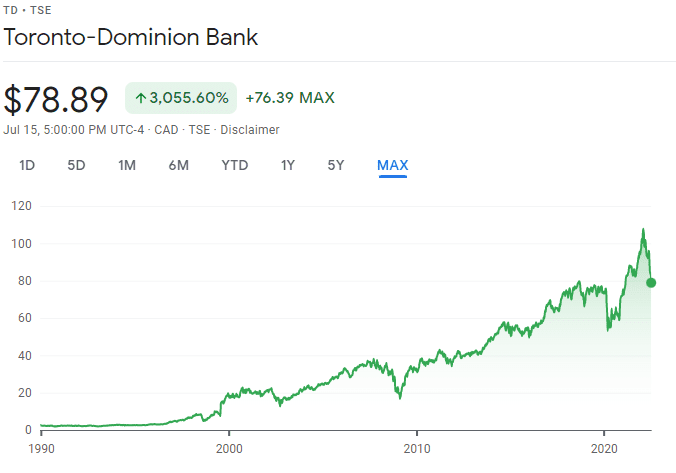

- TD (TD.TO)

- Vanguard Canada All Cap ETF (VCN)

- iShares ex-Canada international ETF (XAW)

In total we invested almost $115,000 to our dividend portfolio. Subtracting money from the 2020 sales, we added about $87,000 of new capital.

2021

- TD (TD.TO)

- Capital Power Corp (CPX.TO)

- Granite REIT (GTR.UN)

- Enbridge (ENB.TO)

- Algonquin Power & Utilities Corp (AQN.TO)

- Fortis (FTS.TO)

- iShares ex-Canada international ETF (XAW)

- TC Energy (TRP.TO)

- AbbVie (ABBV)

- Brookfield Renewable Energy (BEP.UN & BEPC)

- BCE Inc. (BCE.TO)

- Telus (T.TO)

- SmartCentres REIT (SRU.UN)

- BlackRock (BLK)

- Apple (APPL)

- Verizon (VZ)

- Bank of Nova Scotia (BNS.TO)

- Power Corp (POW.TO)

- VICI Properties (VICI)

- Bank of Montreal (BMO.TO)

- National Bank (NA.TO)

- Waste Connections (WCM.TO)

- Brookfield Asset Management (BAM.A)

- Canadian National Railway (CNR.TO)

We added around $207,000 in 2021. Subtracting money from all the sales that year, we added a total of $129,000 of new cash.

2022

- SmartCentres REIT (SRU.TO)

- Granite REIT (GRT.UN)

- Enbridge (ENB.TO)

- Algonquin Power & Utilities Corp (AQN.TO)

- Brookfield Renewable Corp (BEPC.TO)

- Apple (APPL)

- CIBC (CM.TO)

- BCE Inc (BCE.TO)

- Power Corp (POW.TO)

- Bank of Montreal (BMO.TO)

- Bank of Nova Scotia (BNS.TO)

- Costco (COST)

- iShares ex-Canada international ETF (XAW)

- Manulife Financial (MFC.TO)

So far in 2022 we have added about $83,000. Subtracting the money from the CU sale, we have added $73,200 toward our dividend portfolio. Hopefully, we can add more new cash and invest in more dividend paying stocks before this year wraps up.

A detailed summary of all of our purchases for any curious readers:

