Since 2011, Mrs. T and I have been working hard to grow our dividend portfolio so one day our dividend income and other passive income are greater or equal to our annual expenses. When this happens, we can call ourselves financially independent.

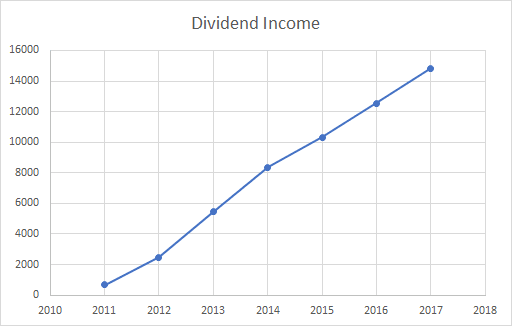

Back in 2011, we only received $675.21 in dividend income from a total of 4 dividend stocks. In 2012, we added a large amount of capital to our dividend portfolio as a result of matured GIC’s and selling a bunch mutual funds. We went from 4 dividend stocks to 26 dividend stocks and received a total of $2,484.37 in annual dividend income in 2012.

In 2013 we more than doubled our annual dividend income from $2,484.37 to $5,456.20. The number of dividend stocks in our portfolio also went from 26 to 34.

Every year, we have been consistently adding a large sum of money into our portfolio by having a high savings rate and striving for high efficiency. This has helped to grow our dividend portfolio and our dividend income.

The last 7 years looked something like this…

- 2011: $675.21, 4 dividend stocks

- 2012: $2,484.37, 26 dividend stocks

- 2013: $5,456.20, 34 dividend stocks

- 2014: $8,362.30, 53 dividend stocks

- 2015: $10,318.02, 61 dividend stocks (including 2 index ETFs)

- 2016: $12,559.74, 69 dividend stocks (including 2 index ETFs)

- 2017: $14,834.38, 74 dividend stocks (including 2 index ETFs)

- 2018: $4,133.71 so far, 72 dividend stocks (including 2 index ETFs)

So far in 2018, we have been breaking our all-time monthly dividend income every single month. Mrs. T and I are very pleased with such amazing progress. My guess is that our April dividend income will set another all-time record. Stay tuned for an updated!

Although we utilize a hybrid investing strategy by incorporating the best of dividend growth investing and index ETFs investing, lately, I have been wondering if we should consider trimming some of our dividend holdings. We’d then reinvest the money in stocks elsewhere to try to improve overall return and dividend income.

One important thing to note is that investing in dividend stocks does not mean you should only track dividend income and completely ignore the total return. Total return (i.e. stock price gain) is pretty important too.

Dividend stocks allocation for Canadians

Before we go any further, here’s a quick recap of how we allocate our dividend stocks so we can be as tax efficient as possible.

- We only own US dividend stocks and American depositary receipts (ADR) in RRSPs to avoid the 15% withholding tax.

- We hold Real Estate Income Trusts (REITs) and other income trusts in our TFSAs and RRSPs.

- We only hold dividend stocks that distribute Canadian eligible dividends in our taxable accounts.

Every year, we always maximize our TFSAs and RRSPs before we start investing in taxable accounts.

Re-examine our dividend portfolio

If you look at our dividend portfolio, you can see that we currently own 69 companies and 2 index ETFs as of the end of April 2018.

The 69 individual dividend stocks are:

- Apple (APPL)

- Pure Industrial REIT (AAR.UN)

- AbbVie (ABBV)

- BCE (BCE.TO)

- Brookfield Renewable Energy (BEP.UN)

- Bank of Montreal (BMO.TO)

- Bank of Nova Scotia (BNS.TO)

- BP PLC (BP)

- CIBC (CM.TO)

- Canadian Natural Resources (CNQ.TO)

- Canadian National Railway (CNR.TO)

- ConocoPhillips (COP)

- Costco (COST)

- Canadian Tire (CTC.A)

- Canadian Utilities (CU.TO)

- Chevron (CVX)

- Dream Office REIT (D.UN

- Dream Industrial REIT (DIR.UN)

- Dream Global REIT (DRG.UN)

- Emera (EMA.TO)

- Enbridge (ENB.TO)

- Enbridge Income Fund (ENF.TO)

- Evertz Technologies (ET.TO)

- Fortis (FTS.TO)

- General Mills (GIS)

- Hydron One (H.TO)

- High Liner Foods (HLF.TO)

- H&R REIT (HR.UN)

- Intact Financial (IFC.TO)