| Year | Ticker | Shares | Price | Current Price | G/L |

| 2020 | AQN.TO | 378 | $19.16 | $17.34 | Loss |

| 2020 | BEP | 100 | $45.85 | $34.21 | Loss |

| 2020 | BMO.TO | 57 | $77.63 | $118.99 | Gain |

| 2020 | BNS.TO | 102 | $53.26 | $71.42 | Gain |

| 2020 | BPY | 341 | $17.08 | N/A | Loss (Sold) |

| 2020 | BPY.UN | 52 | 12.14 | N/A | Gain (Sold) |

| 2020 | CM.TO | 232 | $37.81 | $59.80 | Gain |

| 2020 | CNR.TO | 12 | $118.29 | $145.37 | Gain |

| 2020 | CU.TO | 43 | $32.40 | $40.02 | Gain (Sold) |

| 2020 | ENB.TO | 374 | $38.72 | $53.32 | Gain |

| 2020 | ERE.UN | 450 | $4.69 | $3.31 | Loss |

| 2020 | GRT.UN | 27 | $67.11 | $74.22 | Gain |

| 2020 | IPL.TO | 453 | $22.53 | $17.73 | Loss (Sold) |

| 2020 | NA.TO | 50 | $65.54 | $83.87 | Gain |

| 2020 | PEP | 20 | $135.94 | $169.41 | Gain |

| 2020 | RY.TO | 26 | $84.60 | $120.65 | Gain |

| 2020 | SRU.UN | 121 | $31.83 | $27.25 | Loss |

| 2020 | SU.TO | 118 | $30.63 | $38.45 | Gain |

| 2020 | TD.TO | 320 | $63.11 | $77.69 | Gain |

| 2020 | VCN | 16 | $32.13 | $37.70 | Gain (Sold) |

| 2020 | XAW | 612 | $28.25 | $28.89 | Gain |

| 2021 | TD.TO | 61 | $71.99 | $77.69 | Gain |

| 2021 | CPX.TO | 144 | $34.83 | $46.15 | Gain |

| 2021 | GTR.UN | 35 | $76.65 | $74.22 | Loss |

| 2021 | ENB.TO | 212 | $44.83 | $53.32 | Gain |

| 2021 | AQN.TO | 965 | $19.87 | $17.34 | Loss |

| 2021 | FTS.TO | 249 | $50.96 | $61.35 | Gain |

| 2021 | XAW | 611 | $33.78 | $28.89 | Loss |

| 2021 | TRP.TO | 293 | $57.80 | $65.46 | Gain |

| 2021 | ABBV | 13 | $104.33 | $149.66 | Gain |

| 2021 | BEPC.TO | 337 | $48.80 | $46.05 | Loss |

| 2021 | BCE.TO | 50 | $56.89 | $63.81 | Gain |

| 2021 | T.TO | 301 | $27.89 | $28.79 | Gain |

| 2021 | BLK | 10 | $745.50 | $586.38 | Loss |

| 2021 | TRP.TO | 51 | $59.63 | $65.46 | Gain |

| 2021 | AAPL | 7 | $132.96 | $147.18 | Gain |

| 2021 | VZ | 52 | $58.44 | $50.25 | Loss |

| 2021 | BNS.TO | 23 | $80.98 | $71.42 | Loss |

| 2021 | POW.TO | 250 | $42.48 | $32.89 | Loss |

| 2021 | SRU.UN | 219 | $30.02 | $27.25 | Loss |

| 2021 | VICI | 162 | $29.29 | $31.42 | Gain |

| 2021 | BMO.TO | 15 | $132.90 | $118.99 | Loss |

| 2021 | NA.TO | 149 | $97.24 | $83.87 | Loss |

| 2021 | RY.TO | 77 | $129.79 | $120.65 | Loss |

| 2021 | WCN.TO | 50 | $169.01 | $162.74 | Loss |

| 2021 | BAM.A | 100 | $73.90 | $56.30 | Loss |

| 2021 | CNR.TO | 50 | $161.69 | $145.37 | Loss |

| 2022 | SRU.UN | 203 | $32.08 | $27.25 | Loss |

| 2022 | GRT.UN | 64 | $103.39 | $74.22 | Loss |

| 2022 | ENB.TO | 320 | $51.26 | $53.32 | Gain |

| 2022 | AQN.TO | 387 | $17.72 | $17.34 | Loss |

| 2022 | BEPC.TO | 26 | $40.43 | $46.05 | Gain |

| 2022 | AAPL | 34 | $164.72 | $147.18 | Loss |

| 2022 | CM.TO | 32 | $81.22 | $59.80 | Loss |

| 2022 | BCE.TO | 119 | $69.88 | $63.81 | Loss |

| 2022 | POW.TO | 157 | $38.64 | $32.89 | Loss |

| 2022 | BMO.TO | 61 | $146.81 | $118.99 | Loss |

| 2022 | SBUX | 10 | $87.76 | $77.58 | Loss |

| 2022 | BMO.TO | 26 | $146.07 | $118.99 | Loss |

| 2022 | BNS.TO | 25 | $81.40 | $71.42 | Loss |

| 2022 | COST | 2 | $433.88 | $507.33 | Gain |

| 2022 | CM.TO | 56 | $69.28 | $59.80 | Loss |

| 2022 | XAW | 111 | $30.14 | $28.89 | Loss |

| 2022 | MFC | 298 | 22.1 | 21.81 | Loss |

In summary, we have added $405k worth of dividend stocks or about $289k of fresh capital since 2020. To be honest, as I write this article, I am shocked at how much money we managed to deploy over the last two and half years. We are extremely grateful that we’re in a position to do this.

Please note, like our dividend income reports, we ignored the USD to CAD exchange rate so the total cash deployed is actually higher than what I have indicated.

We did really well for our purchases in 2020. However, this hasn’t been the case for purchases made in 2021 and 2022. We are currently sitting in the red for purchases made in 2021 and 2022. This is mostly caused by the current bear stock market condition. Having said that, I’m not concerned. I believe the market will eventually recover and go higher. In the meantime, we can wait and collect regular dividends.

Thoughts & Analyses on Dividend Stock Purchases

Here are some quick thoughts and analyses on our purchases from 2020 to 2022. For the sake of not repeating myself, I’ll skip stocks that we have since sold or closed out and you can check out the thoughts & analyses in the previous section.

2020

- Algonquin Power & Utilities Corp: We believe in renewable energy for the long term sustainability aspect. Obviously, AQN is facing some headwinds, given the rising interest rates environment. We plan to hold AQN for the long term and plan to continue to add more shares to dollar cost average down if possible.

- Brookfield Renewable Partners: Similar investment thesis as AQN. We think Brookfield Renewable is one of the leading renewable energy companies in Canada. This is another long term holding for us.

- Bank of Montreal: We thought the share price was greatly undervalued and it looks like we made the right decision in buying BMO shares, even with the recent price drop in 2022.

- Bank of Nova Scotia: Share price was undervalued, despite all the loan loss protections that BNS set aside. We made the right call to buy BNS shares in 2020.

- CIBC: The Canadian banks seemed undervalued throughout 2020, mostly caused by concerns about potential loan losses. We took a long term view and bought more CIBC shares. This turned out to be a very good move.

- Canadian National Railway: Goods need a way to be transported across North America. I believed CNR’s share price was undervalued when we made the purchase.

- Enbridge: Because of all the pandemic restrictions, demands for crude were extremely low, Enbridge’s share price took a hit. Since Enbridge is a long term hold for us, with a dividend yield of over 7% throughout 2020, we decided to purchase more shares. I had concerns about whether Enbridge was able to continue to pay dividends but per the free cash flow analysis, it appeared the company would be able to pay and grow dividends.

- European Residential REIT: We wanted to buy a smaller REIT thinking it might get acquired by a bigger REIT later, just as what happened with Pure Industrial REIT. So far ERE.UN hasn’t done all that great in terms of share price performance. It was a mistake for us to purchase the stock, as we looked too far ahead, and thought that we might profit from a potential acquisition. We may consider selling ERE.UN later and reinvest the money elsewhere.

- Granite REIT: After Pure Industrial REIT got acquired, we wanted to invest in another industrial REIT. Granite REIT looked like a great company, with very strong holdings.

- National Bank: Another Canadian bank that was undervalued at the time of purchase.

- Pepsi Co: We’ve wanted to invest in Pepsi for a while and finally pulled the trigger.