- Intel (INTC)

- Johnson & Jonson (JNJ)

- Keg Royalties (KEG.UN)

- Coca-Cola (KO)

- Laurentian Bank of Canada (LB.TO)

- Magellan Aerospace Corp (MAL.TO)

- McDonald’s (MCD)

- Manulife Financial (MFC.TO)

- Magna International (MG.TO)

- MCAN Mortgage Corp (MKP.TO)

- Metro (MRU.TO)

- National Bank (NA.TO)

- Nutrien (TR.TO)

- Omega Healthcare (OHI)

- Procter & Gamble (PG)

- PrairieSky Royalty Ltd (PSK.TO)

- Qualcomm (QCOM)

- Rogers Communication (RCI.B)

- RioCan REIT (REI.UN)

- Royal Bank (RY.TO)

- Saputo (SAP.TO)

- Sabra Health Care (SBRA)

- Starbucks (SBUX)

- Smart REIT (SRU.UN)

- Suncor (SU.TO)

- AT&T (T)

- Telus (T.TO)

- TD Bank (TD.TO)

- Target (TGT)

- TranCanada Corp (TRP.TO)

- Domtar Corp (UFS.TO)

- Unilever PLC (IL)

- Visa (V)

- Vodafone Group (VOD)

- Ventas Inc (VTR)

- Verizon Wireless (VZ)

- WestJet (WJA.TO)

- Waste Management (WM)

- Wal-Mart (WMT)

- Exco Technologies (XTC.TO)

And 2 index ETFs:

- Vanguard Canada All Cap (VCN.TO)

- Vanguard Global Ex-Canada (VXC.TO)

A few notes regarding stocks that we own in our dividend portfolio…

- We received Verizon Wireless shares from Verizon Wireless buying out the percentage of Verizon business that Vodafone used to own.

- We received some Suncor shares from the Canadian Oil Sand acquisition.

- Nutrien shares were from owning Potash and Agrium shares. Potash and Agrium had merged to create a new company called Nutrien.

- Sabra Health Care shares were originally called Care Capital (CCP), which were obtained from the Ventas & CCP split. Care Capital renamed the business to Sabra Health Care in 2017.

- We received some shares of PrairieSky Royalty by owning Canadian Natural Resources.

As of the end of April 2018, our forward-looking dividend is close to $19,000. This is not considering USD to CAD exchange rate. If you have been reading our monthly dividend income report, you’ll know that we use a 1:1 exchange rate to keep the math simple. In reality, if we do convert dividend income received in USD to CAD, our forward dividend income would easily be over $20,000.

The current top 5 individual dividend stocks in our portfolio are (not in order): Royal Bank, Bank of Nova Scotia, Enbridge, TD, and National Bank. As you can see, we have a large exposure to Canadian banks and the Canadian banking sector. Generally speaking, I like Canadian banks as many of them have been paying dividends since the late 1800’s. Furthermore, Canadian banks are well regulated and make a large amount of money each quarter (cue Dr. Evil… billions!). Canadians also have a low tendency to switch their banks, so the customer loyalty is pretty high.

How much money does our dividend portfolio worth? Well, you can take a wild guess by using 2% dividend yield, 3% dividend yield, 4% dividend yield, or 5% dividend yield and calculate backward using our forward-looking dividend.

That’d put our dividend portfolio value somewhere between $950,000 to $380,000. Yup, that’s a pretty wide range but I like to be ambitious here for privacy season. Regardless what our actual portfolio value is, is a sizable chunk of money.

Owning 69 dividend stocks and 2 index ETFs does offer quite a bit of sector diversification and income diversification. But perhaps we are too diversified? Are there some stocks that we can potentially sell?

Selling some stocks that might not be performing as well and reinvest the money elsewhere may provide better dividend income and better overall return.

Shuffling the deck – Selling dividend stocks

Over the last couple of years, we actually exited from a number of stocks, such as Husky Energy (HSE.TO), Kinder Morgan (KMI), Royal Dutch Shell (RDS.B), General Electric (GE), and Corus Entertainment (CJR.B). Dividend reductions or suspensions was the key reason for selling these stocks and reinvest our money elsewhere.

Are there more stocks in our dividend portfolio we can potentially sell and reinvest the money elsewhere? Here are some potential candidates:

- Sabra Health Care: As mentioned, we obtained Sabra Health Care shares from the Ventas & CCP split. We have less than 10 shares so perhaps it is not worth holding on such a small amount of shares.