- Royal Bank: You can’t go wrong with Royal Bank, especially when it was yielding close to 5%. I made the mistake of selling Royal Bank shares in 2009 at $29.05 when the stock was heavily undervalued. I wasn’t going to make the same mistake twice.

- SmartCentres REIT: In the fall of 2020 we ventured out to a local shopping mall only to find it packed with shoppers, despite the trip taking place during one of the COVID waves. Despite all the different restrictions, I realized that people like to shop in physical stores. More importantly, many people congregate in shopping malls to socialize.

- TD: Another undervalued Canadian bank. Buy buy buy!

- iShares ex-Canada international ETF: We wanted to buy more XAW for diversification’s sake.

2021

- TD: I continued to believe TD was undervalued at around low $70 so we purchased more shares.

- Capital Power Corp: This was a new position for us. My original investment thoughts are in our January 2021 dividend update. Essentially we liked that Capital Power has some renewable projects under development and most of its facilities are relatively young. The dividend yield and growth rate both seemed quite attractive. This was our way to diversify in the utilities sector.

- Granite REIT: Bought more Granite REIT because we continued to like this REIT and the future growth potential.

- Enbridge: Share price remained low so we continued buying.

- Algonquin Power & Utilities Corp: Continued to average our cost basis down. I listed AQN as one of the best Canadian utility stocks, so I’m optimistic AQN’s share price will trend upward long term.

- Fortis: Since we purchased a lot of stocks in the financial sector in 2020, we wanted to increase exposure in other sectors. Fortis has a solid dividend increase streak and its dividends are almost bond like. (if Fortis raises dividend payout next year, it will become the second Canadian aristocrat king)

- iShares ex-Canada international ETF: We bought more XAW to increase our international diversification. XAW and VXC are two popular ex-Canada international index ETFs and you can’t go wrong with either one of them.

- TC Energy: Having bought quite a bit of Enbridge, we wanted to buy more TC Energy so we’re not too heavily exposed to Enbridge.

- AbbVie: AbbVie not only has a solid yield but a solid dividend growth history as well. With some US cash on hand, we purchased more ABBV shares to increase our exposure in the health care sector.

- Brookfield Renewable Energy: Continued to average down our cost basis. Renewables were very hot prior to 2020 and the market had a different view on the sector, unfortunately.

- BCE Inc: Solid yield and free cash flow covered its dividends. We were underweight in the telecommunications sector so we bought more BCE to increase the exposure.

- Telus: Same reason as BCE above.

- SmartCentres REIT: REITs remain a bit volatile but SmartCentres was one of the few REITs that didn’t cut or freeze dividends during 2020 so we remained confident that it would continue to pay and possibly raise dividends in the future.

- BlackRock: We’ve been wanting to own BlackRock for a very long time because it is the parent company of iShares ETFs. Since millions of people are buying iShares ETFs, why not invest in the parent company and profit from it? The stock was over $900 per share before it started tumbling down in early 2022. We plan to add more BlackRock shares in the future to bring down our cost average.

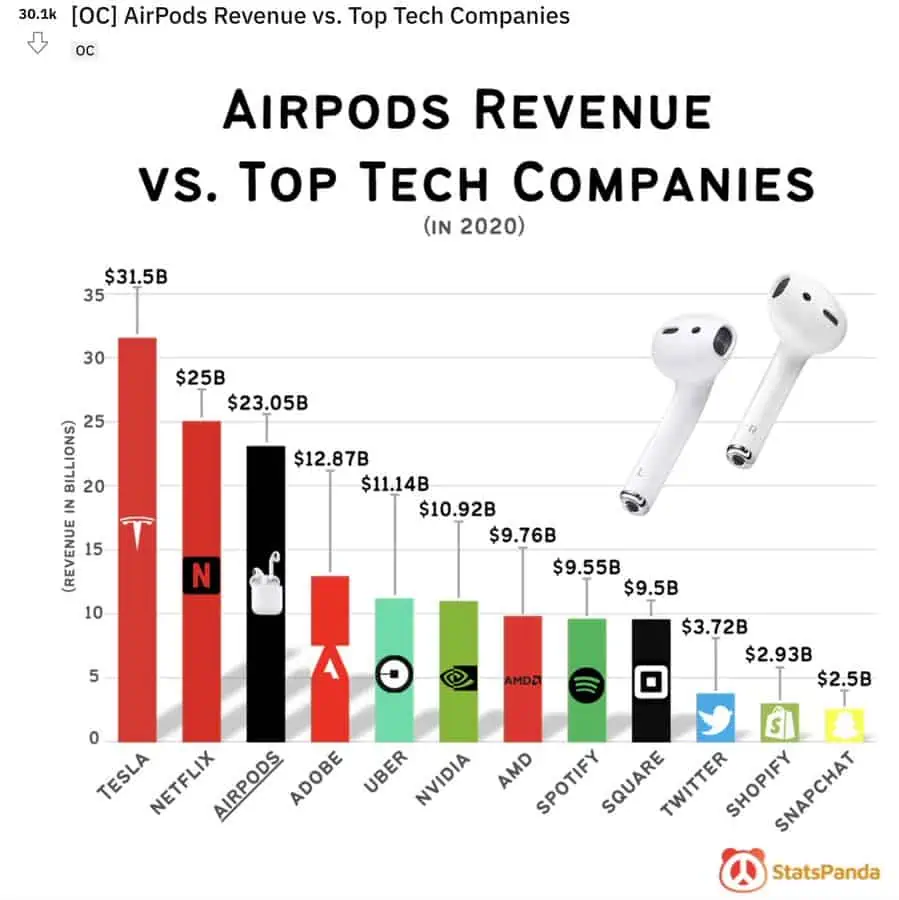

- Apple: Apple is a beast! Did you know that Apple had revenue of $23.05 billion from AirPods sales alone? The company is highly profitable and has a very strong ecosystem. However, since then, Apple’s share price has tumbled down due to concerns about the rising interest rates. Long term, I believe Apple will do just fine

- Verizon: We added more Verizon to increase our exposure in the telecommunication sector and exposure in the US as well. Looking back, $58.44 per share was probably too high of a price to pay for Verizon, given its share price was more or less flat over the last five years. Luckily, the Verizon position makes up a tiny portion of our dividend portfolio so we’ll just continue to collect dividends for the time being.

- Bank of Nova Scotia: We were a bit underweight in our BNS position so decided to buy more shares.

- Power Corp: This was a new position for us. We decided to invest in Power Corp because the company owns 60% of Canada Life, IG Wealth Management, and Mackenzie Investments. It also owns 55.9% of Wealthsimple through Power Financial, Lifeco, and IGM. Basically, we like being an owner of solid parent companies, the same reasoning behind why we purchased BlackRock.

- VICI Properties: We started a position in VICI because we like the idea that VICI will own a large portion of properties on the Las Vegas strip. With Las Vegas being a vacation destination for many people, we believe VICI would benefit from it.

- Bank of Montreal: We were underweight in the BMO position so decided to add more BMO. Unfortunately, we added shares at a relatively high price compared to the current price.

- National Bank: We added more National Bank shares because we quite like the direction of the company. Since we added shares in late 2021, the share price was quite high compared to the current price. Assuming NA doesn’t cut dividends as we face some market uncertainties, we can collect dividends in the meantime and wait.

- Waste Connections: We did really well with our investment in Waste Management. Waste Connections is WM’s equivalent in Canada. Right now we’re sitting at a paper loss for this position but I believe WCN will do just fine in the long term. We humans will continue to make garbage and someone needs to collect and dispose of it. I like the easy and simple business model it has.