- PrairieSky Royalty: same deal as Sabra Health Care. We only have a few shares of PSK.TO. The tricky part is that we own these shares in our taxable account, so we will need to report the capital gain when filing for taxes if we were to sell the stock.

- BP PLC & Chevron: the crude price has recovered from the 2016 lows and seems to be going up. As a result, BP and Chevron stock prices have recovered. The oil sector is very cyclical so perhaps it makes sense to sell both BP and Chevron and reinvest money in other sectors.

- ConocoPhillips: Similar to BP and Chevron, the stock price of ConocoPhillips has recovered from the lows of 2016. ConocoPhillips cut its dividends in 2016 and the company has only increased dividends by a very small amount since. The overall dividend yield is pretty low as a result (below 2%). By reinvesting the money elsewhere, we should be able to get higher dividend yield quite easily.

- Dream Office REIT: Dream Office REIT stock price has been suffering due to the poor office rental market in Calgary. This was mostly a result of the crude price and many energy companies in Calgary have cut back on their office spaces. Dream Office has also cut its dividends a few times in the last few years. We continued to hold onto Dream Office shares during this time despite the dividend cuts. I had thought the stock price would eventually recover and dividends would get increased again. By ditching Dream Office and invest the money in another Canadian REIT, we can probably easily increase our overall dividend income.

- Target & Wal-Mart: With Amazon getting stronger and stronger each day, I’m not fully convinced that Target and Wal-Mart will continue to be profitable. Perhaps it may make sense to sell Target and Wal-Mart when the stock prices are near the 52-week high and reinvest the money elsewhere.

Dividend stocks to consider

If we are reshuffling our dividend portfolio by exiting some positions, we will have money to reinvest somewhere else. Here are some dividend stocks we may purchase. Now some of them we already own but a few of them we currently do not own. I suppose this kind of defeats the purpose of trimming the number of holdings in our portfolio.

- Procter & Gamble (PG): The stock price has retreated over the last 3 months. PG is an international brand with a consistent dividend raise streak. It may make sense to add some shares of PG to allow us to enroll in DRIP.

- General Mills (GIS): General Mills saw a similar price trend as Procter & Gamble so far in 2018. There seems to be a general weakness in the consumer stable sector currently. It may make sense to take advantage of this general weakness by adding some General Mills shares.

- PepsiCo (PEP), Kimberly Clark (KMB), 3M (MMM), Kraft Heinsz (KHC): The price of these four stocks have been tumbling so far this year. Given these companies are big international brands currently facing some headwinds, it may make sense to take advantage of this opportunity to invest in these companies and wait for the stock price to recover.

- Emera, Canadian Utilities: We have been buying more utility stocks in the little last while. We use gas and electricity every day, so investing in utility stocks makes sense to me based on my building a dividend city logic. Having said that, we plan to keep the utility sector a small portion of our dividend portfolio. We definitely want to limit our exposure to the utility sector.

- Metro & Saputo: Both of these stocks are in the consumer staple sector and we currently own both dividend stocks. As a way to lower our exposure in the financial sector, it may make sense to invest in Metro and Saputo. Both stocks are yielding about 1.5% which is quite low. However, both stocks have extremely low payout ratios and have very strong dividend payout history.

For some reasons, most of the stocks listed are US dividend stocks. We will have to consider whether it makes sense to convert CAD to USD, given the poor exchange rate.

We also plan to continue purchasing shares of VCN and VXC to take advantage of the commission-free ETF purchase that Questrade offers.

Final Thoughts

I hope this post gave you some perspectives on what our dividend portfolio looks like and some of the things we are considering. Please remember, I am not a professional licensed investment advisor. What I have written in this post is simply personal opinions. Please do your own research and consult with a professional before you make a stock purchase.

Dear readers, do you have any thoughts on our dividend portfolio? Are you paying a close attention to any particular dividend stocks?

Hi Tawcan,

I love to hear you take advantage of stock dividends. I personally just have 8 of them so I can keep a daily watch on each of the stock’s progress, so I’m shocked at how many you have. I feel I have good diversity even with 8 stocks, so I wish you well with your pairing down. But it might be like how many pairs of shoes one is happy owning, I tend to be a minimalist.

Hi Martine,

Typically you want to have around 20-25 stocks for diversification purpose. We perhaps have a bit more than usual, that’s why we’re slowly reducing the number of stocks that we own.