- Brookfield Asset Management: BAM.A is Reader B’s favourite stock. With around $724 billion in assets under management, BAM.A is a juggernaut. The stock price has done really well since 2010 but has dropped over 26% year to date. We’re currently looking at a 23% paper loss. Ouch! It’s tough to see but we may buy more shares to bring down our cost basis. The stock has a relatively low yield, so most of the return will come from stock price appreciation. Recently, the company announced plans to spin off its asset management business, once this completes, it may drive the stock price upward. I do think that we need to pay some attention to BAM.A, especially with the rising interest rates.

- Canadian National Railway: We added more CNR toward the end of 2021 but clearly we bought shares at around the 52-week high. If the price continues to slide we will likely add more shares.

2022

- SmartCentres REIT: We bought some shares in early January with the new TFSA contribution room. The share price has dropped quite a bit but that’s fine since it would allow us to DRIP shares at a discounted price every month.

- Granite REIT: We bought more Granite shares in our TFSA with the plan to eventually enroll in a DRIP but we’re still a long way from that. Unfortunately, we basically bought these shares at a 52-week high and the share price has dropped quite a bit since. For now, we’ll probably just continue collecting dividends and wait for the share price to recover.

- Enbridge: We decided to add more Enbridge but wished we had purchased the shares below $50. If Enbridge drops down to below $50, we may add more shares.

- Algonquin Power & Utilities Corp: Same reasoning as previous AQN purchases. The stock price has been flat for a little while, allowing us to load up on more shares.

- Brookfield Renewable Corp: Same idea as AQN.

- Apple: We really like Apple but unfortunately the share price has taken a beating in 2022 due to concerns with inflation. The Apple M1 and M2 processors are significantly better than Intel processors. This leads me to believe many people will update their Macs over the next few years. Apple will continue to dominate and make billions each quarter, therefore, no we’re not worried about the stock price performance right now.

- CIBC: We decided to add some CM shares after the stock split but the share price has been on a downward trend since then, just like the overall market. As long as CIBC continues to pay dividends, we can afford to wait for the share price to recover.

- BCE Inc: It’s hard to ignore BCE’s ~5.5% dividend yield. The payout ratio is a bit high for my liking but BCE’s free cash flow can cover its dividends.

- Power Corp: Added more POW shares to bring down our cost average. The yield and dividend growth rate are pretty solid so this is another case of collecting dividends while waiting for the share price to appreciate.

- Bank of Montreal: We bought more BMO shares to increase the overall weighting in our portfolio but the share price has continued to go down since. We plan to buy more BMO shares in the future.

- Bank of Nova Scotia: BNS shares were on a downward trend so I thought it’d be a good idea to add some more. At an average cost basis of $81.40, we essentially bought shares at the late 2021 price. But the price has continued to slide since our purchases due to recession concerns. We plan to buy more BNS shares in the future.

- Costco: The stock price took a dive due to the poor results from Target and Walmart. Since Costco has a very different operating model than Target and Walmart (i.e. Costco relies on membership fees), we took advantage of the price drop and added 2 shares. Ideally, we’d love to buy more but we only had a small amount of US cash available in our RRSP at the time of the price drop.

- iShares ex-Canada international ETF: Like previous XAW purchases, we bought more XAW to increase our global diversification.

- Manulife Financial: Not sure if MFC’s share price will appreciate much over the next little while but it is hard to pass a ~6% yield.

Summary – Reviewing every dividend stock transaction between 2020 – 2022

Wow, this post turned out to be a lot longer than I anticipated (over 5,600 words!). But it has also given me the opportunity to review and analyze our sales and purchases since 2020. It is particularly interesting that most of our purchases from 2020 did quite well. But this is expected given the stock market has gone up since the mid-March 2020 low.

At one point in 2020, our portfolio dropped by over $250k. It was gut-wrenching but at the same time a good learning experience for us. Many of our purchases were in the red for most of 2020. It wasn’t until late 2020 and early 2021 that we started seeing gains with these purchases.

We’re experiencing a bit of deja vu right now as our portfolio value has dropped quite a bit so far in 2022 and many of our purchases from 2021 and 2022 have not done well. But we’ve been reminding ourselves to take a long term view, be patient, and focus on what we can control – live below our means and save and invest money regularly. At the current share prices and assuming no changes to dividends, my personal opinion is that the six Canadian banks that we hold are undervalued. Therefore, we plan to continue to buy more shares whenever we can.

Looking back, I’m surprised at how much money we managed to deploy over the last two and half years and we are very grateful that we could do that. These purchases should propel us toward our goal to live off dividends by 2025.

Dear readers, how have your stock transaction been over the last two and half years? Did you find this post useful? I’d love to hear your comments.

A magnum opus, Bob, and reassuring for many of your readers, including me. Very well done, and thank you.

Gain or loss is interesting but not super helpful.

I’d love to see if you’re beating the index on individual stock investments, or overall, or even compared to some arbitrary per annum target for returns.

I have a conservative target of 6% total return. Over the long term that’s about what I’m getting in my self-managed portfolios, and it could be argued that I should have just put it all in an index etf.

Right, it’d be interesting to compare to the index.

While I don’t leave comments for every post, I really appreciate your regular posts each week and I read them all 🙂

Your summer posts have been all very insightful and I am re reading this one and “Be Curious” one again! ☺

For someone who joined the investment scene during the pandemic, it is still very daunting to learn the tricks of the trade (e.g. financial market terminologies, reading the quarterly statements etc) So I really appreciate posts like these where you explain plainly why you bought/sold your different positions across your portfolio over time! Thanks for this long post and I hope you do this type of all-transaction review annually or semi-annually

Hi Sarah,

You’re very welcome. Glad to hear that you find my posts helpful.

Impressive Bob. I agree, you occasionally have to adjust some of your holdings to keep your process working for you even with sometimes taking losses. You can’t possibly win them all.

Obviously over the past 11 years or so, it has definitely worked with what you are doing with your approach to dividend investing. I also cut and trim as necessary as I see fit from time to time although the majority of my stocks are buy and hold and just get paid! They all start as buy and hold however with material business and economic changes we can never predict if we will ever have to sell a stock, but we must if something changes with the business that makes sense to do so.

I don’t mind downturns, I load up with more of my favorite stocks on sale and even better is the dividends are reinvested at the cheaper stock prices which just has the end result of receiving more shares in my favorite companies.

Thanks for all your posts, I enjoy seeing your progress and gives reassurance that what I do with my own investments is the right thing to do since we have very similar strategies.

Keep well,

Charles

Certianly can’t win them all but if you have more winners than losers overall, you’re still good. 🙂

We don’t mind downturns either, they give us opportunities to load up on our favourite stocks.

Appreciate your on-going support.

Excellent post. I am so nosey when it comes to other investors’ portfolios, so thank you for sharing your transactions with us all.

We can’t win all the time – although we try our hardest. As investors, we just need to be confident in the decisions we do make. In saying that, your post clearly shows the decisions you made were thoughtfully reviewed prior to execution.

Finally, what an amazing dollar amount deployed to your accounts! Wow. Very impressive.

Thank you. Haha, I know how you feel about being nosey. 🙂

I’ve been following your progress for years. What I appreciate most about your investing style is your mentality. And it is the mentality that will help you hold the course and invest over 200k in the last 2.5 years as the sole bread winner in the family. Congrats on that!

I have held pretty much the same stocks since I got out of the US market with exception to ETFs back in 2012. I think because of how defensive my portfolio is, especially my TFSA, it has allowed me to crush the market so far this year. I’m up 4.67% as of today in my TFSA and peaked at 13.07% April 20th. My trough was -3.91% June 16. Since Jan 1, 2020 until today, I’m up 59.20% total return. It’s definately above my average return over the past 10 years thanks to the crazy run in 2020 and 2021. Do you mind letting us know what your historical return has been?