Hi Tawcan,

Do you hold any bonds in your portfolio? I am in my 20’s and have a high risk tolerance. I am wondering what you think of holding bonds if you have a long term investing horizon.

Thanks

Hi Jill,

A good question. We do hold bonds but a very very small amount and they are in my work’s RRSP account. We are mostly in equities because of our long investing horizon. Besides, at the current bond yield, I might as well invest that money in dividend stocks.

Hi Bob, what do you think of BEP.UN with a negative P/E ratio right now?

Hi Aaron,

BEP.UN is a LP, so you can’t just look at them purely based on P/E ratio. You need to do an analysis similar to what you do with REITs (i.e. FFO and Price/FFO). Based on their Q1 results, FFO is $0.62 per unit, and distributions of $0.49 per unit.

From the results:

Funds From Operations per Unit of $0.62 increased 13% from the prior year.

Distributions of $0.49 per LP Unit represents an increase of 5% over the prior year.

Hi Bob, this is my first reply or question here. You’re amazing in putting mindful thoughts into words not just about your investment journey. A question as a newbie in everything in discussion here. I haven’t started investing in stocks yet as I have a heavy exposure in Real Estate. As a RE investor, I realized I have a tendency to focus only a few in one kinds. For instance, I would pick just one in Canadian banking industry. Likewise, I would pick only one or two at most in Canadian telecom industry, probably three or four in Staples..

Do you have any particular reason or rationale, specifically in bank stocks, to have all of them in your portfolio when they looks same in many aspects (if it is just to me)? Is that somehow to avoid each bank’s own risks?

Hi David,

Thank you very much for your kind words. If anything, we probably have too many holdings in our dividend portfolio right now. That’s why I’m looking to trim a few holdings. To answer your questions, why hold so many Canadian banks rather than just hold one? Because each one gives different market exposure and provides a different type of diversification. For example, TD has a large exposure in US and Canada while Bank of Nova Scotia has more of an international exposure. So by buying both TD and Bank of Nova Scotia, we are decreasing our exposure to the overall Canadian market. Hope that makes sense.

I see that you have Canadian stocks and US stocks in your RRSP. I’d like to add some US aristocrats but their dividend yield is a often less than 2%. Should we stick to Canadian stocks with their higher yield or dive into US stocks with their low yields?

That’s a personal judgement call. US stocks typically yield less than Canadian ones but US dividend stocks tend to have more international exposure and may have a slightly better overall return (obviously depends on the sector the stock is in).

Thanks for sharing, this one was interesting to read. I also need to review my holdings and my personal finance in general in the near future.

You’re welcome. It’s always worthwhile to re-examine the portfolio and see what kind of improvements we can make.

Nice report Bob,

Have you considered using XAW instead of VXC. Its foreign withholding taxes drag is smaller, and slightly lower MER. See here Justin’s comparison on the foreign withholding taxes:

https://www.canadianportfoliomanagerblog.com/war-of-the-worlds-ex-canada/

I have looked at XAW but haven’t thought about selling VXC for the sake of XAW. I don’t plan to continue selling and buying different ETFs whenever there’s a new one with slightly lower MER out there. Worthwhile to build a XAW position.

Can you make a guide on starting from scratch in 2018? Love your stuff

@Judy

I don’t think 2018 or any other year is different. You just need to start and it depends on how much money you start with. Go with Computershare if you are starting from nearly $0 and you can invest small amounts. If you have some money and can invest in the thousands, get a discount broker and start getting setup with all of the accounts properly.

When it comes to choosing stocks, as a Canadian, the Canadian Banks are the obvious bet to start with as they provide a good dividend, dividend growth, and stock appreciation. After that, it’s not so easy … Investing horizon and goals come into play.

Best of luck.

Agree with what Dividend Earner said. 🙂

Here are a few articles that I’ve written on this:

https://tawcan.com/start-dividend-investing-today/

https://tawcan.com/start-investing-dividend-paying-stocks/

Hope this helps.

Very cool Tawcan

And nice seeing the yearly process.

If i had usd id be buying 3m right now. I wouldnt sell that. Curious why cu and emera are the utilities you would sell? Got to love cu’s dividend history and at 52 week lows maybe buy instead.

I would consider selling hydro one. Its a political nightmare and hasnt done anything since its ipo…. the aquisition in the states will be good but its a coal power plant if i recall right?

Anyways im glad i sold them when i did.

Very cool post, thanks.

Cheers

I’ve been wanting to get 3M for a while now but the price is always high. Maybe this is a good opportunity.