Thank you Mr. Financial. Mentality is very important when it comes to investing for the long term. Congrats on your performance so far. You can take a look at our historical performance here – https://tawcan.com/dividend-portfolio-beating-the-tsx/

That’s a very impressive return over the years. It is proof that your system is working! Keep up the awesome portfolio.

I have done very little and actually added little for other reasons. I am mulling over using a LOC now to add more but with that said, considering the drop in the banks, I sold all my AQN and swapped into BNS. Since I am not adding much funds, it’s hard to just take a full position and AQN has just been going down for 2 years (before this recession).

I figure that the banks will recover faster than AQN, yeah my magic ball said so :), and they both have the same yield now. I try to keep my stock count under 25 and I have 80% of my portfolio in 15 stocks.

My taxable account is now an income account whereas the other accounts are dividend growth accounts for now.

I stopped rebalancing, I let my winners ride !!! I also don’t pay much attention to sector allocation anymore, I prefer to look at the industry as it’s more representative of the economical risk. I think the sector concept should be about defense vs offense and maybe there is a neutral type of business.

Makes sense that you have done very little since you’re further along than we are. Interesting that you sold all of your AQN and swapped into BNS. I suppose that makes sense given AQN has been going down for 2 years. Yes, Canadian banks probably will recover faster than AQN but BNS has been lagging in terms of performance compared to other Canadian banks. 🙂

Interesting point about not paying too much attention to sector allocation. Will have to consider that moving forward.

Love the transparency and candid share. Great buys! I also appreciate you sharing your reflections on your buys and sells. That’s where a lot of learning happens.

Thanks Moe.

Posts like these help me stay the course, Tawcan. This was very helpful to me in determining how I’m doing and gives me an idea on your own investment policy.

I’m not copying you but many of the stocks you mention I also own, along with XAW ETF!

Regarding your selling, as you said you win some and you lose some. Overall, you obviously did the right thing but no one can time the market and no one knows the future in advance. We can look back and with perfect hindsight may come up with what we should have done but I think it’s a trap. Make the decision and move on.

I like your approach and commend you on a very thorough and honest analysis. Good job!

Thank you very much R. Hindsight is always 20/20 but it’s important to look back and learn from both your own successes and failures. It is far better to hold solid stocks rather than inferior ones and hope they can recover. We certainly made some mistakes in the past and we will learn from them.

Quite the article. Lots of detail. It is a good analysis.

Two points.

I understand the philosophy we cant time the market….but I do think there are a number of opportunities to transition your portfolio from equities to more liquid forms of investment.

At the end of 2021 there were more and more discussions about how the markets were performing. It was a good opportunity to review your portfolio for future risk and adjust the balance of your investments. The market has gone down this year so those that held cash vs the market are doing better. Holding onto cash to find future buying opportunities is not a bad thing.

The second point is it feels like you have a lot of activity going on. I dont know how long you owned the various investments for but from my own experience in dealing with client portfolios with a lot of wealth stock turnover is relative low. Investments tend to be bought for a longer holding period with adjustments to deal with downturn in the business or sometimes just to sell some of the profits and rebalance. I just wonder if there is too many stocks in play. It isnt necessarily just the number but lets take bank stocks….how many do we need to invest in? Do we have so many we might just as well buy the market or an ETF?

Good points Brent.

I’ve seen the ups and downs of the market for many years. I believe in investing money regularly over the long term rather than trying to time the market with a load of cash. We’ve been rebalancing our portfolio each year by buying stocks that are either underweight or underperforming.

We don’t typically sell stocks so we have had more sales the last few years than we’d like. Certianly trying to keep the stock turnover to as low as possible.

Impressive analysis! I’d like to actually see what’d have happened if you have never sold any of the stocks you sold. Would you have had more money in total now or less.

I think that would be the real lesson here. To hold or to sell for a loss or a small gain! D.UN dropped significantly since then but many others gained a lot even after the recent markets meltdown.

A lot of that money we reinvested by buying Canadian banks so overall I think selling was the right decision, but a good question nonetheless.