I think you misread the article. We may want to buy more CU and Emera if we can. 🙂

Yea, have to monitor Hydro One more closely to see how things unfold.

Good idea to review the portfolio. I have rules and guidelines for how much I want per sector, and how much I want to hold within 1 holding so that pretty much sets up the grid 🙂 My target number of stocks is technically 25 and I have 26.

I like that you are thinking about total returns. For that reason, I started holding US stocks in our TFSA or non-registered. 15% of 1% yield isn’t much when you compare the potential total return of a stock like Visa against other Canadian alternatives. I have plenty of the Canadian Banks and I find the Canadian market limited … Run the numbers and ask yourself what the opportunity lost is between the total return and the 15% tax on 1% yield.

That’s very neat you have rules and guidelines on how much you want to hold per sector and per holding. I guess we don’t have hard rules and guidelines when it comes to that.

Although I don’t talk too much about total return in my monthly dividend income reports, I think total return is very important. I disagree with the idea of “who cares what the stock price is doing, the stock is yielding 5%.” Isn’t it better to have a stock yielding say 3% and gaining 5% in price at the same time?

That’s a lot of diversification. By comparison, I’m one of those crazy people that believes in ‘focus’. I own 8 different stocks, and I’m actively contemplating going down to just 6 to focus even further.

Why do you need so many? Perhaps you should adopt a policy of dropping certain stocks that don’t maintain some strict criteria of both growth and appreciation? See my post on ‘filters’. It’s important not just to buy the right ones, but to review them regularly.

I don’t know if I can stomach only holding 8 different stocks. I guess you might be OK if a couple of these are index ETFs. I like having a bit more income diversification.

Yup, definitely don’t need this many, that’s why I’ve been thinking to drop a few. But when I think about it, there are so many great companies that I’d love to own. It’s tough. 🙂

Hey Bob! You listed great combination of what you can sell to redeploy the capital. Any combination will play in a your favor. The Dream REIT is recovering very nicely. You might sell it higher later on. Good luck!

The Dream Office REIT is recovering and the company has bought back shares at $24 a few times. Would be nice if the price will go above $24.

I tend to get rid of small positions in my portfolio (or add to them). They are extra work to track and even if they do well, they would have an insignificant effect on the overall portfolio.

One correction to your article: COP has increased its dividend slightly since they cut it a few years ago. I actually sold my shares back in October as part of my own portfolio clean-up. While it looks like I should have hung onto COP a bit longer, I’m glad I’m not still hanging on to the GE shares I sold as part of that clean-up.

That’s true that smaller positions take extra work to track, that’s why we are thinking of exiting from these positions.

Good point on COP, will fix this in the article.

hey bob. i’ve been closely watching that brookfield renewable. those folks really seem to be able to run a utility well and i might start a position soon. i like visa as a future aristocrat (although i have MC as a sub). they make boatloads of cash and i could see them doubling the dividend every 4-5 years. you ever buy any preferred etf’s? they’re on sale now from par. nice portfolio.

Thanks Freddy. We might add more Brookfield Renewable, we do like the idea of invest in renewable energy. I think both Visa and MC are great investment, people are using credit cards more and more.

Haven’t really looked into preferred ETFs, probably should do that. 🙂

I own a lot of dividend stocks, many picked up during the Great Recession, and someone asked me why I didn’t buy a growth dividend fund or ETF. One of the reasons is because I liked the idea of analyzing and picking stocks, it was a responsible way to scratch that itch.

So, I wanted to pose this question to you… why own so many stocks when you could do similarly well picking a fund? 🙂

Hi Jim,

That’s a great question. I’m like you, I like the idea of analyzing and picking stocks. Also I like the idea of having the ability to determine the weighing of each stock. With index ETFs you don’t really have a choice. I elaborated a bit more in this post here

https://tawcan.com/top-canadian-dividend-etfs-dont/

We do own index ETFs, just not dividend ETFs. 🙂

Isn’t there an issue with Dividend ETFs if your plan is for future dividend income (due to fact they are constantly selling and buying to mimic the index)? Let’s say you bought 10K of each of the 10 top stocks in one of the big Canada Dividend ETFs 10 years ago and compared that to the holding the Dividend ETF (same $100K investment). Assume no dividends are reinvested. Now 10 years later, which choice would lead to the highest total cash from dividends, highest total portfolio value and highest YOC. I have this perception the ETF choice would NOT be the best choice. Just need someone to prove it for me with the calculation :)…